Global Healthcare Nutrition Market

Market Size in USD Billion

USD

58.35 Billion

USD

97.51 Billion

2025

2033

USD

58.35 Billion

USD

97.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 58.35 Billion | |

| USD 97.51 Billion | |

| % | |

|

Healthcare Nutrition Market Overview

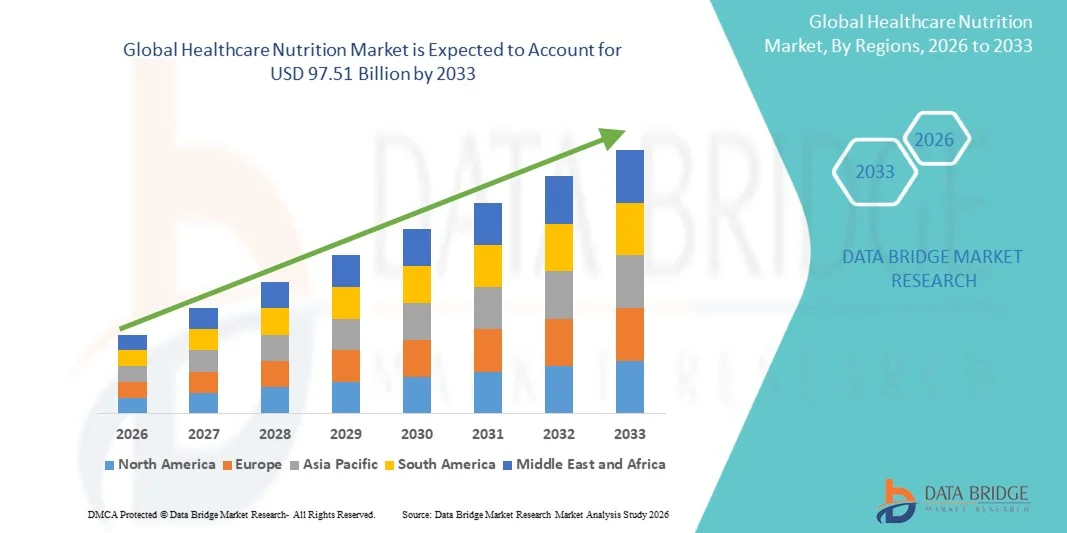

As per Data Bridge Market Research Analysis the global Healthcare Nutrition Market was valued at USD 58.35 billion in 2025 and is projected to reach USD 97.51 billion by 2033, growing at a CAGR of 6.30% from 2026 to 2033. The Healthcare Nutrition Market is witnessing steady growth driven by increasing consumer awareness regarding preventive healthcare, rising prevalence of chronic diseases, and a growing emphasis on personalized and functional nutrition solutions. Expanding aging populations across developed and emerging economies, along with higher demand for clinically supported dietary supplements, medical nutrition products, and fortified foods, is further accelerating market expansion.

The rising burden of lifestyle-related disorders such as diabetes, cardiovascular diseases, obesity, and gastrointestinal conditions is encouraging healthcare providers, hospitals, and consumers to adopt targeted nutritional interventions. In addition, advancements in nutraceutical formulations, improved bioavailability technologies, and expanding applications in clinical nutrition, sports nutrition, and pediatric and geriatric care are strengthening market adoption. Supportive regulatory frameworks and increasing integration of nutrition into mainstream healthcare systems are also contributing to the widespread use of specialized healthcare nutrition products across global markets.

Market Size & Forecast

- Global Market Value (2025): USD 58.35 Billion

- Expected Market Value (2033): USD 97.51 Billion

- Forecast CAGR (2026–2033): 6.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America dominated the Healthcare Nutrition Market with the largest revenue share of 39.26% in 2025, supported by advanced healthcare infrastructure, high adoption of clinical nutrition therapies, strong presence of leading nutraceutical companies, and increasing prevalence of chronic diseases requiring specialized nutritional support.

- The Oral segment dominated the market with a share of 30% in 2025, supported by ease of consumption, lower cost, and high patient compliance across both clinical and homecare settings.

- Asia-Pacific is expected to be the fastest-growing region, registering a CAGR of 7.2% from 2026 to 2033, driven by rising urbanization, increasing healthcare infrastructure investments, expanding middle-class population, and growing awareness of clinical and preventive nutrition in countries such as China, India, and Japan.

