Global Home Care Providers Market

Market Size in USD Billion

USD

429.74 Billion

USD

772.15 Billion

2025

2033

USD

429.74 Billion

USD

772.15 Billion

2025

2033

| 2026 - 2033 | |

| USD 429.74 Billion | |

| USD 772.15 Billion | |

| % | |

|

Home Care Providers Market Overview

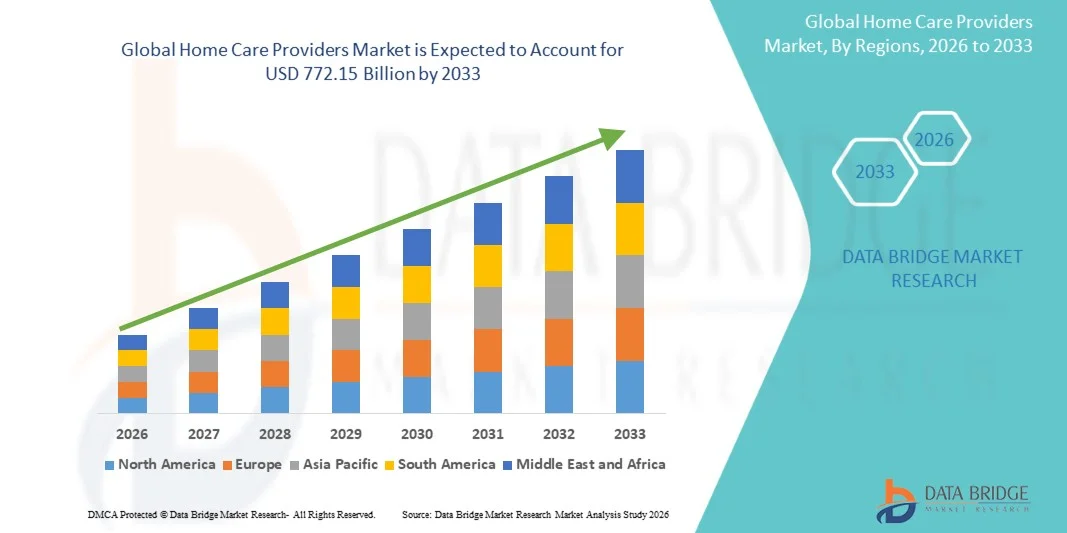

The Home Care Providers Market was valued at USD 429.74 billion in 2025 and is projected to reach USD 772.15 billion by 2033, growing at a CAGR of 7.60% from 2026 to 2033. The market is experiencing steady growth driven by rising demand for in-home healthcare services, increasing aging population, and growing preference for cost-effective alternatives to institutional care settings.

The rising prevalence of chronic diseases globally, combined with growing pressure on hospital infrastructure and supportive government policies promoting home-based care, is compelling healthcare systems, insurers, and families to adopt structured home care solutions. Skilled nursing, personal care assistance, and post-acute recovery services are increasingly shifting from hospitals to home environments, offering safer, more personalized, and cost-efficient long-term care delivery models.

Key Market Trends & Insights

- North America dominated the Home Care Providers Market with the largest revenue share of 38.42% in 2025, supported by well-established home healthcare infrastructure, strong insurance coverage systems, and high adoption of post-acute care services.

- The Home Health Care Agencies segment led the market with a 46.82% share in 2025, driven by their comprehensive service offerings that combine skilled nursing, personal care, rehabilitation, and chronic disease management under a single care coordination model.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.1% from 2026 to 2033, fueled by rapid population aging, improving healthcare accessibility, and expanding private home care service providers in countries such as India, China, and Japan.

- In-Home Hospice Care Services are the fastest-growing service projected to register a CAGR of 8.4%, reflecting the surge in demand for end-of-life care in comfortable, non-institutional settings.

- The Daily segment dominated the duration category with a 52.36% revenue share in 2025, led by high demand for continuous assistance among elderly patients, post-surgical cases, and individuals with severe chronic conditions.

