Global High Pressure Contrast Media Injectors Market

Market Size in USD Million

USD

276.62 Million

USD

694.76 Million

2025

2033

USD

276.62 Million

USD

694.76 Million

2025

2033

| 2026 - 2033 | |

| USD 276.62 Million | |

| USD 694.76 Million | |

| % | |

|

High Pressure Contrast Media Injectors Market Overview

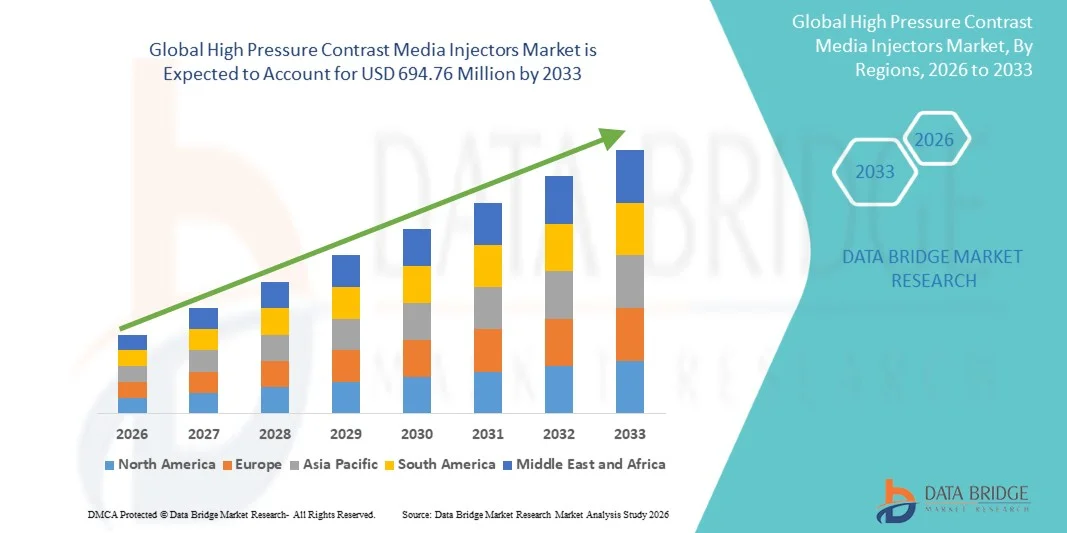

The High Pressure Contrast Media Injectors Market was valued at USD 276.62 million in 2025 and is projected to reach USD 694.76 million by 2033, growing at a CAGR of 12.20% from 2026 to 2033. Market growth is supported by rising prevalence of cardiovascular diseases, increasing demand for advanced diagnostic imaging procedures, and growing adoption of minimally invasive interventional procedures across healthcare facilities worldwide.

The superior precision and consistency offered by high pressure contrast media injectors in delivering contrast agents during computed tomography (CT), angiography, and magnetic resonance imaging (MRI) procedures are driving increased adoption among radiologists and interventional specialists. These devices enable optimal contrast enhancement, reduced procedure times, and improved patient safety through automated injection protocols and dose management capabilities. Ongoing technological advancements in injector systems, including integration with imaging platforms, wireless connectivity, and enhanced safety features such as air detection and pressure monitoring, are expanding clinical applicability across interventional cardiology, interventional radiology, and neuroradiology specialties. In addition, growing healthcare infrastructure investments in emerging markets and the expansion of diagnostic imaging centers are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the High Pressure Contrast Media Injectors Market with the largest revenue share of 38.7% in 2025, supported by high adoption rates of advanced imaging technologies, established reimbursement frameworks, and the presence of leading market players.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 14.35% from 2026 to 2033, driven by expanding healthcare infrastructure, rising demand for diagnostic imaging procedures, and increasing healthcare expenditure.

- The Injector Systems segment led the product category with a 62.4% market share in 2025, reflecting the critical role of automated injection platforms in ensuring precise contrast delivery and procedural efficiency across imaging modalities.

