Global Hyaluronic Acid Injectable Fillers Market

Market Size in USD Billion

USD

4.04 Billion

USD

9.03 Billion

2024

2032

USD

4.04 Billion

USD

9.03 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.04 Billion | |

| USD 9.03 Billion | |

| % | |

|

Hyaluronic Acid Injectable Fillers Market Size

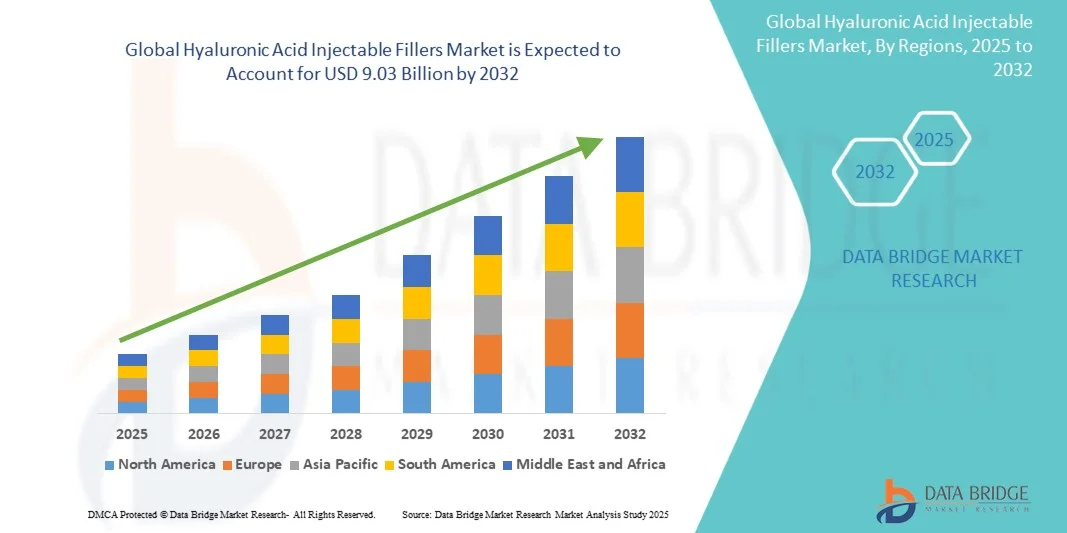

- The global hyaluronic acid injectable fillers market size was valued at USD 4.04 billion in 2024 and is expected to reach USD 9.03 billion by 2032, at a CAGR of 10.58% during the forecast period

- The market growth for hyaluronic acid injectable fillers is largely fueled by increasing awareness of aesthetic and cosmetic procedures, rising consumer preference for minimally invasive treatments, and technological advancements in filler formulations that offer improved safety, longevity, and natural-looking results

- Furthermore, growing disposable incomes, expanding medical tourism, and the rising influence of social media and celebrity endorsements are driving demand, accelerating the adoption of hyaluronic acid injectable fillers solutions, thereby significantly boosting the overall growth of the industry

Hyaluronic Acid Injectable Fillers Market Analysis

- Hyaluronic Acid Injectable Fillers, offering minimally invasive cosmetic enhancements for facial aesthetics, are increasingly popular due to their effectiveness in reducing wrinkles, restoring volume, and achieving natural-looking results with minimal downtime

- The escalating demand for these fillers is primarily fueled by rising awareness of aesthetic procedures, increasing disposable incomes, growing influence of social media, and the preference for non-surgical cosmetic treatments

- North America dominated the hyaluronic acid injectable Fillers market with the largest revenue share of 43.5% in 2024, driven by advanced healthcare infrastructure, high adoption of aesthetic procedures, and a strong presence of key industry players, with the U.S. experiencing substantial growth in filler treatments, particularly in dermatology and cosmetic clinics

- Asia-Pacific is expected to be the fastest-growing region in the hyaluronic acid injectable Fillers market during the forecast period, accounting for 27.3% of the market in 2024, due to increasing urbanization, rising disposable incomes, growing medical tourism, and expanding awareness of minimally invasive aesthetic procedures in countries such as India and China

- The prescription segment dominated the largest market revenue share of 67.4% in 2024, driven by the requirement for trained medical professionals to administer injectable fillers safely

Report Scope and Hyaluronic Acid Injectable Fillers Market Segmentation

|

Attributes |

Hyaluronic Acid Injectable Fillers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hyaluronic Acid Injectable Fillers Market Trends

“Enhanced Convenience Through Advanced Formulations and Minimally Invasive Procedures”

