Global Hot Stamping Body In White Market

Market Size in USD Billion

USD

2.96 Billion

USD

3.77 Billion

2025

2033

USD

2.96 Billion

USD

3.77 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.96 Billion | |

| USD 3.77 Billion | |

| % | |

|

Hot Stamping Body in White Market Overview

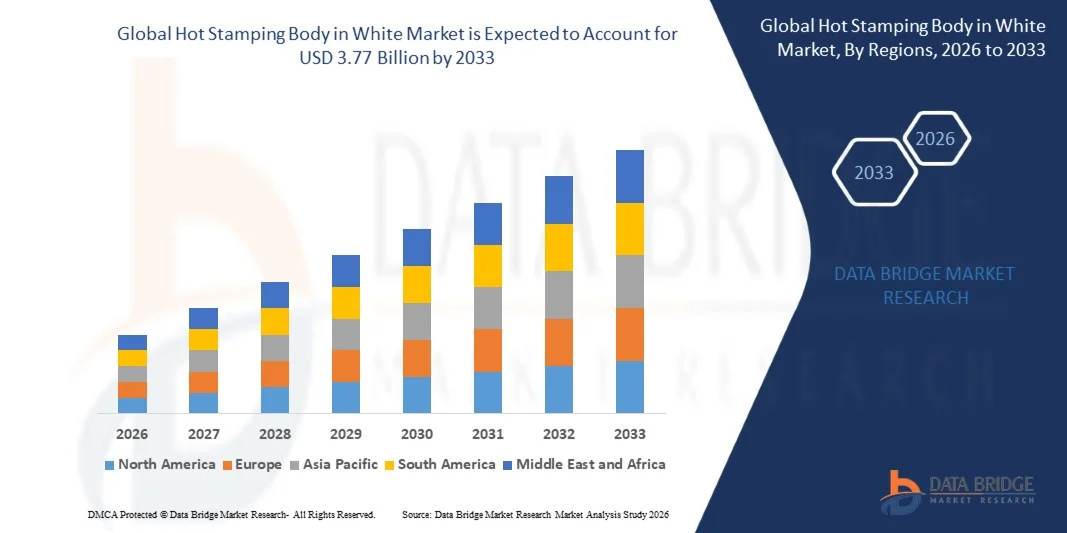

The Hot Stamping Body in White Market was valued at USD 2.96 billion in 2025 and is projected to reach USD 3.77 billion by 2033, growing at a CAGR of 3.10% from 2026 to 2033. The market is experiencing steady growth driven by increasing demand for lightweight vehicle structures, rising focus on passenger safety standards, and growing adoption of high-strength steel components in automotive manufacturing.

The growing emphasis on fuel efficiency and emission reduction regulations is encouraging automotive OEMs to replace conventional steel parts with advanced hot-stamped components that offer superior crash resistance and weight reduction benefits. In addition, expanding electric vehicle production and the need for optimized structural integrity in battery enclosures are further accelerating market adoption across global automotive platforms.

Key Market Trends & Insights

- North America dominated the hot stamping body in white market with the largest revenue share in 2025, supported by strong automotive manufacturing capabilities, high adoption of advanced press hardening technologies, and increasing demand for safety-enhanced and lightweight vehicle architectures.

- Asia-Pacific is expected to be the fastest-growing region, recording a strong CAGR from 2026 to 2033. Growth is driven by rapid vehicle production expansion, increasing EV penetration, supportive government policies, and rising investments in automotive manufacturing infrastructure across China, India, and Japan.

- The Passenger Vehicles segment held the largest market revenue share of approximately 58.6% in 2025, driven by high production volumes, increasing demand for passenger safety features, and widespread adoption of lightweight high-strength body structures in mass-market and premium cars. The segment benefits from strict global crash safety regulations such as Euro NCAP and NHTSA standards, which are pushing OEMs to integrate hot stamped components in critical structural zones such as A-pillars, B-pillars, and side impact beams. Growing urbanization and rising disposable income are further supporting passenger car production, especially in Asia-Pacific markets such as China and India.