- Older Persons accounted for 61.8% of the market, preferred by rapidly aging global population and increasing incidence of age-related chronic conditions such as Alzheimer’s, cardiovascular diseases, and mobility disorders.

- The Weekly segment is the fastest-growing duration category, with a CAGR of 7.9%, driven by the rising preference for flexible, cost-effective care solutions among middle-income populations.

Market Size & Forecast

- Global Market Value (2025): USD 429.74 Billion

- Expected Market Value (2033): USD 772.15 Billion

- Forecast CAGR (2026–2033): 7.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Home Care Providers Market Segmentation

|

Attributes |

Home Care Providers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Amedisys, Inc. (U.S.) · Home Instead, Inc. (U.S.) · Addus HomeCare Corporation (U.S.) · Bayada Home Health Care (U.S.) · Aveanna Healthcare Holdings Inc. (U.S.) · LHC Group, Inc. (U.S.) · Kindred at Home (U.S.) · Brookdale Senior Living Inc. (U.S.) · BrightSpring Health Services (U.S.) · AccentCare, Inc. (U.S.) · Maxim Healthcare Services (U.S.) · Right at Home, LLC (U.S.) · Visiting Angels (U.S.) · Interim HealthCare Inc. (U.S.) · Humana At Home (U.S.) · Care Advantage, Inc. (U.S.) · Elara Caring (U.S.) · Help at Home, LLC (U.S.) · Cera Care Ltd (U.K.) · Alliance Homecare (U.S.) |

|

Market Opportunities |

· Expansion of hospital-at-home programs by healthcare systems · Growing adoption of AI-powered elder care platforms and smart monitoring devices · Rapid penetration of private-pay and subscription-based home care models |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Home Care Providers Market Trends

Trend: Expansion of Digital and Telehealth-Enabled Home Care Models

Home care providers are increasingly integrating telehealth platforms, remote patient monitoring, and digital care coordination systems to deliver continuous medical and non-medical support at home. These technologies are improving real-time patient tracking, reducing hospital dependency, and enabling faster clinical decision-making for chronic and post-acute care patients. Care delivery is becoming more hybrid, combining in-person visits with virtual consultations to enhance efficiency and scalability. For instance, many providers are deploying remote monitoring kits and virtual nursing platforms to manage elderly patients with diabetes and cardiovascular diseases in real time.

Home Care Providers Market Dynamics

Key Market Driver: Rising Demand for Aging-in-Place and Chronic Care Management

The increasing global elderly population, along with the growing prevalence of chronic diseases such as dementia, cancer, and cardiovascular disorders, is significantly driving demand for structured home care services. Healthcare systems are shifting toward home-based care models to reduce hospital congestion and overall treatment costs while improving patient comfort and long-term care outcomes. Insurance coverage expansion and government-backed home healthcare programs are further accelerating adoption across developed and emerging economies. For instance, several national healthcare systems are expanding subsidized home nursing and post-surgical care programs to support aging populations and reduce inpatient hospital stays.

Key Restraint/Challenge: Limited Skilled Workforce and High Service Delivery Complexity

A major challenge in the Home Care Providers Market is the shortage of trained caregivers, nurses, and specialized healthcare professionals required to deliver high-quality home-based services. The fragmented nature of service delivery, combined with rising operational costs and regulatory variability across regions, makes scaling consistent care standards difficult. In addition, ensuring patient safety, data privacy, and emergency response readiness outside clinical environments adds further complexity.

For instance, many home care agencies face staffing shortages in rural and semi-urban regions, leading to service delays and uneven care quality across patient populations.

