Global Hydrogenated Styrenic Block Copolymers Hsbc Market

Market Size in USD Billion

USD

2.01 Billion

USD

3.02 Billion

2024

2032

USD

2.01 Billion

USD

3.02 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.01 Billion | |

| USD 3.02 Billion | |

| % | |

|

Hydrogenated Styrenic Block Copolymers (HSBC) Market Size

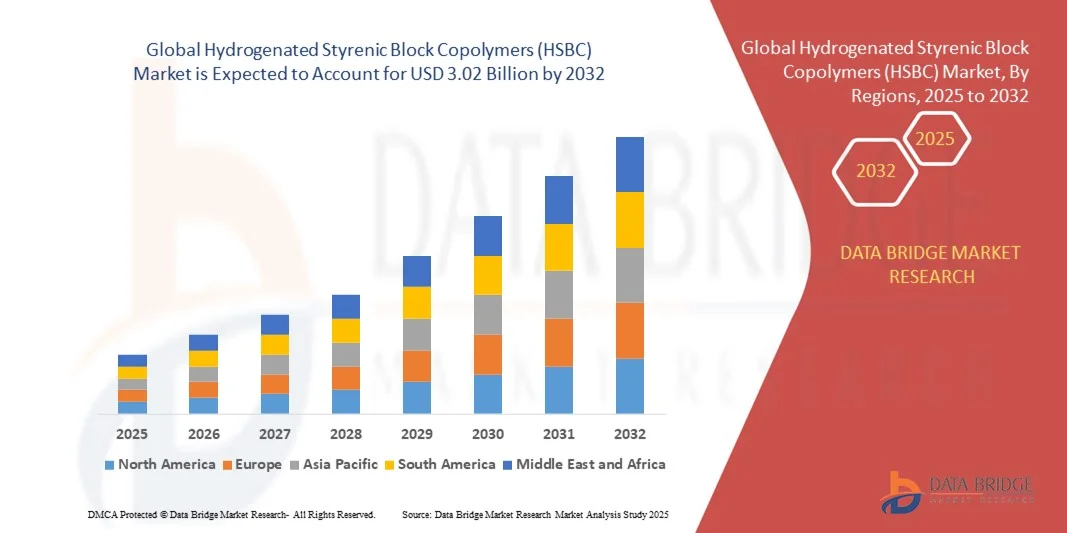

- The global hydrogenated styrenic block copolymers (HSBC) market size was valued at USD 2.01 billion in 2024 and is expected to reach USD 3.02 billion by 2032, at a CAGR of 5.20% during the forecast period

- The market growth is largely fuelled by increasing demand for high-performance thermoplastic elastomers in automotive, footwear, adhesives, and consumer goods applications, where durability, flexibility, and aesthetic appeal are critical

- Rising adoption of sustainable and recyclable polymer solutions in packaging and industrial applications is further driving the market, along with innovations in polymer processing techniques that enhance material performance and reduce production costs

Hydrogenated Styrenic Block Copolymers (HSBC) Market Analysis

- Growing use of HSBC in automotive applications, such as interior trim, seals, and gaskets, is driving demand due to its excellent mechanical properties, chemical resistance, and thermal stability

- The footwear and consumer goods sectors are increasingly integrating HSBC for its soft-touch, elastic, and durable properties, enhancing product performance and user comfort

- North America dominated the HSBC market with the largest revenue share of 38.5% in 2024, driven by strong demand from the automotive, footwear, and construction industries, coupled with rising adoption of lightweight and durable thermoplastic elastomers

- Asia-Pacific region is expected to witness the highest growth rate in the global hydrogenated styrenic block copolymers (HSBC) market, driven by rising demand for lightweight and durable materials in emerging economies, expanding infrastructure projects, and government initiatives promoting advanced manufacturing technologies

