Global High Viscosity Biologics Fill Finish Market

Market Size in USD Billion

USD

1.68 Billion

USD

5.89 Billion

2025

2033

USD

1.68 Billion

USD

5.89 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.68 Billion | |

| USD 5.89 Billion | |

| % | |

|

High-Viscosity Biologics Fill-Finish Market Overview

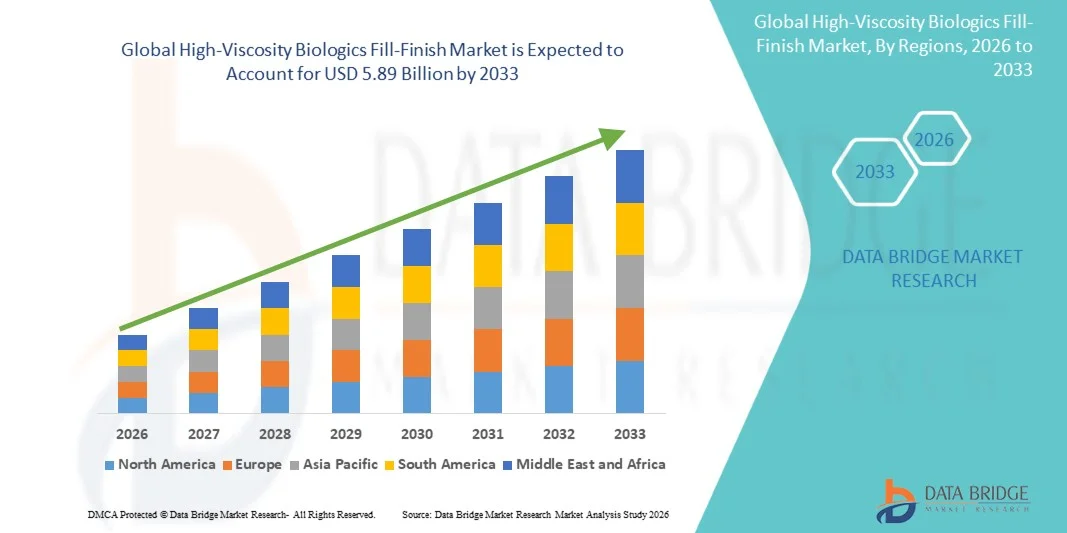

The High-Viscosity Biologics Fill-Finish Market was valued at USD 1.68 billion in 2025 and is projected to reach USD 5.89 billion by 2033, growing at a CAGR of 17.00% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for advanced biologics manufacturing capabilities, increasing adoption of high-viscosity biologics such as monoclonal antibodies and injectable therapies, and expanding investments in aseptic fill-finish technologies across pharmaceutical and biotechnology industries.

The rapid growth of biologics, including complex therapies, biosimilars, and next-generation injectable drugs, combined with increasing demand for efficient and scalable manufacturing solutions, is encouraging pharmaceutical companies and contract manufacturing organizations to adopt specialized high-viscosity fill-finish systems. Advanced automated filling technologies, robotic systems, and improved containment solutions are enabling manufacturers to handle highly concentrated biologic formulations with greater accuracy, sterility, and reduced product loss. These technologies are increasingly supporting the production of large-volume biologics, personalized medicines, and emerging therapies while improving manufacturing efficiency and regulatory compliance across global markets.

Key Market Trends & Insights

- North America dominated the High-Viscosity Biologics Fill-Finish Market with the largest revenue share of 35.6% in 2025, supported by the presence of advanced biopharmaceutical manufacturing infrastructure, strong adoption of automated fill-finish technologies, and significant investments in biologics and injectable drug production. The region benefits from a strong presence of biologics manufacturers, contract development and manufacturing organizations (CDMOs), and regulatory-driven adoption of advanced aseptic processing solutions.

- The aseptic filling systems segment dominated the market with a 42.3% share in 2025, owing to increasing demand for sterile manufacturing solutions for complex biologics, monoclonal antibodies, vaccines, and injectable therapies.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 9.1% from 2026 to 2033, fueled by expanding biologics manufacturing capacity, rising healthcare investments, increasing adoption of biosimilars, and growing pharmaceutical outsourcing activities in countries such as China, India, South Korea, and Japan. The region is witnessing rapid development of new biologics production facilities requiring advanced fill-finish capabilities.

