Global Higher Alpha Olefins Market

Market Size in USD Billion

USD

3.99 Billion

USD

5.50 Billion

2024

2032

USD

3.99 Billion

USD

5.50 Billion

2024

2032

Forecast Period |

2025 - 2032 |

Market Size (Base Year) |

USD 3.99 Billion |

Market Size (Forecast Year) |

USD 5.50 Billion |

CAGR |

% |

Major Markets Players |

|

Higher Alpha Olefins Market Size

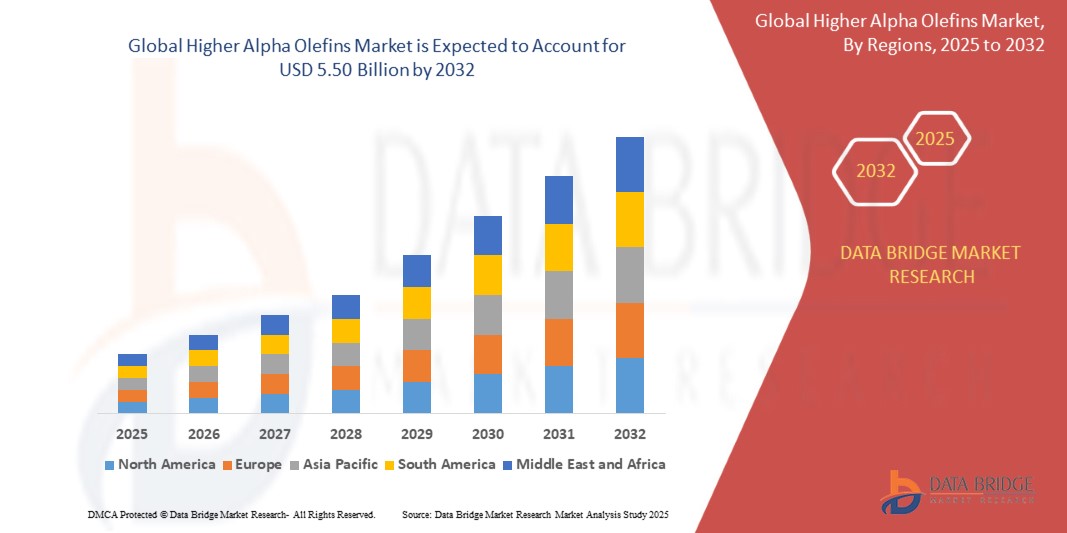

- The global higher alpha olefins market size was valued at USD 3.99 billion in 2024 and is expected to reach USD 5.50 billion by 2032, at a CAGR of 4.10% during the forecast period

- The market growth is largely fueled by the rising demand for polyethylene comonomers, synthetic lubricants, and specialty chemicals, driven by expanding packaging, automotive, and construction industries worldwide

- Furthermore, increasing focus on lightweight, durable, and energy-efficient materials, along with technological advancements in alpha olefins production, is accelerating product adoption across multiple industrial applications, thereby significantly boosting the industry's growth

Higher Alpha Olefins Market Analysis

- Higher alpha olefins are essential chemical intermediates produced through the oligomerization of ethylene and are widely used in manufacturing polyethylene, lubricants, surfactants, and specialty chemicals. Their unique linear structure offers desirable properties such as flexibility, strength, and improved performance in end-use products

- The escalating demand for higher alpha olefins is primarily driven by the growing need for advanced packaging solutions, high-performance synthetic lubricants, and eco-friendly surfactants, supported by increased industrialization, rising consumer goods demand, and sustainable material trends

- North America dominated the higher alpha olefins market with a share of 36.2% in 2024, due to the significant demand for polyethylene comonomers and synthetic lubricants, along with the region’s strong presence of major petrochemical companies

- Asia-Pacific is expected to be the fastest growing region in the higher alpha olefins market during the forecast period due to rising industrialization, expanding polymer demand, and increasing investments in chemical manufacturing across countries such as China, India, and Japan

