Global Hemophilia A Treatment Market

Market Size in USD Billion

USD

14.04 Billion

USD

22.47 Billion

2025

2033

USD

14.04 Billion

USD

22.47 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.04 Billion | |

| USD 22.47 Billion | |

| % | |

|

Hemophilia A Treatment Market Overview

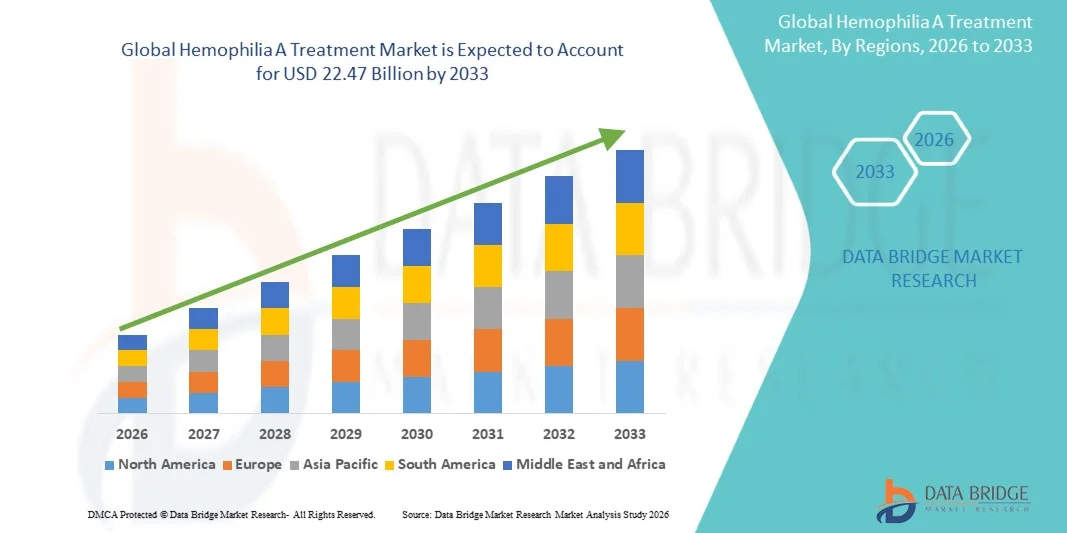

As per Data Bridge Market Research analysis the Hemophilia A Treatment Market was valued at USD 14.04 billion in 2025 and is projected to reach USD 22.47 billion by 2033, growing at a CAGR of 6.06% from 2026 to 2033. The market is experiencing steady growth driven by the increasing prevalence of hemophilia A, rising adoption of recombinant clotting factor therapies, and continuous advancements in gene therapy and non-factor replacement treatments.

The growing focus on early diagnosis and comprehensive disease management, coupled with improved access to specialized healthcare services and supportive reimbursement frameworks, is encouraging healthcare providers and patients to adopt advanced treatment options. Recombinant factor VIII products, extended half-life therapies, and innovative monoclonal antibody-based treatments are increasingly replacing conventional plasma-derived therapies in many regions, offering enhanced efficacy, reduced treatment burden, and improved patient outcomes. In addition, ongoing clinical research, expanding gene therapy pipelines, and increasing awareness initiatives by healthcare organizations are further supporting market expansion worldwide.

Key Market Trends & Insights

- North America dominated the Hemophilia A Treatment Market with the largest revenue share of 39.12% in 2025, supported by strong healthcare infrastructure, high diagnosis rates, and widespread adoption of advanced recombinant and non-factor therapies.

- The Severe segment led the market with a 52.34% share in 2025, driven by the high frequency of spontaneous bleeding episodes and the need for continuous prophylactic treatment

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by improving healthcare access, increasing awareness of bleeding disorders, and expanding availability of innovative therapies across China, India, and Japan.

- Moderate are the fastest-growing type, projected to register a CAGR of 7.8%, reflecting the surge in diagnosis rates and improved access to preventive treatment strategies.