- The Consumables segment is anticipated to be the fastest-growing product category, driven by recurring demand for syringes, tubing sets, and accessories required for each imaging procedure.

- The Dual Head Injectors segment dominated the type category with a 48.6% market share in 2025, supported by their ability to deliver multiple contrast agents or saline flush simultaneously, improving workflow efficiency in CT and cardiovascular imaging.

- The Syringeless Injectors segment is expected to witness the fastest growth during the forecast period, driven by reduced consumable costs, environmental sustainability, and operational efficiency.

- The Interventional Cardiology segment dominated the application category with a 36.8% market share in 2025, supported by high procedural volumes in coronary angiography and percutaneous coronary interventions requiring precise contrast delivery.

- The Interventional Neuroradiology segment is expected to witness strong growth, driven by increasing incidence of cerebrovascular diseases and expanding neurovascular intervention capabilities.

- The Hospitals segment dominated the end-use category with a 71.3% market share in 2025, supported by comprehensive imaging infrastructure, high procedural volumes, and multidisciplinary clinical teams.

- The Diagnostic Centers segment is expected to witness strong growth during the forecast period, driven by expansion of outpatient imaging services and cost-effective procedural delivery.

Market Size & Forecast

- Global Market Value (2025): USD 276.62 Million

- Expected Market Value (2033): USD 694.76 Million

- Forecast CAGR (2026–2033): 12.20%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and High Pressure Contrast Media Injectors Market Segmentation

|

Attributes |

High Pressure Contrast Media Injectors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Bayer AG (Germany) · Bracco Imaging S.p.A. (Italy) · Guerbet Group (France) · Medtron AG (Germany) · ulrich GmbH & Co. KG (Germany) · Nemoto Kyorindo Co., Ltd. (Japan) · Sino Medical-Device Technology Co., Ltd. (China) · Apollo RT Co., Ltd. (South Korea) · Anke High-Tech Co., Ltd. (China) · Shenzhen Seacrown Electromechanical Co., Ltd. (China) · Vivid Imaging Solutions (India) · Sequoia Healthcare (U.S.) |

|

Market Opportunities |

· Expansion of diagnostic imaging infrastructure in emerging markets with growing procedural volumes and healthcare modernization initiatives · Development of integrated, AI-enabled injector systems with enhanced workflow automation, dose optimization, and connectivity with imaging platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

High Pressure Contrast Media Injectors Market Trends

Trend: Integration of AI-Enabled Automation and Connectivity in Injector Systems

Clinical adoption of high pressure contrast media injectors continues to accelerate as technological innovations improve injection precision, workflow efficiency, and patient safety. Advanced injector platforms now feature integrated artificial intelligence algorithms for automated dose calculation based on patient parameters, real-time pressure monitoring, and predictive maintenance alerts. Wireless connectivity enables seamless integration with hospital information systems, PACS, and imaging equipment, facilitating standardized protocols and comprehensive procedure documentation.

For instance,

Bayer's Stellant FLEX CT Injection System incorporates advanced automation features including patient-specific protocol optimization and integrated safety monitoring, enabling radiologists to deliver consistent contrast enhancement while minimizing adverse events.

In addition, research demonstrates that automated contrast injection systems reduce variability in image quality, decrease contrast media waste, and improve diagnostic accuracy compared to manual injection techniques, supporting broader clinical adoption across radiology and interventional specialties. The integration of AI-enabled automation is expected to strengthen adoption of advanced injector platforms globally.

High Pressure Contrast Media Injectors Market Dynamics

Key Market Driver: Rising Demand for Advanced Diagnostic Imaging Procedures

The growing prevalence of cardiovascular diseases, oncological conditions, and neurological disorders requiring advanced diagnostic imaging is a primary driver of market growth. High pressure contrast media injectors enable precise, reproducible delivery of contrast agents during CT angiography, coronary angiography, and MRI procedures, ensuring optimal image quality for accurate diagnosis and treatment planning. The increasing procedural volumes in interventional cardiology and radiology departments, combined with the expansion of outpatient imaging services, are expanding the addressable market for injector systems.