- C6-C8 segment dominated the market with a market share of 49.2% in 2024, due to its extensive use as a comonomer in polyethylene production. These olefins, particularly hexene and octene, are critical for enhancing the mechanical strength, flexibility, and processability of polyethylene, making them essential in packaging films, industrial containers, and high-performance materials. Their wide compatibility with various polymer formulations and consistent demand from the plastics industry have reinforced the dominance of the C6-C8 segment

Report Scope and Higher Alpha Olefins Market Segmentation

|

Attributes |

Higher Alpha Olefins Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Higher Alpha Olefins Market Trends

“Rising High-Purity Demand in Polyethylene and Specialty Application”

- A significant and accelerating trend in the global higher alpha olefins market is the rising demand for high-purity HAOs in polyethylene comonomers, specialty chemicals, and environmentally sustainable formulations such as biodegradable surfactants and synthetic lubricants

- For instance, companies such as Chevron Phillips Chemical and Shell are investing in advanced catalytic processes and cleaner production technologies to supply high-purity HAOs for use in packaging films, containers, and high-performance plastics

- The adoption of HAOs in the manufacture of polyethylene enhances polymer flexibility, impact strength, and processability, supporting the shift toward lighter, more durable, and recyclable packaging solutions

- Regulatory pressures such as REACH in Europe and FDA guidelines in the U.S. are prompting manufacturers to innovate with low-toxicity, high-purity HAO products, driving the development of new grades and applications

- This trend toward sustainable materials and high-performance intermediates is fundamentally reshaping product development and supply chain strategies in the chemical industry. Companies such as INEOS and Sasol are expanding capacity and integrating downstream operations to meet growing demand for specialty HAOs in lubricants, oilfield chemicals, and detergent alcohols

- The demand for HAOs that offer enhanced environmental compatibility, superior performance, and regulatory compliance is growing rapidly across both established and emerging markets, as industries increasingly prioritize sustainability and advanced material properties

Higher Alpha Olefins Market Dynamics

Driver

“Industrial Growth and Expanding Applications in Packaging and Chemicals”

- The expansion of global industrial activity, coupled with the growing use of HAOs in packaging, construction, automotive, and specialty chemical sectors, is a significant driver for market growth

- For instance, companies such as ExxonMobil and Sasol are scaling up production to supply HAOs for use in linear low-density polyethylene (LLDPE), high-density polyethylene (HDPE), and a wide range of specialty chemicals

- As manufacturers seek materials with improved flexibility, durability, and process efficiency, HAOs provide essential properties for applications such as flexible packaging, automotive lubricants, and oilfield drilling fluids

- The trend toward modernization and technological advancement in emerging economies is making HAOs critical inputs for infrastructure, consumer goods, and high-value specialty products

- The convenience of using HAOs in diverse applications, coupled with ongoing investments in production technology and supply chain optimization, is propelling market expansion. The rise of sustainable packaging and advanced chemical formulations further contributes to the growing adoption of HAOs

Restraint/Challenge

“Competition from Substitutes and Feedstock Price Volatility”

- Competition from substitute materials such as bio-based olefins and alternative comonomers, as well as volatility in ethylene and other feedstock prices, poses a significant challenge to the higher alpha olefins market

- For instance, fluctuations in global ethylene supply and demand, along with the emergence of bio-based and recycled alternatives, have led companies such as INEOS and Chevron Phillips Chemical to diversify sourcing strategies and invest in risk management

- Addressing these challenges through innovation in process efficiency, product differentiation, and sustainable sourcing is crucial for maintaining competitiveness. Companies are focusing on developing advanced catalytic systems and integrating bio-based feedstocks to reduce dependency on traditional raw materials and mitigate price risks

- The high cost and complexity of upgrading production facilities to meet environmental and regulatory standards can be a barrier for smaller producers and new entrants

- Overcoming these challenges through industry collaboration, technology partnerships, and the development of high-value specialty grades will be vital for sustained market growth and resilience in the face of market fluctuations

Higher Alpha Olefins Market Scope

The market is segmented on the basis of type and application.

