Global Hospital Robotics Market

Market Size in USD Billion

USD

12.68 Billion

USD

29.85 Billion

2025

2033

USD

12.68 Billion

USD

29.85 Billion

2025

2033

| 2026 - 2033 | |

| USD 12.68 Billion | |

| USD 29.85 Billion | |

| % | |

|

Hospital Robotics Market Overview

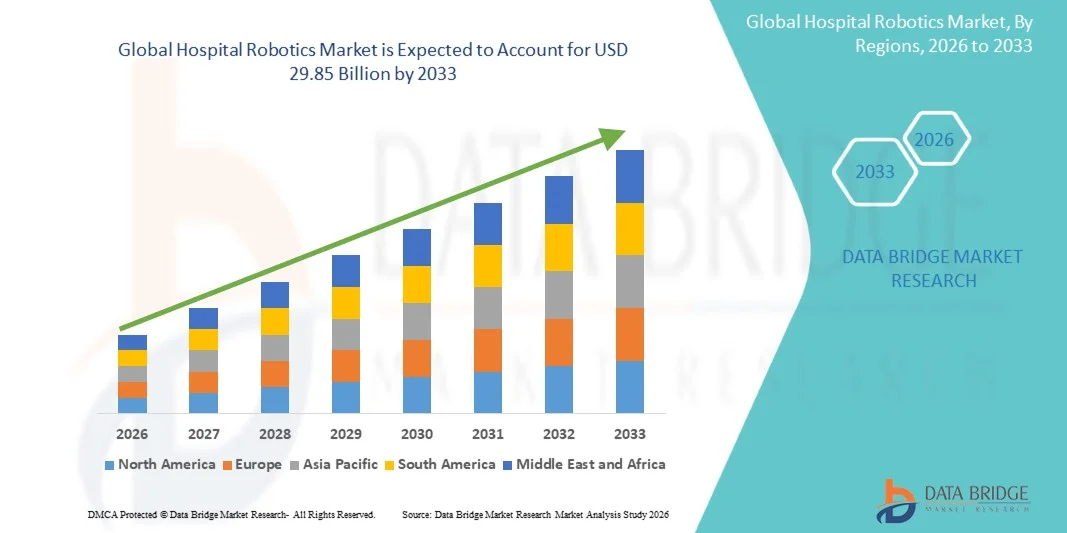

As per Data Bridge Market Research analysis The hospital robotics market was valued at USD 12.68 billion in 2025 and is projected to reach USD 29.85 billion by 2033, growing at a CAGR of 11.30% from 2026 to 2033. The market is experiencing steady growth driven by increasing adoption of robotic technologies in healthcare facilities, rising demand for automation in clinical and non-clinical hospital operations, and continuous advancements in artificial intelligence, machine vision, and robotic-assisted systems.

The growing burden on healthcare systems, coupled with workforce shortages and the need to improve operational efficiency, is encouraging hospitals to invest in robotic solutions for surgery, pharmacy automation, laboratory management, patient assistance, and disinfection. Autonomous mobile robots, surgical robots, and AI-enabled service robots are increasingly being deployed to enhance patient outcomes, reduce human error, and streamline hospital workflows. Furthermore, the rising emphasis on infection control, precision medicine, and minimally invasive procedures is accelerating the adoption of advanced hospital robotics across developed and emerging healthcare markets.

Market Size & Forecast

- Global Market Value (2025): USD 12.68 Billion

- Expected Market Value (2033): USD 29.85 Billion

- Forecast CAGR (2026–2033): 11.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Key Market Trends & Insights

- North America dominated the hospital robotics market with the largest revenue share of 38.62% in 2025, supported by advanced healthcare infrastructure, high adoption of robotic-assisted surgery systems, and strong investments in healthcare automation.

- The Surgical Robots segment led the market with a 43.82% share in 2025, driven by the increasing adoption of minimally invasive procedures, superior surgical precision, and improved patient outcomes.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 12.1% from 2026 to 2033, fueled by expanding healthcare infrastructure, rising healthcare expenditures, and increasing adoption of robotic technologies in China, India, and Japan.

- Autonomous Mobile Robots are the fastest-growing product type, projected to register a CAGR of 12.5%, reflecting the surge in demand for automation in hospital logistics and material transportation.

- The Hardware segment dominated the component category with a 61.47% revenue share in 2025, led by the substantial investments in robotic platforms, robotic arms, sensors, cameras, controllers, and imaging systems.