- Advanced robotic filling systems are the fastest-growing filling technology segment, projected to register a CAGR of 10.2% from 2026 to 2033, reflecting increasing demand for automation, improved precision, reduced human intervention, and enhanced sterility assurance in high-value biologics manufacturing. Pharmaceutical companies are increasingly adopting robotic systems to support flexible, scalable, and high-throughput production of complex injectable therapies.

- Monoclonal antibodies segment dominates the product type category with a 38.7% revenue share in 2025, supported by increasing demand for targeted therapies, immunological treatments, and biologic drugs for oncology, autoimmune diseases, and chronic conditions. The growing pipeline of antibody-based therapeutics and expansion of large-scale biologics manufacturing facilities are driving the leading position of this segment.

Market Size & Forecast

- Global Market Value (2025): USD 1.68 Billion

- Expected Market Value (2033): USD 5.89 Billion

- Forecast CAGR (2026–2033): 17.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and High-Viscosity Biologics Fill-Finish Market Segmentation

|

Attributes |

High-Viscosity Biologics Fill-Finish Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Thermo Fisher Scientific (U.S.) |

|

Market Opportunities |

· Expansion of Monoclonal Antibodies, Biosimilars, and Next-Generation Biologics · Increasing Adoption of Automated and Robotic Fill-Finish Technologies · Growth of Outsourced Biologics Manufacturing and CDMO Expansion |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

High-Viscosity Biologics Fill-Finish Market Trends

Trend: Growth in Advanced Biologics Manufacturing and Automated Fill-Finish Technologies

The High-Viscosity Biologics Fill-Finish Market is witnessing strong growth as pharmaceutical and biotechnology companies increasingly adopt advanced filling technologies to support the production of complex biologic therapies, including monoclonal antibodies, vaccines, recombinant proteins, and gene & cell therapy products. The rising demand for injectable biologics, increasing biologics pipelines, and expansion of contract manufacturing organizations (CMOs/CDMOs) are accelerating investments in high-precision fill-finish platforms. Manufacturers are increasingly adopting automated and robotic filling systems to improve sterility assurance, reduce product loss, and enhance operational efficiency for high-viscosity formulations that are more challenging to process compared with traditional liquid drugs. For instance, pharmaceutical companies are investing in advanced aseptic processing technologies such as isolator-based filling systems and robotic platforms to meet stringent regulatory expectations from agencies including the U.S. FDA and European Medicines Agency (EMA). The growing commercialization of biologics and personalized therapies is further increasing demand for flexible, scalable fill-finish solutions.

High-Viscosity Biologics Fill-Finish Market Dynamics

Key Market Driver: Rising Demand for Biologics, Monoclonal Antibodies, and Advanced Therapies

The rapid expansion of the biologics industry is a major factor driving demand for high-viscosity biologics fill-finish technologies. Complex biologics such as monoclonal antibodies, antibody-drug conjugates (ADCs), and cell and gene therapies require highly controlled filling processes due to their sensitivity, viscosity characteristics, and strict sterility requirements. The increasing prevalence of chronic diseases, including cancer and autoimmune disorders, has accelerated adoption of biologic medicines, creating a need for advanced manufacturing infrastructure. According to industry estimates, biologics account for a significant share of the global pharmaceutical pipeline, with thousands of biologic candidates under development, increasing the requirement for specialized fill-finish capabilities. Biopharmaceutical companies and CDMOs are expanding manufacturing capacity to support commercial-scale production. For instance, companies such as Thermo Fisher Scientific and Lonza Group have continued investing in biologics manufacturing infrastructure and advanced processing capabilities to support increasing demand for injectable therapies.

Key Restraint/Challenge: High Capital Investment and Complex Manufacturing Requirements

A major challenge in the High-Viscosity Biologics Fill-Finish Market is the significant investment required for advanced aseptic filling infrastructure. High-viscosity biologic products often require specialized equipment capable of handling difficult flow characteristics, maintaining product integrity, and ensuring precise dosing accuracy. Modern fill-finish facilities require advanced cleanroom environments, automated inspection systems, isolators, robotics, and highly trained technical personnel, resulting in substantial capital expenditure. Smaller pharmaceutical manufacturers and emerging biotechnology companies may face difficulties in adopting these technologies due to high installation costs, validation requirements, and ongoing maintenance expenses. In addition, regulatory compliance requirements for sterile manufacturing increase operational complexity. Facilities must undergo extensive qualification and validation processes to comply with global standards, increasing development timelines and costs.

