Global Hydrocephalus Treatment Market

Market Size in USD Billion

USD

2.00 Billion

USD

2.53 Billion

2024

2032

USD

2.00 Billion

USD

2.53 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.00 Billion | |

| USD 2.53 Billion | |

| % | |

|

Hydrocephalus Treatment Market Size

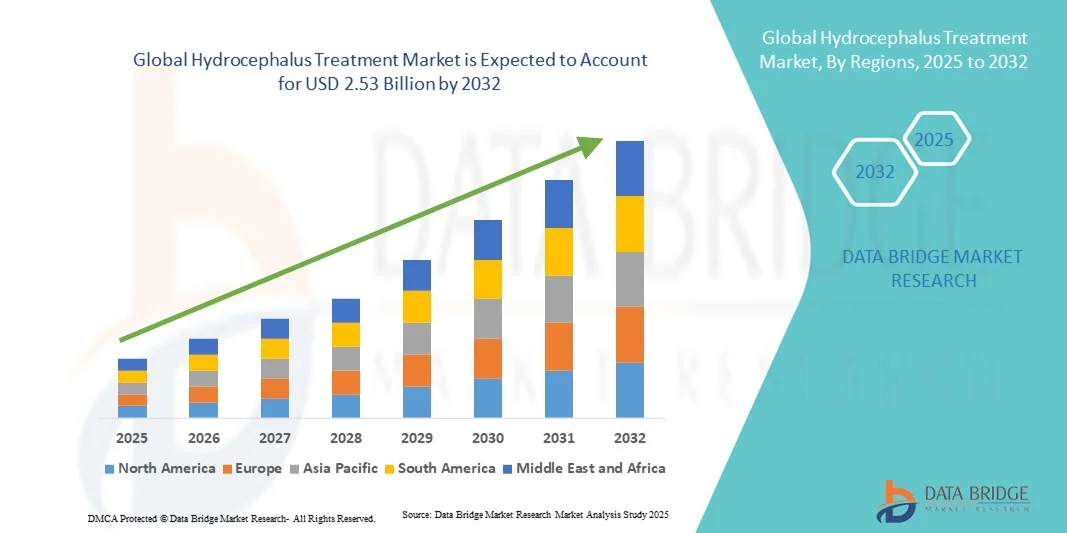

- The global hydrocephalus treatment market size was valued at USD 2.00 billion in 2024 and is expected to reach USD 2.53 billion by 2032, at a CAGR of 3.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of hydrocephalus, advancements in diagnostic imaging, and the development of innovative treatment options, including shunt systems and endoscopic procedures, which are improving patient outcomes and quality of life

- Furthermore, rising awareness among healthcare professionals and caregivers, along with the growing availability of minimally invasive and technologically advanced treatment solutions, is establishing hydrocephalus treatment as a critical focus area in neurosurgery and pediatric care. These converging factors are accelerating the adoption of hydrocephalus treatment solutions, thereby significantly boosting the industry's growth

Hydrocephalus Treatment Market Analysis

- Hydrocephalus Treatment, including shunt systems, endoscopic third ventriculostomy (ETV), and other interventional procedures, has become an essential component of modern neurosurgical care due to its effectiveness in managing cerebrospinal fluid accumulation and improving patient outcomes

- The growing demand for hydrocephalus treatment is primarily fueled by the increasing prevalence of hydrocephalus, advancements in diagnostic imaging and treatment technologies, and rising awareness among healthcare professionals and caregivers about early intervention

- North America dominated the hydrocephalus treatment market with the largest revenue share of 41.2% in 2024, supported by advanced healthcare infrastructure, high adoption of innovative neurosurgical procedures, and strong R&D activities in the U.S., driving wider treatment adoption

- Asia-Pacific is expected to be the fastest-growing region in the hydrocephalus treatment market during the forecast period due to increasing urbanization, improving healthcare access, and rising disposable incomes in countries such as China and India

- The Shunt Insertion segment dominated the largest market revenue share of 53.4% in 2024, as it remains the standard and most effective intervention for most types of hydrocephalus

Report Scope and Hydrocephalus Treatment Market Segmentation

|

Attributes |

Hydrocephalus Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hydrocephalus Treatment Market Trends