- The Electric Vehicles segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by rapid EV adoption, increasing need for lightweight battery enclosures, and growing focus on crash safety and structural rigidity in next-generation electric platforms across Asia-Pacific and Europe. Hot stamping is increasingly used in EV body structures to compensate for heavy battery packs by reducing overall vehicle weight and improving range efficiency. Automotive OEMs are also integrating press-hardened steel in battery protection systems to enhance thermal and impact safety. Government incentives supporting EV adoption and carbon neutrality targets are further accelerating segment expansion globally.

- The Monocoque segment held the largest market revenue share of approximately 72.3% in 2025, driven by its extensive use in modern passenger vehicles due to superior weight efficiency, structural strength, and crash energy absorption capabilities. Monocoque structures allow better integration of hot stamped components into the vehicle body shell, improving stiffness and passenger safety performance. Increasing preference for unibody designs in sedans, hatchbacks, and electric vehicles is further strengthening segment dominance. OEMs are also leveraging monocoque architectures to optimize material usage and meet strict emission reduction targets.

- The Frame Mounted segment is projected to grow at a steady CAGR of 6.8% from 2026 to 2033, driven by continued demand for commercial vehicles, SUVs, and off-road applications where durability and load-bearing capacity are critical design requirements. This structure is widely used in heavy-duty trucks and utility vehicles where structural robustness is prioritized over weight reduction. Increasing infrastructure development and logistics expansion are supporting demand for frame-mounted vehicles in emerging economies. In addition, manufacturers are incorporating hot stamped reinforcements in key chassis components to enhance durability under high-stress operating conditions.

- The Steel segment held the largest market revenue share of approximately 83.7% in 2025, driven by the extensive use of boron steel in hot stamping processes due to its high tensile strength, cost efficiency, and suitability for mass production in automotive body structures. Steel remains the preferred material due to its excellent crash energy absorption properties and compatibility with existing press hardening infrastructure. Automakers continue to rely on advanced high-strength steel (AHSS) to achieve a balance between safety performance and manufacturing cost efficiency.

- The CFRP segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing adoption in premium and electric vehicles where ultra-lightweight structures and high performance are prioritized to improve efficiency, range, and crash safety performance. CFRP is gaining traction in next-generation EV platforms due to its superior strength-to-weight ratio compared to conventional metals. Although currently expensive, ongoing material innovation and scaling of composite manufacturing processes are gradually improving affordability. Aerospace-inspired design integration and increasing use in luxury EV brands are further accelerating long-term adoption trends.

Market Size & Forecast

- Global Market Value (2025): USD 2.96 Billion

- Expected Market Value (2033): USD 3.77 Billion

- Forecast CAGR (2026–2033): 3.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Hot Stamping Body in White Market Segmentation

|

Attributes |

Hot Stamping Body in White Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Autokiniton (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Hot Stamping Body in White Market Trends

Trend: Growth In Lightweight Materials Adoption And Advanced Hot Stamping Technologies

Increasing demand for lightweight, high-strength automotive structures is driving the adoption of hot stamping body in white technologies across passenger vehicles, commercial vehicles, and electric vehicle platforms. Traditional cold-formed steel components add higher vehicle weight and limit crash performance efficiency, encouraging OEMs to shift toward ultra-high-strength steel solutions that offer improved rigidity, safety, and weight reduction.

In modern vehicle manufacturing, OEMs are increasingly integrating hot stamped components such as A-pillars, B-pillars, roof rails, and side impact beams, For instance in battery electric vehicles, to enhance crash resistance while reducing overall body weight by up to 15–25% compared to conventional stamping methods. Automotive manufacturers in Europe and Asia are expanding press hardening lines to support mass production of safety-optimized body structures for next-generation EV platforms.