- The automotive segment held the largest market revenue share in 2024, driven by increasing use of HSBC in interior trims, sealants, and molded components for enhanced durability, thermal stability, and lightweight performance. HSBC’s superior elasticity and resistance to wear make it a preferred choice for automotive manufacturers seeking high-performance materials that improve vehicle longevity and reduce maintenance costs

Report Scope and Hydrogenated Styrenic Block Copolymers (HSBC) Market Segmentation

|

Attributes |

Hydrogenated Styrenic Block Copolymers (HSBC) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hydrogenated Styrenic Block Copolymers (HSBC) Market Trends

Increasing Adoption of High-Performance HSBC in Automotive, Footwear, and Industrial Applications

- The growing use of hydrogenated styrenic block copolymers (HSBC) is transforming multiple end-use industries by offering enhanced elasticity, durability, and thermal stability. Automotive components, footwear soles, and consumer goods are increasingly relying on HSBC for superior performance and longevity. Manufacturers are also leveraging HSBC to meet stricter quality standards and improve product lifecycle, creating new opportunities across premium segments

- Rising demand for lightweight, flexible, and sustainable thermoplastic elastomers is accelerating the adoption of HSBC in manufacturing processes. The material’s compatibility with recycling and its ability to reduce environmental impact are key factors driving industry uptake. Furthermore, HSBC is increasingly replacing traditional polymers in innovative applications such as wearable devices and flexible packaging, expanding its market footprint

- The versatility and ease of processing of modern HSBC materials make them attractive for adhesives, sealants, and coatings applications, where consistent performance and resilience are critical. Frequent use in these sectors enhances product quality while optimizing production efficiency. In addition, HSBC allows for precise customization of mechanical and chemical properties, making it suitable for specialized industrial requirements

- For instance, in 2023, several European automotive manufacturers integrated HSBC in interior trims and sealants, improving mechanical performance, reducing maintenance, and extending component lifespan. This integration also contributed to lighter vehicle designs, fuel efficiency improvements, and compliance with evolving safety and emission regulations

- While HSBC materials are supporting innovation in performance-oriented products, their market adoption depends on affordability, supply consistency, and continued R&D for high-performance formulations. Manufacturers must focus on scalable and cost-effective solutions to fully capitalize on the growing demand, while simultaneously expanding their global production networks to meet rising end-user requirements

Hydrogenated Styrenic Block Copolymers (HSBC) Market Dynamics

Driver

Rising Demand for Lightweight, Durable, and High-Performance Thermoplastic Elastomers

- Growing automotive production, urban infrastructure development, and the footwear industry are driving demand for lightweight and high-performance polymers such as HSBC. Their elasticity, chemical resistance, and thermal stability make them suitable for a variety of industrial and consumer applications. This trend is further fueled by increasing consumer preference for high-performance and durable goods

- Increasing focus on sustainable materials and recyclable polymers is encouraging manufacturers to adopt HSBC, which can be reused and repurposed, reducing environmental footprint while maintaining high material performance. The adoption of HSBC also aligns with corporate sustainability goals and eco-conscious branding strategies across industries

- The versatility of HSBC in adhesives, sealants, coatings, and molded components supports industrial efficiency, product durability, and enhanced functionality, promoting widespread adoption across end-use sectors. It also allows manufacturers to reduce waste, optimize production cycles, and enhance product consistency across multiple applications

- For instance, in 2022, several Asian industrial and automotive manufacturers shifted to HSBC-based components, achieving improved product resilience and operational efficiency. This transition also lowered long-term maintenance costs, minimized material failures, and enhanced competitiveness in global markets

- While performance benefits are driving market growth, widespread adoption depends on balancing cost, production scalability, and supply chain optimization for global distribution. Strategic partnerships, technology upgrades, and regional manufacturing expansion are essential to ensure stable supply and meet diverse end-user demands

Restraint/Challenge

High Production Costs and Limited Availability in Certain Regions

- The premium pricing of hydrogenated styrenic block copolymers compared to conventional polymers limits adoption among small and medium-sized enterprises, especially in developing regions. Cost remains a primary barrier to entry for many end-users, and price-sensitive industries often opt for alternative materials despite HSBC’s superior performance