- The Recombinant Factor Concentrates segment dominated the product type category with a 48.67% revenue share in 2025, led by its established safety profile and widespread clinical acceptance.

- Adult accounted for 63.18% of the market, preferred by the larger diagnosed patient population receiving long-term treatment.

- The Genetic Testing segment is the fastest-growing diagnosis category, with a CAGR of 8.2%, driven by the increasing adoption of precision medicine approaches

Market Size & Forecast

- Global Market Value (2025): USD 14.04 Billion

- Expected Market Value (2033): USD 22.47 Billion

- Forecast CAGR (2026–2033): 6.06%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Hemophilia A Treatment Market Segmentation

|

Attributes |

Hemophilia A Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Novo Nordisk A/S (Denmark) · F. Hoffmann-La Roche Ltd (Switzerland) · Pfizer Inc. (U.S.) · Sanofi (France) · Takeda Pharmaceutical Company Limited (Japan) · Bayer AG (Germany) · CSL Behring LLC (U.S.) · Octapharma AG (Switzerland) · BioMarin Pharmaceutical Inc. (U.S.) · Grifols, S.A. (Spain) · Sobi (Sweden) · Kedrion S.p.A. (Italy) · Chugai Pharmaceutical Co., Ltd. (Japan) · Genentech, Inc. (U.S.) · Spark Therapeutics, Inc. (U.S.) · uniQure N.V. (Netherlands) · Sangamo Therapeutics, Inc. (U.S.) · GC Biopharma Corp. (South Korea) · SK plasma Co., Ltd. (South Korea) · LFB BIOMEDICAMENTS (France) |

|

Market Opportunities |

· Expansion of gene therapy commercialization · Growing diagnosis and treatment access in emerging markets · Increasing adoption of personalized prophylaxis and extended half-life therapies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hemophilia A Treatment Market Trends

Trend: Rising Adoption of Gene Therapy and Long-Acting Treatments

Healthcare providers are increasingly adopting advanced gene therapies and extended half-life treatment options to improve disease management, reduce infusion frequency, and enhance patient quality of life. The integration of personalized treatment approaches enables more effective prophylaxis planning and long-term bleed prevention. Hemophilia treatment centers and specialty clinics are similarly utilizing innovative therapies to optimize outcomes through individualized care pathways, while ongoing biotechnology advancements are creating solutions that closely address unmet patient needs.

For instance, in April 2025, Pfizer and Sangamo Therapeutics continued advancing investigational gene therapy programs for hemophilia A, highlighting the industry's focus on long-term treatment innovation.

Hemophilia A Treatment Market Dynamics

Key Market Driver: Growing Adoption of Prophylactic and Innovative Treatment Approaches

The increasing adoption of prophylactic therapies and innovative treatment modalities has created substantial demand for advanced hemophilia A products that can prevent bleeding episodes, improve patient outcomes, and reduce long-term complications. Pharmaceutical manufacturers, treatment centers, and healthcare systems are incorporating novel therapies as a core component of disease management strategies, reducing hospitalization rates, improving adherence, and enhancing overall quality of care.

For instance, Hemlibra has seen expanding adoption globally as a prophylactic treatment for hemophilia A, supporting improved bleed control and patient convenience.

Key Restraint/Challenge: High Treatment Costs of Advanced Hemophilia Therapies

A significant restraint in the Hemophilia A Treatment Market is the high cost associated with advanced therapeutic options. Modern treatment regimens include recombinant clotting factors, non-factor replacement therapies, and emerging gene therapies, requiring substantial expenditure for acquisition, administration, and long-term monitoring. The overall economic burden extends to follow-up care, specialized clinical services, and reimbursement complexities, making access challenging for patients in lower-income regions and resource-constrained healthcare systems.

For instance, several recently introduced gene therapy candidates have been associated with premium pricing expectations, reflecting the broader affordability challenge facing healthcare providers and payers worldwide.