Key Market Opportunity: Integration of Smart Care Technologies and AI-Based Patient Monitoring

The integration of artificial intelligence, IoT-enabled medical devices, and predictive analytics platforms presents a major growth opportunity in the home care sector. These technologies enable early disease detection, personalized care planning, and continuous health monitoring, improving both patient outcomes and operational efficiency for providers. The rise of smart homes and connected health ecosystems is further expanding the scope of technology-driven home healthcare delivery models. For instance, AI-powered fall detection systems and wearable health trackers are being used to monitor elderly patients remotely and alert caregivers instantly during emergencies.

Home Care Providers Market Scope

The home care providers market is segmented on the basis of service type, duration of care, and end user.

- By Service

On the basis of service, the Home Care Providers Market is segmented into home health care agencies, visiting nurses, and in-home hospice care services. The Home Health Care Agencies segment dominated the market with a 46.82% share in 2025, owing to their comprehensive service offerings that combine skilled nursing, personal care, rehabilitation, and chronic disease management under a single care coordination model. These agencies are widely preferred by patients and insurers due to their structured service delivery, regulatory compliance, and ability to manage long-term care needs efficiently. They also benefit from strong referral networks with hospitals and physicians, ensuring a steady patient inflow. Increasing demand for post-acute care and hospital discharge management is further strengthening this segment. Technological integration such as telehealth and remote monitoring is improving service efficiency and scalability. However, workforce shortages remain a persistent operational challenge across regions.

The In-Home Hospice Care Services segment is the fastest growing at a CAGR of 8.4% from 2026 to 2033, driven by rising demand for end-of-life care in comfortable, non-institutional settings. Patients and families increasingly prefer hospice care at home due to emotional comfort, reduced hospitalization costs, and personalized attention. Healthcare systems are also promoting palliative care models to reduce hospital burden and improve quality of life for terminally ill patients. Expanding insurance coverage for hospice services is further supporting adoption. Increasing awareness of dignified end-of-life care is boosting demand in both developed and emerging markets. Integration of multidisciplinary care teams is enhancing service quality and patient satisfaction.

- By Duration

On the basis of duration, the Home Care Providers Market is segmented into daily, weekly, monthly, quarterly, and annually based care models. The Daily Care segment dominated the market with a 52.36% share in 2025, due to high demand for continuous assistance among elderly patients, post-surgical cases, and individuals with severe chronic conditions. Daily care services ensure consistent medical supervision, medication adherence, and support with activities of daily living, making them essential for high-dependency patients. Hospitals frequently recommend daily home care after discharge to reduce readmission risks. The segment benefits from strong caregiver availability models in urban regions. Increasing prevalence of neurodegenerative disorders such as dementia is further boosting demand. However, operational cost intensity remains a limiting factor for wider adoption in low-income regions.

The Weekly Care segment is the fastest growing at a CAGR of 7.9% from 2026 to 2033, driven by rising preference for flexible, cost-effective care solutions among middle-income populations. Weekly care models are increasingly used for follow-up visits, rehabilitation monitoring, and chronic disease check-ins. This structure provides a balance between professional care and family-based support, making it highly attractive for stable but long-term patients. Expansion of subscription-based home care packages is supporting growth. Increasing adoption in semi-urban and emerging markets is further accelerating demand. Digital scheduling and teleconsultation support are improving efficiency and accessibility.

- By End User

On the basis of end user, the Home Care Providers Market is segmented into patients after surgery, older persons, mothers and new-borns, people with disabilities, mentally ill adults, and others. The Older Persons segment dominated the market with a 61.28% share in 2025, driven by the rapidly aging global population and increasing incidence of age-related chronic conditions such as Alzheimer’s, cardiovascular diseases, and mobility disorders. Elderly patients require long-term assistance with daily activities, medication management, and continuous monitoring, making home care a preferred option over institutional care. Government initiatives promoting aging-in-place healthcare models are further supporting this segment. Strong demand for companionship and palliative care services is also contributing to growth. Insurance-backed home care programs in developed regions are accelerating adoption. However, caregiver shortages remain a key operational constraint.

