Global Hdac Inhibitor Drug Market

Market Size in USD Billion

USD

2.31 Billion

USD

5.43 Billion

2025

2033

USD

2.31 Billion

USD

5.43 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.31 Billion | |

| USD 5.43 Billion | |

| % | |

|

HDAC Inhibitor Drug Market Size

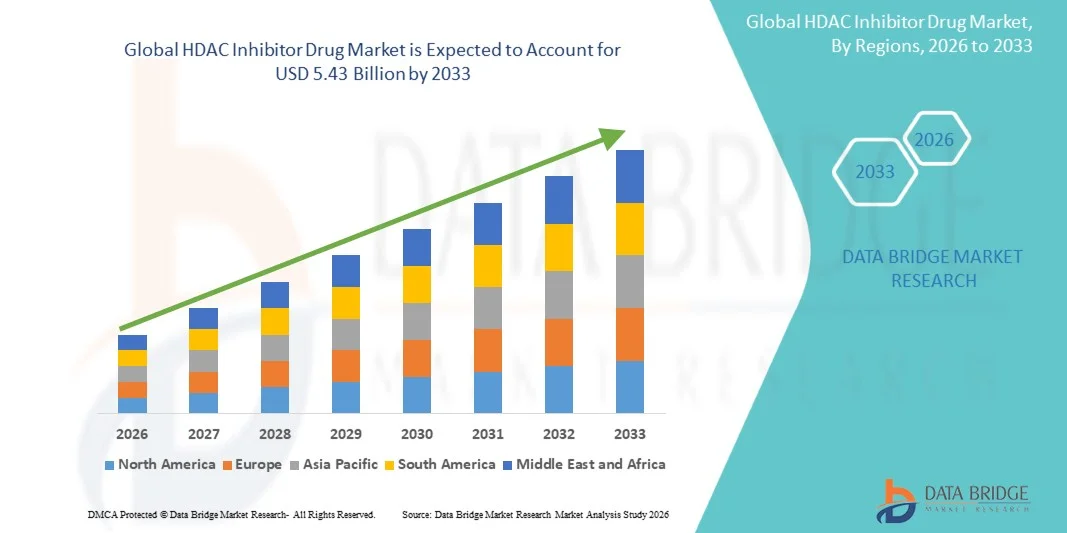

- The global HDAC inhibitor drug market size was valued at USD 2.31 billion in 2025 and is expected to reach USD 5.43 billion by 2033, at a CAGR of 11.30% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cancer and other related diseases, coupled with rapid advancements in targeted therapies and precision medicine, leading to the growing adoption of HDAC inhibitor drugs in oncology and other therapeutic areas

- Furthermore, rising demand for more effective, safer, and personalized treatment options is establishing HDAC inhibitors as a preferred therapeutic solution. These converging factors are accelerating the uptake of HDAC Inhibitor Drug solutions, thereby significantly boosting the industry's growth

HDAC Inhibitor Drug Market Analysis

- HDAC inhibitors, offering targeted modulation of histone deacetylase enzymes, are increasingly vital components of modern oncology and therapeutic regimens due to their enhanced efficacy, precision targeting, and ability to improve patient outcomes

- The escalating demand for HDAC inhibitors is primarily fueled by the growing prevalence of cancers and neurological disorders, rising focus on personalized medicine, and the need for safer and more effective treatment options

- North America dominated the HDAC Inhibitor Drug market with the largest revenue share of 42.5% in 2025, characterized by advanced healthcare infrastructure, high adoption of innovative therapies, and a strong presence of key pharmaceutical players, with the U.S. experiencing substantial growth in HDAC inhibitor drug usage across oncology centers and research hospitals

- Asia-Pacific is expected to be the fastest-growing region in the HDAC Inhibitor Drug market during the forecast period, with a projected CAGR of 14%, driven by increasing healthcare expenditure, rising incidence of cancers, and expanding adoption of novel therapies in countries such as China, Japan, and India

- The Hematologic Malignancies segment dominated with a 56.3% revenue share in 2025, due to the high efficacy of HDAC inhibitors in blood cancers, including lymphoma and multiple myeloma

Report Scope and HDAC Inhibitor Drug Market Segmentation

|

Attributes |

HDAC Inhibitor Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Roche (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