- A significant and accelerating trend in the global hyaluronic acid injectable fillers market is the increasing development of advanced formulations and minimally invasive delivery techniques. These innovations enhance treatment precision, longevity, and patient comfort, significantly improving user satisfaction and procedural outcomes

- For instance, new cross-linked hyaluronic acid fillers are designed to integrate seamlessly with tissue, offering natural-looking results and reducing the risk of adverse effects. Similarly, combination therapies with botulinum toxin or collagen stimulators are being introduced to achieve multi-dimensional aesthetic improvements, providing comprehensive facial rejuvenation

- AI and digital imaging technologies are being adopted to assist practitioners in precise injection planning, predicting outcomes, and optimizing filler volumes for individualized patient needs. Enhanced visualization tools enable better assessment of facial contours and allow real-time procedural adjustments, increasing treatment efficacy

- The integration of novel delivery systems, such as microcannulas and precision syringes, facilitates targeted filler placement, minimizing bruising, swelling, and downtime. These advancements contribute to a safer and more predictable procedure, attracting more patients to minimally invasive cosmetic interventions

- The trend toward combination aesthetic procedures, personalized treatment plans, and advanced product formulations is fundamentally reshaping patient expectations in cosmetic dermatology. Consequently, key market players are developing fillers with enhanced durability, biocompatibility, and versatility to meet growing consumer demand

- The increasing focus on natural, long-lasting, and customizable aesthetic results is driving widespread adoption across clinics, hospitals, and specialty dermatology centers. Patients increasingly prefer treatments that deliver immediate effects with minimal recovery time, fueling market growth

Hyaluronic Acid Injectable Fillers Market Dynamics

Driver

“Rising Demand for Aesthetic Enhancements and Minimally Invasive Procedures”

- The growing emphasis on cosmetic appearance, anti-aging, and minimally invasive procedures is a major driver of the global Hyaluronic Acid Injectable Fillers market. Increasing social media influence and aesthetic awareness have fueled demand across age groups

- For instance, in 2024, several leading aesthetic clinics launched advanced hyaluronic acid filler lines with improved longevity and tissue integration, highlighting the commercial potential of innovative formulations. These strategies by key companies are expected to accelerate market growth in the forecast period

- Rising disposable incomes and expanding middle-class populations, particularly in emerging economies, are enabling more individuals to opt for elective cosmetic procedures, further boosting market demand

- The trend toward non-surgical facial rejuvenation, including wrinkle reduction, lip augmentation, and cheek contouring, is creating opportunities for new product launches and combination therapies

- Growing availability of professional training programs and aesthetic certifications for practitioners ensures safe, effective treatment delivery, which encourages patient confidence and adoption

- Increasing collaborations between product manufacturers and dermatology clinics are enhancing product accessibility, treatment education, and patient engagement, strengthening market penetration

Restraint/Challenge

“Concerns Regarding Safety, Side Effects, and High Costs”

- Safety concerns, potential side effects, and adverse reactions such as swelling, bruising, and nodules can pose challenges to market growth, particularly among first-time patients or in regions with limited practitioner training

- Regulatory hurdles, including strict approval processes for injectable fillers, may delay market entry for new products and limit innovation in certain countries

- For instance, the FDA’s comprehensive evaluation of new hyaluronic acid formulations can extend the launch timeline and impact early adoption

- The relatively high cost of premium hyaluronic acid injectable fillers can deter price-sensitive consumers, especially in developing regions, restricting broader adoption. While more affordable generic alternatives are emerging, differences in quality and longevity may influence patient preferences

- Patient awareness regarding correct administration techniques and post-procedure care is crucial to prevent complications; lack of information may reduce treatment uptake

- Competition from alternative cosmetic procedures, such as botulinum toxin, autologous fat grafting, and laser therapies, presents a market challenge, particularly among patients seeking comprehensive aesthetic solutions

- Ensuring product safety, practitioner training, and cost-effective options are vital to overcoming barriers and sustaining long-term market growth

Continuous research on biocompatible formulations, longer-lasting results, and reduced side effects will remain key to mitigating concerns and expanding consumer confidence in injectable fillers

Hyaluronic Acid Injectable Fillers Market Scope

The market is segmented on the basis of product type, application, end user, and mode of purchase.