The People with Disabilities segment is the fastest growing at a CAGR of 8.6% from 2026 to 2033, driven by increasing awareness of inclusive care models and improved access to specialized home-based support services. This segment includes individuals requiring long-term physical, cognitive, or developmental assistance in daily living activities. Expansion of disability support programs and government subsidies is boosting service accessibility. Technological advancements such as assistive devices and smart home integration are improving independence and quality of life. Rising demand for personalized rehabilitation and therapy services is further accelerating growth. Growing social acceptance of home-based disability care is strengthening market expansion globally.

Home Care Providers Market Regional Analysis

North America dominated the Home Care Providers Market with the largest revenue share of 38.42% in 2025, supported by well-established home healthcare infrastructure, strong insurance coverage systems, and high adoption of post-acute care services. The region benefits from a rapidly aging population, high prevalence of chronic diseases, and strong adoption of post-acute and long-term care services delivered at home. Expansion of hospital-at-home programs, advanced telehealth integration, and availability of skilled caregivers further strengthen market growth. Increasing preference for cost-effective alternatives to institutional care and strong presence of organized home care agencies continue to reinforce North America’s leadership position in the global market.

U.S. Home Care Providers Market Insight

The U.S. home care providers market is witnessing strong growth due to rising demand for aging-in-place services, increasing healthcare expenditure, and expanding insurance coverage for home-based care. The country’s well-developed healthcare infrastructure, along with a high prevalence of chronic diseases and post-acute care needs, is driving adoption across skilled nursing, personal care, and hospice services. In addition, growing integration of telehealth, remote patient monitoring, and hospital-at-home programs is accelerating service delivery efficiency. Increasing focus on reducing hospital readmissions and improving patient outcomes continues to strengthen demand across both public and private home care providers.

Europe Home Care Providers Market Insight

The Europe home care providers market remains a major contributor to global revenue, driven by strong government healthcare support, aging population trends, and well-established social care systems. The widespread adoption of structured elderly care programs and palliative care services is supporting market expansion across the region. Increasing investments in digital health infrastructure, home nursing services, and integrated care models is further enhancing service accessibility. Strict healthcare regulations and strong emphasis on patient safety and quality care continue to promote standardized home care delivery across European countries.

U.K. Home Care Providers Market Insight

The U.K. home care providers market is experiencing steady growth, supported by rising demand for elderly care services, increasing pressure on public healthcare systems, and growing preference for home-based recovery solutions. Expansion of NHS-supported home care initiatives and private care providers is contributing to market development. Integration of digital care platforms, remote monitoring systems, and AI-enabled scheduling tools is improving service efficiency and patient management. Furthermore, rising focus on reducing hospital occupancy rates is strengthening demand for structured home care services across the country.

Germany Home Care Providers Market Insight

The Germany home care providers market is expanding steadily due to a rapidly aging population, strong healthcare infrastructure, and increasing demand for long-term care services. The country’s focus on insurance-supported elder care programs and rehabilitation services is driving adoption of structured home-based healthcare solutions. Rising use of digital health technologies and care coordination platforms is improving service efficiency and patient monitoring. In addition, strong regulatory frameworks and increasing emphasis on quality-driven care delivery are further supporting market growth in Germany.

Asia-Pacific Home Care Providers Market Insight

The Asia-Pacific home care providers market is expected to witness rapid growth, driven by rising aging populations, improving healthcare accessibility, and increasing awareness of home-based care benefits across countries such as China, India, and Japan. Growing urbanization and rising healthcare expenditures are supporting demand for both medical and non-medical home care services. Expanding private healthcare providers and government initiatives promoting community-based care are further strengthening regional adoption. In addition, increasing integration of digital health platforms and telemedicine services is accelerating market expansion across both urban and semi-urban areas.