HDAC Inhibitor Drug Market Trends

“Enhanced Convenience Through Targeted Therapy and Novel Formulations”

- A significant and accelerating trend in the global HDAC Inhibitor Drug market is the growing adoption of targeted therapies and novel formulations, which enhance patient outcomes and ease of treatment administration. This trend is significantly improving treatment precision, reducing side effects, and optimizing dosing schedules

- For instance, oral and injectable HDAC inhibitors are increasingly being integrated into combination therapy protocols, allowing for more effective treatment of hematologic malignancies and solid tumors. This approach facilitates tailored therapy plans that cater to individual patient needs, improving overall treatment adherence and clinical outcomes

- Advances in formulation technology enable extended-release and less frequent dosing options, which improve patient convenience and compliance. Moreover, pharmaceutical companies are developing combination therapies that pair HDAC inhibitors with immunotherapies or chemotherapeutics, enhancing efficacy while reducing systemic toxicity

- The increasing collaboration between biotechnology firms, research institutions, and healthcare providers facilitates centralized clinical management and the development of more effective therapeutic protocols. Through these initiatives, physicians can make evidence-based decisions and closely monitor patient responses to treatment

- This trend toward more effective, patient-centric, and precise treatment options is fundamentally reshaping the expectations for oncology care. Consequently, companies are focusing on novel delivery methods, combination therapies, and expansion into new indications to meet rising patient and physician demand

- The demand for HDAC inhibitors with improved efficacy, safety, and patient compliance is growing rapidly across oncology and hematology segments, as healthcare providers increasingly prioritize outcome-driven therapies

HDAC Inhibitor Drug Market Dynamics

Driver

“Growing Need Due to Rising Cancer Incidence and Therapeutic Advancements”

- The increasing prevalence of cancer worldwide, coupled with advancements in targeted therapy and precision medicine, is a significant driver for the heightened demand for HDAC inhibitors

- For instance, in 2025, several new HDAC inhibitor formulations received regulatory approvals for treatment of hematologic cancers, expanding patient access and treatment options. Such developments are expected to drive HDAC inhibitor market growth in the forecast period

- As patients and clinicians seek more effective therapies with fewer side effects, HDAC inhibitors offer advanced benefits such as selective histone modification, tumor suppression, and synergy with combination therapies

- Furthermore, the growing awareness of personalized medicine and the integration of HDAC inhibitors into standard oncology protocols are making these drugs an essential part of modern cancer treatment

- The expansion of oncology centers, clinical trials, and improved reimbursement policies are key factors propelling HDAC inhibitor adoption globally. Rising investments in research and development for new indications and combination regimens further contribute to market growth

Restraint/Challenge

“Concerns Regarding High Costs and Regulatory Complexity”

- High treatment costs and complex regulatory approval processes pose significant challenges to broader market penetration. HDAC inhibitors often require specialized administration and monitoring, increasing overall treatment expenses for patients and healthcare systems

- For instance, In addition, stringent regulatory requirements in major markets such as the U.S., EU, and Japan can delay drug approvals, limiting timely patient access

- Addressing these challenges through enhanced clinical data, health economic studies, and strategic collaborations is crucial for market expansion. Pharmaceutical companies are increasingly offering patient assistance programs and partnering with payers to improve affordability

- The relatively high R&D costs for developing next-generation HDAC inhibitors, coupled with competitive pressures from generic formulations and biosimilars, may hinder profitability for some companies

- While market entry barriers and pricing pressures exist, the continued innovation in drug formulations, expansion into emerging markets, and focus on combination therapies are expected to sustain long-term growth of the HDAC inhibitor market

HDAC Inhibitor Drug Market Scope

The market is segmented on the basis of Type and Application.

