Global High Entropy Alloys Market

Market Size in USD Billion

USD

1.43 Billion

USD

9.91 Billion

2025

2033

USD

1.43 Billion

USD

9.91 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.43 Billion | |

| USD 9.91 Billion | |

| % | |

|

High-Entropy Alloys Market Overview

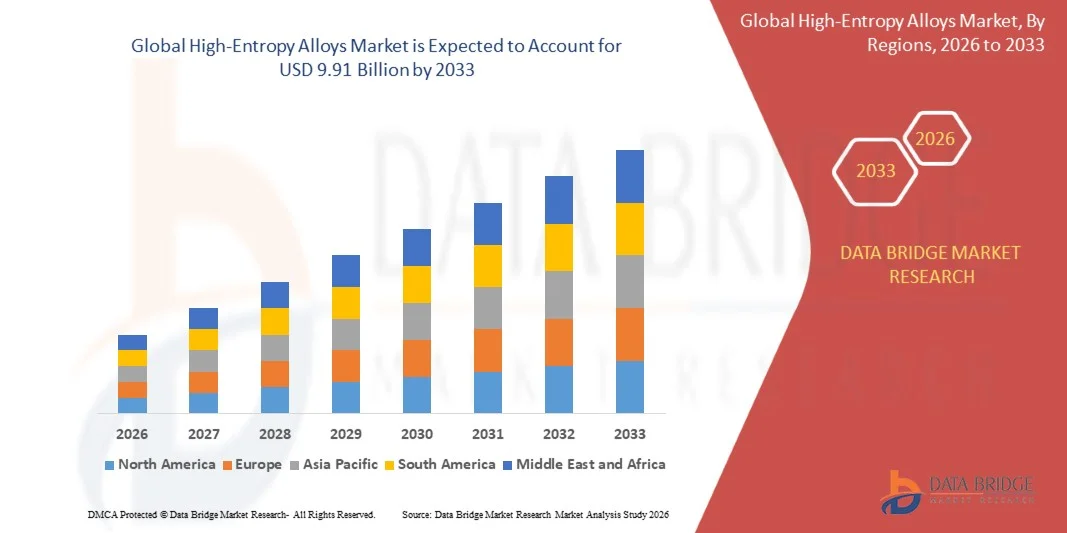

As per Data Bridge Market Research Analysis the High-Entropy Alloys Market was valued at USD 1.43 billion in 2025 and is projected to reach USD 9.91 billion by 2033, growing at a CAGR of 27.40% from 2026 to 2033. The market is experiencing explosive growth driven by surging demand for lightweight, high-strength materials with superior thermal stability and corrosion resistance across aerospace, defense, and energy sectors. Breakthroughs in additive manufacturing and powder metallurgy are enabling cost-effective production of complex alloy compositions, while increased R&D investments and government support for advanced materials are accelerating commercialization.

The remarkable CAGR of 27.40% reflects a paradigm shift in materials engineering, as high-entropy alloys—comprising five or more principal elements in near-equiatomic ratios—offer unprecedented combinations of mechanical strength, wear resistance, and radiation tolerance that conventional alloys cannot match. Their unique atomic structures enable sluggish diffusion and lattice distortion, delivering exceptional performance in extreme environments ranging from hypersonic aerospace components to next-generation nuclear reactors.

Market Size & Forecast

- Global Market Value (2025): USD 1.43 billion

- Expected Market Value (2033): USD 9.91 billion

- Forecast CAGR (2026–2033): 27.40%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Key Market Trends & Insights

- North America is projected to dominate the High-Entropy Alloys Market, supported by robust federally funded research programs through the Department of Energy and Department of Defense, strong aerospace and defense demand from industry leaders, and significant R&D expenditure in materials innovation.

- Asia-Pacific is expected to be the fastest-growing region, fueled by rapid industrialization, expanding automotive and electronics production capacity, and aggressive government-backed research initiatives in China, Japan, and South Korea.