The rapid expansion of electric mobility and stricter global crash safety regulations is further accelerating adoption of hot stamping technologies in body in white production. In addition, increasing use of press hardened boron steel in structural reinforcements is enabling manufacturers to meet stringent Euro NCAP and NHTSA safety standards while maintaining design flexibility and material efficiency. Pilot production programs in Germany and China during 2025 have demonstrated improved tensile strength levels exceeding 1500 MPa in hot stamped components, supporting enhanced vehicle crash performance under high-impact conditions

Hot Stamping Body in White Market Dynamics

Key Market Driver: Rising Demand For Lightweight And High-Safety Vehicle Structures

Automotive manufacturers are under increasing pressure to reduce vehicle weight, improve fuel efficiency, and enhance crash safety performance due to strict global emission norms and regulatory safety standards. Hot stamping technology enables the production of ultra-high-strength steel components that significantly improve structural integrity while reducing overall vehicle mass, making it highly suitable for modern automotive design requirements.

Automotive OEMs such as Volkswagen, BMW, and Toyota are increasingly adopting hot stamped parts in body in white structures to achieve better crash energy absorption and weight optimization. For instance in electric vehicles, lightweight body structures help extend driving range by improving overall energy efficiency, making hot stamping a critical enabling technology.

Similarly, rising global EV production and increasing adoption of multi-material vehicle architectures are driving demand for advanced press hardening processes in chassis and safety-critical components. Industry reports from 2024 indicate that hot stamped components can reduce vehicle body weight by approximately 20–30% compared to conventional high-strength steel stamping applications

Key Restraint/Challenge: High Production Cost And Complex Manufacturing Process

Hot stamping processes require specialized press hardening equipment, high-temperature furnaces, and precision tooling systems, which significantly increase capital investment and operational costs for manufacturers. The need for controlled heating and rapid cooling cycles adds complexity to production lines, limiting adoption among small and mid-sized automotive suppliers.

In addition, longer cycle times compared to conventional stamping processes reduce production efficiency in high-volume manufacturing environments. Material handling challenges and tool wear at high temperatures further increase maintenance requirements and overall production costs, making scalability difficult in cost-sensitive markets.

Benchmarking studies in automotive manufacturing indicate that hot stamping processes can increase production costs by 25–40% compared to conventional cold stamping methods, primarily due to energy-intensive heating cycles and specialized equipment requirements

Key Market Opportunity: Expansion In Electric Vehicle And Advanced Safety Architecture Applications

The rapid growth of electric vehicles and next-generation automotive safety systems is creating significant opportunities for hot stamping body in white technologies. EV manufacturers require lightweight yet highly durable structural components to support battery protection, crash safety, and vehicle efficiency requirements.

Automotive companies are increasingly integrating hot stamped ultra-high-strength steel components in EV platforms, For instance in battery enclosures, side impact structures, and roof reinforcements, to improve structural rigidity without increasing vehicle weight. In addition, increasing demand for autonomous and connected vehicles is further driving the need for stronger safety architectures capable of protecting sensitive electronic systems.

In addition, advancements in advanced high-strength steel (AHSS) grades and improved press hardening techniques are expanding application scope across premium and mass-market vehicles. Industry trials conducted in 2025 across Europe and Asia indicate that hot stamped body structures can improve crash energy absorption by nearly 20–35% while maintaining lightweight design targets, supporting broader adoption across global automotive OEMs

Hot Stamping Body in White Market Scope

The market is segmented on the basis of vehicle type, construction type, and material type.

• By Vehicle Type

On the basis of vehicle type, the Hot Stamping Body in White Market is segmented into Passenger Vehicles, Light Commercial Vehicles (LCV), Medium and Heavy Commercial Vehicles (MHCV), and Electric Vehicles. The Passenger Vehicles segment held the largest market revenue share of approximately 58.6% in 2025, driven by high production volumes, increasing demand for passenger safety features, and widespread adoption of lightweight high-strength body structures in mass-market and premium cars. The segment benefits from strict global crash safety regulations such as Euro NCAP and NHTSA standards, which are pushing OEMs to integrate hot stamped components in critical structural zones such as A-pillars, B-pillars, and side impact beams. Growing urbanization and rising disposable income are further supporting passenger car production, especially in Asia-Pacific markets such as China and India.

The Electric Vehicles segment is projected to register the fastest growth at a CAGR of 12.4% from 2026 to 2033, driven by rapid EV adoption, increasing need for lightweight battery enclosures, and growing focus on crash safety and structural rigidity in next-generation electric platforms across Asia-Pacific and Europe. Hot stamping is increasingly used in EV body structures to compensate for heavy battery packs by reducing overall vehicle weight and improving range efficiency. Automotive OEMs are also integrating press-hardened steel in battery protection systems to enhance thermal and impact safety. Government incentives supporting EV adoption and carbon neutrality targets are further accelerating segment expansion globally.

