Global High Performance Computing Hpc Accelerator Market

Market Size in USD Billion

USD

14.86 Billion

USD

41.72 Billion

2025

2033

USD

14.86 Billion

USD

41.72 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.86 Billion | |

| USD 41.72 Billion | |

| % | |

|

High-Performance Computing (HPC) Accelerator Market Overview

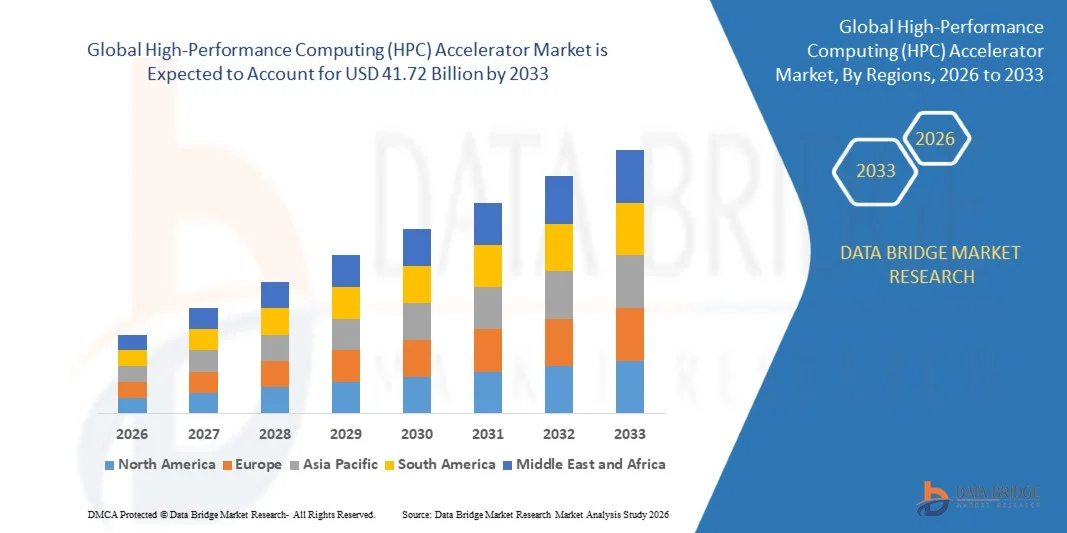

The High-Performance Computing (HPC) Accelerator Market was valued at USD 14.86 billion in 2025 and is projected to reach USD 41.72 billion by 2033, growing at a CAGR of 13.8% from 2026 to 2033. The market is expanding rapidly due to rising demand for AI training, scientific simulation, genomics, weather forecasting, digital twins, and large-scale parallel computing. GPU-based accelerator platforms remain the core of HPC modernization, while FPGA and ASIC accelerators are increasingly used for workload-specific performance optimization and energy efficiency.

Hyperscale cloud providers, national labs, and enterprise R&D centers are accelerating investment in heterogeneous compute architectures to improve throughput and reduce time-to-insight. Leading vendors including NVIDIA, AMD, Intel, and Advanced Micro Devices' ecosystem partners continue to strengthen the market through new accelerator launches, memory-bandwidth improvements, and AI-HPC convergence.

Key Market Trends & Insights

- North America dominated the global HPC accelerator market with the largest revenue share of 38.4% in 2025, supported by strong semiconductor innovation, major cloud infrastructure investment, and the presence of leading HPC and AI hardware suppliers.

- The GPU Accelerators segment led the market with a 61.7% share in 2025 due to superior parallel processing performance and widespread use in AI, simulation, and scientific computing workloads.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 15.1% from 2026 to 2033, driven by government supercomputing programs, semiconductor manufacturing growth, and expanding AI infrastructure.

- Cloud HPC is growing quickly as organizations adopt elastic compute capacity to avoid large upfront infrastructure spending and to scale workloads on demand.

- AI accelerator ASICs are gaining traction for large model training and inference optimization, especially in energy-sensitive and high-density computing environments.

- Research & Academia remained the largest end-use segment in 2025, supported by national research initiatives, university supercomputing centers, and public funding for advanced computing.