- The 3D Transition Metal HEAs segment led the market in 2024 with a 38.1% share, driven by cost-effectiveness, mechanical resilience, and compatibility with additive manufacturing processes.

- Refractory Metal HEAs are emerging as a high-growth segment, with the sub-market projected to grow at a CAGR of 20.1%, driven by demand for materials that can withstand temperatures exceeding 1,500°C in turbine engines and hypersonic vehicle components.

- The Aerospace & Defense sector dominated end-use industries in 2024, driven by ongoing demand for lightweight materials with high mechanical strength and thermal resistance for jet engines, airframes, and defense equipment.

- Casting & Solidification remained the dominant manufacturing method with a 43.1% share in 2024, owing to its scalability, cost-efficiency, and integration with existing metallurgical systems.

- Additive Manufacturing is the fastest-growing manufacturing method, enabling complex part designs and rapid prototyping while reducing material waste.

- Superior Mechanical Properties represented the largest property segment in 2024, with high tensile strength, impact resistance, and ductility making HEAs essential for structural applications requiring integrity under cyclic stress.

Report Scope and High-Entropy Alloys Market Segmentation

|

Attributes |

High-Entropy Alloys Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

High-Entropy Alloys Market Trends

Trend: Evolution from System of Record to System of Action

Modern GRC platforms are fundamentally transforming from passive repositories of risk and compliance data into active systems that orchestrate outcomes and actions . This shift involves integrating with a broader ecosystem of risk technologies, using automation and AI to not only identify and report risks but also to initiate remediation workflows and recommend actions. Vendors are focusing on providing orchestration capabilities that help risk professionals proactively manage threats and demonstrate the effectiveness of their programs, moving beyond mere documentation towards driving strategic value .

High-Entropy Alloys Market Dynamics

Key Market Driver: Rising Demand in Aerospace, Automotive, and Energy Sectors

The aerospace and defense sectors are increasingly utilizing high-entropy alloys because of their exceptional strength, heat resistance, and corrosion protection. These alloys enhance the performance of engines, structural elements, and protective equipment by withstanding harsh environments and mechanical stress. The push for lighter, more durable, and energy-efficient materials motivates manufacturers to replace conventional alloys with HEAs. In the automotive sector, HEAs offer promising applications in electric vehicle components due to their thermal stability and corrosion resistance, while the energy industry deploys them in nuclear reactors, gas turbines, and solar thermal systems.

Key Restraint/Challenge: High Production Costs and Scalability Limitations

A significant restraint in the High-Entropy Alloys Market is the high upfront capital required for advanced manufacturing systems. The multi-element compositions and reliance on specialized fabrication methods—including additive manufacturing, powder metallurgy, and sophisticated casting techniques—drive up component costs. Achieving uniform microstructures and optimal properties demands specialized machinery, skilled personnel, and extensive quality control. Raw material expenses, particularly for refractory metals and precious elements, further increase production costs. These financial barriers limit adoption among smaller manufacturers, research institutions, and cost-sensitive industries, slowing broader market penetration despite HEAs' superior performance advantages.

Key Market Opportunity: Energy and Power Generation Applications

The energy and power generation industries offer substantial growth opportunities for high-entropy alloys, which provide excellent heat resistance, durability, and corrosion protection in demanding environments. HEAs are increasingly suitable for turbines, nuclear facilities, heat exchangers, and offshore energy infrastructure where conventional metals struggle. The growing focus on renewable energy projects, including next-generation solar thermal and hydrogen storage systems, is expanding addressable markets. Hydrogen storage high-entropy alloys alone represented a USD 463.47 million market in 2025, projected to reach USD 1.38 billion by 2032 at a CAGR of 16.7%. Energy-focused HEA development enables companies to deliver materials that meet stringent performance and maintenance requirements for critical infrastructure.

High-Entropy Alloys Market Scope

The high-entropy alloys market is segmented on the basis of alloy type, manufacturing method, property, application, end-use industry, and region.

