Global Heart Block Treatment Market

Market Size in USD Billion

USD

3.90 Billion

USD

7.71 Billion

2024

2032

USD

3.90 Billion

USD

7.71 Billion

2024

2032

| 2025 - 2032 | |

| USD 3.90 Billion | |

| USD 7.71 Billion | |

| % | |

|

Heart Block Treatment Market Size

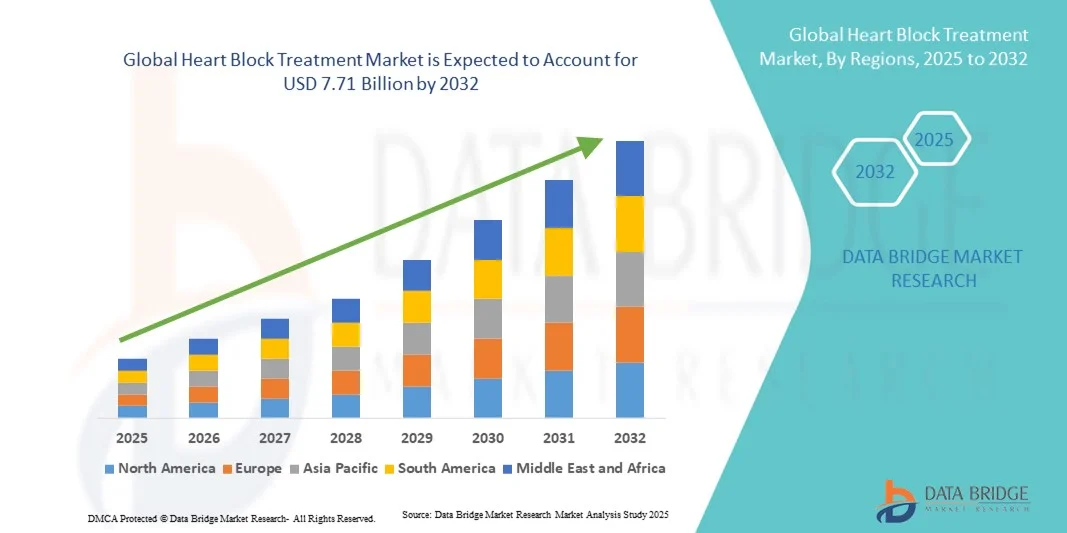

- The global heart block treatment market size was valued at USD 3.90 billion in 2024 and is expected to reach USD 7.71 billion by 2032, at a CAGR of 8.90% during the forecast period

- The market growth is largely fueled by increasing prevalence of cardiovascular disorders, rising awareness of early diagnosis, and growing adoption of advanced cardiac care solutions across hospitals and clinics

- Furthermore, the development of minimally invasive treatment options, coupled with expanding access to specialized cardiology services, is accelerating the uptake of Heart Block Treatment solutions, thereby significantly boosting the industry's growth

Heart Block Treatment Market Analysis

- Heart Block Treatment, encompassing pharmacological and device-based interventions, is critical for managing arrhythmias and complications associated with heart conduction abnormalities in both pediatric and adult patients, due to its effectiveness in stabilizing cardiac function and improving patient outcomes

- The rising prevalence of cardiovascular disorders, increasing awareness among clinicians, and advancements in treatment protocols are driving the demand for Heart Block Treatment globally

- North America dominated the heart block treatment market with the largest revenue share of 35% in 2024, characterized by advanced healthcare infrastructure, high clinician awareness, and the strong presence of key pharmaceutical and medical device companies, with the U.S. experiencing substantial growth in heart block treatment adoption, particularly in hospital-based protocols and emergency care settings

- Asia-Pacific is expected to be the fastest-growing region in the heart block treatment market during the forecast period, projected to register a CAGR driven by rising cardiovascular disorders, expanding hospital networks, increasing investments in healthcare infrastructure, and greater access to advanced treatment options in countries such as China, India, and Japan

- The Pacemaker segment dominated the heart block treatment market with the largest market revenue share of 41.3% in 2024, owing to its critical role in restoring normal heart rhythm in patients with severe heart block

Report Scope and Heart Block Treatment Market Segmentation

|

Attributes |

Heart Block Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Heart Block Treatment Market Trends

Enhanced Patient Care and Access to Advanced Therapies

- A significant and accelerating trend in the global heart block treatment market is the increasing availability of advanced therapeutic options and comprehensive patient management programs. These developments are improving patient outcomes, accessibility, and overall treatment convenience

- For instance, in 2023, certain hospitals in North America introduced integrated treatment programs combining device implantation, pharmacological therapy, and continuous patient monitoring, providing a streamlined approach to managing heart block conditions