• By Product Type

On the basis of product type, the Hyaluronic Acid Injectable Fillers market is segmented into cross-linked hyaluronic acid fillers and non-cross-linked hyaluronic acid fillers. The cross-linked hyaluronic acid fillers segment dominated the largest market revenue share of 57.8% in 2024, driven by their longer-lasting effects, higher viscosity, and better suitability for facial contouring and wrinkle reduction procedures. Cross-linked fillers are preferred by dermatologists and aesthetic practitioners for deep tissue augmentation, offering predictable and consistent results. The growing popularity of minimally invasive cosmetic procedures, combined with rising disposable income in key markets, supports sustained demand. Advanced formulations with improved biocompatibility and reduced side effects have further strengthened the segment’s position. The segment also benefits from enhanced patient satisfaction, repeat treatments, and strong clinical endorsement in aesthetic practices. Product innovations focusing on dual-phase and monophasic cross-linked gels improve ease of administration, further bolstering adoption. Ongoing marketing campaigns emphasizing longer-lasting results and natural aesthetics also drive consumer preference.

The non-cross-linked hyaluronic acid fillers segment is anticipated to witness the fastest CAGR of 11.2% from 2025 to 2032, owing to growing demand for subtle volumization, hydration, and skin rejuvenation applications. Non-cross-linked fillers are widely used for fine line treatment, mesotherapy, and superficial skin enhancement due to their lower viscosity and natural integration into dermal tissues. Rising awareness about non-invasive cosmetic procedures and an expanding pool of aesthetic clinics offering non-cross-linked formulations accelerate growth. The segment is further fueled by innovations in low-molecular-weight hyaluronic acid gels, enhancing absorption and minimizing swelling or bruising. Patient preference for softer, reversible treatments, and growing adoption among younger demographics contribute to rapid uptake. Additionally, increasing use in combination with other skincare procedures and injectables strengthens market penetration. The expanding presence of trained practitioners, online education, and digital marketing campaigns targeting cosmetic-conscious consumers also support segment growth.

• By Application

On the basis of application, the Hyaluronic Acid Injectable Fillers market is segmented into wrinkle reduction & fine lines, lip augmentation, cheek/facial contouring, and others. The wrinkle reduction & fine lines segment dominated the largest market revenue share of 48.5% in 2024, driven by the prevalence of aging populations, increasing demand for minimally invasive cosmetic procedures, and rising awareness about aesthetic enhancements. Dermal fillers in this category are commonly used for forehead lines, crow’s feet, and nasolabial folds, offering quick, effective, and non-surgical results. The segment benefits from high repeat treatment rates due to gradual filler absorption and the need for maintenance. Clinician preference for reliable, approved formulations ensures consistent adoption. Marketing campaigns emphasizing youthful appearance and natural results have strengthened consumer confidence. Integration with other treatments such as botulinum toxins and skin rejuvenation therapies expands the scope. Advanced training programs for aesthetic professionals further contribute to segment dominance.

The lip augmentation segment is projected to witness the fastest CAGR of 12.8% from 2025 to 2032, fueled by rising popularity of fuller lips influenced by social media trends and celebrity endorsements. Consumers increasingly seek non-surgical, customizable lip enhancement solutions, driving demand. Innovations in softer, highly malleable hyaluronic acid formulations offer precise control over shape, volume, and symmetry, minimizing complications. Expanding aesthetic clinics in emerging markets, combined with growing disposable income and urbanization, further accelerate growth. Rising awareness about lip hydration and volume restoration as part of overall facial aesthetics strengthens adoption. Additionally, the segment benefits from influencer-driven marketing campaigns and social media exposure, encouraging first-time and repeat treatments.

• By End User

On the basis of end user, the Hyaluronic Acid Injectable Fillers market is segmented into hospitals & clinics, dermatology & aesthetic clinics, and medical spas & cosmetic centers. The dermatology & aesthetic clinics segment dominated the largest market revenue share of 52.6% in 2024, driven by specialized services, expert practitioners, and high consumer trust in certified aesthetic professionals. These clinics offer advanced treatment protocols, tailored injection techniques, and combination therapies, ensuring optimal outcomes and safety. The segment benefits from repeat visits and loyalty programs, increasing overall revenue share. The growing number of certified dermatologists and aesthetic professionals enhances the availability of high-quality injectable procedures. Clinics also benefit from marketing campaigns highlighting minimally invasive procedures and natural-looking results. Urban centers and metro regions witness higher clinic density, supporting accessibility. Ongoing innovations in treatment techniques, patient education programs, and social media-driven awareness contribute to segment dominance.

The medical spas & cosmetic centers segment is anticipated to witness the fastest CAGR of 13.1% from 2025 to 2032, due to increasing consumer preference for non-invasive, holistic cosmetic treatments in premium wellness environments. Spas offer bundled services, combining hyaluronic acid fillers with skincare, facials, and wellness therapies, attracting new and repeat clients. Rising disposable incomes, lifestyle-driven aesthetics, and influencer marketing drive segment adoption. The availability of flexible appointment schedules and discreet settings enhances consumer comfort. Furthermore, the segment benefits from partnerships with product suppliers and training programs, ensuring high-quality service delivery. Expanding in suburban and semi-urban regions provides access to younger demographics seeking aesthetic enhancements.