- Hybrid HPC deployments are becoming more common as enterprises combine on-premises performance with cloud flexibility for burst workloads and collaboration.

Market Size & Forecast

- Global Market Value (2025): USD 14.86 Billion

- Expected Market Value (2033): USD 41.72 Billion

- Forecast CAGR (2026–2033): 13.8%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and High-Performance Computing (HPC) Accelerator Market Segmentation

|

Attributes |

High-Performance Computing (HPC) Accelerator Market Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· NVIDIA Corporation (U.S.) · Advanced Micro Devices, Inc. (U.S.) · Intel Corporation (U.S.) · IBM Corporation (U.S.) · Hewlett Packard Enterprise (U.S.) · Dell Technologies (U.S.) · Lenovo (U.S.) · Super Micro Computer (U.S.) · Fujitsu (Japan) · NEC Corporation (Japan) · Cisco Systems (U.S.) · Penguin Solutions (U.S.) · Cerebras Systems (U.S.) · SambaNova Systems (U.S.) · Graphcore (United Kingdom) · Tenstorrent (Canada) · Marvell Technology (U.S.) · Qualcomm Technologies (U.S.) · Atos (France) |

|

Market Opportunities |

· Growth in AI-HPC convergence, expansion of energy-efficient accelerators · Rising demand for cloud supercomputing · Increasing adoption in life sciences, defense, and climate modeling. |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

High-Performance Computing (HPC) Accelerator Market Trends

Trend: Convergence of AI and HPC Workloads

HPC environments are increasingly being designed for both traditional simulation workloads and AI training or inference, which is boosting demand for accelerators with high memory bandwidth and mixed-precision performance. This convergence is pushing vendors to deliver unified platforms that can support scientific computing, machine learning, and data analytics in one infrastructure stack.

High-Performance Computing (HPC) Accelerator Market Dynamics

Key Market Driver: Rising Demand for Parallel Computing Performance

The need for faster simulation, modeling, and AI training is driving investment in HPC accelerators across research, enterprise, and government environments. As workloads become more complex and data-intensive, organizations are increasingly relying on GPU-centric and heterogeneous architectures to achieve the required throughput.

Key Restraint/Challenge: High Infrastructure and Power Costs

HPC accelerator deployments require substantial capital investment in hardware, cooling, networking, and power delivery. Energy consumption remains a major issue, especially for large GPU clusters and national supercomputing facilities, making total cost of ownership a critical decision factor.

Key Market Opportunity: Expansion of Cloud-Based HPC

Cloud HPC is opening access to advanced computer resources for smaller enterprises, startups, and research teams that cannot afford dedicated supercomputing infrastructure. This model is expanding the addressable market for accelerator vendors and cloud service providers by lowering the barrier to entry.

High-Performance Computing (HPC) Accelerator Market Scope

The Global HPC Accelerator Market is segmented on the basis of accelerator type, deployment, and end-use industry.

- By Accelerator Type

On the basis of accelerator type, the market is segmented into GPU Accelerators, CPU Accelerators, FPGA Accelerators, and AI Accelerator ASICs. GPU Accelerators dominated the market in 2025 because they are the preferred choice for massively parallel workloads such as AI training, computational fluid dynamics, molecular simulation, and weather modeling.

FPGA and ASIC accelerators are growing in niche applications that require lower latency, higher efficiency, or custom workload optimization.

- By Deployment

On the basis of deployment, the market is segmented into On-Premises HPC, Cloud HPC, and Hybrid HPC. On-Premises HPC remained the dominant deployment model in 2025 for national labs, defense systems, and large research institutes requiring direct control over performance and data security.

Cloud HPC is expected to register the fastest growth through 2033 as elastic compute and pay-as-you-go models become more attractive.

- By End-Use Industry

On the basis of end-use industry, the market is segmented into BFSI, Healthcare & Life Sciences, Manufacturing, Research & Academia, and Government & Defense. Research & Academia held the largest share in 2025 due to strong supercomputing demand for physics, chemistry, materials science, and climate research.