Key Market Opportunity: Expansion of Gene Therapy and Personalized Medicine Platforms

The expansion of gene therapy and personalized medicine approaches presents a significant market opportunity. Advanced therapeutic platforms can provide durable clinical benefits, support individualized treatment strategies, and reduce dependence on frequent replacement therapy administration. The development of next-generation vectors and precision treatment models is further improving accessibility to innovative care, opening growth opportunities across emerging healthcare markets in Asia-Pacific, Latin America, and the Middle East.

For instance, Roctavian has demonstrated the commercial potential of gene therapy for hemophilia A, encouraging further investment in personalized treatment development.

Hemophilia A Treatment Market Scope

The Hemophilia A treatment market is segmented on the basis of type, product, patient, diagnosis, treatment, therapy, drug class, route of administration, dosage form, end-users, and distribution channel.

- By Type

On the basis of type, the Hemophilia A Treatment Market is segmented into severe, moderate, and mild. The Severe segment dominated the market with an estimated 52.34% share in 2025, owing to the high frequency of spontaneous bleeding episodes and the need for continuous prophylactic treatment. Patients with severe hemophilia A typically require lifelong management with factor replacement or non-factor therapies. The segment accounts for a substantial share of healthcare spending due to intensive treatment requirements. Increasing adoption of extended half-life products and innovative biologics is further supporting market growth. Early diagnosis programs are also improving treatment uptake among severe patients. The significant clinical burden associated with severe disease continues to strengthen its market dominance.

The Moderate segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing diagnosis rates and improved access to preventive treatment strategies. Growing awareness among healthcare professionals is supporting earlier intervention and disease monitoring. Patients are increasingly receiving prophylactic therapy to prevent long-term joint damage and complications. Expanding availability of advanced therapeutics is improving treatment outcomes. Favorable reimbursement policies in developing healthcare systems are further encouraging adoption. Continuous improvements in patient management approaches are expected to accelerate segment growth.

- By Product

On the basis of product, the Hemophilia A Treatment Market is segmented into recombinant factor concentrates, plasma-derived factor concentrates, and extended half-life products. The Recombinant Factor Concentrates segment led the market with an estimated 48.67% share in 2025 due to its established safety profile and widespread clinical acceptance. These products minimize the risk of blood-borne pathogen transmission and are extensively recommended in treatment guidelines. Strong physician preference and broad product availability support their dominance. Continuous advancements in recombinant technologies are enhancing efficacy and patient convenience. Healthcare providers increasingly favor recombinant therapies for both prophylactic and on-demand treatment. Their long-standing role in hemophilia management continues to drive market leadership.

The Extended Half-life Products segment is expected to witness the fastest growth at a CAGR of 8.5% from 2026 to 2033, driven by their ability to reduce infusion frequency and improve treatment adherence. These products provide prolonged circulation time, enabling better bleed protection. Patients benefit from reduced treatment burden and enhanced quality of life. Growing adoption among pediatric and adult populations is supporting market expansion. Ongoing product innovations and clinical evidence are strengthening physician confidence. Rising demand for convenient long-term therapies is accelerating segment growth.

- By Patient

On the basis of patient, the Hemophilia A Treatment Market is segmented into pediatric and adult. The Adult segment dominated the market with an estimated 63.18% share in 2025 owing to the larger diagnosed patient population receiving long-term treatment. Adult patients often require continuous prophylaxis and management of disease-related complications. Increased life expectancy among hemophilia patients has expanded the treatment population. Growing utilization of advanced biologics and gene therapies is further supporting market demand. Regular monitoring and specialized care contribute significantly to healthcare expenditure. The need for lifelong disease management sustains the segment’s leading position.

The Pediatric segment is anticipated to register the fastest growth at a CAGR of 7.6% from 2026 to 2033 due to increasing emphasis on early intervention and preventive care. Healthcare providers are increasingly initiating prophylactic therapy at younger ages to prevent joint damage. Advances in treatment safety are encouraging broader adoption among children. Improved newborn screening and genetic testing programs are supporting earlier diagnosis. Rising awareness among parents and caregivers is contributing to treatment uptake. The focus on long-term health outcomes is expected to drive substantial segment growth.

