Global Hypercoagulable Treatment Market

Market Size in USD Billion

USD

767.10 Billion

USD

1,048.21 Billion

2024

2032

USD

767.10 Billion

USD

1,048.21 Billion

2024

2032

| 2025 - 2032 | |

| USD 767.10 Billion | |

| USD 1,048.21 Billion | |

| % | |

|

Hypercoagulable Treatment Market Size

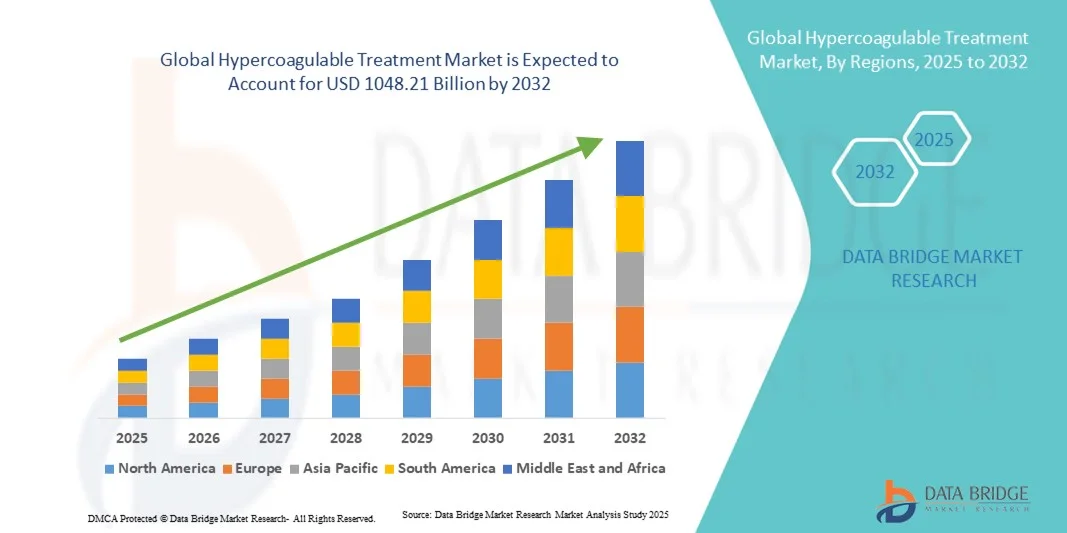

- The global hypercoagulable treatment market size was valued at USD 767.10 billion in 2024 and is expected to reach USD 1048.21 billion by 2032, at a CAGR of 3.98% during the forecast period

- The market growth is largely fueled by the increasing prevalence of hypercoagulable disorders, advancements in diagnostic technologies, and the development of innovative anticoagulant and targeted therapies, which are improving patient outcomes and reducing the risk of thrombotic events

- Furthermore, rising awareness among healthcare providers and patients, along with the growing availability of personalized and minimally invasive treatment options, is establishing Hypercoagulable Treatment as a key focus area in hematology and cardiovascular care. These converging factors are accelerating the adoption of Hypercoagulable Treatment solutions, thereby significantly boosting the industry's growth

Hypercoagulable Treatment Market Analysis

- Hypercoagulable Treatment, including anticoagulants, antiplatelet therapies, and novel targeted therapeutics, has become an essential component of modern hematology and cardiovascular care due to its effectiveness in preventing thrombotic events and improving patient outcomes

- The growing demand for Hypercoagulable Treatment is primarily fueled by the increasing prevalence of hypercoagulable disorders, advancements in diagnostic and therapeutic technologies, and rising awareness among healthcare professionals and patients about early intervention

- North America dominated the hypercoagulable treatment market with the largest revenue share of 42.3% in 2024, supported by advanced healthcare infrastructure, high adoption of innovative therapies, and strong research and development activities in the U.S., driving wider treatment adoption

- Asia-Pacific is expected to be the fastest-growing region in the hypercoagulable treatment market during the forecast period due to increasing prevalence of thrombotic disorders, improving healthcare access, and rising disposable incomes in countries such as China and India

- The Oral segment dominated the market with 52% revenue share in 2024, driven by convenience, ease of long-term therapy, and better patient compliance

Report Scope and Hypercoagulable Treatment Market Segmentation

|

Attributes |

Hypercoagulable Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Hypercoagulable Treatment Market Trends

Advancements in Innovative Therapies and Digital Health Integration

- A significant and accelerating trend in the global hypercoagulable treatment market is the increasing adoption of advanced diagnostics, AI-assisted risk assessment tools, and personalized treatment protocols. These innovations are significantly enhancing patient management, early intervention, and overall treatment outcomes