- Limited availability of high-quality raw materials and complex hydrogenation processes can result in supply chain bottlenecks, impacting timely delivery for manufacturers. These constraints are further compounded by geopolitical factors, fluctuating raw material costs, and transportation delays, which can slow production and raise overall project expenses

- The requirement for advanced processing equipment and specialized knowledge in handling HSBC materials adds to operational complexity, particularly for new market entrants or regions lacking technical infrastructure. This complexity can increase training requirements, production downtime, and operational inefficiencies, making adoption challenging for smaller manufacturers

- For instance, in 2023, several South American and African industrial firms reported delayed integration of HSBC-based products due to raw material shortages and high production costs, slowing adoption in these regions. These delays also impacted product launches, supply commitments, and competitive positioning in regional markets

- While technological advancements are improving manufacturing efficiency and material quality, addressing cost and accessibility challenges is critical to expand global market penetration and long-term growth. Strategic investment in local production facilities, supply chain resilience, and material innovation will be essential to overcome these barriers

Hydrogenated Styrenic Block Copolymers (HSBC) Market Scope

The market is segmented on the basis of type, end user, application, and types.

- By End User

On the basis of end user, the hydrogenated styrenic block copolymers (HSBC) market is segmented into construction, automotive, footwear, chemicals, healthcare, and others. The automotive segment held the largest market revenue share in 2024, driven by increasing use of HSBC in interior trims, sealants, and molded components for enhanced durability, thermal stability, and lightweight performance. HSBC’s superior elasticity and resistance to wear make it a preferred choice for automotive manufacturers seeking high-performance materials that improve vehicle longevity and reduce maintenance costs.

The footwear segment is expected to witness the fastest growth rate from 2025 to 2032, propelled by rising demand for lightweight, flexible, and durable soles in sports, casual, and industrial footwear. HSBC’s compatibility with modern manufacturing techniques and its ability to provide comfort, cushioning, and abrasion resistance are key factors driving adoption. Moreover, growing consumer preference for eco-friendly and recyclable materials in footwear is accelerating the integration of HSBC into product lines.

- By Application

On the basis of application, the HSBC market is segmented into cable and wire, footwear, asphalt modifier, adhesives, and artificial leather. The adhesives segment accounted for a significant revenue share in 2024, owing to HSBC’s exceptional bonding properties, thermal stability, and elasticity. The use of HSBC in adhesives enhances product performance, reduces curing time, and ensures durability across diverse industrial applications.

The artificial leather segment is expected to grow at the fastest CAGR from 2025 to 2032, driven by the increasing demand for sustainable, high-performance alternatives to conventional leather. HSBC provides superior flexibility, tensile strength, and processability, making it suitable for fashion, automotive, and furniture applications. In addition, growing adoption in synthetic textiles and flexible consumer goods is boosting market expansion.

- By Types

On the basis of types, the HSBC market is segmented into Styrene Ethylene Propylene Styrene (SEPS) and Styrene Ethylene Butylene Styrene (SEBS). The SEBS segment held the largest market revenue share in 2024 due to its enhanced thermal stability, mechanical properties, and compatibility with a wide range of applications including automotive, footwear, and adhesives. SEBS is increasingly preferred for high-performance, durable, and recyclable products, which are critical for industrial and consumer applications.

The SEPS segment is expected to witness the fastest growth rate from 2025 to 2032, driven by its excellent elasticity, transparency, and cost-effectiveness. SEPS is widely used in molded components, flexible packaging, and specialty industrial applications. Its versatility and ease of processing are attracting manufacturers across multiple end-use sectors, supporting rapid market adoption globally.