Advancements in Innovative Therapies and Digital Health Integration

- A significant and accelerating trend in the global hydrocephalus treatment market is the increasing adoption of minimally invasive procedures, AI-assisted diagnostics, and digital monitoring systems. These technologies are enhancing patient outcomes, optimizing treatment plans, and enabling timely intervention

- For instance, in July 2023, Medtronic launched the AI-enabled ventriculoperitoneal (VP) shunt monitoring system, allowing clinicians to remotely track shunt functionality and detect potential blockages early, reducing the risk of complications

- The integration of digital health platforms and remote monitoring is also improving long-term care for hydrocephalus patients. For instance, in March 2022, Integra LifeSciences partnered with a telehealth provider to deliver virtual post-operative follow-ups and symptom tracking, ensuring continuous patient monitoring without frequent hospital visit

- Moreover, the trend toward novel shunt designs, endoscopic third ventriculostomy (ETV), and programmable valves is reshaping treatment expectations. For instance, in May 2024, Sophysa introduced a next-generation programmable valve designed to provide precise cerebrospinal fluid (CSF) pressure control and reduce the need for revision surgeries

- These developments, combining advanced surgical devices with AI-assisted monitoring and telehealth, are creating more personalized, proactive, and patient-centric hydrocephalus care models worldwide

Hydrocephalus Treatment Market Dynamics

Driver

Rising Incidence and Growing Awareness of Early Intervention

- The increasing prevalence of hydrocephalus, particularly in neonatal and aging populations, is a key driver for market growth

- For instance, in April 2023, Boston Scientific reported a 10% increase in VP shunt procedures in North America, reflecting greater early detection and proactive treatment strategies

- Advances in treatment technologies, such as smart shunts, endoscopic procedures, and minimally invasive catheters, are further encouraging adoption. For instance, in October 2024, Integra LifeSciences launched a new endoscopic system that reduces surgical time and improves precision in CSF flow management

- Government initiatives and funding for neurological research are also supporting market expansion. For instance, in August 2022, the National Institutes of Health (NIH) in the U.S. allocated USD 8 million for hydrocephalus research, aimed at developing safer and more effective treatment approaches

- Increasing awareness among healthcare providers and parents about early intervention is boosting treatment rates. For instance, in September 2023, a global awareness campaign by Hydrocephalus Association helped improve early diagnosis in infants, leading to timely surgical intervention

- Expansion of healthcare infrastructure in emerging economies is driving growth. For instance, in July 2023, Medtronic collaborated with hospitals in India to expand access to minimally invasive hydrocephalus treatment technologies in rural and semi-urban regions

- Rising adoption of integrated patient management programs, combining surgery, monitoring, and follow-up care, is also fueling demand. For instance, in November 2024, Sophysa initiated a patient support program in Europe that provides continuous remote monitoring alongside valve therapy

Restraint/Challenge

High Treatment Costs and Limited Accessibility

- Despite advances, the high cost of hydrocephalus treatments, particularly shunt implantation and advanced monitoring systems, remains a significant barrier to adoption

- For instance, in April 2024, a study reported that the average cost of VP shunt implantation in the U.S. exceeds USD 25,000, making it unaffordable for many patients in developing regions

- Limited availability of specialized neurosurgeons and advanced treatment facilities restricts access, particularly in low-income regions. For instance, in December 2023, a survey in Southeast Asia found that over 40% of hydrocephalus patients experienced delays in surgical intervention due to limited hospital infrastructure

- Regulatory hurdles and approval delays for new devices and shunt technologies pose additional challenges. For instance, in September 2025, Sophysa announced extended regulatory review timelines for its new programmable valve in certain European countries, slowing market penetration

- Post-surgical complications and the need for shunt revisions can increase long-term treatment costs and patient burden. For instance, in January 2024, a multi-center study reported that nearly 30% of pediatric hydrocephalus patients required shunt revision within the first year after surgery

- Unequal distribution of advanced treatment infrastructure between urban and rural areas limits patient access to specialized care. For instance, in March 2025, WHO highlighted that many rural communities in Africa and Latin America lack access to neurosurgical facilities capable of hydrocephalus treatment

- Addressing these challenges through innovative, cost-effective shunt designs, telemedicine follow-up programs, and increased training for neurosurgeons is critical for sustained growth of the hydrocephalus treatment market

Hydrocephalus Treatment Market Scope

The market is segmented on the basis of type, age group, diagnostic, treatment type, and end user.