- Surgery accounted for 39.84% of the market, preferred by the growing adoption of robotic-assisted procedures across multiple medical specialties.

- The Logistics & Material Handling segment is the fastest-growing application category, with a CAGR of 12.3%, driven by the increasing demand for hospital workflow automation.

Report Scope and Hospital Robotics Market Segmentation

|

Attributes |

Hospital Robotics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Intuitive Surgical, Inc. (U.S.) · Stryker (U.S.) · Medtronic plc (Ireland) · Zimmer Biomet (U.S.) · Smith+Nephew plc (U.K.) · Johnson & Johnson Services, Inc. (U.S.) · CMR Surgical Ltd (U.K.) · Asensus Surgical, Inc. (U.S.) · Renishaw plc (U.K.) · Omnicell, Inc. (U.S.) · Swisslog Healthcare (Switzerland) · TUG Robotics (Aethon) (U.S.) · Omron Corporation (Japan) · FUJIFILM Holdings Corporation (Japan) · Samsung Electronics Co., Ltd. (South Korea) · GE HealthCare (U.S.) · Siemens Healthineers AG (Germany) · KUKA AG (Germany) · Diligent Robotics Inc. (U.S.) · Panasonic Holdings Corporation (Japan) |

|

Market Opportunities |

· Expansion of autonomous mobile robots (AMRs) in hospital logistics · Growing adoption of robotic disinfection and sterilization systems · Integration of AI-powered robotic platforms with hospital digital ecosystems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hospital Robotics Market Trends

Trend: Increasing Adoption of Autonomous Robots for Hospital Workflow Automation

Hospitals are increasingly deploying autonomous robotic systems to streamline logistics, automate repetitive tasks, and improve operational efficiency across healthcare facilities. The integration of artificial intelligence, machine vision, and navigation technologies enables robots to transport medications, laboratory samples, medical supplies, and equipment with minimal human intervention. Healthcare providers are similarly leveraging robotic platforms to optimize resource utilization through standardized, data-driven workflows, while advanced connectivity and automation technologies create intelligent environments that closely support modern hospital operations.

For instance, in March 2025, Swisslog Healthcare expanded its autonomous mobile robot solutions for hospital logistics, enabling healthcare facilities to automate internal transport operations and improve workflow efficiency.

Hospital Robotics Market Dynamics

Key Market Driver: Growing Adoption of Robotic-Assisted Surgery and Healthcare Automation

The rapid expansion of minimally invasive procedures and hospital automation initiatives has created substantial demand for advanced robotic systems that can enhance surgical precision, optimize clinical workflows, and improve patient outcomes across healthcare environments. Hospitals, specialty care centers, and healthcare networks are deploying robotic platforms as a core component of their modernization strategies, reducing procedural variability, accelerating operational efficiency, and improving overall quality of care delivery.

For instance, in 2024, Intuitive Surgical continued expanding installations of its robotic-assisted surgical systems globally, reflecting increasing healthcare provider investment in precision surgery technologies and automation-driven patient care.

Key Restraint/Challenge: High Initial Investment Cost of Advanced Hospital Robotics Systems

A significant restraint in the hospital robotics market is the high upfront capital required for advanced robotic platforms. Modern systems integrate sophisticated robotic arms, artificial intelligence software, imaging technologies, and navigation capabilities, demanding substantial investment in procurement, installation, and ongoing maintenance. The total cost of ownership extends to software upgrades, staff training, and technical support, making adoption difficult for smaller hospitals, community healthcare facilities, and budget-constrained organizations.

For instance, the deployment of multi-specialty robotic surgery platforms across large healthcare institutions requires significant infrastructure investment and specialized workforce training, highlighting the financial barriers that continue to limit broader adoption among smaller providers.

Key Market Opportunity: Integration of AI and Data-Driven Hospital Robotics Platforms

The integration of artificial intelligence in hospital robotics presents a significant market opportunity. AI-enabled platforms can support predictive workflow management, provide real-time clinical insights, and enhance robotic decision-making across diverse healthcare applications. The development of interoperable robotic ecosystems and cloud-connected healthcare platforms is further expanding access to advanced automation capabilities, opening growth opportunities across emerging healthcare markets in Asia-Pacific, Latin America, and the Middle East.

For instance, in January 2025, Medtronic advanced AI-enabled robotic surgery and digital healthcare initiatives designed to improve procedural efficiency, support clinical decision-making, and strengthen connected hospital ecosystems.

Hospital Robotics Market Scope

The hospital robotics market is segmented on the basis of product type, component, application, and end user.