• By Type

On the basis of type, the higher alpha olefins market is segmented into C6-C8, C10-C14, and C16. The C6-C8 segment dominated the market with the largest revenue share of 49.2% in 2024, driven by its extensive use as a comonomer in polyethylene production. These olefins, particularly hexene and octene, are critical for enhancing the mechanical strength, flexibility, and processability of polyethylene, making them essential in packaging films, industrial containers, and high-performance materials. Their wide compatibility with various polymer formulations and consistent demand from the plastics industry have reinforced the dominance of the C6-C8 segment.

The C10-C14 segment is anticipated to witness the fastest growth rate from 2025 to 2032, fueled by rising consumption in the production of high-performance lubricants, synthetic oils, and specialty chemicals. These olefins provide superior viscosity properties, oxidation stability, and energy efficiency, making them highly sought after in automotive and industrial lubricant applications. Additionally, their growing role in the formulation of surfactants and detergents for cleaning and personal care products contributes to the strong growth outlook for the C10-C14 segment.

• By Application

On the basis of application, the higher alpha olefins market is segmented into polyethylene comonomers, lubricants & synthetic oils, detergents & surfactants, and other applications. The polyethylene comonomers segment held the largest market revenue share in 2024, primarily due to the extensive use of alpha olefins such as hexene and octene in enhancing the physical properties of polyethylene products. The demand for lightweight, durable, and flexible plastic materials in packaging, automotive, and construction sectors continues to drive significant consumption of alpha olefins in this application segment.

The lubricants & synthetic oils segment is projected to record the fastest CAGR from 2025 to 2032, supported by the growing need for advanced lubricants with superior thermal stability, fuel efficiency, and reduced emissions. Alpha olefins serve as key intermediates in the production of high-performance synthetic base oils, which are increasingly used in automotive, aerospace, and industrial equipment sectors. The expanding global focus on energy efficiency, sustainability, and improved equipment performance is expected to drive strong growth in this application area.

Higher Alpha Olefins Market Regional Analysis

- North America dominated the higher alpha olefins market with the largest revenue share of 36.2% in 2024, driven by the significant demand for polyethylene comonomers and synthetic lubricants, along with the region’s strong presence of major petrochemical companies

- The growing use of higher alpha olefins in packaging materials, industrial lubricants, and surfactants is supported by advanced refining infrastructure, technological innovation, and increasing investments in polymer production

- In addition, favorable economic conditions, expanding automotive and construction industries, and the rising adoption of eco-friendly, high-performance materials continue to fuel market growth across the U.S. and Canada

U.S. Higher Alpha Olefins Market Insight

The U.S. higher alpha olefins market captured the largest revenue share within North America in 2024, driven by substantial production capacity, technological expertise, and robust demand for polyethylene and lubricant applications. The country’s advanced chemical manufacturing sector, combined with abundant shale gas resources, ensures a steady supply of raw materials for alpha olefins production. The growing emphasis on lightweight plastics, high-performance synthetic oils, and energy-efficient solutions across packaging, automotive, and industrial sectors continues to strengthen the U.S. market

Europe Higher Alpha Olefins Market Insight

The Europe higher alpha olefins market is projected to expand at a considerable CAGR throughout the forecast period, fueled by stringent environmental regulations, increased demand for sustainable packaging, and the rising consumption of advanced lubricants. European manufacturers are increasingly adopting alpha olefins for producing eco-friendly materials, particularly in automotive, consumer goods, and construction applications. The region’s focus on energy efficiency and circular economy principles further drives the integration of alpha olefins in specialty chemicals and polymers

Germany Higher Alpha Olefins Market Insight

The Germany higher alpha olefins market is expected to witness steady growth during the forecast period, supported by the country’s strong chemical and automotive industries. Germany’s emphasis on innovative materials, coupled with growing demand for lightweight plastics and advanced lubricants, fuels alpha olefins consumption. The market is also benefiting from sustainable initiatives promoting low-emission products and efficient production technologies