- By Type

On the basis of type, the Hydrocephalus Treatment market is segmented into Congenital Hydrocephalus, Acquired Hydrocephalus, Normal-Pressure Hydrocephalus, and Ex-Vacuo Hydrocephalus. The Congenital Hydrocephalus segment dominated the largest market revenue share of 45.1% in 2024, driven by its higher incidence in newborns and infants globally. Early detection through routine prenatal screening and neonatal check-ups has led to timely diagnosis and intervention, increasing the adoption of effective treatments. The segment benefits from well-established surgical protocols, primarily shunt insertions, which remain the standard of care. Advances in minimally invasive surgeries, coupled with supportive postoperative care, enhance patient outcomes and reduce complications. The presence of specialized pediatric neurosurgical centers further strengthens market dominance. In addition, government initiatives focusing on child health and early intervention programs support widespread treatment access. The segment’s dominance is also attributed to the higher awareness among caregivers and clinicians regarding congenital hydrocephalus management. Growing investments in neonatal care infrastructure, integration of advanced imaging technologies, and rising hospital-based treatments contribute to sustained revenue. Public and private healthcare funding for congenital disorders further reinforces this segment's position in the market.

The Normal-Pressure Hydrocephalus (NPH) segment is anticipated to witness the fastest CAGR of 10.8% from 2025 to 2032, driven by the increasing prevalence of NPH in the aging population and growing awareness among clinicians and patients. Early recognition of symptoms such as gait disturbance, urinary incontinence, and cognitive decline has accelerated diagnosis and treatment adoption. Advancements in diagnostic modalities, including MRI and CT scans, facilitate accurate and timely identification. Minimally invasive interventions such as ventriculoperitoneal shunting and endoscopic third ventriculostomy are increasingly preferred due to lower risk profiles and improved patient outcomes. Increasing healthcare access, rising geriatric population, and government programs supporting elderly care contribute to market expansion. Continuous R&D in treatment techniques and postoperative care enhances efficacy. Growing clinical guidelines recommending early surgical intervention and rehabilitation improve adoption rates. In addition, collaborations between hospitals and geriatric care centers ensure better follow-up and monitoring. Increasing patient awareness campaigns and education on early symptoms also drive faster adoption. Expansion of insurance coverage for NPH treatments further supports market growth. Telemedicine and remote monitoring solutions are emerging as key enablers in follow-up care. Overall, the segment is witnessing accelerated growth due to rising awareness, improved diagnostic capabilities, and aging demographics.

- By Age Group

On the basis of age group, the Hydrocephalus Treatment market is segmented into Infants, Children, and Adults. The Infants segment held the largest market revenue share of 48.3% in 2024, due to the high incidence of congenital hydrocephalus diagnosed at birth or during early months. Early surgical interventions, primarily shunt insertions, are critical to prevent long-term neurological deficits, driving market demand. The segment benefits from widespread neonatal screening programs, advanced pediatric imaging facilities, and increasing hospital infrastructure dedicated to infant care. Rising awareness among parents and caregivers regarding early intervention is a key factor. Access to specialized pediatric neurosurgeons, high adoption of minimally invasive surgeries, and supportive postoperative care contribute to the dominance. Government healthcare initiatives and private funding for neonatal treatments further enhance adoption. The presence of academic research hospitals and clinical trials focused on infant hydrocephalus ensures ongoing improvement in treatment outcomes. Adoption of innovative shunt technologies, endoscopic procedures, and continuous monitoring protocols drives segment growth. Public health campaigns and educational programs for caregivers reinforce timely treatment. The segment’s dominance is also supported by rising demand for comprehensive care in tertiary hospitals. Increasing investments in pediatric healthcare infrastructure globally continue to strengthen this segment’s market position.