- For instance, in March 2023, Siemens Healthineers launched an AI-powered coagulation monitoring system that enables clinicians to assess patient thrombotic risks more accurately and adjust anticoagulant therapy in real time. Similarly, Roche Diagnostics introduced a next-generation laboratory assay capable of rapidly detecting hypercoagulable conditions, supporting early diagnosis and timely intervention

- Integration of digital health platforms and remote monitoring systems is also improving patient outcomes. For instance, some wearable devices now allow continuous monitoring of coagulation parameters, alerting healthcare providers if abnormalities are detected and enabling proactive management

- These advancements facilitate centralized patient management, allowing clinicians to track therapy effectiveness, manage dosage adjustments, and predict risk factors through a single platform. This unified approach supports better coordination of care, reduces complications, and improves adherence to prescribed treatment regimens

- The trend towards more personalized, proactive, and data-driven hypercoagulable treatment strategies is fundamentally reshaping patient expectations for care. Consequently, companies such as Baxter International and Grifols are developing advanced anticoagulant therapies and monitoring solutions to optimize treatment plans and enhance patient safety

- The demand for hypercoagulable treatment solutions that combine innovative diagnostics, personalized therapy, and digital monitoring is growing rapidly across both hospital and outpatient settings, as patients and healthcare providers increasingly prioritize precision care and improved outcomes

Hypercoagulable Treatment Market Dynamics

Driver

Rising Prevalence of Thrombotic Disorders and Growing Awareness

- The increasing prevalence of hypercoagulable conditions, such as deep vein thrombosis (DVT), pulmonary embolism (PE), and hereditary thrombophilia, is a key driver of market growth

- For instance, in April 2024, Bayer Healthcare expanded its anticoagulant therapy portfolio with a focus on high-risk patient groups, aiming to provide safer and more effective treatment options. Such initiatives by leading companies are expected to drive hypercoagulable treatment adoption during the forecast period

- Increasing awareness among healthcare professionals and patients regarding the risks of untreated hypercoagulable conditions is boosting the demand for early diagnosis and intervention. For instance, educational campaigns by the American Heart Association in 2023 emphasized the importance of coagulation screening in high-risk populations

- Furthermore, the rising adoption of personalized medicine approaches is driving demand, as clinicians are increasingly tailoring anticoagulant therapy based on genetic, lifestyle, and comorbidity factors

- Expansion of healthcare infrastructure, especially in emerging economies, is facilitating broader access to diagnostic and therapeutic solutions for hypercoagulable disorders. For instance, in July 2023, Siemens Healthineers partnered with hospitals in India to deploy advanced coagulation testing platforms in regional healthcare centers

- Increasing investment in R&D for novel anticoagulant drugs, biologics, and combination therapies is also supporting market growth. In September 2024, Pfizer announced a clinical trial for a next-generation oral anticoagulant targeting rare hereditary clotting disorders

Restraint/Challenge

High Treatment Costs and Limited Access to Advanced Therapies

- The high cost of advanced diagnostic tools and anticoagulant therapies remains a significant barrier to widespread adoption, particularly in low- and middle-income countries

- For instance, a 2024 study highlighted that the cost of genetic screening for thrombophilia can exceed several hundred dollars per patient, limiting accessibility

- Limited availability of specialized hematologists and advanced coagulation testing facilities restricts patient access, particularly in rural and underserved regions

- Regulatory challenges and approval delays for novel therapies can slow market expansion. For instance, in June 2025, Grifols reported extended regulatory review periods for a new anticoagulant therapy in certain European countries

- Potential side effects and complications associated with anticoagulant therapy, such as bleeding risks, may hinder adoption among clinicians and patients

- Variability in reimbursement policies across regions further limits access to advanced hypercoagulable treatments, particularly for high-cost biologic therapies

- Overcoming these challenges through cost-effective diagnostic platforms, broader healthcare access, training of healthcare professionals, and patient education will be crucial for sustained market growth in the hypercoagulable treatment segment

Hypercoagulable Treatment Market Scope

The market is segmented on the basis of type, drugs, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the Hypercoagulable Treatment market is segmented into Factor V Leiden, Prothrombin 20210, Antiphospholipid Syndrome, and Others. The Factor V Leiden segment dominated the largest market revenue share of 41.8% in 2024, driven by its high prevalence among patients with inherited thrombophilia. The widespread use of genetic testing and routine screening in high-risk populations enhances early diagnosis and intervention. Factor V Leiden patients benefit from targeted anticoagulant therapies that help prevent recurrent thromboembolic events. Strong awareness campaigns among healthcare professionals and patients support adoption. Reimbursement policies in developed regions, combined with inclusion in clinical guidelines, further strengthen market penetration. Advances in precision medicine, risk stratification, and patient monitoring have improved therapeutic outcomes. Clinical research on novel anticoagulants continues to provide growth opportunities. Healthcare institutions increasingly adopt standardized treatment protocols. The segment also benefits from increasing patient education programs, improved laboratory diagnostics, and growing prevalence of lifestyle-related risk factors. Hospitals and specialty centers contribute significantly to revenue.