- By Product Type

On the basis of product type, the hospital robotics market is segmented into surgical robots, autonomous mobile robots, pharmacy automation robots, laboratory automation robots, disinfection & sterilization robots, telepresence robots, rehabilitation robots, and patient assistance robots. The Surgical Robots segment dominated the market with a 43.28% share in 2025, owing to increasing adoption of minimally invasive procedures, superior surgical precision, and improved patient outcomes. These systems enable surgeons to perform complex procedures with enhanced dexterity, visualization, and control. Hospitals are investing heavily in robotic-assisted surgery platforms to reduce complications, shorten hospital stays, and improve recovery times. The growing prevalence of chronic diseases requiring surgical intervention is further supporting demand. Continuous technological advancements in robotic imaging, navigation, and AI-assisted guidance are enhancing system capabilities. Strong reimbursement support and expanding clinical acceptance continue to reinforce the segment’s leadership position globally.

The Autonomous Mobile Robots (AMRs) segment is projected to register the fastest growth at a CAGR of 12.5% from 2026 to 2033, driven by rising demand for automation in hospital logistics and material transportation. These robots efficiently transport medications, laboratory samples, medical supplies, and equipment across healthcare facilities. Growing healthcare workforce shortages are encouraging hospitals to automate repetitive non-clinical tasks. Advances in AI, navigation systems, and real-time obstacle avoidance technologies are significantly improving operational performance. Hospitals are increasingly deploying AMRs to enhance productivity while reducing operational costs. Rising investments in smart hospitals and digital healthcare infrastructure are further accelerating adoption. Their ability to improve workflow efficiency and patient service levels is expected to drive strong future growth.

- By Component

On the basis of component, the hospital robotics market is segmented into hardware, software, and services. The Hardware segment dominated the market with a 61.47% share in 2025 due to substantial investments in robotic platforms, robotic arms, sensors, cameras, controllers, and imaging systems. Hardware represents the foundational infrastructure required for robotic-assisted healthcare operations. Increasing installations of surgical robots, autonomous mobile robots, and pharmacy automation systems are driving demand. Healthcare providers continue to allocate significant capital toward advanced robotic equipment to improve clinical and operational efficiency. Technological innovations in sensors, machine vision, and robotic mechanics are further enhancing system performance. The high acquisition cost of robotic platforms contributes significantly to overall market revenue. Continuous expansion of robotic deployments across hospitals maintains the segment’s dominant position.

The Software segment is expected to witness the fastest growth at a CAGR of 11.8% from 2026 to 2033, supported by growing integration of artificial intelligence, machine learning, and data analytics capabilities. Advanced software platforms enable robotic navigation, workflow automation, predictive maintenance, and clinical decision support. Hospitals are increasingly adopting intelligent software solutions to optimize robotic performance and improve healthcare outcomes. The growing trend toward connected healthcare ecosystems is creating strong demand for interoperable robotic software. Continuous advancements in cloud computing and real-time data processing are expanding software functionality. AI-driven automation is enabling robots to perform increasingly complex tasks with greater efficiency. As healthcare digitalization accelerates, software adoption is expected to grow rapidly.

- By Application

On the basis of application, the hospital robotics market is segmented into surgery, pharmacy automation, laboratory automation, logistics & material handling, cleaning & disinfection, rehabilitation & physical therapy, telepresence & remote consultation, and patient care & monitoring. The Surgery segment accounted for the largest market share of 39.84% in 2025, driven by the growing adoption of robotic-assisted procedures across multiple medical specialties. Robotic surgery offers enhanced precision, smaller incisions, reduced blood loss, and faster patient recovery. Increasing demand for minimally invasive treatments is encouraging healthcare providers to expand robotic surgical capabilities. Hospitals are investing in advanced robotic platforms to improve procedural accuracy and clinical outcomes. Technological advancements in imaging, navigation, and robotic controls continue to strengthen adoption. Rising surgical procedure volumes worldwide further support the segment’s dominance.

The Logistics & Material Handling segment is projected to be the fastest-growing application at a CAGR of 12.3% from 2026 to 2033, fueled by increasing demand for hospital workflow automation. Hospitals are deploying robotic systems to automate transportation of medications, medical supplies, laboratory specimens, and equipment. These solutions reduce manual workload, minimize delivery errors, and improve operational efficiency. Growing pressure to optimize healthcare resources and address staffing shortages is accelerating implementation. Advances in autonomous navigation and fleet management technologies are enhancing system reliability. Smart hospital initiatives are creating additional opportunities for logistics automation. The segment is expected to experience substantial growth as healthcare facilities prioritize efficiency improvements.