• By Mode of Purchase

On the basis of mode of purchase, the Hyaluronic Acid Injectable Fillers market is segmented into prescription and over-the-counter (OTC). The prescription segment dominated the largest market revenue share of 67.4% in 2024, driven by the requirement for trained medical professionals to administer injectable fillers safely. Regulatory approvals, clinical supervision, and quality assurance protocols support this segment’s leadership. Prescribed fillers are preferred for advanced procedures such as cheek contouring, lip augmentation, and deep wrinkle correction, offering controlled and reliable outcomes. Hospitals, aesthetic clinics, and dermatology centers primarily dispense prescription products, ensuring patient safety and treatment efficacy. Marketing campaigns and professional endorsements further strengthen consumer confidence in prescribed products. The segment benefits from repeat treatments due to gradual absorption and long-lasting effects, maintaining revenue dominance.

The OTC segment is projected to witness the fastest CAGR of 9.7% from 2025 to 2032, driven by the growing availability of lower-concentration, self-administered fillers and topical hyaluronic acid gels for skin hydration and minor enhancements. Rising awareness of home-based aesthetic solutions, convenience, and cost-effectiveness is propelling demand. OTC products are increasingly popular among younger demographics seeking preventive skin care and minor cosmetic improvements. E-commerce channels, online tutorials, and influencer-driven marketing campaigns are accelerating adoption. The segment benefits from product innovations that ensure safety, ease of use, and non-invasive outcomes, further expanding its consumer base.

Hyaluronic Acid Injectable Fillers Market Regional Analysis

- North America dominated the hyaluronic acid injectable fillers market with the largest revenue share of 43.5% in 2024, driven by advanced healthcare infrastructure, high adoption of aesthetic procedures, and a strong presence of key industry players. The U.S. experienced substantial growth in filler treatments, particularly in dermatology and cosmetic clinics, fueled by rising consumer awareness, increasing disposable incomes, and demand for minimally invasive aesthetic solutions

- The market is supported by well-established regulatory frameworks, availability of FDA-approved products, and widespread presence of trained aesthetic professionals. Rising preference for non-surgical cosmetic enhancements, combined with high urbanization and growing medical tourism in key cities, further accelerates adoption. Marketing campaigns by leading aesthetic brands and clinics, along with celebrity and influencer endorsements, contribute to heightened consumer interest

- Repeat procedures and maintenance treatments for wrinkle reduction, lip augmentation, and facial contouring strengthen the market share. The segment also benefits from technological advancements in filler formulations, such as cross-linked and hyaluronic acid blends, offering longer-lasting and natural results

U.S. Hyaluronic Acid Injectable Fillers Market Insight

The U.S. hyaluronic acid injectable fillers market captured the largest revenue share in North America in 2024, driven by rapid adoption of aesthetic procedures and growing awareness of dermal filler benefits. Dermatology and cosmetic clinics are increasingly integrating advanced filler technologies for wrinkle reduction, lip augmentation, and facial contouring, meeting rising patient demand. The presence of well-trained practitioners, robust healthcare infrastructure, and comprehensive insurance coverage in certain procedures facilitates market growth. Consumer inclination toward minimally invasive procedures with reduced downtime is further propelling adoption. The availability of diverse product portfolios from leading brands, alongside promotional activities and awareness campaigns, enhances patient trust and encourages repeat treatments. The U.S. market remains a benchmark for innovation, with ongoing clinical trials, product launches, and combination therapies supporting sustained expansion.

Europe Hyaluronic Acid Injectable Fillers Market Insight

The Europe hyaluronic acid injectable fillers market is projected to expand at a substantial CAGR during the forecast period, primarily driven by advanced healthcare systems, increasing urbanization, and rising demand for aesthetic enhancements. Consumers are seeking minimally invasive solutions for wrinkle reduction, facial contouring, and lip augmentation, boosting adoption in dermatology and cosmetic clinics. Countries such as Germany, France, and the U.K. are witnessing high growth due to robust infrastructure, regulatory approvals, and high disposable incomes. The market benefits from increasing awareness about aging, anti-aging treatments, and non-surgical cosmetic procedures. Marketing campaigns and professional endorsements further stimulate demand. Repeat treatments and combination therapies enhance revenue potential. Aesthetic clinics continue to invest in training and advanced techniques, ensuring better clinical outcomes and patient satisfaction. Rising demand in multi-family housing areas, urban centers, and tourist destinations also contributes to growth.