The Adults segment is expected to witness the fastest CAGR of 11.5% from 2025 to 2032, primarily driven by the rising prevalence of acquired and normal-pressure hydrocephalus among the elderly population. Growing awareness of hydrocephalus symptoms in adults, including cognitive decline and motor dysfunction, has led to increased diagnosis through advanced imaging such as MRI and CT scans. Minimally invasive surgical options and improved postoperative care are fueling treatment adoption. Expanding geriatric healthcare infrastructure, rising insurance coverage, and early intervention programs support rapid growth. The segment benefits from increased hospital-based treatments, access to specialty neurosurgical centers, and training programs for adult care management. R&D in novel shunt designs and endoscopic procedures improves patient outcomes, encouraging higher adoption rates. Integration of rehabilitation and follow-up care enhances quality of life for patients. Awareness campaigns targeting caregivers and clinicians further accelerate treatment uptake. The aging population in developed and emerging economies contributes significantly to growth. Telehealth and homecare solutions for postoperative monitoring are emerging as key facilitators. Collaboration between hospitals and research institutions ensures continuous advancement in adult hydrocephalus management.

- By Diagnostic

On the basis of diagnostic, the Hydrocephalus Treatment market is segmented into CT scan–Head, MRI, and Head Ultrasound. The MRI segment dominated the largest market revenue share of 50.7% in 2024, due to its superior imaging quality, non-invasive nature, and ability to detect early structural abnormalities in the brain. MRI facilitates accurate diagnosis of hydrocephalus type, severity, and associated complications, which informs treatment planning. The segment benefits from increasing availability of high-resolution MRI machines in hospitals and specialty centers. Rising awareness among clinicians about the importance of advanced imaging, combined with continuous technological advancements, has enhanced market adoption. MRI is also preferred for pediatric and adult patients due to safety and efficacy. Integration with treatment planning software and compatibility with minimally invasive surgical techniques supports adoption. Government and private hospital initiatives to upgrade diagnostic capabilities contribute to market dominance. Continuous research and training programs improve clinician expertise in MRI interpretation. Adoption of MRI in preoperative planning, follow-up monitoring, and postoperative evaluation further strengthens the segment’s position. Awareness campaigns highlighting early detection benefits also drive adoption.

The Head Ultrasound segment is anticipated to witness the fastest CAGR of 12.1% from 2025 to 2032, driven by its non-invasive nature, cost-effectiveness, and ease of use in neonates and infants. Head ultrasound is widely used in neonatal intensive care units (NICUs) for early detection of congenital hydrocephalus. Increasing adoption in developing regions, availability of portable ultrasound devices, and growing focus on early intervention contribute to market growth. Training programs for pediatricians and sonographers enhance utilization. Integration with telemedicine and remote monitoring further facilitates adoption. Awareness campaigns among caregivers about early diagnosis through ultrasound are accelerating growth. Government programs supporting neonatal health and pediatric care also reinforce adoption. The segment benefits from continuous technological innovation in imaging resolution, safety features, and user-friendly interfaces. Growing preference for bedside diagnostics in NICUs enhances convenience and compliance. Expansion of neonatal care facilities in emerging economies drives the fastest CAGR. Adoption in both hospital and clinic settings ensures broader accessibility.

- By Treatment Type

On the basis of treatment type, the Hydrocephalus Treatment market is segmented into Shunt Insertion, Ventriculostomy, and Medication. The Shunt Insertion segment dominated the largest market revenue share of 53.4% in 2024, as it remains the standard and most effective intervention for most types of hydrocephalus. The segment benefits from continuous innovation in shunt design, reduced complication rates, and minimally invasive procedures. Widespread availability in hospitals and surgical centers, as well as increasing pediatric and adult patient awareness, strengthens adoption. Training programs for neurosurgeons, improved postoperative care, and government healthcare initiatives further support the segment’s dominance. Shunt insertion provides long-term relief from intracranial pressure, preventing neurological deficits. Rising investments in surgical infrastructure and technology improve treatment outcomes. Insurance coverage and reimbursement policies enhance accessibility. The segment also benefits from ongoing R&D in smart shunt technologies that monitor intracranial pressure in real time. Hospital-based adoption and integration with diagnostic imaging ensure precise placement and effective management. Growing global prevalence of hydrocephalus reinforces the segment’s revenue share.