- By End User

On the basis of end user, the hospital robotics market is segmented into general hospitals, specialty hospitals, ambulatory surgical centers, rehabilitation centers, and academic & research institutes. The General Hospitals segment dominated the market with a 58.34% share in 2025 due to extensive adoption of robotic technologies across multiple departments and clinical applications. These hospitals perform a high volume of surgical procedures and require advanced automation solutions to manage complex operations. Significant investments in robotic surgery, pharmacy automation, and hospital logistics support widespread adoption. General hospitals also benefit from larger budgets and broader infrastructure capabilities compared to smaller healthcare facilities. Rising patient volumes and increasing demand for operational efficiency are further supporting growth. Continuous modernization initiatives are reinforcing the segment’s leading market position.

The Ambulatory Surgical Centers (ASCs) segment is expected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing preference for outpatient procedures and cost-effective healthcare delivery models. ASCs are rapidly adopting robotic-assisted surgical technologies to improve procedural precision and patient outcomes. These facilities benefit from shorter patient stays, reduced operational costs, and enhanced workflow efficiency. Growing demand for minimally invasive procedures is creating strong opportunities for robotic integration. Technological advancements are making robotic systems more compact and suitable for outpatient settings. Rising healthcare decentralization trends are further accelerating ASC expansion. The need to enhance competitiveness and clinical capabilities is expected to drive robust growth in this segment.

Hospital Robotics Market Regional Analysis

North America dominated the hospital robotics market with the largest revenue share of 38.62% in 2025, supported by advanced healthcare infrastructure, high adoption of robotic-assisted surgery systems, and strong investments in healthcare automation. The region also benefits from high adoption of robotic-assisted surgery systems, favorable reimbursement frameworks, and growing deployment of automation solutions across hospitals and healthcare facilities. Increasing use of AI-enabled robotic platforms, autonomous mobile robots, and precision surgical technologies continues to expand adoption across clinical and operational applications. Rising focus on healthcare efficiency, patient safety, and minimally invasive procedures continues to strengthen North America's leadership position in the global market.

U.S. Hospital Robotics Market Insight

The U.S. hospital robotics market is witnessing strong growth due to rising investments in robotic-assisted surgery systems, healthcare automation initiatives, and advanced patient care technologies. The country’s mature healthcare ecosystem, along with increasing adoption of AI-powered, autonomous, and connected robotic platforms, is driving demand across surgical, pharmacy, laboratory, and logistics applications. In addition, growing emphasis on improving clinical outcomes, reducing healthcare costs, and addressing workforce shortages is accelerating robotic system adoption across hospitals and healthcare networks.

Europe Hospital Robotics Market Insight

The Europe hospital robotics market remains a major contributor to global revenue, driven by strong government support, technological innovation, and high demand for advanced healthcare automation solutions. The widespread use of robotic-assisted surgery systems, autonomous mobile robots, and rehabilitation robots is supporting market expansion across the region. Increasing investments in intelligent healthcare technologies, coupled with stringent quality standards and a highly developed healthcare infrastructure, continue to enhance the adoption of hospital robotics throughout Europe.

U.K. Hospital Robotics Market Insight

The U.K. hospital robotics market is experiencing steady growth, supported by rising adoption of robotic technologies in surgery, hospital automation, and patient care applications. Increasing investments in advanced robotic infrastructure and growing demand for efficient, technology-driven healthcare delivery are contributing to market growth. Furthermore, integration of AI, machine learning, and digital health technologies is improving robotic performance and operational efficiency, positioning the U.K. as a key innovation hub in the hospital robotics industry.

Germany Hospital Robotics Market Insight

The Germany hospital robotics market is expanding steadily due to the country’s strong medical technology sector, advanced research capabilities, and increasing adoption of next-generation robotic healthcare solutions. Hospitals, research institutions, and healthcare providers are increasingly utilizing robotic systems for surgery, laboratory automation, and operational efficiency improvement. Continuous advancements in robotic precision, AI integration, and medical imaging technologies, along with strong government focus on healthcare innovation and quality care, are further driving market growth in Germany.

Asia-Pacific Hospital Robotics Market Insight

The Asia-Pacific hospital robotics market is expected to witness rapid growth, driven by expanding healthcare infrastructure, increasing healthcare expenditure, and rising investments in medical technology across countries such as China, India, and Japan. Growing awareness regarding healthcare automation, rising adoption of advanced robotic systems, and increasing demand for efficient patient care solutions are supporting regional market expansion. In addition, the growing presence of healthcare innovation centers and modernization initiatives is accelerating robotic adoption across hospitals and healthcare facilities.