- By Diagnosis

On the basis of diagnosis, the Hemophilia A Treatment Market is segmented into genetic testing, fibrinogen test, factor VIII and factor IX tests, prothrombin time (PT), and complete blood count (CBC). The Factor VIII and Factor IX Tests segment dominated the market with an estimated 44.89% share in 2025 as these tests remain the primary standard for confirming hemophilia severity and diagnosis. They provide accurate assessment of clotting factor activity levels. Physicians rely extensively on these tests for treatment planning and disease monitoring. Their widespread availability supports routine clinical use. Growing screening initiatives are increasing testing volumes globally. Their central role in diagnosis continues to maintain segment dominance.

The Genetic Testing segment is projected to grow at the fastest rate at a CAGR of 8.2% from 2026 to 2033, driven by increasing adoption of precision medicine approaches. Genetic testing enables identification of disease-causing mutations and supports family screening programs. Rising awareness regarding inherited bleeding disorders is accelerating utilization. Technological advancements are improving testing accuracy and accessibility. Healthcare providers increasingly use genetic information for personalized treatment planning. Expanding research in gene therapy is further supporting segment growth.

- By Treatment

On the basis of treatment, the Hemophilia A Treatment Market is segmented into prophylaxis and on demand. The Prophylaxis segment held the largest market share at 68.42% in 2025 due to its effectiveness in preventing bleeding episodes and reducing long-term complications. Clinical guidelines increasingly recommend preventive treatment for improved patient outcomes. Prophylaxis significantly lowers hospitalization rates and joint damage risks. Growing adoption of extended half-life and non-factor therapies is enhancing treatment convenience. Improved reimbursement support is encouraging wider use. The shift toward preventive care continues to strengthen segment leadership.

The On Demand segment is expected to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033 due to continued utilization in developing healthcare systems and mild disease cases. These therapies remain essential for managing acute bleeding episodes. Improved access to treatment products is supporting demand growth. Cost considerations often make on-demand treatment a practical option in resource-limited settings. Healthcare providers continue to utilize this approach for individualized patient management. Expanding healthcare access is expected to support segment expansion.

- By Therapy

On the basis of therapy, the Hemophilia A Treatment Market is segmented into factor replacement therapy and non-factor replacement therapy. The Factor Replacement Therapy segment dominated the market with a 71.26% share in 2025 owing to its long-established role as the standard treatment approach. These therapies effectively replace deficient clotting factors and provide reliable bleed control. Extensive clinical experience supports physician confidence in their use. Strong product availability across major markets further strengthens adoption. Continuous advancements in recombinant formulations are improving efficacy. Their critical role in disease management maintains market dominance.

The Non-factor Replacement Therapy segment is projected to register the fastest growth at a CAGR of 8.8% from 2026 to 2033, driven by increasing demand for convenient and effective treatment alternatives. These therapies offer less frequent administration schedules and improved patient compliance. Growing clinical evidence supports their long-term effectiveness in bleed prevention. Adoption is expanding among both pediatric and adult populations. Healthcare providers increasingly recommend these therapies for suitable patients. Continuous innovation is expected to accelerate segment growth.

- By Drug Class

On the basis of drug class, the Hemophilia A Treatment Market is segmented into vasopressin and coagulation factors. The Coagulation Factors segment accounted for the largest market share with 83.57% in 2025 due to their fundamental role in replacing deficient clotting proteins. These products are widely used across prophylactic and on-demand treatment settings. Strong clinical effectiveness supports their extensive adoption. Ongoing product improvements continue to enhance treatment outcomes. Healthcare providers rely on coagulation factors as a primary therapeutic option. Their essential role in hemophilia management sustains segment dominance.

The Vasopressin segment is expected to grow at the fastest pace at a CAGR of 6.5% from 2026 to 2033 due to its utility in selected mild hemophilia A cases. The therapy can temporarily increase endogenous factor VIII levels and reduce bleeding risks. Growing awareness regarding alternative treatment approaches is supporting utilization. Improved access to specialized care is increasing appropriate patient selection. Healthcare providers continue to evaluate vasopressin as part of individualized treatment plans. Expanding clinical awareness is expected to support growth.