The Ventriculostomy segment is expected to witness the fastest CAGR of 11.8% from 2025 to 2032, fueled by increasing adoption of minimally invasive endoscopic third ventriculostomy procedures in both pediatric and adult patients. Ventriculostomy offers an alternative to shunt insertion, particularly in patients at risk of shunt-related complications. Rising clinician expertise, availability of advanced endoscopic instruments, and increasing hospital adoption drive growth. Integration with MRI and CT-based preoperative planning enhances accuracy and outcomes. Expanding awareness of less invasive surgical options, insurance coverage, and government support for surgical innovation further accelerate adoption. Training programs for neurosurgeons and research initiatives improve procedural success rates. Growing patient preference for procedures with fewer long-term complications supports market expansion. Telemedicine and remote monitoring of postoperative patients aid follow-up care. Rising geriatric population and increased incidence of acquired hydrocephalus contribute to segment growth. Government initiatives to improve surgical infrastructure in emerging regions further support the fastest CAGR.

- By End User

On the basis of end user, the Hydrocephalus Treatment market is segmented into Hospital, Clinics, Diagnostic Centres, Surgical Centers, Ambulatory Surgical Centers, and Others. The Hospital segment accounted for the largest market revenue share of 58.6% in 2024, due to comprehensive infrastructure, multidisciplinary teams, and advanced diagnostic and surgical facilities. Hospitals manage complex hydrocephalus cases requiring shunt insertion, ventriculostomy, and postoperative care. Rising hospital admissions, specialized neurosurgery departments, and access to advanced imaging contribute to dominance. Government initiatives, insurance coverage, and patient awareness programs support adoption. Hospitals provide integrated care, including rehabilitation and long-term monitoring. Access to experienced neurosurgeons, research collaborations, and training programs enhance treatment outcomes. Adoption of minimally invasive techniques, smart shunt technologies, and postoperative follow-up further strengthens hospital dominance. High patient trust and referral patterns reinforce segment revenue.

The Ambulatory Surgical Centers segment is expected to witness the fastest CAGR of 10.9% from 2025 to 2032, driven by increased preference for outpatient procedures, shorter hospital stays, and cost-effectiveness. These centers offer minimally invasive surgeries, rapid recovery, and lower treatment costs, making them attractive for patients and healthcare providers. Growth is fueled by expanding healthcare infrastructure, rising insurance coverage, and adoption of advanced surgical techniques. Patient convenience, availability of specialized neurosurgical teams, and growing awareness of ambulatory care benefits accelerate adoption. Partnerships with hospitals and clinics enhance access and credibility. Expansion in urban and semi-urban regions ensures broader market reach. Telemedicine for preoperative consultation and postoperative follow-up supports faster growth. Increasing preference for outpatient care in developed and emerging economies drives segment CAGR. Government initiatives to promote ambulatory care and cost-effective treatments reinforce adoption.

Hydrocephalus Treatment Market Regional Analysis

- North America dominated the hydrocephalus treatment market with the largest revenue share of 41.2% in 2024

- Supported by advanced healthcare infrastructure, high adoption of innovative neurosurgical procedures, and strong R&D activities in the U.S., driving wider treatment adoption

- The presence of leading hospitals and specialized neurosurgical centers, along with the availability of advanced programmable shunts and minimally invasive procedures, is contributing to the market growth in both adult and pediatric populations

U.S. Hydrocephalus Treatment Market Insight

The U.S. hydrocephalus treatment market captured the largest revenue share in 2024 within North America, fueled by the increasing availability of minimally invasive neurosurgical procedures, growing awareness of hydrocephalus management, and the rising adoption of advanced post-operative monitoring systems. Patients and healthcare providers are increasingly prioritizing treatments such as programmable shunts, endoscopic third ventriculostomy (ETV), and AI-assisted patient monitoring programs, which improve patient outcomes and reduce the risk of complications. The presence of highly skilled neurosurgeons and leading research institutions is also supporting innovation and wider adoption of effective hydrocephalus treatments.

Europe Hydrocephalus Treatment Market Insight

The Europe hydrocephalus treatment market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent healthcare regulations, increasing investments in specialized neurosurgical centers, and the growing emphasis on early diagnosis and intervention for hydrocephalus. Urbanization, rising patient awareness, and the expansion of advanced hospital infrastructure are fostering the adoption of innovative treatments across both pediatric and adult populations. Countries like Germany, France, and Italy are witnessing increased integration of programmable shunt systems and minimally invasive procedures in standard treatment protocols.