Japan Home Care Providers Market Insight

The Japan home care providers market is witnessing consistent growth due to one of the world’s most rapidly aging populations and strong demand for elderly care services. Increasing preference for home-based long-term care over institutional facilities is driving market expansion. The country’s advanced healthcare system and strong government support for elder care insurance programs are further strengthening adoption. In addition, integration of robotics, remote monitoring, and digital care technologies is improving efficiency and quality of home-based healthcare delivery.

China Home Care Providers Market Insight

The China home care providers market is growing rapidly, driven by rising aging population, increasing prevalence of chronic diseases, and expanding healthcare infrastructure. Strong government focus on elderly care systems and community-based healthcare services is significantly boosting demand for home care solutions. Rapid urbanization and increasing adoption of digital health platforms are further supporting market expansion. In addition, growing private sector participation and rising awareness of home-based care benefits are positioning China as one of the fastest-growing markets globally.

Home Care Providers Market Share

The home care providers industry is primarily led by well-established companies, including:

- Amedisys, Inc. (U.S.)

- Home Instead, Inc. (U.S.)

- Addus HomeCare Corporation (U.S.)

- Bayada Home Health Care (U.S.)

- Aveanna Healthcare Holdings Inc. (U.S.)

- LHC Group, Inc. (U.S.)

- Kindred at Home (U.S.)

- Brookdale Senior Living Inc. (U.S.)

- BrightSpring Health Services (U.S.)

- AccentCare, Inc. (U.S.)

- Maxim Healthcare Services (U.S.)

- Right at Home, LLC (U.S.)

- Visiting Angels (U.S.)

- Interim HealthCare Inc. (U.S.)

- Humana At Home (U.S.)

- Care Advantage, Inc. (U.S.)

- Elara Caring (U.S.)

- Help at Home, LLC (U.S.)

- Cera Care Ltd (U.K.)

- Alliance Homecare (U.S.)

Latest Developments in Home Care Providers Market

- In January 2024, BrightSpring Health Services completed its initial public offering, marking a major milestone in the home and community-based healthcare services sector. The IPO provided capital to expand its home health, pharmacy, and community living services across the United States. It also strengthened investments in technology-enabled care coordination and service delivery infrastructure. The listing reflects increasing investor confidence in scalable home-based healthcare models and continued market consolidation

- In March 2023, DispatchHealth expanded its hospital-at-home and in-home acute care services through partnerships with health systems across the United States. The company strengthened its ability to deliver hospital-level treatment in patient homes, reducing unnecessary emergency room visits and hospital admissions. Its services include advanced diagnostics, urgent care, and chronic disease management delivered at home. This expansion highlights the growing shift toward decentralized, technology-enabled healthcare delivery models

- In February 2023, Optum (UnitedHealth Group) completed the acquisition of LHC Group, significantly expanding its home health and post-acute care capabilities across the United States. The acquisition strengthened Optum’s integrated care delivery model by combining LHC Group’s skilled nursing and home health services with its broader healthcare ecosystem. This move enhanced access to hospital-at-home programs, chronic disease management, and value-based care services. It also enabled better coordination between payers and providers, improving efficiency in home-based healthcare delivery solutions

- In December 2021, Humana completed its acquisition of Kindred at Home, marking a major expansion in the U.S. home healthcare and hospice care market. The deal significantly increased Humana’s footprint in skilled home health, personal care, and end-of-life care services. It aligned with the company’s strategy to strengthen value-based care models for aging populations and Medicare Advantage members. The acquisition also reinforced consolidation trends in the home care sector, enabling more integrated and scalable care delivery systems

- In January 2021, AccentCare merged with Seasons Hospice & Palliative Care, creating one of the largest providers of home-based hospice and post-acute care services in the United States. The merger expanded AccentCare’s geographic reach and strengthened its service portfolio across skilled nursing, hospice care, and chronic care management. It enhanced the delivery of coordinated end-of-life care services in home settings. The transaction also reflected increasing private equity-driven consolidation in the home healthcare industry

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.