For instance,

According to industry analysis, global CT scan volumes exceeded 400 million procedures annually by 2025, with contrast-enhanced studies representing a substantial proportion of diagnostic examinations. Rising demand for contrast-enhanced imaging is expected to strengthen adoption of high pressure injector technologies across healthcare facilities.

Key Restraint/Challenge: High Capital Investment and Maintenance Costs

The substantial upfront capital investment required for advanced injector systems, along with ongoing maintenance, software updates, and consumable costs, presents a significant barrier to adoption, particularly for smaller imaging centers and healthcare facilities in emerging markets. The total cost of ownership, including service contracts and consumable procurement, can limit the financial feasibility of upgrading legacy injection equipment.

For instance,

Healthcare facilities evaluating injector system adoption must balance the clinical benefits of advanced automation against significant capital expenditure, with premium systems from leading manufacturers requiring substantial initial investment compared to basic manual alternatives. High acquisition and operating costs may constrain adoption among budget-sensitive healthcare providers.

Key Market Opportunity: Expansion into Emerging Markets and Outpatient Imaging Centers

The development of cost-effective, modular injector systems is creating opportunities for adoption beyond large hospital radiology departments. Diagnostic imaging centers and outpatient facilities are increasingly incorporating automated injection platforms to improve procedural efficiency and patient throughput. Simultaneously, expanding healthcare infrastructure in Asia-Pacific, Latin America, and the Middle East is driving demand for advanced imaging capabilities in previously underserved markets.

For instance,

The Asia-Pacific diagnostic imaging equipment market is experiencing rapid growth, driven by healthcare modernization initiatives, increasing disease burden, and rising patient expectations for advanced diagnostic services. The expansion of imaging infrastructure in emerging markets is expected to create significant growth opportunities for high pressure contrast media injector manufacturers.

High Pressure Contrast Media Injectors Market Scope

The high pressure contrast media injectors market is segmented on the basis of product, type, application, and end-use.

By Product

On the basis of product, the High Pressure Contrast Media Injectors Market is segmented into injector systems and consumables. The Injector Systems segment dominated the market with a 62.4% market share in 2025, reflecting the critical role of automated injection platforms in ensuring precise contrast delivery and procedural efficiency across imaging modalities. Advanced injector systems with integrated safety features, dose management capabilities, and connectivity with imaging platforms are increasingly adopted in hospital radiology departments and cardiac catheterization laboratories. High procedure volumes and the need for standardized injection protocols contribute to segment leadership.

The Consumables segment is expected to witness the fastest growth from 2026 to 2033, driven by recurring demand for syringes, tubing sets, extension lines, and accessories required for each imaging procedure. The transition toward single-use, pre-filled syringes and disposable components to minimize cross-contamination risk is accelerating consumable adoption across healthcare facilities.

By Type

On the basis of type, the High Pressure Contrast Media Injectors Market is segmented into single head injectors, dual head injectors, and syringeless injectors. The Dual Head Injectors segment dominated the market with a 48.6% market share in 2025, supported by their ability to deliver multiple contrast agents or saline flush simultaneously, improving workflow efficiency in CT and cardiovascular imaging. Dual head configurations enable seamless contrast-saline mixing, bolus timing optimization, and reduced procedure times, making them the preferred choice for high-volume imaging centers and cardiac catheterization laboratories.

The Syringeless Injectors segment is expected to witness the fastest growth from 2026 to 2033, driven by reduced consumable costs, environmental sustainability, and operational efficiency. Syringeless technology eliminates the need for disposable syringes, reducing per-procedure costs and medical waste generation while maintaining injection precision and safety.