- The Chamber Bags segment dominated the product type category with a 38.60% revenue share in 2025, owing to their widespread use in hospital-based parenteral nutrition therapies and increasing demand for convenient, pre-formulated nutrient delivery systems.

- The Oral Route of Administration segment held the largest share of 61.30% in 2025, supported by higher patient preference, ease of consumption, cost-effectiveness, and expanding use of oral nutritional supplements in both clinical and home-care settings.

- The Diabetes application segment accounted for the largest revenue share of 28.40% in 2025, driven by the rising global prevalence of diabetes and increasing adoption of disease-specific nutritional management solutions to support glycemic control.

- The Oncology Nutrition indication segment led the market with a 26.90% share in 2025, fueled by the growing burden of cancer worldwide and the critical role of targeted nutritional support in improving treatment outcomes and patient recovery.

- The Hospitals distribution channel segment dominated the market with a 44.80% share in 2025, attributed to high patient inflow, strong reliance on clinical nutrition therapies in inpatient care, and the availability of specialized healthcare professionals for nutrition management.

Report Scope and Healthcare Nutrition Market Segmentation

|

Attributes |

Healthcare Nutrition Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

|

| Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

|

What is the Key Trend in the Healthcare Nutrition Market?

Trend: Rising Demand for Personalized and Disease-Specific Nutrition Solutions

The Healthcare Nutrition Market is witnessing a strong shift toward personalized and condition-specific nutrition products, particularly in diabetes management, oncology care, renal failure, and geriatric nutrition. Healthcare providers and nutraceutical companies are increasingly leveraging genetic profiling, microbiome analysis, and AI-driven dietary planning to develop customized nutrition regimens. For instance, Nestlé Health Science’s Persona Nutrition platform and Abbott’s disease-specific formulations such as Ensure Diabetes Care highlight the growing commercialization of personalized nutrition solutions. Hospitals across North America and Europe are also integrating clinical decision-support systems to tailor parenteral and oral nutrition therapies, improving patient recovery outcomes and reducing hospital stay durations by an estimated 10–18% in critical care settings.

Healthcare Nutrition Market Dynamics

Key Market Driver: Rising Burden of Chronic Diseases and Hospital-Acquired Malnutrition

The increasing prevalence of chronic diseases such as diabetes, cancer, cardiovascular disorders, and gastrointestinal conditions is significantly driving demand for clinical nutrition solutions. According to global health estimates, over 420 million people worldwide suffer from diabetes, while cancer incidence is projected to reach 28 million cases annually by 2040, creating sustained demand for therapeutic nutrition support.

Hospitals are increasingly adopting enteral and parenteral nutrition therapies to combat malnutrition in ICU and post-surgical patients, where malnutrition rates can exceed 30–50% in critical care units. Companies like Fresenius Kabi, B. Braun, and Baxter International are expanding their intravenous nutrition portfolios to meet this rising clinical demand, particularly in intensive care and oncology wards.

Key Restraint/Challenge: High Cost of Clinical Nutrition Products and Limited Reimbursement in Emerging Economies

A major challenge in the healthcare nutrition market is the high cost of specialized nutrition therapies, particularly parenteral nutrition and disease-specific medical formulas. Advanced formulations containing amino acids, lipid emulsions, and trace elements require stringent manufacturing standards, significantly increasing product costs.

In developing regions such as parts of Asia-Pacific and Africa, reimbursement coverage for medical nutrition therapy remains limited, with out-of-pocket expenditure accounting for over 60% of total healthcare nutrition spending in some markets. This restricts adoption among lower-income patient populations and limits penetration in rural healthcare systems. In addition, cold-chain storage requirements for certain lipid emulsions and injectable nutrition products further increase operational costs for hospitals and pharmacies.

Key Market Opportunity: Expansion of Home-Based Clinical Nutrition and Digital Health Integration

A major growth opportunity lies in the expansion of home healthcare nutrition and digital monitoring solutions. Increasing demand for post-discharge nutritional support is driving adoption of home enteral nutrition (HEN) and oral nutritional supplements. Companies such as Danone (Nutricia Homeward program) and Abbott’s home nutrition services are enabling patients to receive long-term nutritional therapy outside hospital settings, reducing healthcare costs by up to 25–35% compared to inpatient care. Furthermore, the integration of digital health platforms, remote monitoring devices, and AI-based diet tracking apps is enhancing adherence and outcomes in chronic disease management. The expansion of e-commerce distribution channels for nutritional supplements in regions like Asia-Pacific (projected CAGR ~7–8%) is also opening new revenue streams for manufacturers

Healthcare Nutrition Market Scope

The Healthcare Nutrition market is segmented on the basis of type, product type, route of administration, application, indication, and distribution channel.