• By Type

On the basis of type, the HDAC Inhibitor Drug market is segmented into Vorinostat, Panobinostat, Romidepsin, Belinostat, and Other HDAC inhibitors. The Vorinostat segment dominated the market with a 42.5% revenue share in 2025, due to its well-established approval for multiple hematologic malignancies and strong clinician preference. Vorinostat is widely used in the treatment of cutaneous T-cell lymphoma and other indications. Extensive clinical data support its efficacy and safety, encouraging physician adoption. The drug is also widely available through hospital pharmacies and oncology centers. Pharmaceutical companies invest in awareness programs and training for oncologists. Research studies continue to explore new indications, enhancing market confidence. Reimbursement policies in developed regions support accessibility. Its oral formulation improves patient adherence. Ongoing trials expand its potential use in combination therapies. Urban oncology centers report higher prescription rates. Partnerships with specialty pharmacies ensure consistent supply. Marketing strategies target high-volume cancer treatment hospitals.

The Panobinostat segment is expected to witness the fastest CAGR of 17.4% from 2026 to 2033, driven by growing adoption in multiple myeloma and advanced cancer treatments. Clinical trials demonstrating synergistic efficacy with proteasome inhibitors boost confidence. Pharmaceutical companies are investing in expanding global access. Increasing incidence of hematologic malignancies supports adoption. Its intravenous and oral formulations improve versatility. Expanded regulatory approvals in emerging markets drive growth. Hospitals and oncology clinics increasingly prescribe it as part of combination regimens. Patient assistance programs support affordability and adherence. Awareness campaigns educate oncologists on optimal dosing schedules. Improved supply chain logistics reduce treatment delays. Research on biomarkers enhances targeted therapy applications. Oncology conferences and professional training further promote clinical use.

• By Application

On the basis of application, the HDAC Inhibitor Drug market is segmented into Hematologic Malignancies, Solid Tumors, and Others. The Hematologic Malignancies segment dominated with a 56.3% revenue share in 2025, due to the high efficacy of HDAC inhibitors in blood cancers, including lymphoma and multiple myeloma. Hospital oncology departments prioritize these drugs for acute and refractory cases. Clinical guidelines recommend HDAC inhibitors as part of combination or second-line therapies. Strong reimbursement policies in developed markets improve patient access. Multidisciplinary oncology teams increase prescription confidence. Awareness campaigns by pharma companies enhance treatment adoption. Emerging markets show rising use due to expanding oncology infrastructure. High patient survival rates with HDAC therapy drive clinician preference. Academic research continues to validate efficacy. Urban cancer centers report higher uptake. Government initiatives to improve cancer treatment access further support growth. Partnerships with specialty pharmacies ensure steady supply of critical drugs.

The Solid Tumors segment is projected to witness the fastest CAGR of 15.8% from 2026 to 2033, driven by clinical studies showing promising activity in solid tumor types, such as lung, breast, and prostate cancers. Expanded research into combination therapies with immunotherapy fuels adoption. Hospitals and specialized oncology centers increasingly use HDAC inhibitors in clinical trial protocols. Growing incidence of solid tumors globally contributes to the market. Physician awareness programs improve prescription rates. Advanced diagnostic tools allow better patient stratification. Pharmaceutical companies invest in educational seminars and workshops. Regulatory approvals in multiple countries enhance market reach. Oral formulations improve patient compliance. Collaboration with academic research centers promotes clinical innovation. Tele-oncology programs improve access to HDAC therapies. Increasing patient demand for targeted therapies drives hospital procurement.

HDAC Inhibitor Drug Market Regional Analysis

- North America dominated the HDAC inhibitor drug market with the largest revenue share of 42.5% in 2025

- Characterized by advanced healthcare infrastructure, high adoption of innovative therapies, and a strong presence of key pharmaceutical players

- The region’s growth is further supported by high healthcare spending, widespread access to advanced diagnostic technologies, and the adoption of targeted and combination therapies

U.S. HDAC Inhibitor Drug Market Insight

The U.S. HDAC inhibitor drug market captured the largest revenue share of 83% in North America in 2025, fueled by substantial adoption of HDAC inhibitors across oncology centers, research hospitals, and specialized cancer treatment facilities. Rising incidence of hematologic malignancies and solid tumors, increased healthcare expenditure, and strong investment in clinical research and drug development are driving market growth. Moreover, early adoption of novel therapies and favorable reimbursement policies further support expansion in hospitals, specialty clinics, and multi-center clinical trials.