By Application

On the basis of application, the High Pressure Contrast Media Injectors Market is segmented into interventional cardiology, interventional radiology, endovascular surgery, and interventional neuroradiology. The Interventional Cardiology segment dominated the market with a 36.8% market share in 2025, supported by high procedural volumes in coronary angiography, percutaneous coronary interventions, and structural heart procedures requiring precise contrast delivery. The increasing prevalence of coronary artery disease, growing adoption of catheter-based interventions, and emphasis on optimized contrast protocols for patient safety contribute to segment leadership.

The Interventional Neuroradiology segment is expected to witness strong growth during the forecast period, driven by increasing incidence of cerebrovascular diseases, expanding neurovascular intervention capabilities, and growing adoption of mechanical thrombectomy for acute ischemic stroke. Technological advancements in neuroimaging and the development of specialized contrast delivery protocols are supporting segment expansion.

By End-use

On the basis of end-use, the High Pressure Contrast Media Injectors Market is segmented into hospitals and diagnostic centers. The Hospitals segment dominated the market with a market share of 71.3% in 2025, driven by comprehensive imaging infrastructure, high procedural volumes, and multidisciplinary clinical teams. Hospitals serve as primary centers for complex interventional procedures requiring advanced injector systems, inpatient monitoring, and specialized postoperative care. The concentration of cardiology, radiology, and neurology imaging programs within hospital systems contributes to high equipment utilization and consumable demand.

The Diagnostic Centers segment is expected to witness the fastest growth from 2026 to 2033, driven by expansion of outpatient imaging services, cost-effective procedural delivery, and increasing patient preference for convenient, accessible diagnostic facilities. The development of compact, automated injector systems suitable for ambulatory settings is enabling high-quality contrast-enhanced imaging outside traditional hospital environments.

High Pressure Contrast Media Injectors Market Regional Analysis

North America dominated the high pressure contrast media injectors market with a revenue share of 38.7% in 2025, supported by high adoption rates of advanced imaging technologies, established reimbursement frameworks, and the presence of leading market players including Bayer AG and Bracco Imaging. Favorable regulatory pathways, robust clinical training infrastructure, and extensive procedural volumes in interventional cardiology and radiology contribute to regional market leadership.

U.S. High Pressure Contrast Media Injectors Market Insight

The U.S. high pressure contrast media injectors market benefits from the highest installed base of advanced CT and angiography systems globally, extensive imaging procedure volumes, and strong clinical evidence supporting automated injection protocols. Academic medical centers, large health systems, and specialty cardiovascular practices continue to invest in advanced injector platforms with integrated safety features and connectivity capabilities. Favorable Medicare and commercial payer reimbursement supports procedural volumes and equipment investment. The U.S. accounted for 82.4% of the North American market share in 2025.

Europe High Pressure Contrast Media Injectors Market Insight

The Europe high pressure contrast media injectors market remains a major contributor, with strong hospital-based imaging programs across Germany, France, the U.K., and Italy. Growing adoption of integrated injector systems with AI-enabled automation is improving workflow efficiency and standardizing contrast delivery protocols across public and private healthcare systems. Cross-disciplinary guidelines and structured training pathways are improving procedural outcomes and patient safety.

U.K. High Pressure Contrast Media Injectors Market Insight

The U.K. high pressure contrast media injectors market is characterized by expanding imaging programs within NHS hospitals and private healthcare facilities. Investment in advanced injector platforms for cardiac CT, CT angiography, and interventional procedures is improving access to high-quality diagnostic imaging and reducing procedural variability.

Germany High Pressure Contrast Media Injectors Market Insight

Germany's robust hospital infrastructure and advanced imaging capabilities support comprehensive contrast injection programs across radiology and interventional cardiology departments. Strong clinical training networks and favorable reimbursement frameworks contribute to high procedure volumes and technology adoption. Germany accounted for the largest market share within Europe at 24.6% in 2025.