Key Market Opportunity: Integration of Automation, Robotics, and Digital Manufacturing Platforms

The integration of automation, robotics, and digital technologies presents a significant growth opportunity for the High-Viscosity Biologics Fill-Finish market. Automated fill-finish platforms enable improved accuracy, reduced contamination risks, enhanced batch consistency, and increased production efficiency. The adoption of robotic filling systems and digital monitoring solutions is expanding as manufacturers seek to improve scalability and reduce human intervention in sterile processing environments. Artificial intelligence (AI)-based process monitoring, real-time analytics, and predictive maintenance are also being integrated into biologics manufacturing operations to optimize production performance.

High-Viscosity Biologics Fill-Finish Market Scope

The High-Viscosity Biologics Fill-Finish Market is segmented on the basis of filling technology and product type.

- By Filling Technology

On the basis of filling technology, the High-Viscosity Biologics Fill-Finish Market is segmented into aseptic filling systems, automated fill-finish systems, manual & semi-automated filling systems, and advanced robotic filling systems. The aseptic filling systems segment dominated the market with a 42.3% share in 2025, owing to increasing demand for sterile manufacturing solutions for complex biologics, monoclonal antibodies, vaccines, and injectable therapies. These systems provide high contamination control, improved product stability, and compliance with stringent regulatory requirements from agencies such as the U.S. FDA and EMA. The growing adoption of isolator-based technologies, restricted access barrier systems (RABS), and advanced sterile processing environments across pharmaceutical manufacturing facilities is strengthening the dominance of this segment. Increasing biologics production capacity expansion by pharmaceutical companies and CDMOs is further supporting market growth.

The advanced robotic filling systems segment is projected to register the fastest growth at a CAGR of 10.2% from 2026 to 2033, driven by increasing adoption of automation, robotics, and digital manufacturing technologies in biologics production. Robotic systems enable higher filling precision, reduced human intervention, improved sterility assurance, and enhanced operational efficiency, making them highly suitable for high-value biologic products and advanced therapies. The rising commercialization of gene and cell therapies, personalized medicines, and small-batch biologics is accelerating demand for flexible robotic fill-finish platforms. In addition, integration of artificial intelligence, real-time monitoring, and automated inspection technologies is further enhancing adoption across modern pharmaceutical facilities.

- By Product Type

On the basis of product type, the High-Viscosity Biologics Fill-Finish Market is segmented into monoclonal antibodies, vaccines, recombinant proteins, gene & cell therapy products, and other biologics. The Monoclonal Antibodies segment dominated the market with a 38.7% share in 2025, supported by increasing demand for targeted biologic therapies in oncology, autoimmune diseases, and chronic disease management. Monoclonal antibodies represent one of the largest and fastest-growing categories of biologic medicines, requiring specialized fill-finish technologies due to their high viscosity, sensitivity, and strict sterility requirements. The expansion of antibody-based drug pipelines, rising approvals of biologic therapies, and increasing manufacturing investments by pharmaceutical companies and CDMOs are driving segment leadership.

The Gene & Cell Therapy Products segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, driven by increasing investments in advanced therapy medicinal products (ATMPs), personalized medicine, and next-generation biologics. Gene and cell therapies require highly specialized fill-finish solutions capable of handling sensitive formulations, smaller batch sizes, and complex manufacturing requirements. The growing number of clinical trials and commercial launches of advanced therapies is increasing demand for flexible and precise filling technologies. In addition, rising adoption of modular manufacturing systems and automated solutions for advanced therapies is expected to accelerate segment expansion globally.

High-Viscosity Biologics Fill-Finish Market Regional Analysis

North America dominated the High-Viscosity Biologics Fill-Finish Market and accounted for the largest revenue share of 35.6% in 2025, supported by advanced biopharmaceutical manufacturing infrastructure, strong adoption of automated fill-finish technologies, and significant investments in biologics and injectable drug production. The region benefits from the presence of leading biologics manufacturers, contract development and manufacturing organizations (CDMOs), and advanced pharmaceutical facilities equipped with aseptic processing capabilities. Increasing demand for monoclonal antibodies, biosimilars, and high-concentration biologic therapies, along with strict regulatory requirements for sterile manufacturing, is driving the adoption of advanced high-viscosity fill-finish solutions across the U.S. and Canada.