- By Route of Administration

On the basis of route of administration, the Hemophilia A Treatment Market is segmented into parenteral, nasal spray, and others. The Parenteral segment dominated the market with a 78.91% share in 2025 owing to the widespread administration of factor replacement products and biologics through intravenous or subcutaneous routes. These methods provide rapid therapeutic action and reliable efficacy. Most approved hemophilia therapies are delivered parenterally. Strong clinical acceptance supports continued utilization. Healthcare providers prefer these routes for precise dosing and treatment control. Their extensive use across treatment settings sustains market leadership.

The Nasal Spray segment is projected to witness the fastest growth at a CAGR of 7.1% from 2026 to 2033, driven by increasing demand for convenient and non-invasive treatment options. Nasal administration improves patient comfort and ease of use. It is particularly beneficial in selected patient populations requiring rapid treatment access. Growing interest in self-administration is supporting adoption. Technological advancements are improving formulation effectiveness. Rising focus on patient-centric care is accelerating segment growth.

- By Dosage Form

On the basis of dosage form, the Hemophilia A Treatment Market is segmented into injection, solutions, and others. The Injection segment held the largest market share with 74.65% in 2025 due to the dominance of injectable clotting factor products and biologic therapies. Injections provide effective delivery and rapid therapeutic response. Most commercially available treatments are designed in injectable formulations. Healthcare professionals have extensive experience administering these products. Strong regulatory approvals support broad market availability. Their established role in treatment continues to drive segment dominance.

The Solutions segment is expected to register the fastest growth at a CAGR of 7.3% from 2026 to 2033 owing to increasing development of user-friendly formulations. These dosage forms improve preparation convenience and administration efficiency. Growing adoption in homecare settings is supporting demand. Manufacturers are focusing on improving product stability and usability. Enhanced patient preference for simplified treatment processes is contributing to growth. Continued innovation is expected to strengthen market expansion.

- By End-Users

On the basis of end-users, the Hemophilia A Treatment Market is segmented into hospitals, specialty clinics, homecare, and others. The Hospitals segment dominated the market with a 49.83% share in 2025 due to their ability to provide comprehensive diagnosis, treatment, and emergency care services. Hospitals serve as primary centers for managing severe bleeding episodes and complex cases. Availability of multidisciplinary healthcare teams supports patient outcomes. Access to advanced therapies further strengthens utilization. High patient volumes contribute significantly to revenue generation. Their central role in treatment delivery sustains segment leadership.

The Homecare segment is projected to witness the fastest growth at a CAGR of 8.0% from 2026 to 2033, driven by increasing adoption of self-administration and long-term prophylactic therapy. Homecare improves convenience while reducing hospital visits and associated costs. Advances in treatment formulations are enabling safer administration outside clinical settings. Patients increasingly prefer home-based management for better quality of life. Supportive healthcare policies are encouraging this transition. Growing emphasis on patient-centered care is accelerating segment growth.

- By Distribution Channel

On the basis of distribution channel, the Hemophilia A Treatment Market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The Hospital Pharmacy segment led the market with a 56.43% share in 2025 owing to the high distribution volume of specialized hemophilia therapies through hospital networks. These pharmacies ensure proper storage, handling, and monitoring of high-value biologic products. Strong coordination with healthcare providers supports treatment continuity. Patients often obtain therapies directly through hospital-based programs. Access to specialized pharmaceutical expertise further enhances utilization. Their critical role in therapy management maintains market dominance.