- Recent advances in device technology, such as improved pacemakers and implantable cardiac monitors, enable better regulation of heart rhythms and more personalized care. For instance, some devices now offer real-time monitoring capabilities that alert physicians to arrhythmias, allowing timely intervention

- The growing focus on patient-centered care and structured follow-up programs facilitates coordinated management of heart block across multiple healthcare providers. Through these programs, patients receive regular assessments, therapy adjustments, and lifestyle guidance, improving adherence and long-term outcomes

- This trend towards more effective, accessible, and integrated treatment solutions is reshaping expectations for heart block management. Consequently, healthcare providers and medical device companies are developing advanced treatment options with improved reliability, safety, and clinical efficacy

- The demand for such comprehensive care solutions is growing rapidly across hospitals, cardiac clinics, and outpatient care settings, as patients and healthcare providers increasingly prioritize treatment effectiveness, accessibility, and continuity of care

Heart Block Treatment Market Dynamics

Driver

Growing Need Due to Rising Cardiovascular Incidences and Technological Advancements

- The increasing prevalence of cardiovascular conditions, including heart block, coupled with rising awareness among patients and healthcare professionals, is a significant driver of demand for advanced therapies

- For instance, in April 2024, a leading medical center in Europe launched a dedicated cardiac arrhythmia program, integrating pacemaker implantation, remote monitoring, and patient education. Such initiatives by key healthcare providers are expected to drive Heart Block Treatment market growth during the forecast period

- As patients and clinicians recognize the importance of early intervention, advanced therapies offer improved rhythm management, fewer complications, and enhanced quality of life

- Furthermore, the growing adoption of minimally invasive procedures and device-based therapies is expanding treatment options and making management of heart block more effective and convenient

- The availability of structured patient care programs, continuous monitoring, and follow-up ensures higher adherence to therapy, which is propelling adoption across hospital and outpatient care settings

- Increasing investments by healthcare providers in modern treatment infrastructure and the rising number of clinical awareness campaigns further support market growth

Restraint/Challenge

High Treatment Costs and Limited Accessibility in Certain Regions

- The relatively high cost of advanced heart block therapies and implantable devices can restrict adoption, particularly in developing countries or among price-sensitive patient populations

- For instance, specialized pacemaker implantation procedures in parts of Southeast Asia remain limited due to high device costs and the need for trained cardiologists, creating barriers for widespread adoption

- Limited accessibility to specialized healthcare facilities in rural and remote regions can delay diagnosis and intervention, impacting patient outcomes

- High out-of-pocket expenses and insurance coverage limitations also hinder the uptake of advanced therapies, especially where reimbursement policies are restrictive

- While the cost of basic pacemaker therapies is gradually decreasing, premium devices with advanced monitoring features often remain expensive for many patients

- Overcoming these challenges through expanded healthcare infrastructure, improved insurance coverage, patient education, and cost-effective treatment solutions will be vital for sustained market growth

- In addition, shortage of trained cardiologists and specialized medical staff in certain regions limits the ability to perform complex procedures or manage post-implantation care, creating further adoption barriers

Heart Block Treatment Market Scope

The market is segmented into four notable segments based on type, treatment, end-users, and distribution channel.

- By Type

On the basis of type, the heart block treatment market is segmented into first-degree heart blocks, second-degree heart blocks, left bundle branch block, right bundle branch block, third-degree heart blocks, and others. The second-degree heart blocks segment dominated the largest market revenue share of 38.7% in 2024, driven by its high prevalence among patients requiring cardiac monitoring and intervention. Hospitals and specialty clinics often prioritize treatment for second-degree blocks due to the risk of progression to complete heart block and potential complications. The segment benefits from established clinical protocols, widespread awareness among cardiologists, and availability of effective interventions such as pacemakers and transcutaneous pacing. Its dominance is also supported by strong insurance coverage, inclusion in hospital treatment guidelines, and frequent hospital admissions for symptomatic cases. Increasing awareness of early diagnosis and timely treatment among clinicians further bolsters this segment. The demand is particularly high in North America and Europe, where advanced healthcare infrastructure facilitates rapid diagnosis and treatment. Second-degree heart blocks are commonly observed in both adult and pediatric populations, emphasizing the segment’s clinical importance. Overall, consistent hospital usage, strong clinical outcomes, and high-risk management contribute to the leading revenue share of this segment.