Hydrogenated Styrenic Block Copolymers (HSBC) Market Regional Analysis

- North America dominated the HSBC market with the largest revenue share of 38.5% in 2024, driven by strong demand from the automotive, footwear, and construction industries, coupled with rising adoption of lightweight and durable thermoplastic elastomers

- Manufacturers in the region highly value the performance benefits of HSBC, including elasticity, thermal stability, and chemical resistance, which enhance product quality and durability in end-use applications

- This widespread adoption is further supported by advanced manufacturing infrastructure, technological expertise, and increasing investment in R&D for high-performance polymers, establishing HSBC as a preferred material across industrial and consumer applications

U.S. HSBC Market Insight

The U.S. HSBC market captured the largest revenue share in North America in 2024, fueled by rapid growth in automotive production, footwear manufacturing, and industrial components. Rising focus on sustainable and recyclable materials is encouraging manufacturers to incorporate HSBC into high-performance products. The versatility of HSBC in adhesives, coatings, and molded components is driving adoption, while increasing investment in lightweight and durable materials enhances operational efficiency and product longevity across industries.

Europe HSBC Market Insight

The Europe HSBC market is expected to witness the fastest growth rate from 2025 to 2032, primarily driven by stringent environmental regulations, sustainability initiatives, and rising demand for high-performance polymers in automotive and construction sectors. European manufacturers are increasingly integrating HSBC into industrial applications, footwear soles, and adhesive solutions to improve durability and reduce environmental impact. The adoption is further supported by advanced polymer processing facilities and increasing R&D activities for innovative material formulations.

U.K. HSBC Market Insight

The U.K. HSBC market is expected to witness the fastest growth rate from 2025 to 2032, driven by demand for lightweight and durable thermoplastic elastomers in automotive, construction, and industrial applications. Rising awareness of sustainability and recyclable materials is encouraging the use of HSBC in manufacturing processes. The integration of HSBC in adhesives, coatings, and molded components is also gaining traction due to improved performance and cost-effectiveness, boosting overall market growth.

Germany HSBC Market Insight

The Germany HSBC market is expected to witness the fastest growth rate from 2025 to 2032, fueled by increasing industrial automation, high-quality manufacturing standards, and adoption of eco-friendly polymers. German manufacturers are leveraging HSBC for automotive parts, industrial components, and footwear soles, benefiting from enhanced thermal stability, elasticity, and chemical resistance. The focus on sustainability and innovative material solutions further supports the widespread use of HSBC across multiple industrial sectors.

Asia-Pacific HSBC Market Insight

The Asia-Pacific HSBC market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid industrialization, urbanization, and rising demand for lightweight and durable thermoplastic elastomers in countries such as China, Japan, and India. The region's expanding automotive, footwear, and construction industries are increasingly adopting HSBC for high-performance applications. In addition, APAC’s emergence as a manufacturing hub for polymers is enhancing affordability and accessibility, fueling widespread adoption across industrial and consumer sectors.

Japan HSBC Market Insight

The Japan HSBC market is expected to witness the fastest growth rate from 2025 to 2032 due to the country’s high-tech manufacturing culture, emphasis on sustainability, and demand for durable, high-performance materials. Adoption of HSBC in automotive components, industrial parts, and adhesives is increasing, supported by integration with advanced polymer processing technologies. Japan’s focus on innovative material solutions and lightweight components is further driving market growth across both industrial and consumer applications.

China HSBC Market Insight

The China HSBC market accounted for the largest revenue share in Asia-Pacific in 2024, attributed to rapid urbanization, industrial growth, and increasing demand for high-performance thermoplastic elastomers. The automotive, footwear, and construction industries are major contributors, integrating HSBC into products to enhance elasticity, durability, and thermal stability. Government initiatives promoting sustainable materials, coupled with strong domestic manufacturing capabilities, are key factors propelling the market in China.

Hydrogenated Styrenic Block Copolymers (HSBC) Market Share

The Hydrogenated Styrenic Block Copolymers (HSBC) industry is primarily led by well-established companies, including:

- HEXPOL AB. (Sweden)

- KRATON CORPORATION. (U.S.)