Asia-Pacific High Pressure Contrast Media Injectors Market Insight

The Asia-Pacific high pressure contrast media injectors market is poised for rapid growth with a CAGR of 14.35% during the forecast period, driven by expanding healthcare infrastructure, rising demand for diagnostic imaging procedures, and increasing healthcare expenditure. Private healthcare systems in China, Japan, India, and South Korea are investing in advanced imaging capabilities to meet growing patient demand and improve diagnostic accuracy.

Japan High Pressure Contrast Media Injectors Market Insight

The Japan high pressure contrast media injectors market benefits from advanced healthcare infrastructure, strong technological expertise, and favorable reimbursement for imaging procedures. Automated injector systems are well-established across hospital radiology departments, with expanding applications in cardiac imaging and oncological staging.

China High Pressure Contrast Media Injectors Market Insight

The China high pressure contrast media injectors market is experiencing rapid growth driven by healthcare modernization initiatives, expanding hospital networks, and increasing patient demand for advanced diagnostic imaging. Domestic injector system manufacturers are complementing imported platforms, improving market accessibility and price competitiveness. China is expected to record the fastest growth within Asia-Pacific at a CAGR of 15.20% from 2026 to 2033.

High Pressure Contrast Media Injectors Market Share

The high pressure contrast media injectors industry is primarily led by well-established companies, including:

- Bayer AG (Germany)

- Bracco Imaging S.p.A. (Italy)

- Guerbet Group (France)

- Medtron AG (Germany)

- ulrich GmbH & Co. KG (Germany)

- Nemoto Kyorindo Co., Ltd. (Japan)

- Sino Medical-Device Technology Co., Ltd. (China)

- Apollo RT Co., Ltd. (South Korea)

- Anke High-Tech Co., Ltd. (China)

- Shenzhen Seacrown Electromechanical Co., Ltd. (China)

- Vivid Imaging Solutions (India)

- Sequoia Healthcare (U.S.)

Latest Developments in High Pressure Contrast Media Injectors Market

- In March 2026, Bayer AG announced the launch of its next-generation Stellant FLEX CT Injection System with enhanced AI-powered dose optimization algorithms and expanded connectivity features. The upgraded platform enables seamless integration with hospital PACS and electronic health records, improving workflow efficiency and procedural documentation across radiology departments.

- In January 2026, Guerbet Group completed the acquisition of a specialized contrast delivery technology company to strengthen its injector systems portfolio. The acquisition supports Guerbet's strategy to expand its presence in the high pressure contrast media injectors market and enhance its integrated imaging solutions offerings.

- In November 2025, Bracco Imaging S.p.A. received U.S. FDA 510(k) clearance for its ACIST Empowering CVi System with advanced pressure monitoring and automated air detection capabilities. The clearance expands Bracco's cardiovascular imaging portfolio and strengthens its position in the interventional cardiology injector segment.

- In September 2025, Medtron AG introduced its Accutron HP-D Dual Head Injector System with wireless connectivity and tablet-based control interface at the European Congress of Radiology. The system features enhanced safety protocols and compatibility with multiple contrast media formulations across CT and angiography applications.

- In June 2025, ulrich GmbH & Co. KG announced a strategic partnership with a leading hospital network in Asia-Pacific to deploy its injector systems across multiple imaging centers. The partnership supports ulrich's expansion into emerging markets and reinforces its commitment to advancing contrast delivery technology globally.

- In April 2025, Nemoto Kyorindo Co., Ltd. launched its Dual Shot GX7 Injector System in European markets following CE marking approval. The system incorporates advanced bolus tracking technology and patient-specific protocol optimization for improved image quality in CT angiography procedures.

- In February 2025, Sino Medical-Device Technology Co., Ltd. announced the installation of its 10,000th high pressure injector system in healthcare facilities across China and Southeast Asia. The milestone reflects accelerating adoption of domestically manufactured contrast delivery systems in the Asia-Pacific region.

- In December 2024, Bayer AG announced expanded manufacturing capacity at its contrast media injector production facility in Germany to meet growing global demand. The investment supports increased production of Stellant and Medrad injector platforms for distribution across North America, Europe, and Asia-Pacific markets.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.