• By Construction Type

On the basis of construction type, the market is segmented into Monocoque and Frame Mounted structures. The Monocoque segment held the largest market revenue share of approximately 72.3% in 2025, driven by its extensive use in modern passenger vehicles due to superior weight efficiency, structural strength, and crash energy absorption capabilities. Monocoque structures allow better integration of hot stamped components into the vehicle body shell, improving stiffness and passenger safety performance. Increasing preference for unibody designs in sedans, hatchbacks, and electric vehicles is further strengthening segment dominance. OEMs are also leveraging monocoque architectures to optimize material usage and meet strict emission reduction targets.

The Frame Mounted segment is projected to grow at a steady CAGR of 6.8% from 2026 to 2033, driven by continued demand for commercial vehicles, SUVs, and off-road applications where durability and load-bearing capacity are critical design requirements. This structure is widely used in heavy-duty trucks and utility vehicles where structural robustness is prioritized over weight reduction. Increasing infrastructure development and logistics expansion are supporting demand for frame-mounted vehicles in emerging economies. In addition, manufacturers are incorporating hot stamped reinforcements in key chassis components to enhance durability under high-stress operating conditions.

• By Material Type

On the basis of material type, the market is segmented into Steel, Aluminium, Magnesium, and CFRP. The Steel segment held the largest market revenue share of approximately 83.7% in 2025, driven by the extensive use of boron steel in hot stamping processes due to its high tensile strength, cost efficiency, and suitability for mass production in automotive body structures. Steel remains the preferred material due to its excellent crash energy absorption properties and compatibility with existing press hardening infrastructure. Automakers continue to rely on advanced high-strength steel (AHSS) to achieve a balance between safety performance and manufacturing cost efficiency.

The CFRP segment is projected to register the fastest growth at a CAGR of 11.6% from 2026 to 2033, driven by increasing adoption in premium and electric vehicles where ultra-lightweight structures and high performance are prioritized to improve efficiency, range, and crash safety performance. CFRP is gaining traction in next-generation EV platforms due to its superior strength-to-weight ratio compared to conventional metals. Although currently expensive, ongoing material innovation and scaling of composite manufacturing processes are gradually improving affordability. Aerospace-inspired design integration and increasing use in luxury EV brands are further accelerating long-term adoption trends.

Hot Stamping Body in White Market Regional Analysis

North America Hot Stamping Body In White Market Insight

North America dominated the hot stamping body in white market with the largest revenue share of approximately 34.8% in 2025, supported by strong automotive production, high adoption of advanced safety technologies, and increasing demand for lightweight vehicle structures. The region benefits from the presence of leading OEMs and Tier-1 suppliers actively investing in press hardening technologies to improve crash performance and reduce vehicle weight. Rising consumer preference for SUVs and premium vehicles, combined with strict safety regulations such as FMVSS standards, is further accelerating adoption of hot stamped components across vehicle platforms. In addition, increasing electrification trends are pushing manufacturers to integrate lightweight ultra-high-strength steel parts to improve EV range efficiency and structural safety.

U.S. Hot Stamping Body In White Market Insight

The U.S. hot stamping body in white market captured the largest revenue share in 2025 within North America, driven by rapid adoption of advanced automotive manufacturing technologies and strong presence of global OEMs such as Ford, General Motors, and Stellantis. The growing shift toward electric vehicles and lightweight vehicle architectures is increasing demand for hot stamped components in safety-critical structures such as side impact beams and battery enclosures. Rising investments in automotive R&D and automation in stamping facilities are further supporting market expansion. In addition, increasing consumer demand for high safety-rated vehicles and government emphasis on emission reduction targets are encouraging OEMs to adopt press hardened steel solutions in next-generation vehicle platforms.