- China Petrochemical Corporation (China)

- Grupo Dynasol (Spain)

- Teknor Apex (U.S.)

- Eastman Chemical Company (U.S.)

- Marubeni Europe plc (U.K.)

- LCY GROUP. (Taiwan)

- Kuraray America, Inc. (U.S.)

- TSRC (Taiwan)

- LG Chem. (South Korea)

- BASF SE (Germany)

- INEOS Styrolution Group GmbH (Germany)

- Eni S.p.A. (Italy)

- JSR Corporation. (Japan)

- KUMHO PETROCHEMICAL. (South Korea)

- RTP Company. (U.S.)

- Asahi Kasei Corporation. (Japan)

- Exxon Mobil Corporation. (U.S.)

- BP (U.K.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET SIZE

2.3 VENDOR POSITIONING GRID

2.4 MARKETS COVERED

2.5 GEOGRAPHIC SCOPE

2.6 YEARS CONSIDERED FOR THE STUDY

2.7 RESEARCH METHODOLOGY

2.8 TECHNOLOGY LIFE LINE CURVE

2.9 MULTIVARIATE MODELLING

2.1 PRIMARY INTERVIEWS WITH KEY OPINION LEADERS

2.11 DBMR MARKET POSITION GRID

2.12 MARKET APPLICATION COVERAGE GRID

2.13 DBMR MARKET CHALLENGE MATRIX

2.14 IMPORT AND EXPORT DATA

2.15 SECONDARY SOURCES

2.16 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET: RESEARCH SNAPSHOT

2.17 ASSUMPTIONS

3 MARKET OVERVIEW

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHTS

5.1 PRODUCTION CONSUMPTION ANALYSIS

5.2 IMPORT EXPORT SCENARIO

5.3 PRICE TREND ANALYSIS

5.4 RAW MATERIAL PRODUCTION COVERAGE

5.5 TECHNOLOGICAL ADVANCEMENT BY MANUFACTURERS

5.6 PORTER’S FIVE FORCES

5.7 PESTEL ANALYSIS

5.8 REGULATION COVERAGE

6 SUPPLY CHAIN ANALYSIS

6.1 OVERVIEW

6.2 LOGISTIC COST SCENARIO

6.3 IMPORTANCE OF LOGISTICS SERVICE PROVIDERS

7 CLIMATE CHANGE SCENARIO

7.1 ENVIRONMENTAL CONCERNS

7.2 INDUSTRY RESPONSE

7.3 GOVERNMENT’S ROLE

7.4 ANALYST RECOMMENDATIONS

8 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET, BY TYPE, 2022-2031, (USD MILLION)

8.1 OVERVIEW

8.2 STYRENE ETHYLENE PROPYLENE STYRENE (SEPS)

8.3 STYRENE ETHYLENE BUTYLENE STYRENE (SEBS)

9 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET, BY APPLICATION, 2022-2031, (USD MILLION)

9.1 OVERVIEW

9.2 CABLE & WIRE

9.3 FOOTWEAR

9.4 ASPHALT MODIFIER

9.5 ADHESIVES

9.6 ARTIFICIAL LEATHER

9.7 TPE COMPOUNDING & MOLDING

9.8 AUTOMOTIVE

9.9 ELECTRONICS

9.1 OTHERS

10 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET, BY END USER, 2022-2031, (USD MILLION)

10.1 OVERVIEW

10.2 MANUFACTURING

10.3 CONSTRUCTION

10.4 AUTOMOTIVE & TRANSPORTATION

10.5 HEALTHCARE

10.6 CONSUMER GOODS

10.7 PACKAGING

10.8 OTHERS

11 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET, BY GEOGRAPHY , 2024-2031, (USD MILLION)

LOBAL HYDROGEN GENERATION MARKET, (ALL SEGMENTATION PROVIDED ABOVE IS REPRESENTED IN THIS CHAPTER BY COUNTRY)