U.K. Hydrocephalus Treatment Market Insight

The U.K. hydrocephalus treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising geriatric population, growing awareness of neurological healthcare, and an increasing emphasis on minimally invasive surgical procedures. Concerns regarding long-term patient outcomes and complications from traditional shunt systems are motivating healthcare providers to adopt more advanced treatment options. The U.K.’s strong healthcare infrastructure, alongside patient education initiatives, is expected to continue stimulating market growth.

Germany Hydrocephalus Treatment Market Insight

The Germany hydrocephalus treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by robust healthcare infrastructure, advanced neurosurgical technologies, and a high level of patient awareness regarding treatment options. Hospitals and specialty centers are increasingly utilizing programmable shunts, endoscopic procedures, and advanced post-operative monitoring techniques to improve patient outcomes. The preference for precision surgical interventions and innovation-focused healthcare policies supports the adoption of these advanced therapies.

Asia-Pacific Hydrocephalus Treatment Market Insight

The Asia-Pacific hydrocephalus treatment market is poised to grow at the fastest CAGR during the forecast period of 2025 to 2032, driven by increasing urbanization, improving healthcare access, rising disposable incomes, and government initiatives promoting neurological healthcare in countries such as China, Japan, and India. Expansion of advanced neurosurgical centers, availability of minimally invasive procedures, and adoption of programmable shunt systems are increasing patient access to treatment. The focus on improving clinical outcomes and the rising number of trained neurosurgeons are key factors driving market growth.

Japan Hydrocephalus Treatment Market Insight

The Japan hydrocephalus treatment market is gaining momentum due to the country’s advanced healthcare system, rapid urbanization, and high patient awareness regarding neurological conditions. The adoption of minimally invasive neurosurgical procedures, programmable shunts, and enhanced post-operative monitoring systems is improving patient outcomes. Additionally, Japan’s aging population is expected to drive demand for convenient, safe, and effective hydrocephalus treatments across both hospital and specialty care settings.

China Hydrocephalus Treatment Market Insight

The China hydrocephalus treatment market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, a growing middle-class population, increased healthcare expenditure, and government focus on neurological health. Expansion of specialized neurosurgical centers, increasing patient awareness, and access to advanced shunt systems and minimally invasive procedures are supporting market growth. The push for improved clinical outcomes, alongside strong domestic healthcare manufacturers, is further driving the adoption of innovative hydrocephalus treatments in both pediatric and adult populations.

Hydrocephalus Treatment Market Share

The Hydrocephalus Treatment industry is primarily led by well-established companies, including:

- Medtronic (U.S.)

- Integra LifeSciences (U.S.)

- B. Braun SE (Germany)

- Sophysa SA (France)

- Spiegelberg GmbH & Co. KG (Germany)

- Natus Medical Incorporated (U.S.)

- CereVasc, Inc. (U.S.)

- Anuncia Medical (U.S.)

- Kaneka Medix Corporation (Japan)

- HPbio (South Korea)

- G. Surgiwear Ltd (India)

- Christoph Miethke GmbH & Co. KG (Germany)

- Dispomedica (U.S.)

- Delta Surgical (U.S.)

- Argi Group (Germany)

Latest Developments in Global Hydrocephalus Treatment Market

- In May 2021, Penn State researchers introduced the HydroFix shunt, an advanced surgical system designed to mitigate the risks associated with traditional shunts and provide a durable treatment solution for normal pressure hydrocephalus (NPH) patient

- In June 2025, Yale Medicine initiated a Phase III clinical trial for a minimally invasive treatment for NPH using the eShunt System, which allows cerebrospinal fluid to drain into the venous system through a needle puncture in the groin, eliminating the need for skull drilling

- In September 2025, the Placebo-Controlled Effectiveness in iNPH Shunting (PENS) Trial provided compelling evidence supporting the effectiveness of brain shunt implantation in elderly patients diagnosed with iNPH

- In September 2025, Michigan Governor Gretchen Whitmer proclaimed September as Hydrocephalus Awareness Month, highlighting the significance of brain shunt surgery as the primary treatment for hydrocephalus

- In June 2025, the Hydrocephalus Association reported that hydrocephalus research received USD 1.57 million in funding through the Peer Reviewed Medical Research Program (PRMRP) in 2024, supporting advancements in shunt technology and treatment strategies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.