- By Type

On the basis of type, the Healthcare Nutrition Market is segmented into Paediatric Nutrition, Parenteral Nutrition, Elderly Nutrition, and Sport Nutrition. The Elderly Nutrition segment dominated the market with a revenue share of 40.15% in 2025, driven by the rapidly expanding geriatric population worldwide, increasing prevalence of age-related disorders, and rising demand for specialized formulations supporting immunity, bone health, and cognitive function. Growing life expectancy and higher hospitalization rates among elderly patients further strengthen demand for clinical nutritional support across hospitals and homecare settings. In addition, companies such as Nestlé Health Science and Danone Nutricia are expanding geriatric-focused product portfolios, enhancing market penetration. Government healthcare programs supporting aging populations in Europe, Japan, and North America also contribute significantly to segment dominance.

The Paediatric Nutrition segment is expected to register the fastest CAGR of 6.8% from 2026 to 2033, driven by rising cases of childhood malnutrition, low birth weight complications, and increasing awareness of early-life nutritional interventions. Expanding neonatal intensive care units (NICUs) and growing adoption of fortified infant formulas are further supporting growth. Emerging economies such as India, Brazil, and Southeast Asian countries are witnessing strong demand due to improving maternal and child healthcare programs. In addition, product innovations in hypoallergenic and probiotic-enriched infant formulas are enhancing clinical outcomes. Rising partnerships between healthcare institutions and nutrition companies are further accelerating segment expansion globally.

- By Product Type

On the basis of product type, the market is segmented into Amino Acid Solution, Multiple Vitamins and Antioxidants, Lipid Emulsion, Trace Elements, and Chamber Bags. The Chamber Bags segment dominated the market with a share of 38.60% in 2025, owing to its extensive use in parenteral nutrition therapies within hospital settings. These pre-mixed nutrient delivery systems ensure sterility, accuracy, and ease of administration, making them highly preferred in intensive care and surgical recovery units. Rising ICU admissions and growing demand for ready-to-use intravenous nutrition solutions further strengthen segment leadership. Hospitals prefer chamber bags due to reduced contamination risk and improved clinical efficiency. Major players like Fresenius Kabi and Baxter continue expanding production capacities to meet rising demand.

The Lipid Emulsion segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by increasing use in energy-dense parenteral nutrition formulations for critically ill and cancer patients. Lipid emulsions play a vital role in providing essential fatty acids and caloric support in patients unable to consume oral nutrition. Advancements in omega-3 based lipid formulations and improved emulsification technologies are enhancing therapeutic outcomes. Rising oncology cases and postoperative recovery needs are further fueling demand. In addition, growing ICU nutrition protocols in developed and emerging markets are significantly accelerating adoption.

- By Route of Administration

On the basis of route of administration, the market is segmented into Parenteral and Oral nutrition. The Oral segment dominated the market with a share of 61.30% in 2025, supported by ease of consumption, lower cost, and high patient compliance across both clinical and homecare settings. Oral nutritional supplements are widely used in diabetes, oncology, and geriatric care for long-term dietary management. Increasing awareness of preventive healthcare and availability of flavored, disease-specific formulations are further driving adoption. Retail expansion and strong e-commerce penetration have also improved accessibility. Companies like Abbott and Nestlé dominate this segment through brands such as Ensure and Boost.

The Parenteral segment is expected to register the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing ICU admissions, surgical procedures, and cases of severe gastrointestinal disorders. Parenteral nutrition is essential for patients who cannot absorb nutrients orally, particularly in oncology and critical care settings. Advancements in sterile manufacturing, multi-chamber systems, and lipid-based formulations are improving safety and efficacy. Rising hospital infrastructure investments and expansion of critical care units in Asia-Pacific and Latin America are further boosting demand. In addition, growing adoption of home-based parenteral nutrition programs is supporting long-term growth.