The Left Bundle Branch Block segment is anticipated to witness the fastest CAGR of 22.1% from 2025 to 2032, fueled by rising awareness of its association with heart failure, improved diagnostic capabilities, and increasing adoption of device-based therapies. Advances in electrophysiology and implantable devices are enhancing patient outcomes, leading to greater hospital adoption. The segment also benefits from growing research initiatives and guideline updates recommending proactive management. Increasing cardiovascular disease prevalence, rising hospital admissions, and greater clinician focus on early intervention further accelerate growth. In addition, improved reimbursement policies, expanding hospital infrastructure in emerging markets, and enhanced patient education contribute to the rapid adoption of treatment solutions. Hospitals and specialty clinics are integrating innovative monitoring technologies to manage left bundle branch block patients more efficiently, which supports faster growth. Rising investment in cardiology departments and enhanced procedural capabilities further amplify market expansion in this segment.

- By Treatment

On the basis of treatment, the heart block treatment market is segmented into Transcutaneous Pacing (TCP), Pacemaker, Anti-Arrhythmic Drugs, and Electrophysiology. The Pacemaker segment dominated the largest market revenue share of 41.3% in 2024, owing to its critical role in restoring normal heart rhythm in patients with severe heart block. Pacemakers are widely preferred due to proven clinical efficacy, guideline recommendations, and long-term patient benefits. Hospitals and specialty clinics heavily rely on pacemaker implantation for second-degree and third-degree heart blocks. The segment’s dominance is reinforced by technological advancements, availability of minimally invasive procedures, and increasing adoption in both adult and pediatric patients. Strong insurance coverage, reimbursement schemes, and inclusion in hospital protocols drive widespread adoption. Market leadership is also aided by awareness campaigns highlighting the benefits of pacemakers for symptomatic heart block. North America holds a significant share due to advanced healthcare infrastructure and high clinician adoption rates. Continuous innovation in pacemaker design, including MRI-compatible and leadless devices, further strengthens the segment.

Transcutaneous Pacing (TCP) is expected to witness the fastest CAGR of 21.6% from 2025 to 2032, driven by its non-invasive nature, ease of emergency use, and growing preference for temporary pacing in acute care settings. TCP adoption is rising in hospital emergency departments and intensive care units, especially for immediate management of symptomatic heart block patients. Increasing awareness of acute cardiac intervention protocols, training of clinicians, and hospital emergency preparedness contribute to growth. Technological enhancements improving patient comfort and procedure safety also support market expansion. Growing cardiovascular disease prevalence, rising hospital admissions, and expanding healthcare infrastructure in Asia-Pacific are key factors accelerating TCP adoption. Integration with cardiac monitoring systems further enhances its clinical utility and drives rapid growth in this segment.

- By End-Users

On the basis of end-users, the heart block treatment market is segmented into hospitals, ambulatory surgical centers, specialty clinics, and others. The Hospitals segment dominated the largest market revenue share of 46.5% in 2024, due to the concentration of advanced cardiac care facilities, availability of specialized cardiologists, and access to high-end treatment technologies. Hospitals handle most heart block cases, ranging from initial diagnosis to device implantation and follow-up care. The dominance is further supported by robust healthcare infrastructure, insurance coverage, and established clinical protocols. Hospitals also conduct complex procedures such as pacemaker implantation and electrophysiology studies, reinforcing their leading market position. High patient volumes, multi-specialty cardiac departments, and strong adoption of guideline-based interventions contribute to the segment’s substantial revenue share. In addition, hospitals in North America and Europe act as key hubs for research, clinical trials, and technology adoption, maintaining dominance in treatment delivery.

Ambulatory Surgical Centers are expected to witness the fastest CAGR of 19.8% from 2025 to 2032, fueled by increasing preference for outpatient procedures, minimally invasive treatments, and cost-effective care. Growing awareness among patients for outpatient pacing procedures, availability of advanced equipment, and rising focus on short recovery times drive adoption. Expansion of ASC networks, especially in North America and Asia-Pacific, enhances accessibility for patients seeking timely intervention. Rising investments in cardiology-focused ASCs and improved procedural protocols support rapid growth. Integration of telemedicine for follow-up and monitoring also contributes to adoption. The cost-effectiveness, convenience, and reduced hospital stay requirements make ASCs increasingly attractive for heart block management, propelling growth in this segment.

Heart Block Treatment Market Regional Analysis

- North America dominated the heart block treatment market with the largest revenue share of 35% in 2024, driven by advanced healthcare infrastructure

- High clinician awareness, and the strong presence of key pharmaceutical and medical device companies

- The market witnessed substantial growth in heart block treatment adoption, particularly through hospital-based protocols, emergency care initiatives, and the integration of innovative cardiac therapies

U.S. Heart Block Treatment Market Insight

The U.S. heart block treatment market captured the largest revenue share within North America in 2024, fueled by widespread adoption of evidence-based treatment protocols, early diagnosis of cardiac conduction disorders, and increasing use of pacemakers and anti-arrhythmic drugs. Growing investments in specialized cardiac centers, coupled with rising clinician awareness and patient education programs, are further driving the market expansion.