Asia-Pacific Higher Alpha Olefins Market Insight

The Asia-Pacific higher alpha olefins market is expected to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by rising industrialization, expanding polymer demand, and increasing investments in chemical manufacturing across countries such as China, India, and Japan. Rapid growth in the packaging, automotive, and construction sectors, combined with favorable government policies supporting domestic production, is accelerating alpha olefins consumption in the region

Japan Higher Alpha Olefins Market Insight

The Japan higher alpha olefins market is gaining momentum, supported by the country’s advanced materials sector and growing demand for high-quality polyethylene and specialty lubricants. Japan’s focus on technological innovation, coupled with its strong automotive and electronics industries, is driving alpha olefins adoption for lightweight, durable, and energy-efficient products. Additionally, sustainability initiatives and increasing reliance on high-performance synthetic oils contribute to market growth

China Higher Alpha Olefins Market Insight

The China higher alpha olefins market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid industrial expansion, large-scale polymer production, and significant investments in petrochemical infrastructure. China’s robust demand for packaging materials, construction products, and automotive components is fueling alpha olefins consumption. The country’s role as a major manufacturing hub, combined with efforts to enhance energy efficiency and promote advanced chemical products, continues to drive strong market growth in China.

Higher Alpha Olefins Market Share

The higher alpha olefins industry is primarily led by well-established companies, including:

- Shell Chemicals (U.K.)

- INEOS Oligomers (U.K.)

- Chevron Phillips Chemical (U.S.)

- ExxonMobil Chemical (U.S.)

- Sasol Ltd. (South Africa)

- SABIC (Saudi Arabia)

- QatarEnergy (Qatar)

- Idemitsu Kosan Co., Ltd. (Japan)

- Godrej Industries (India)

- Linde plc. (Ireland)

Latest Developments in Global Higher Alpha Olefins Market

- In May 2025, Chevron Phillips Chemical announced the divestment of its interest in Chevron Phillips Singapore Chemicals to Aster Chemicals and Energy, including a high-density polyethylene manufacturing facility. This strategic portfolio realignment reflects Chevron Phillips’ focus on optimizing core assets, which is expected to influence regional supply dynamics for polyethylene, a key application of alpha olefins

- In April 2025, Shell Eastern Trading Pte. Ltd., a subsidiary of Shell plc, completed the acquisition of Pavilion Energy Pte. Ltd. This move strengthens Shell's position in the integrated energy and petrochemical sector, which could enhance its alpha olefins supply capabilities and support long-term growth in synthetic lubricants, detergents, and polyethylene markets

- In 2024, INEOS Oligomers significantly expanded its linear alpha olefins (LAO) production at its Chocolate Bayou facility in Texas, increasing capacity to 420,000 metric tons per year, making it one of the world’s largest LAO production sites. This capacity expansion is set to improve the global availability of alpha olefins, supporting rising demand for synthetic lubricants, polyethylene comonomers, and specialty chemicals, while reinforcing INEOS's market leadership

- In December 2022, Chevron Phillips Chemical and Charter Next Generation introduced overwrap films made with Marlex Anew Circular Polyethylene, utilizing alpha olefins. This development reflects growing industry efforts toward sustainable packaging solutions, which is expected to drive demand for alpha olefins in circular economy initiatives, particularly in food, medical, and consumer product packaging

- In January 2022, Shell Chemical secured approval for a USD 1.4 billion investment to build a world-scale linear alpha olefins plant at its Geismar facility. The project is expected to significantly enhance global LAO production capacity, supporting supply for critical downstream applications such as detergents, plastics, lubricants, and waxes, thereby strengthening Shell’s competitive position in the alpha olefins market.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Higher Alpha Olefins Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Higher Alpha Olefins Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Higher Alpha Olefins Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.