Healthcare & Life Sciences is emerging rapidly as genomics, drug discovery, and bioinformatics workloads become more accelerator-intensive.

High-Performance Computing (HPC) Accelerator Market Regional Analysis

North America dominated the Global HPC Accelerator Market in 2025, led by the U.S. with its concentration of semiconductor vendors, cloud providers, national laboratories, and enterprise AI infrastructure investment. The region continues to set the pace for innovation in GPU, AI accelerator, and heterogeneous compute architectures.

U.S. High-Performance Computing (HPC) Accelerator Market Insight

The United States dominates the global HPC accelerator market, driven by the strong presence of hyperscale cloud providers such as AWS, Microsoft Azure, and Google Cloud, along with leading semiconductor companies like NVIDIA, AMD, and Intel. The country benefits from advanced digital infrastructure, heavy investments in AI research, and early adoption of exascale computing systems. U.S. government-backed initiatives in defense, space exploration, and scientific simulation further strengthen demand for high-performance accelerators such as GPUs, FPGAs, and AI ASICs. The increasing deployment of AI workloads, generative AI models, and real-time analytics is accelerating the adoption of HPC accelerators across enterprise and research ecosystems.

Europe High-Performance Computing (HPC) Accelerator Market Insight

Europe holds a significant share of the HPC accelerator market, supported by strong government funding, academic research institutions, and industrial applications. Countries such as Germany, France, and the United Kingdom are leading adopters, particularly in automotive design, aerospace engineering, climate modeling, and energy simulations. The European Union’s focus on digital sovereignty and sustainable computing is pushing investments in energy-efficient HPC infrastructure and AI-optimized data centers. Europe also benefits from collaborative supercomputing initiatives such as EuroHPC, which are enhancing regional competitiveness in advanced computing technologies.

U.K. High-Performance Computing (HPC) Accelerator Market Insight

The United Kingdom is one of the fastest-growing HPC accelerator markets in Europe, driven by rapid digital transformation, strong academic research, and expansion of AI-driven cloud infrastructure. The country is increasingly investing in next-generation data centers and high-performance computing systems to support financial modeling, life sciences, and advanced engineering applications. The UK market is projected to grow at a high CAGR of nearly 26.9% (2025–2030), reflecting strong demand for GPU-accelerated computing and AI workloads across public and private sectors.

Germany High-Performance Computing (HPC) Accelerator Market Insight

Germany is a key HPC hub in Europe, supported by its strong industrial base and leadership in automotive engineering, manufacturing, and industrial automation. The country heavily utilizes HPC accelerators for simulation-driven design, digital twin technologies, and climate research. Germany’s focus on Industry 4.0 and smart manufacturing is increasing the deployment of GPU and AI accelerator-based systems across enterprises. Additionally, government-supported supercomputing projects and research institutions such as those under the Gauss Centre for Supercomputing further enhance demand for high-performance accelerator infrastructure.

Asia-Pacific High-Performance Computing (HPC) Accelerator Market Insight

Asia Pacific is the fastest-growing regional market for HPC accelerators, fueled by rapid digital transformation, cloud expansion, and large-scale AI adoption. Countries such as China, India, Japan, and South Korea are investing heavily in supercomputing infrastructure, semiconductor development, and AI research. The region is witnessing strong deployment of GPU-based clusters for generative AI, smart manufacturing, and scientific computing. Government initiatives and sovereign AI programs are also driving domestic production of HPC hardware, especially in China and India. Asia Pacific is expected to record the highest CAGR globally due to rising demand for data-intensive applications.

Japan High-Performance Computing (HPC) Accelerator Market Insight

Japan remains a highly advanced HPC market, supported by strong government-backed research programs and global leadership in supercomputing. The country’s flagship systems, such as Fugaku and upcoming next-generation projects, highlight its focus on combining CPUs and GPUs for hybrid AI-HPC workloads. Japan is increasingly applying HPC accelerators in climate modeling, disaster prediction, automotive innovation, and pharmaceutical research. Collaboration between Fujitsu, RIKEN, and global semiconductor leaders is strengthening Japan’s position in next-generation exascale and zettascale computing systems.