Europe Heart Block Treatment Market Insight

The Europe heart block treatment market is projected to expand at a substantial CAGR throughout the forecast period, supported by increasing awareness of cardiovascular disorders, improvements in healthcare infrastructure, and rising adoption of advanced treatment options. Countries such as the U.K. and Germany are witnessing robust growth, driven by hospital initiatives for early detection and management of heart block conditions, as well as expanding access to innovative therapies.

U.K. Heart Block Treatment Market Insight

The U.K. heart block treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by government-supported healthcare programs, rising prevalence of cardiovascular disorders, and the integration of advanced diagnostic and therapeutic technologies. In addition, hospital-based initiatives and training programs for clinicians are contributing to increased adoption of heart block treatment solutions.

Germany Heart Block Treatment Market Insight

The Germany heart block treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, high patient awareness, and the availability of technologically advanced treatment solutions. Growing investments in cardiac care centers, coupled with the emphasis on preventive cardiology and early intervention, are supporting market growth in both hospital and outpatient settings.

Asia-Pacific Heart Block Treatment Market Insight

The Asia-Pacific heart block treatment market is expected to grow at the fastest CAGR during the forecast period, driven by rising cardiovascular disorders, expanding hospital networks, increasing investments in healthcare infrastructure, and greater access to advanced treatment options in countries such as China, India, and Japan. Improved healthcare delivery systems and growing awareness among clinicians and patients are contributing to the accelerated adoption of heart block therapies.

Japan Heart Block Treatment Market Insight

The Japan heart block treatment market is witnessing steady growth due to the country’s advanced healthcare system, increasing prevalence of cardiac conduction disorders, and rising adoption of pacemakers and other therapeutic interventions. Government support for specialized cardiac care, coupled with growing patient awareness and early diagnosis initiatives, is fueling market expansion.

China Heart Block Treatment Market Insight

The China heart block treatment market accounted for a significant revenue share in Asia-Pacific in 2024, driven by the country’s expanding middle class, increasing cardiovascular disorder prevalence, rapid development of specialized cardiac centers, and growing accessibility to advanced treatment options such as pacemakers, transcutaneous pacing, and anti-arrhythmic drug

Heart Block Treatment Market Share

The Heart Block Treatment industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- Biotronik SE & Co. KG (Germany)

- Edwards Lifesciences (U.S.)

- LivaNova (U.K.)

- GE Healthcare (U.S.)

- Siemens Healthineers AG (Germany)

- Johnson & Johnson and its affiliates (U.S.)

- MicroPort Scientific Corporation (China)

- BIOTRONIK (Germany)

- Cardiac Science Corporation (U.S.)

- Fukuda Denshi Co., Ltd. (Japan)

- Koninklijke Philips N.V. (Netherlands)

Latest Developments in Global Heart Block Treatment Market

- In July 2023, Abbott Laboratories received U.S. FDA approval for the AVEIR Dual Chamber (DR) Leadless Pacemaker System, marking the world's first dual-chamber leadless pacing system designed to treat patients with abnormal or slow heart rhythms. This innovative device eliminates the need for traditional leads, offering a minimally invasive solution for heart block patients

- In June 2024, Abbott announced the receipt of the European CE Mark for the Aveir DR Dual-Chamber Leadless Pacemaker System, further expanding its availability to patients in Europe. This approval underscores Abbott's commitment to advancing cardiac care through innovative pacing technologies

- In March 2024, UC San Diego Health became the first in the region to successfully implant the world's first dual-chamber leadless pacemaker system. This procedure utilized innovative technology to regulate heart rhythm, offering a new treatment option for patients with heart block

- In September 2024, Boston Scientific received FDA approval for an expanded indication of its INGEVITY+ Pacing Leads to include conduction system pacing of the left bundle branch area. This technique may promote greater ventricular synchrony and reduce the long-term risk of heart failure associated with traditional right ventricular pacing

- In July 2024, Biotronik launched Amvia Sky in Canada, the world's first pacemaker approved for Left Bundle Branch Area Pacing (LBBAP). The first implant of Amvia Sky in Canada was performed at the Centre Hospitalier de l'Université de Montréal, marking a significant advancement in physiological pacing techniques

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.