The Online Pharmacy segment is expected to register the fastest growth at a CAGR of 8.4% from 2026 to 2033 due to increasing digital healthcare adoption and expanding access to specialty medications. Online platforms offer convenience, home delivery, and improved treatment accessibility. Patients benefit from streamlined ordering processes and enhanced medication availability. Growth in telehealth services is supporting online pharmacy utilization. Expanding internet penetration is encouraging adoption across emerging markets. The shift toward digital healthcare channels is expected to drive substantial growth

Hemophilia A Treatment Market Regional Analysis

North America dominated the Hemophilia A Treatment Market with the largest revenue share of 39.12% in 2025, supported by strong healthcare infrastructure, high diagnosis rates, and widespread adoption of advanced recombinant and non-factor therapies. The region also benefits from favorable reimbursement frameworks, widespread adoption of recombinant factor therapies, non-factor replacement treatments, and increasing availability of innovative gene therapy products. Growing awareness of bleeding disorders, strong patient support programs, and extensive clinical research activities continue to drive market expansion. Increasing focus on personalized medicine approaches and long-term disease management continues to strengthen North America’s leadership position in the global market.

U.S. Hemophilia A Treatment Market Insight

The U.S. hemophilia A treatment market is witnessing strong growth due to rising adoption of advanced prophylactic therapies, increasing awareness of bleeding disorders, and expanding access to innovative treatment options. The country’s well-established healthcare infrastructure, along with growing utilization of recombinant factor products, non-factor replacement therapies, and gene therapy solutions, is driving demand across hospitals and specialty treatment centers. In addition, increasing emphasis on early diagnosis and long-term disease management is accelerating treatment adoption among pediatric and adult patient populations.

Europe Hemophilia A Treatment Market Insight

The Europe hemophilia A treatment market remains a major contributor to global revenue, driven by strong healthcare systems, favorable reimbursement policies, and high demand for advanced treatment solutions. The widespread use of recombinant factor therapies, extended half-life products, and non-factor replacement treatments is supporting market expansion across the region. Increasing investments in rare disease research, coupled with supportive regulatory frameworks and specialized treatment networks, continue to enhance the adoption of hemophilia A therapies throughout Europe.

U.K. Hemophilia A Treatment Market Insight

The U.K. hemophilia A treatment market is experiencing steady growth, supported by rising adoption of innovative therapies, expanding access to specialized care, and increasing focus on preventive treatment strategies. Growing investments in hemophilia management programs and rising demand for effective long-term treatment solutions are contributing to market growth. Furthermore, advancements in gene therapy research, personalized medicine approaches, and patient monitoring technologies are improving treatment outcomes, positioning the U.K. as a key innovation hub in the hemophilia A treatment industry.

Germany Hemophilia A Treatment Market Insight

The Germany hemophilia A treatment market is expanding steadily due to the country’s advanced healthcare infrastructure, strong research capabilities, and increasing adoption of next-generation therapeutic solutions. Healthcare providers, specialty clinics, and treatment centers are increasingly utilizing innovative therapies for disease management, bleed prevention, and long-term patient care. Continuous advancements in recombinant technologies, non-factor treatments, and gene therapy development, along with strong government support for rare disease management, are further driving market growth in Germany.

Asia-Pacific Hemophilia A Treatment Market Insight

The Asia-Pacific hemophilia A treatment market is expected to witness rapid growth, driven by increasing healthcare expenditure, improving diagnosis rates, and rising investments in rare disease treatment infrastructure across countries such as China, India, and Japan. Growing awareness regarding bleeding disorders, rising adoption of advanced therapeutic options, and increasing demand for accessible and effective treatment solutions are supporting regional market expansion. In addition, the growing presence of specialized treatment centers and expanding patient support programs are accelerating therapy adoption across the region.

Japan Hemophilia A Treatment Market Insight

The Japan hemophilia A treatment market is witnessing consistent growth due to rising investments in advanced treatment technologies, rare disease research, and patient care initiatives. Pharmaceutical companies, healthcare institutions, and research organizations are increasingly adopting innovative therapies for bleed prevention, disease management, and long-term outcome improvement. Moreover, increasing availability of recombinant products and the country’s focus on high-quality healthcare delivery are further contributing to market growth.