China High-Performance Computing (HPC) Accelerator Market Insight

China is one of the most rapidly expanding HPC accelerator markets, driven by strong government investment in AI, supercomputing, and semiconductor self-sufficiency. Due to restrictions on advanced GPU imports, China is increasingly developing domestic HPC architectures, including CPU-based and AI-optimized accelerator systems. The country is deploying large-scale supercomputers for AI training, earth observation, defense simulations, and industrial analytics. Massive investments in data centers and indigenous chip development (such as Huawei-based ecosystems) are strengthening China’s HPC ecosystem and reducing reliance on Western technologies.

High-Performance Computing (HPC) Accelerator Market Share

The High-Performance Computing (HPC) Accelerator Market industry is primarily led by well-established companies, including:

- NVIDIA Corporation (U.S.)

- Advanced Micro Devices, Inc. (U.S.)

- Intel Corporation (U.S.)

- IBM Corporation (U.S.)

- Hewlett Packard Enterprise (U.S.)

- Dell Technologies (U.S.)

- Lenovo (U.S.)

- Super Micro Computer (U.S.)

- Fujitsu (Japan)

- NEC Corporation (Japan)

- Cisco Systems (U.S.)

- Penguin Solutions (U.S.)

- Cerebras Systems (U.S.)

- SambaNova Systems (U.S.)

- Graphcore (United Kingdom)

- Tenstorrent (Canada)

- Marvell Technology (U.S.)

- Qualcomm Technologies (U.S.)

- Atos (France)

Latest Developments in High-Performance Computing (HPC) Accelerator Market

- In April 2026 is the expansion of the partnership between Intel and SambaNova Systems to build a heterogeneous AI–HPC acceleration platform. The collaboration integrates Intel Xeon CPUs, GPUs, and networking with SambaNova’s reconfigurable dataflow units (RDUs) to optimize AI inference and HPC workloads. This architecture is designed to distribute workloads efficiently across multiple hardware layers, improving scalability for enterprise HPC systems. The platform is expected to launch in the second half of 2026 and is positioned as a direct alternative to GPU-centric ecosystems dominated by NVIDIA.

- In May 2026, Intel has further strengthened its commitment to the HPC accelerator ecosystem by increasing its investment in SambaNova Systems through multiple funding rounds in 2026. This investment aims to accelerate development of next-generation AI inference and HPC accelerator systems, while expanding enterprise deployment through Intel-powered infrastructure. The move reflects Intel’s broader strategy to regain competitiveness in AI accelerators by supporting external innovation and building hybrid compute ecosystems combining CPUs and specialized AI chips.

- In February 2026, SambaNova Systems secured over $350 million in a major funding round led by Vista Equity Partners, with participation from Intel Capital. The company is using this capital to scale its SN50 AI accelerator chips and expand its cloud-based AI infrastructure offerings. Additionally, SoftBank became an early adopter of SambaNova systems for next-generation AI data centers in Japan. This development highlights increasing investor confidence in non-GPU accelerator architectures within the HPC market.

- In May 2026, Cerebras Systems marked a major milestone with its IPO in 2025–2026, reflecting strong market demand for alternative HPC accelerator architectures. The company’s wafer-scale chips, significantly larger than conventional GPUs, are positioned for high-throughput AI training and HPC workloads. Cerebras reported strong revenue growth and expanding customer adoption, including cloud providers and AI research organizations. The IPO highlights growing investor interest in specialized HPC accelerators beyond traditional GPU dominance.

- In December 2025, Advanced Micro Devices (AMD) is preparing a major expansion in the HPC accelerator space with its upcoming Instinct MI450 series and rack-scale “Helios” solution, expected in 2026. These accelerators aim to improve performance in AI training, scientific simulations, and HPC workloads while competing directly with NVIDIA’s GPU dominance. AMD’s strategy also includes strengthening its ROCm software ecosystem and increasing adoption in enterprise and hyperscale cloud environments, positioning the company as a strong alternative in the HPC accelerator market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.