- By Application

On the basis of application, the market is segmented into Paediatric Malnutrition, Gastrointestinal Diseases, Renal Failure, Cancer, Pulmonary Diseases, Diabetes, and Neurological Diseases. The Diabetes segment dominated the market with a share of 28.40% in 2025, driven by the rising global diabetic population and increasing demand for glycemic-control nutritional formulations. Specialized diabetes nutrition products help manage blood sugar levels and reduce complications, making them widely recommended in clinical care. Increasing obesity rates and sedentary lifestyles are major contributing factors. Hospitals and homecare providers increasingly recommend diabetes-specific supplements as part of long-term disease management strategies. Companies like Abbott and Danone have developed dedicated diabetes nutrition portfolios to support this demand.

The Cancer segment is expected to register the fastest CAGR of 7.3% from 2026 to 2033, driven by rising global cancer incidence and increasing importance of nutritional support during chemotherapy and recovery phases. Oncology nutrition helps improve immunity, reduce treatment side effects, and enhance patient survival outcomes. Expanding oncology treatment centers and increasing integration of nutritional therapy in cancer care protocols are supporting growth. Governments and healthcare systems are increasingly recognizing clinical nutrition as a key component of cancer treatment. In addition, innovations in immune-boosting and high-protein formulations are further driving adoption.

- By Indication

On the basis of indication, the market is segmented into Hepatic Disorders, Renal Disorders, Diabetes, Dysphagia, Oncology Nutrition, Neurology Nutrition, and Others. The Oncology Nutrition segment dominated the market with a share of 26.90% in 2025, driven by the increasing global cancer burden and critical need for nutritional intervention during treatment cycles. Cancer patients often experience severe malnutrition, requiring specialized formulations to support recovery and immunity. Hospitals and oncology centers widely adopt enteral and parenteral nutrition support systems. Rising chemotherapy and radiotherapy procedures further strengthen demand. Key players are expanding oncology-focused nutrition portfolios globally.

The Dysphagia segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by increasing prevalence among elderly populations and patients with neurological disorders such as stroke and Parkinson’s disease. Dysphagia nutrition products are designed to ensure safe swallowing and adequate nutrient intake. Growing geriatric population and rising post-stroke rehabilitation cases are significantly contributing to demand. Hospitals and long-term care facilities are increasingly adopting thickened liquid formulations. Awareness programs and improved diagnosis rates are also accelerating market growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospitals, Compounding Pharmacy, Retail Pharmacy, and E-Commerce Websites. The Hospitals segment dominated the market with a share of 44.80% in 2025, owing to high patient inflow, strong reliance on clinical nutrition therapies, and availability of specialized healthcare professionals. Hospitals are the primary point of administration for parenteral and enteral nutrition, especially in ICU and surgical care. Increasing hospitalization rates due to chronic diseases further support dominance. Strong procurement systems and bulk purchasing agreements with manufacturers also reinforce this segment.

The E-Commerce Websites segment is expected to register the fastest CAGR of 7.4% from 2026 to 2033, driven by rising digital health adoption and increasing consumer preference for home-based nutritional solutions. Online platforms provide easy access to oral nutritional supplements, vitamins, and disease-specific formulas. Expanding internet penetration and mobile health applications in Asia-Pacific and Latin America are accelerating growth. Direct-to-consumer sales models by companies like Abbott and Nestlé are further boosting online distribution. In addition, subscription-based nutrition delivery services are gaining strong traction globally.

Healthcare Nutrition Market Regional Analysis

North America dominated the Healthcare Nutrition market and accounted for the largest revenue share of 39.26% in 2025, supported by advanced healthcare infrastructure, high adoption of clinical nutrition therapies, strong presence of leading nutraceutical and pharmaceutical companies, and increasing prevalence of chronic diseases such as diabetes, cancer, and renal disorders requiring specialized nutritional support. The region also benefits from well-established reimbursement systems, high awareness of medical nutrition therapy, and strong integration of nutrition into hospital care protocols. Increasing demand for personalized nutrition, home-based clinical nutrition, and disease-specific formulations continues to strengthen North America’s leadership position in the global market.