Asia-Pacific Hyaluronic Acid Injectable Fillers Market Insight

Asia-Pacific hyaluronic acid injectable fillers market is expected to be the fastest-growing region in the Hyaluronic Acid Injectable Fillers market during the forecast period, accounting for 27.3% of the market in 2024, driven by increasing urbanization, rising disposable incomes, growing medical tourism, and expanding awareness of minimally invasive aesthetic procedures in countries such as India and China. The region’s market is fueled by rising demand for wrinkle reduction, lip augmentation, and facial contouring in both metropolitan and tier-2 cities. Expanding networks of dermatology and aesthetic clinics, coupled with the availability of trained practitioners and advanced filler formulations, support rapid growth. India is witnessing particularly strong adoption due to growing healthcare awareness, increasing disposable income, and preference for non-surgical cosmetic solutions. China’s large patient pool, combined with the expansion of private aesthetic clinics and technological adoption, drives substantial revenue. Rising popularity of social media-driven cosmetic trends, influencer marketing, and increasing affordability of high-quality fillers accelerate market expansion. The focus on minimally invasive procedures, short recovery times, and natural aesthetic results ensures robust CAGR growth throughout the forecast period.

China Hyaluronic Acid Injectable Fillers Market Insight

The China hyaluronic acid injectable fillers market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s expanding middle class, rapid urbanization, and high rates of technological and medical adoption. The increasing preference for cosmetic procedures in major urban centers, supported by a network of private aesthetic clinics and dermatology specialists, drives growth. Demand for wrinkle reduction, lip augmentation, and cheek/facial contouring is particularly strong in metropolitan cities. Marketing initiatives, social media influence, and medical tourism further strengthen adoption. High patient awareness and increasing disposable income encourage repeat procedures and preference for premium formulations.

India Hyaluronic Acid Injectable Fillers Market Insight

The India hyaluronic acid injectable fillers market is expected to grow at the fastest CAGR during the forecast period, fueled by rising awareness of aesthetic procedures, increasing disposable incomes, expanding access to dermatology and cosmetic clinics, and growing medical tourism. Non-surgical cosmetic procedures are becoming increasingly popular among urban populations, driven by affordability, convenience, and social media influence. Key growth factors include the proliferation of trained practitioners, availability of FDA and CE-approved products, and adoption of advanced filler technologies. Increasing consumer preference for minimally invasive treatments with shorter recovery times is supporting rapid market adoption. The expanding private healthcare sector and rising number of cosmetic centers in tier-1 and tier-2 cities contribute significantly to growth.

Hyaluronic Acid Injectable Fillers Market Share

The Hyaluronic Acid Injectable Fillers industry is primarily led by well-established companies, including:

- Hyliion Therapeutics (U.S.)

- Galderma (Switzerland)

- Revance Therapeutics (U.S.)

- MediTox (South Korea)

- Luminera (Israel)

- Anika Therapeutics (U.S.

- Hugel, Inc. (South Korea)

- Teoxane SA (Switzerland)

- Biomedica (Austria)

- Prollenium Medical Technologies (Canada)

- Caregen Co., Ltd. (South Korea)

- MediTox Inc. (South Korea)

- Suneva Medical (U.S.)

- Lonza Group (Switzerland)

Latest Developments in Global Hyaluronic Acid Injectable Fillers Market

- In June 2023, Galderma received FDA approval for its newest hyaluronic acid filler, Restylane Eyelight, designed to improve the appearance of undereye hollows for up to 18 months. The product utilizes NASHA Technology, offering a unique formulation in the U.S. market

- In February 2025, Evolus announced the FDA approval of its new hyaluronic acid fillers, EVOLYSSE FORM and EVOLYSSE™ SMOOTH. These products employ Cold-X technology, preserving the natural structure of the hyaluronic acid molecule, leading to more natural-looking and longer-lasting outcomes

- In September 2025, Allergan Aesthetics launched the "Naturally You with Injectable Hyaluronic Acid Fillers" campaign, aiming to educate consumers about the safety and natural-looking outcomes of HA injectable fillers. This initiative focuses on correcting misinformation to elevate understanding and celebrate the safe, natural-looking outcomes possible with hyaluronic acid injectable fillers

- In August 2025, Revance launched the Teoxane RHA Collection with Mepivacaine, an FDA-approved hyaluronic acid filler designed to improve patient comfort during aesthetic procedures. The innovative filler line challenges the status quo by replacing the local anesthetic with mepivacaine, providing an anesthetic effect comparable to currently available products but with reduced local vasodilation, which may result in less bruising

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.