Europe HDAC Inhibitor Drug Market Insight

The Europe HDAC inhibitor drug market is projected to expand at a significant CAGR during the forecast period, primarily driven by the rising prevalence of cancer, increasing healthcare expenditure, and adoption of advanced therapeutic protocols. Countries such as Germany, France, and Italy are witnessing higher uptake of HDAC inhibitors in clinical trials and routine oncology treatment. In addition, government support for research, strict regulatory frameworks, and patient awareness programs are fueling market growth.

U.K. HDAC Inhibitor Drug Market Insight

The U.K. HDAC inhibitor drug market is expected to grow at a notable CAGR over the forecast period, propelled by rising incidence of hematologic cancers, increasing adoption of combination therapies, and robust R&D investments. Enhanced access to healthcare services and reimbursement policies support the growing use of HDAC inhibitors across hospitals and specialty clinics.

Germany HDAC Inhibitor Drug Market Insight

The Germany HDAC inhibitor drug market is anticipated to expand steadily, driven by strong pharmaceutical innovation, early adoption of novel therapies, and high-quality healthcare infrastructure. The country’s emphasis on precision medicine and clinical research encourages widespread HDAC inhibitor application in oncology centers, particularly in multi-specialty hospitals and research institutions.

Asia-Pacific HDAC Inhibitor Drug Market Insight

The Asia-Pacific HDAC inhibitor drug market is poised to grow at the fastest CAGR of 14% during the forecast period, fueled by increasing healthcare expenditure, rising incidence of cancers, and expanding adoption of novel therapies in countries such as China, Japan, and India. Government initiatives for cancer care, improved healthcare infrastructure, and rising patient awareness are key factors driving growth in this region.

Japan HDAC Inhibitor Drug Market Insight

The Japan HDAC inhibitor drug market is gaining momentum due to the country’s advanced healthcare system, increasing prevalence of hematologic malignancies, and focus on patient-centric therapies. The integration of HDAC inhibitors into combination treatment protocols, coupled with government-backed research initiatives, supports market expansion in hospitals and specialty clinics.

China HDAC Inhibitor Drug Market Insight

The China HDAC inhibitor drug market accounted for the largest revenue share in Asia-Pacific in 2025, driven by a growing patient population, rising healthcare spending, and increasing adoption of innovative cancer therapies. Expanding oncology centers, rising clinical trial activity, and supportive healthcare policies contribute to rapid market growth.

HDAC Inhibitor Drug Market Share

The HDAC Inhibitor Drug industry is primarily led by well-established companies, including:

• Roche (Switzerland)

• Gilead Sciences (U.S.)

• Novartis (Switzerland)

• Pfizer (U.S.)

• Merck & Co. (U.S.)

• BeiGene (China)

• Constellation Pharmaceuticals (U.S.)

• MEI Pharma (U.S.)

• Acetylon Pharmaceuticals (U.S.)

• Janssen Pharmaceuticals (Belgium)

• OncoEthix (Germany)

• TopAlliance Biopharma (China)

• Symphony Pharmaceuticals (U.S.)

• Genentech (U.S.)

• PharmaEssentia (Taiwan)

• CellDex Therapeutics (U.S.)

• Celgene (U.S.)

• Exelixis (U.S.)

• Takeda Pharmaceutical (Japan)

• Sanofi (France)

Latest Developments in Global HDAC Inhibitor Drug Market

- In March 2024, the U.S. Food and Drug Administration (FDA) approved Duvyzat (givinostat), a histone deacetylase (HDAC) inhibitor developed by Italfarmaco, for the treatment of Duchenne Muscular Dystrophy (DMD) in patients aged six years and older. This approval marked a significant expansion of HDAC inhibitor therapies beyond traditional oncology uses into a rare neuromuscular disorder, offering a new treatment option that slowed functional decline in patients with DMD

- In April 2025, the Committee for Medicinal Products for Human Use (CHMP) of the European Medicines Agency (EMA) issued a positive opinion recommending EU approval of Duvyzat (givinostat) for ambulant patients with Duchenne Muscular Dystrophy aged six years and older, paving the way for conditional marketing authorization across the European Union

- In June 2025, the European Commission granted conditional marketing authorization for Duvyzat (givinostat) in the European Union for treating ambulant patients with DMD aged six years and older when taken with corticosteroids — extending access to the first HDAC inhibitor specifically indicated for DMD in the EU and aligning with prior U.S. approval

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.