U.S. Healthcare Nutrition Market Insight

The U.S. Healthcare Nutrition market is witnessing strong growth due to rising prevalence of chronic diseases, increasing healthcare expenditure, and strong adoption of advanced clinical nutrition solutions. The country has a highly developed hospital infrastructure and strong presence of key players such as Abbott, Baxter International, and Nestlé Health Science, which is driving innovation in oral, enteral, and parenteral nutrition products. Growing use of disease-specific nutritional formulas for diabetes, oncology, and critical care patients is further supporting market expansion. In addition, rising awareness of preventive healthcare and expanding home healthcare services are accelerating demand across both hospital and retail channels.

Europe Healthcare Nutrition Market Insight

The Europe Healthcare Nutrition market remains a significant contributor to global revenue, driven by strong public healthcare systems, increasing aging population, and rising incidence of chronic diseases. The region demonstrates high adoption of clinical nutrition therapies in hospitals and long-term care facilities, particularly in countries such as Germany, France, Italy, and the U.K. Strong regulatory frameworks supporting medical nutrition therapy and increasing integration of nutrition into standard treatment protocols are further boosting demand. In addition, growing investments in personalized nutrition and preventive healthcare initiatives continue to support regional market growth.

U.K. Healthcare Nutrition Market Insight

The U.K. Healthcare Nutrition market is experiencing steady growth, supported by rising prevalence of malnutrition in hospitalized patients and increasing awareness of clinical nutrition benefits. The National Health Service (NHS) plays a key role in driving adoption of oral nutritional supplements and enteral feeding solutions across hospitals and community care settings. Growing focus on elderly care, cancer support nutrition, and post-surgery recovery programs is further contributing to market expansion. In addition, increasing availability of advanced nutritional products through retail pharmacies and e-commerce channels is improving accessibility across the country.

Germany Healthcare Nutrition Market Insight

The Germany Healthcare Nutrition market is expanding steadily due to a strong healthcare system, high geriatric population, and advanced pharmaceutical manufacturing capabilities. Hospitals and care facilities increasingly rely on parenteral and oral nutrition therapies for managing chronic diseases and post-operative recovery. Germany also has a strong presence of global players such as Fresenius Kabi and B. Braun, which are continuously innovating in clinical nutrition formulations. Rising demand for specialized nutrition in oncology and renal care, along with strong regulatory support, is further driving market growth in the country.

Asia-Pacific Healthcare Nutrition Market Insight

The Asia-Pacific Healthcare Nutrition market is expected to witness rapid growth, driven by rising healthcare expenditure, increasing prevalence of malnutrition, and growing burden of chronic diseases across countries such as China, India, and Japan. Expanding hospital infrastructure, improving access to healthcare services, and increasing awareness of clinical nutrition are significantly boosting demand. The region is also witnessing strong growth in oral nutritional supplements due to affordability and ease of use. In addition, rising penetration of multinational nutrition companies and growing e-commerce distribution are further accelerating market expansion.

Japan Healthcare Nutrition Market Insight

The Japan Healthcare Nutrition market is witnessing consistent growth due to its rapidly aging population and high prevalence of age-related disorders requiring specialized nutritional care. The country has a strong healthcare system with advanced hospital infrastructure that widely adopts clinical nutrition therapies, particularly for elderly and post-surgical patients. Increasing demand for functional foods, oral nutritional supplements, and disease-specific formulas is further supporting growth. In addition, strong focus on preventive healthcare and innovation in medical nutrition products continues to strengthen Japan’s market position.

China Healthcare Nutrition Market Insight

The China Healthcare Nutrition market is growing rapidly, driven by rising urbanization, increasing healthcare awareness, and expanding burden of chronic diseases such as diabetes and cancer. Government initiatives supporting nutrition improvement and hospital modernization are significantly boosting adoption of clinical nutrition therapies. Strong growth in both hospital-based and retail nutritional products is also supported by expanding middle-class income levels. In addition, increasing presence of global and domestic nutrition companies, along with rapid growth of e-commerce platforms, is enhancing accessibility and accelerating market expansion across the country.

Which are the Top Companies in Healthcare Nutrition Market?

The Healthcare Nutrition industry is primarily led by well-established companies, including:

- Abbott Laboratories (U.S.)

- Nestlé S.A. (Switzerland)

- Danone S.A. (France)

- Baxter International Inc. (U.S.)

- Fresenius Kabi AG (Germany)

- Mead Johnson Nutrition (Reckitt Benckiser Group plc, U.K.)