Japan Hospital Robotics Market Insight

The Japan hospital robotics market is witnessing consistent growth due to rising investments in healthcare automation technologies, medical innovation, and advanced patient care initiatives. Healthcare providers, hospitals, and research institutes are increasingly adopting robotic systems for surgery, rehabilitation, and operational workflow optimization. Moreover, increasing integration of AI-powered technologies and the country’s focus on efficient, high-quality healthcare services are further contributing to market growth.

China Hospital Robotics Market Insight

The China hospital robotics market is growing rapidly, driven by expanding healthcare infrastructure, increasing government support for healthcare modernization, and rising demand for advanced medical technologies. Growing adoption of AI-enabled robotic platforms across surgical, pharmacy, logistics, and rehabilitation applications is significantly boosting market demand. In addition, rising investments in healthcare innovation, increasing focus on improving patient outcomes, and rapid technological advancements are positioning China as one of the fastest-growing markets for hospital robotics globally.

Hospital Robotics Market Share

The hospital robotics industry is primarily led by well-established companies, including:

- Intuitive Surgical, Inc. (U.S.)

- Stryker (U.S.)

- Medtronic plc (Ireland)

- Zimmer Biomet (U.S.)

- Smith+Nephew plc (U.K.)

- Johnson & Johnson Services, Inc. (U.S.)

- CMR Surgical Ltd (U.K.)

- Asensus Surgical, Inc. (U.S.)

- Renishaw plc (U.K.)

- Omnicell, Inc. (U.S.)

- Swisslog Healthcare (Switzerland)

- TUG Robotics (Aethon) (U.S.)

- Omron Corporation (Japan)

- FUJIFILM Holdings Corporation (Japan)

- Samsung Electronics Co., Ltd. (South Korea)

- GE HealthCare (U.S.)

- Siemens Healthineers AG (Germany)

- KUKA AG (Germany)

- Diligent Robotics Inc. (U.S.)

- Panasonic Holdings Corporation (Japan)

Latest Developments in Hospital Robotics Market

- In January 2024, Intuitive Surgical received U.S. FDA clearance for its da Vinci 5 surgical system, enabling its deployment in hospitals across the United States. The approval marked a key regulatory milestone for next-generation robotic-assisted surgical platforms. The system offers enhanced visualization, improved ergonomics, and advanced data integration for surgeons. It is expected to accelerate adoption of robotic surgery in U.S. hospitals

- In May 2023, Intuitive Surgical, a global leader in robotic-assisted surgery, introduced its next-generation da Vinci 5 surgical system designed to enhance precision, imaging, and surgeon control. The system incorporates advanced computing power, improved force feedback, and enhanced digital integration for complex minimally invasive procedures. It represents a major upgrade in robotic surgery capabilities across multiple surgical specialties. This launch reinforces Intuitive Surgical’s dominance in the hospital robotics market

- In April 2022, Stryker, a leading medical technology company, completed the acquisition of Vocera Communications, a provider of clinical communication and workflow solutions widely used in hospitals. The acquisition strengthened Stryker’s hospital robotics and digital healthcare ecosystem by integrating hands-free communication, workflow automation, and care coordination technologies. Vocera’s platform enables improved clinical communication and faster response times across hospital environments. This development expanded Stryker’s footprint beyond surgical robotics into hospital-wide automation solutions

- In October 2021, CMR Surgical, a medical technology company, announced early clinical adoption of its Versius Surgical Robotic System in India, expanding its presence in the Asia-Pacific hospital robotics market. The system is designed for minimally invasive surgeries with modular robotic arms that offer flexibility and portability in hospital operating rooms. It enables easier integration into existing surgical workflows compared to traditional robotic systems. This development supports broader access to robotic surgery in emerging healthcare markets

- In March 2021, Medtronic, a leading medical technology company, announced that its Hugo™ Robotic-Assisted Surgery (RAS) system received CE Mark approval in Europe, enabling its commercialization across multiple European healthcare facilities. The system is designed for minimally invasive surgeries across urology, gynecology, and general surgery applications. It features a modular architecture, advanced 3D visualization, and data-driven surgical insights to enhance precision and clinical outcomes. This approval marked a significant milestone in expanding competition within the global surgical robotics market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.