- By Alloy Type

On the basis of alloy type, the High-Entropy Alloys Market is segmented into 3D transition metal HEAs, refractory metal HEAs, light metal HEAs, aluminum-containing HEAs, precious metal HEAs, rare earth element-containing HEAs, and others. The 3D transition metal HEAs segment accounted for approximately 38.1% of the market share in 2024, driven by their mechanical strength, corrosion resistance, and economic viability for aerospace, automotive, and energy applications. These alloys, featuring elements such as Fe, Ni, Co, Cr, and Mn, offer high thermal conductivity, excellent radiation tolerance, and compatibility with powder metallurgy and additive manufacturing processes. The refractory Metal HEAs segment is experiencing significant growth, driven by demand for materials that maintain structural integrity at extreme temperatures exceeding 1,500°C for turbine engines and hypersonic vehicle components.

- By Manufacturing Method

On the basis of manufacturing method, the market is segmented into casting & solidification, powder metallurgy, additive manufacturing, thin film deposition, and others. The casting & solidification segment held a dominant 43.1% market share in 2024 due to the scalability, cost-efficiency, and integration capabilities with existing metallurgical systems. This technique facilitates the creation of essential multi-principal element microstructures and homogenization for superior mechanical performance. While additive manufacturing and powder metallurgy continue to gain traction, casting remains the most economical method for bulk production of intricate geometries that undergo intensive thermal and mechanical stress. The Additive Manufacturing segment is projected to register the fastest growth, driven by rapid prototyping, design flexibility, and increased cost-efficiency for customized HEA components.

- By Property

On the basis of property, the market is segmented into superior mechanical properties, thermal stability, corrosion & oxidation resistance, magnetic properties, electrical properties, radiation resistance, and others. The superior mechanical properties segment held the largest market share in 2024, driven by the high yield strength, fracture toughness, and fatigue resistance exhibited by HEAs under extreme mechanical stress. These properties enable HEAs to outperform many traditional metals in demanding applications, including turbine engines, structural frames, and ballistic protection systems. The unique atomic configurations of HEAs promote solid-solution strengthening and sluggish diffusion, contributing to exceptional mechanical stability across a wide temperature range. The radiation resistance property segment is growing significantly, driven by applications in nuclear reactors and space exploration where materials must withstand high-energy particle bombardment.

- By Application

On the basis of application, the market is segmented into structural applications, functional applications, coatings & surface treatments, extreme environment applications, and others. The structural applications segment dominated the market in 2024 due to the broad-spectrum load-bearing capabilities of HEAs, including fatigue resistance, mechanical stability, and high impact resistance. These alloys are frequently chosen for components requiring significant load-bearing capacity or operation in high-stress environments, such as aerospace frameworks, automotive chassis, and industrial machinery. The multi-phase structure of HEAs enhances toughness and prevents failure during high-impact use, making them essential for durability and long service life in transportation and infrastructure sectors. The extreme environment applications segment is expected to witness accelerated growth, driven by demand for materials that perform reliably in cryogenic, ultra-high-temperature, and radiation-intensive environments.

- By End-Use Industry

On the basis of end-use industry, the market is segmented into aerospace & defense, automotive, energy, industrial equipment, electronics & semiconductors, chemical & petrochemical, medical & healthcare, research & academia, and others. The aerospace & defense segment led the global market in 2024, reflecting the sector's ongoing demand for materials that combine lightweight characteristics with high mechanical strength and thermal resistance. Components that operate in rapidly changing thermal environments require enhanced oxidation and creep resistance, which HEAs can provide. The proven reliability of HEAs in harsh conditions continues to drive investment and innovation, particularly for mission-critical systems such as airframes, jet engines, and missiles. The energy segment is expected to witness the fastest growth, driven by increasing adoption in nuclear reactors, gas turbines, and hydrogen storage applications.