The Antiphospholipid Syndrome segment is expected to witness the fastest CAGR of 11.2% from 2025 to 2032, driven by increasing diagnosis among women of childbearing age and rising awareness of associated pregnancy complications. The growing prevalence of autoimmune disorders globally is expanding the patient pool. Early intervention strategies and improved anticoagulant therapies enhance outcomes and reduce thrombotic risks. Specialized treatment centers and multidisciplinary care programs are supporting adoption. Government awareness initiatives further encourage timely diagnosis and treatment. Availability of targeted therapies for APS improves patient compliance. Expansion of homecare services and telemedicine solutions contributes to market growth. Ongoing clinical trials and research into novel therapeutics create additional momentum. The segment benefits from educational programs aimed at both clinicians and patients. Rising patient advocacy and support groups are also promoting awareness. Integration of diagnostic testing with personalized treatment plans strengthens uptake.

- By Drugs

On the basis of drugs, the Hypercoagulable Treatment market is segmented into Heparin, Warfarin, Vitamin K Antagonist, Direct Thrombin Inhibitors, and Others. The Warfarin segment held the largest market revenue share of 43.5% in 2024, due to its long-standing clinical use and established efficacy in preventing thromboembolic events. Its cost-effectiveness, accessibility, and inclusion in standard treatment protocols enhance adoption. Clinician familiarity with Warfarin ensures high prescription rates. Hospitals and specialty centers widely rely on Warfarin for chronic anticoagulation therapy. Routine monitoring using INR tests supports safe and effective usage. Availability across hospital pharmacies, retail pharmacies, and healthcare networks contributes to steady revenue generation. Reimbursement and insurance coverage for Warfarin further facilitate patient access. Patient education programs improve adherence to long-term therapy. Warfarin’s inclusion in treatment guidelines by leading medical associations reinforces its market dominance.

The Direct Thrombin Inhibitors segment is expected to witness the fastest CAGR of 10.8% from 2025 to 2032, driven by higher adoption among patients intolerant to traditional anticoagulants and those seeking therapies with fewer monitoring requirements. The segment benefits from improved safety profiles, lower bleeding risk, and ease of administration. Outpatient convenience and growing awareness of novel therapies enhance adoption. Inclusion in clinical guidelines for targeted therapy contributes to growth. Hospitals and homecare services are increasingly providing Direct Thrombin Inhibitors for patient management. Rising patient preference for modern anticoagulants supports expansion. Research and development of next-generation inhibitors creates additional opportunities. Availability through multiple distribution channels such as hospital and online pharmacies further accelerates uptake. Clinical trials demonstrate therapeutic effectiveness, boosting physician confidence. Patient adherence improves with simplified dosing regimens. Telemedicine and digital health integration facilitate monitoring and remote consultation.

- By Route of Administration

On the basis of route of administration, the market is segmented into Oral and Injectable. The Oral segment dominated the market with 52% revenue share in 2024, driven by convenience, ease of long-term therapy, and better patient compliance. Oral administration reduces hospital visits and monitoring requirements. It supports outpatient management and homecare settings. Widespread clinician familiarity enhances prescription rates. Oral anticoagulants are preferred for chronic conditions and preventive therapy. Reimbursement and insurance coverage improve patient access. Hospitals, specialty centers, and homecare services contribute significantly to revenue. Patient adherence programs reinforce sustained usage. Availability across retail and online pharmacies ensures accessibility. Global awareness campaigns encourage adoption. Simplified dosing and minimal monitoring requirements increase acceptance. Integration with telehealth platforms supports adherence monitoring.

The Injectable segment is expected to witness the fastest CAGR of 10.5% from 2025 to 2032, driven by acute care requirements, hospital-based administration, and perioperative or high-risk use. Prefilled syringes and improved formulations enhance safety and ease of use. Injectable therapies are critical in emergency and inpatient settings. High efficacy in rapid anticoagulation drives adoption. Hospitals, surgical centers, and specialty clinics are key end-users. Telemedicine guidance for home injection contributes to patient confidence. Regulatory approvals and reimbursement support growth. Acute thrombosis management and bridging therapy increase demand. Training programs for caregivers and clinicians improve adherence. Growing awareness of injectable alternatives fosters rapid uptake. Integration with hospital protocols ensures streamlined treatment.