Europe Hot Stamping Body In White Market Insight

The Europe hot stamping body in white market is expected to witness the fastest growth rate from 2026 to 2033, driven by stringent carbon emission regulations, strong focus on vehicle safety standards, and rapid adoption of electric mobility solutions. Automotive manufacturers in the region are increasingly using hot stamping technology to achieve lightweight design requirements while maintaining structural integrity and crash performance. The expansion of EV production in countries such as Germany, France, and Sweden is further accelerating demand for press hardened steel components. In addition, strong emphasis on sustainability and material efficiency is encouraging OEMs to shift toward advanced high-strength steel solutions in body in white applications.

U.K. Hot Stamping Body In White Market Insight

The U.K. hot stamping body in white market is expected to witness steady growth from 2026 to 2033, driven by increasing focus on vehicle safety, electrification, and lightweight material adoption. Growing demand for premium passenger vehicles and electric SUVs is supporting the integration of hot stamped components in structural body parts. The country’s strong automotive engineering ecosystem and increasing investments in EV manufacturing facilities are further boosting market growth. In addition, rising awareness regarding carbon emission reduction and fuel efficiency is encouraging OEMs to adopt advanced press hardening technologies in vehicle body design.

Germany Hot Stamping Body In White Market Insight

The Germany hot stamping body in white market is expected to witness strong growth from 2026 to 2033, supported by its advanced automotive manufacturing base and leadership in premium vehicle production. Germany is a key hub for automotive innovation, with OEMs such as Volkswagen, BMW, and Mercedes-Benz extensively adopting hot stamped components for crash safety and lightweight design optimization. The country’s strong focus on engineering precision and sustainability is accelerating the use of ultra-high-strength steel in body in white structures. In addition, increasing EV production and stringent EU emission regulations are further driving adoption of press hardening technologies across automotive platforms.

Asia-Pacific Hot Stamping Body In White Market Insight

The Asia-Pacific hot stamping body in white market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid vehicle production growth, expanding automotive manufacturing base, and rising EV adoption in countries such as China, Japan, and India. The region is becoming a major hub for cost-effective automotive production, encouraging OEMs to adopt hot stamping technologies for improved safety and lightweight performance. Government initiatives promoting electric mobility and industrial automation are further strengthening market expansion. In addition, increasing investments in automotive press hardening lines are enhancing production capacity across major APAC economies.

Japan Hot Stamping Body In White Market Insight

The Japan hot stamping body in white market is expected to grow steadily from 2026 to 2033 due to strong demand for high-quality automotive components and advanced manufacturing technologies. Japanese OEMs such as Toyota, Honda, and Nissan are increasingly integrating hot stamped parts to improve crash safety and reduce vehicle weight. The country’s emphasis on precision engineering and material innovation is driving adoption of advanced high-strength steel solutions. In addition, rising EV development and hybrid vehicle production are further supporting the integration of press hardened components in next-generation vehicle platforms.

China Hot Stamping Body In White Market Insight

The China hot stamping body in white market accounted for the largest revenue share in Asia-Pacific in 2025, driven by massive automotive production, rapid urbanization, and strong growth in electric vehicle manufacturing. China is a global leader in EV adoption, and manufacturers are increasingly using hot stamped components to improve structural safety and reduce vehicle weight. Strong domestic supply chain capabilities and cost-efficient production infrastructure are further supporting market expansion. In addition, government initiatives promoting new energy vehicles and smart manufacturing are accelerating the adoption of press hardening technologies across automotive OEMs in the country.

Hot Stamping Body in White Market Share

The Hot Stamping Body in White industry is primarily led by well-established companies, including:

• Autokiniton (U.S.)

• AISIN CORPORATION (Japan)

• Gestamp (Spain)

• BENTELER International (Germany)

• MarkLines Co., Ltd. (Japan)

• voestalpine AG (Austria)

• CIE Automotive (Spain)

• Magna International Inc (Canada)

• KIRCHHOFF Automotive GmbH (Germany)

• Jay Bharat Maruti Ltd. (India)

• thyssenkrupp System Engineering GmbH (Germany)

• Martinrea International Inc. (Canada)

• Norsk Hydro ASA (Norway)

• DURA AUTOMOTIVE SYSTEMS (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.