- Nutricia (Danone S.A., France)

- B. Braun Melsungen AG (Germany)

- Archer Daniels Midland Company (U.S.)

- Glanbia plc (Ireland)

- Herbalife Nutrition Ltd. (U.S.)

- Amway Corporation (U.S.)

- Meiji Holdings Co., Ltd. (Japan)

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Fresenius SE & Co. KGaA (Germany)

- Lonza Group AG (Switzerland)

- Kerry Group plc (Ireland)

- Cargill Incorporated (U.S.)

- BASF SE (Germany)

- DSM-Firmenich AG (Switzerland)

- Ajinomoto Co., Inc. (Japan)

- Yakult Honsha Co., Ltd. (Japan)

- Blackmores Limited (Australia)

- Haleon plc (U.K.)

- Pfizer Inc. (U.S.)

- Sanofi S.A. (France)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Reckitt Benckiser Group plc (U.K.)

- Amneal Pharmaceuticals Inc. (U.S.)

- Stada Arzneimittel AG (Germany)

- Pharmavite LLC (U.S.)

- Swisse Wellness Pty Ltd (Australia)

- Zydus Lifesciences Ltd. (India)

- Cipla Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Sun Pharmaceutical Industries Ltd. (India)

- Nestlé Health Science (Switzerland)

Latest Developments in Healthcare Nutrition Market

- In May 2025, Danone acquired a majority stake in Kate Farms, a U.S.-based medical nutrition company specializing in plant-based enteral nutrition formulas and oral nutritional supplements. The acquisition strengthens Danone’s presence in the high-growth clinical nutrition segment, particularly in hospital and homecare settings across the United States. Kate Farms’ products are widely used in pediatric care, oncology nutrition, and tube-feeding applications, addressing increasing demand for plant-based and allergen-free medical nutrition solutions. This move reflects the broader industry shift toward clean-label, sustainable, and disease-specific nutritional therapies in global healthcare systems

- In September 2024, Nutricia (Danone) launched its reformulated Nutrison core range tube feeds at the ESPEN Congress on Clinical Nutrition and Metabolism in Milan. The updated formulation focuses on improved protein quality, better digestibility, and enhanced nutritional density for critically ill and long-term care patients. This launch strengthens Nutricia’s position in hospital nutrition across Europe and supports increasing clinical adoption of evidence-based enteral feeding solutions. It also reflects ongoing innovation in hospital nutrition therapy driven by aging populations and rising chronic disease burden

- In January 2024, Nestlé collaborated with the World Economic Forum’s Global Shapers initiative and Accenture to support youth-led innovation in nutrition and health science. The partnership aims to accelerate innovation in food-as-medicine solutions, including personalized and preventive healthcare nutrition models. This collaboration reflects Nestlé’s broader strategy to strengthen its leadership in medical nutrition and health science innovation. It also highlights the growing convergence of digital health, AI, and clinical nutrition ecosystems globally

- In November 2023, Nestlé launched its Sinergity 6-HMO infant nutrition formula in Hong Kong, designed to closely mimic the structure of human breast milk. The product contains six human milk oligosaccharides (HMOs) and probiotic strains to support infant immunity, digestion, and microbiome development. This innovation represents a major advancement in infant medical nutrition, reinforcing Nestlé’s leadership in early-life nutritional science. The launch reflects rising demand for bioengineered, breast-milk-like formulas in global infant nutrition markets

- In May 2025, Danone announced strong growth in its specialized nutrition division, driven by rising demand for medical nutrition products in China and other Asia-Pacific markets. The company reported robust performance in infant formula and clinical nutrition segments, supported by increasing hospital demand and improving healthcare access. This development highlights Asia-Pacific’s growing importance in global healthcare nutrition consumption, particularly in hospital-based and preventive nutrition categories

- In March 2026 (reflecting 2025 strategic expansion), Danone agreed to acquire Huel, a UK-based plant-based complete nutrition company. Huel specializes in nutritionally complete meal replacements and protein-rich formulations targeting health-conscious consumers and clinical nutrition users. The acquisition strengthens Danone’s position in the fast-growing complete nutrition and medicalized consumer nutrition segment. It also reflects increasing convergence between consumer nutrition and clinical healthcare nutrition markets globally

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.