High-Entropy Alloys Market Regional Analysis

North America dominated the high-entropy alloys market in 2024, supported by robust federally supported materials research through the Department of Energy and Department of Defense, enabling advanced commercialization. The United States market was valued at approximately USD 257-420 million in 2024, with aerospace and defense leaders generating unremitting demand for lightweight, thermally stable, high-strength materials. The energy and automotive sectors further ground the U.S. market by accelerating the use of advanced alloys in EV battery enclosures, turbine parts, and structural components that demand strong performance under mechanical and thermal stress. The Asia-Pacific region is expected to witness the highest CAGR, driven by significant industrial expansion, growing research and development funding, and strong governmental support for advanced materials initiatives in China, India, Japan, and South Korea.

U.S. High-Entropy Alloys Market Insight

The U.S. high-entropy alloys market is witnessing strong growth due to rising investments in advanced materials research, defense modernization programs, and aerospace innovation. The country's mature aerospace and defense ecosystem, along with increasing adoption of additive manufacturing and computational materials engineering, is driving demand across commercial, defense, and energy applications. The U.S. Department of Defense and NASA are actively funding HEA research for hypersonic vehicles, propulsion systems, and space exploration. Growing emphasis on reducing component weight and improving fuel efficiency in commercial aviation is accelerating HEA adoption across the aerospace supply chain.

China High-Entropy Alloys Market Insight

The China high-entropy alloys market is growing at the fastest rate globally, driven by large-scale investments in advanced materials research, aerospace projects, and military-grade alloy applications. The country's focus on self-reliance in critical materials and technologies has created significant government-backed R&D programs, with state-owned laboratories and universities developing novel HEA compositions for strategic applications. Regional clusters for advanced materials manufacturing and wider test campaigns in turbine hot sections and petrochemical equipment are accelerating industrial validation. Increasing adoption in automotive and electronics sectors is positioning China as a key innovation hub and production center for high-entropy alloys.

High-Entropy Alloys Market Share

The high-entropy alloys industry is primarily led by well-established companies, including:

- Carpenter Technology Corporation (U.S.)

- Sandvik AB (Sweden)

- QuesTek Innovations LLC (U.S.)

- Hitachi Metals (Japan)

- Allegheny Technologies Incorporated (U.S.)

- Haynes International (U.S.)

- Aperam S.A. (Luxembourg)

- Nippon Yakin Kogyo (Japan)

- VDM Metals Holding GmbH (Germany)

- Plansee Holding AG (Austria)

- Oerlikon Metco (Switzerland)

- TANAKA Kikinzoku Kogyo K.K. (Japan)

- Heraeus Holding GmbH (Germany)

- Metalysis (U.K.)

- American Elements (U.S.)

- Höganäs AB (Sweden)

- 6K Inc. (U.S.)

- Beijing Yijin New Material Technology Co., Ltd. (China)

- Heeger Materials (U.S.)

Latest Developments in High-Entropy Alloys Market

- In February 2026, 6K Additive signed a global long-term supply agreement with Siemens Energy to supply spent nickel alloy powder from its additive manufacturing facilities for use as feedstock in 6K Additive's proprietary UniMelt® microwave plasma production system, enabling productive reuse of nickel-based superalloy revert material.

- In July 2025, ATI Inc. announced the extension and expansion of its long-term titanium products agreement with The Boeing Company, reinforcing ATI's position as a top supplier of high-performance titanium materials for aerospace, supporting Boeing's full suite of commercial airplane programs.

- In June 2025, Sandvik AB and Additive Industries announced a new metal powder supply partnership for direct filling of Additive Industries' Powder Load Tool (PLT), designed for use with the company's MetalFab Additive Manufacturing machines.

- In February 2025, researchers created a high-entropy alloy catalyst with platinum, palladium, cobalt, nickel, and manganese, further reducing platinum utilization while improving durability and efficiency in hydrogen generation via stable water electrolysis in alkaline seawater.

- In January 2025, Metalysis acquired a 40kW Tekna spheroidiser to increase the production of high-entropy alloys with refractory materials like tantalum and niobium.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global High Entropy Alloys Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global High Entropy Alloys Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global High Entropy Alloys Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.