U.S. High-Viscosity Biologics Fill-Finish Market Insight

The U.S. high-viscosity biologics fill-finish market is witnessing strong growth due to rising investments in biologics manufacturing capacity, increasing production of injectable therapies, and growing adoption of automated aseptic filling technologies. The country’s strong pharmaceutical and biotechnology ecosystem, along with the presence of major biologics developers and CDMOs, is accelerating demand for advanced fill-finish systems capable of handling highly concentrated and viscous formulations. In addition, increasing focus on manufacturing efficiency, contamination control, and scalable production of monoclonal antibodies and next-generation biologics is supporting market expansion across the U.S.

Europe High-Viscosity Biologics Fill-Finish Market Insight

The Europe High-Viscosity Biologics Fill-Finish market remains a major contributor to global revenue, driven by strong pharmaceutical manufacturing capabilities, technological innovation, and increasing demand for advanced biologics production solutions. The region benefits from the presence of established biopharmaceutical companies, CDMOs, and advanced sterile manufacturing facilities. Growing investments in automated filling systems, increasing adoption of biosimilars, and stringent regulatory standards for biologic drug manufacturing are encouraging pharmaceutical companies to upgrade their fill-finish infrastructure across Europe.

U.K. High-Viscosity Biologics Fill-Finish Market Insight

The U.K. high-viscosity biologics fill-finish market is experiencing steady growth, supported by rising investments in biotechnology research, biologics manufacturing, and advanced pharmaceutical processing technologies. Increasing demand for injectable biologics, personalized medicines, and outsourced manufacturing services is contributing to the adoption of high-precision fill-finish solutions. Furthermore, the expansion of biopharmaceutical innovation and growing collaborations between pharmaceutical companies and CDMOs are strengthening the U.K.’s position in the biologics manufacturing ecosystem.

Germany High-Viscosity Biologics Fill-Finish Market Insight

The Germany high-viscosity biologics fill-finish market is expanding steadily due to the country’s strong pharmaceutical manufacturing base, advanced engineering capabilities, and increasing adoption of next-generation aseptic processing technologies. Pharmaceutical companies and contract manufacturers are investing in automated fill-finish systems to improve production efficiency, maintain sterility, and support the growing demand for biologic therapies. Continuous advancements in manufacturing automation, quality control systems, and biologics production infrastructure are further driving market growth in Germany.

Asia-Pacific High-Viscosity Biologics Fill-Finish Market Insight

The Asia-Pacific high-viscosity biologics fill-finish market is expected to witness rapid growth, registering a CAGR of 9.1% from 2026 to 2033, fueled by expanding biologics manufacturing capacity, rising healthcare investments, increasing adoption of biosimilars, and growing pharmaceutical outsourcing activities across China, India, South Korea, and Japan. The region is witnessing rapid development of new biologics production facilities, increasing demand for advanced aseptic filling technologies, and growing investments by pharmaceutical companies seeking cost-effective manufacturing solutions. Rising healthcare access and increasing demand for injectable biologic medicines are further supporting regional market expansion.

Japan High-Viscosity Biologics Fill-Finish Market Insight

The Japan high-viscosity biologics fill-finish market is witnessing consistent growth due to increasing investments in biotechnology, pharmaceutical innovation, and advanced manufacturing technologies. Japanese pharmaceutical companies are adopting automated fill-finish platforms to improve precision, reduce contamination risks, and support the production of complex biologic drugs. Moreover, rising demand for biologics, aging population healthcare needs, and advancements in regenerative medicine and specialty therapies are contributing to market growth.

China High-Viscosity Biologics Fill-Finish Market Insight

The China High-Viscosity Biologics Fill-Finish market is growing rapidly, driven by expanding biopharmaceutical manufacturing capabilities, increasing biosimilar development, and rising investments in advanced pharmaceutical production facilities. Growing demand for injectable biologics, increasing government support for domestic drug manufacturing, and the expansion of CDMO services are accelerating adoption of high-viscosity fill-finish technologies. In addition, China’s growing biotechnology sector and increasing focus on self-sufficient pharmaceutical production are positioning the country as a key growth market for high-viscosity biologics fill-finish solutions.