11.1 NORTH AMERICA

11.1.1 U.S.

11.1.2 CANADA

11.1.3 MEXICO

11.2 EUROPE

11.2.1 GERMANY

11.2.2 U.K.

11.2.3 ITALY

11.2.4 FRANCE

11.2.5 SPAIN

11.2.6 RUSSIA

11.2.7 SWITZERLAND

11.2.8 TURKEY

11.2.9 BELGIUM

11.2.10 NETHERLANDS

11.2.11 LUXEMBURG

11.2.12 REST OF EUROPE

11.3 ASIA-PACIFIC

11.3.1 JAPAN

11.3.2 CHINA

11.3.3 SOUTH KOREA

11.3.4 INDIA

11.3.5 SINGAPORE

11.3.6 THAILAND

11.3.7 INDONESIA

11.3.8 MALAYSIA

11.3.9 PHILIPPINES

11.3.10 AUSTRALIA & NEW ZEALAND

11.3.11 REST OF ASIA-PACIFIC

11.4 SOUTH AMERICA

11.4.1 BRAZIL

11.4.2 ARGENTINA

11.4.3 REST OF SOUTH AMERICA

11.5 MIDDLE EAST AND AFRICA

11.5.1 SOUTH AFRICA

11.5.2 EGYPT

11.5.3 SAUDI ARABIA

11.5.4 UNITED ARAB EMIRATES

11.5.5 ISRAEL

11.5.6 REST OF MIDDLE EAST AND AFRICA

12 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET, COMPANY LANDSCAPE

12.1 COMPANY SHARE ANALYSIS: GLOBAL

12.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

12.3 COMPANY SHARE ANALYSIS: EUROPE

12.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

12.5 MERGERS AND ACQUISITIONS

12.6 NEW PRODUCT DEVELOPMENT AND APPROVALS

12.7 EXPANSIONS

12.8 PARTNERSHIP AND OTHER STRATEGIC DEVELOPMENTS

13 SWOT AND DATA BRIDGE MARKET RESEARCH ANALYSIS

14 GLOBAL HYDROGENATED STYRENIC BLOCK COPOLYMERS (HSBC) MARKET- COMPANY PROFILE

14.1 KRATON FORMOSA POLYMERS CORPORATION

14.1.1 COMPANY SNAPSHOT

14.1.2 REVENUE ANALYSIS

14.1.3 PRODUCT PORTFOLIO

14.1.4 RECENT UPDATES

14.2 LCY

14.2.1 COMPANY SNAPSHOT

14.2.2 REVENUE ANALYSIS

14.2.3 PRODUCT PORTFOLIO

14.2.4 RECENT UPDATES

14.3 TEKNOR APEX

14.3.1 COMPANY SNAPSHOT

14.3.2 REVENUE ANALYSIS

14.3.3 PRODUCT PORTFOLIO

14.3.4 RECENT UPDATES

14.4 MARUBENI EUROPE PLC

14.4.1 COMPANY SNAPSHOT

14.4.2 REVENUE ANALYSIS

14.4.3 PRODUCT PORTFOLIO

14.4.4 RECENT UPDATES

14.5 KURARAY AMERICA, INC

14.5.1 COMPANY SNAPSHOT

14.5.2 REVENUE ANALYSIS

14.5.3 PRODUCT PORTFOLIO

14.5.4 RECENT UPDATES

14.6 ASAHI KASEI

14.6.1 COMPANY SNAPSHOT

14.6.2 REVENUE ANALYSIS

14.6.3 PRODUCT PORTFOLIO

14.6.4 RECENT UPDATES

NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

15 RELATED REPORTS

16 QUESTIONNAIRE

17 CONCLUSION

18 ABOUT DATA BRIDGE MARKET RESEARCH

Global Hydrogenated Styrenic Block Copolymers Hsbc Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Hydrogenated Styrenic Block Copolymers Hsbc Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Hydrogenated Styrenic Block Copolymers Hsbc Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.