China Hemophilia A Treatment Market Insight

The China hemophilia A treatment market is growing rapidly, driven by increasing healthcare awareness, expanding medical infrastructure, and rising government focus on rare disease diagnosis and treatment. Growing adoption of recombinant therapies, non-factor replacement treatments, and emerging gene therapy platforms across hospitals and specialty centers is significantly boosting market demand. In addition, rising investments in biotechnology research, increasing awareness regarding early disease management, and rapid healthcare modernization are positioning China as one of the fastest-growing markets for hemophilia A treatment globally.

Hemophilia A Treatment Market Share

The Hemophilia A treatment industry is primarily led by well-established companies, including:

- Novo Nordisk A/S (Denmark)

- Hoffmann-La Roche Ltd (Switzerland)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Bayer AG (Germany)

- CSL Behring LLC (U.S.)

- Octapharma AG (Switzerland)

- BioMarin Pharmaceutical Inc. (U.S.)

- Grifols, S.A. (Spain)

- Sobi (Sweden)

- Kedrion S.p.A. (Italy)

- Chugai Pharmaceutical Co., Ltd. (Japan)

- Genentech, Inc. (U.S.)

- Spark Therapeutics, Inc. (U.S.)

- uniQure N.V. (Netherlands)

- Sangamo Therapeutics, Inc. (U.S.)

- GC Biopharma Corp. (South Korea)

- SK plasma Co., Ltd. (South Korea)

- LFB BIOMEDICAMENTS (France)

Latest Developments in Hemophilia A Treatment Market

- In June 2025, BioMarin Pharmaceutical announced the presentation of five-year Phase III GENEr8-1 study data for ROCTAVIAN (valoctocogene roxaparvovec) at the ISTH 2025 Congress. The results demonstrated sustained factor VIII expression, long-term bleed control, and continued reduction in prophylactic treatment requirements among patients with severe hemophilia A. The findings reinforced the durability and safety profile of the one-time gene therapy treatment. This development underscores the growing importance of gene therapy as a transformative approach in hemophilia A management

- In March 2025, Sanofi announced that the U.S. Food and Drug Administration (FDA) approved Qfitlia (fitusiran) for routine prophylaxis in patients aged 12 years and older with hemophilia A or B, with or without inhibitors. Qfitlia is the first antithrombin-lowering therapy approved for hemophilia and is designed to provide bleed protection with as few as six injections per year. The approval was supported by positive Phase III ATLAS clinical trial results demonstrating significant reductions in annualized bleeding rates. This development highlights the industry's focus on innovative therapies that reduce treatment burden and improve patient outcomes

- In October 2024, Pfizer announced that the U.S. FDA approved HYMPAVZI (marstacimab-hncq) for routine prophylaxis in adults and adolescents with hemophilia A without factor VIII inhibitors and hemophilia B without factor IX inhibitors. HYMPAVZI became the first once-weekly anti-TFPI therapy approved for these patient populations, offering a convenient subcutaneous treatment option. The approval expands the range of non-factor therapies available to hemophilia patients. This milestone reflects continued innovation aimed at improving treatment adherence and quality of life

- In July 2024, Pfizer announced positive Phase III AFFINE study results for giroctocogene fitelparvovec, its investigational gene therapy for moderately severe to severe hemophilia A. The study demonstrated superiority over routine factor VIII prophylaxis by significantly reducing annualized bleeding rates and maintaining durable factor VIII activity following a single infusion. The results strengthened the therapy’s potential as a long-term treatment solution. This development highlights the accelerating progress of gene therapy innovation within the hemophilia A treatment landscape

- In June 2023, BioMarin Pharmaceutical announced that the U.S. FDA approved ROCTAVIAN (valoctocogene roxaparvovec-rvox), the first gene therapy for adults with severe hemophilia A. The one-time treatment is designed to enable endogenous factor VIII production and reduce dependence on regular prophylactic infusions. The approval marked a major advancement in the treatment of inherited bleeding disorders and introduced a new therapeutic paradigm for hemophilia A patients. This launch underscores the industry's commitment to delivering durable and potentially transformative treatment options

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.