High-Viscosity Biologics Fill-Finish Market Share

The high-viscosity biologics fill-finish industry is primarily led by well-established companies, including:

- Thermo Fisher Scientific (U.S.)

- West Pharmaceutical Services (U.S.)

- Syntegon Technology (Germany)

- IMA Group (Italy)

- Bausch+Ströbel (Germany)

- GEA Group (Germany)

- SP Industries (U.S.)

- Stevanato Group (Italy)

- Gerresheimer AG (Germany)

- Datwyler (Switzerland)

- Nipro Corporation (Japan)

- Shandong Pharmaceutical Glass Co., Ltd. (China)

- Synaffix (Netherlands)

- Recipharm (Sweden)

- Lonza Group (Switzerland)

- Catalent (U.S.)

- Samsung Biologics (South Korea)

- Boehringer Ingelheim (Germany)

- WuXi Biologics (China)

- Fujifilm Diosynth Biotechnologies (U.S./Japan)

- Rentschler Biopharma (Germany)

- AGC Biologics (U.S.)

- Cytiva (U.S.)

- Körber Pharma (Germany)

- Syntegon Technology Filling Systems (Germany)

- IMA Pharma (Italy)

- OPTIMA packaging group (Germany)

- Marchesini Group (Italy)

- Romaco Group (Germany)

- ACIC Pharmaceuticals (India)

- Tofflon Science and Technology (China)

- BSP Pharmaceuticals (Italy)

- Pall Corporation (U.S.)

- Sartorius (Germany)

Latest Developments in High-Viscosity Biologics Fill-Finish Market

- In September 2025, Moog Inc. has unveiled its latest motion systems all electric E60 Series and the electro pneumatic P60 Series, setting a new benchmark for simulation across aviation, land, and maritime training with support for up to 14,000 kg loads and high fidelity motion for Level D flight simulators and other professional uses. The upgraded platforms deliver enhanced reliability, compact design and sustained operational uptime, reflecting modernized electronics and sustainable operation. These new systems strengthen Moog’s market leadership in simulation motion technology by boosting performance, energy efficiency, and usability

- In January 2025, Exail Technologies has acquired Leukos, a French photonics specialist known for pulsed micro lasers, supercontinuum laser sources, ultrafast lasers, and simulation-enabled optical systems, strengthening its technological and industrial capabilities in advanced laser and simulation technologies. The deal integrates Leukos’s expertise with Exail’s photonics, optical, and simulation platforms, broadening product offerings for applications in biophotonics, microelectronics, and high-fidelity training simulations. This strategic acquisition accelerates Exail’s innovation in high-tech technologies, creating synergies that expand its reach in scientific, industrial, and simulation applications while reinforcing its position as a leading advanced-technology provider

- In November 2025, IPG Automotive launched CarMaker 15.0, the latest version of its driving simulation software used for virtual vehicle development. The new release improves simulation accuracy by integrating virtual electronic control units (vECUs), allowing engineers to test software and vehicle systems at earlier development stages. It also includes enhanced sensor models and improved endurance testing capabilities for ADAS and autonomous vehicles. This development strengthens IPG Automotive’s position in the driving simulator market, as CarMaker enables automotive manufacturers to perform complex vehicle tests in a virtual driving environment instead of physical road testing.

- In November 2024, IPG Automotive released CarMaker 14.0, introducing new simulation capabilities including advanced sensor models and more realistic virtual environments. The update allows developers to simulate complex traffic scenarios involving pedestrians, vehicles, and different weather conditions. These features help automotive companies test ADAS and autonomous driving systems more efficiently in driving simulators, reducing development time and cost. The upgrade also expanded simulation capabilities for heavy-duty vehicles using the TruckMaker platform.

- In June 2023, IPG Automotive participated in the UNICARagil research project, collaborating with universities and industry partners to develop automated vehicle architectures. The company contributed its CarMaker driving simulation platform to support simulation and validation of automated driving systems in Software-in-the-Loop (SIL) and Hardware-in-the-Loop (HIL) environments. This collaboration demonstrates the application of High-Viscosity Biologics Fill-Finish in research and development of autonomous mobility solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.