- By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Centres, and Others. The Hospitals segment accounted for the largest market revenue share of 45% in 2024, owing to specialized care availability, laboratory monitoring, and high patient inflow requiring immediate anticoagulation therapy. Hospitals provide comprehensive treatment, access to multidisciplinary teams, and standardized protocols. Integration of diagnostics, drug administration, and monitoring supports effective outcomes. Insurance coverage and reimbursement policies enhance patient accessibility. Hospitals also drive clinical research and adoption of newer therapies. Availability of both oral and injectable options ensures flexibility. Educational initiatives improve adherence and safety. Collaboration with homecare services strengthens continuity of care. Hospitals maintain inventory and supply chain reliability. Expansion of tertiary and specialty care centers boosts market dominance.

The Homecare segment is projected to witness the fastest CAGR of 11% from 2025 to 2032, driven by patient preference for self-administration, telemedicine support, and convenience of oral therapies. Homecare adoption is facilitated by portable anticoagulant devices and easy-to-use delivery systems. Rising awareness of chronic disease management promotes uptake. Integration with digital health platforms enhances adherence monitoring. Patient and caregiver training programs increase confidence and safety. Insurance coverage for homecare services supports market expansion. Remote consultation and monitoring reduce hospital visits. Telehealth and digital reminders improve compliance. Growth in the geriatric population further drives demand. Accessibility of oral and injectable formulations boosts adoption. Government and NGO awareness programs encourage homecare solutions.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Online Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated with 48% revenue share in 2024, benefiting from direct supply chains, institutional procurement, and integration with patient care protocols. Hospitals ensure continuous availability, quality control, and adherence to treatment protocols. Centralized purchasing supports cost efficiency. Professional guidance and monitoring during therapy reinforce safety. Hospitals also play a key role in training healthcare staff and patients on proper medication administration, further enhancing treatment effectiveness and patient outcomes

The Online Pharmacy segment is expected to witness the fastest CAGR of 12% from 2025 to 2032, fueled by e-commerce adoption, home delivery convenience, digital prescription services, and growing telehealth integration. Online pharmacies provide access to both oral and injectable therapies, expanding patient reach. Convenience, privacy, and ease of access drive adoption. Telemedicine consultations support safe self-administration. Promotional campaigns and awareness programs further accelerate uptake. Integration with digital health platforms ensures adherence tracking. Rising internet penetration and smartphone use support expansion. Online pharmacy platforms offer subscription-based delivery and reminders. Home delivery reduces logistical barriers and enhances continuity of care. Insurance coverage and reimbursement for online purchases further boost growth.

Hypercoagulable Treatment Market Regional Analysis

- North America dominated the hypercoagulable treatment market with the largest revenue share of 42.3% in 2024, supported by advanced healthcare infrastructure, high adoption of innovative therapies, and strong research and development activities in the U.S., driving wider treatment adoption

- The region benefits from well-established hospitals, specialized treatment centers, and comprehensive patient awareness programs that encourage early diagnosis and adherence to therapeutic regimens. High healthcare expenditure, favorable reimbursement policies, and a focus on precision medicine are further contributing to market growth

- Increasing clinical trials and collaborations among healthcare institutions and pharmaceutical companies are enabling faster access to novel therapies. Enhanced availability of advanced diagnostic tools also supports timely and accurate detection of thrombotic disorders

U.S. Hypercoagulable Treatment Market Insight

The U.S. hypercoagulable treatment market captured the largest revenue share in North America in 2024, driven by the growing prevalence of coagulation disorders and increasing adoption of advanced anticoagulant therapies. Strong healthcare infrastructure, high patient awareness, and rising preference for early diagnosis and specialized care further bolster market expansion. The country is witnessing a surge in clinical trials and research initiatives focused on developing next-generation therapies. Additionally, government initiatives and health programs targeting cardiovascular and thrombotic conditions are facilitating wider treatment penetration. The adoption of hospital-based and outpatient care models ensures effective management of hypercoagulable conditions, improving patient outcomes and driving sustained market growth.

Europe Hypercoagulable Treatment Market Insight

The Europe hypercoagulable treatment market is projected to expand at a substantial CAGR during the forecast period, supported by increasing awareness about thrombotic disorders, growing geriatric population, and government-led health initiatives. Rising demand for advanced therapies and structured treatment protocols in hospitals and specialty clinics is further propelling growth. Regulatory frameworks encouraging the use of innovative anticoagulants and supportive therapies are also contributing. Countries such as Germany, France, and Italy are witnessing improved diagnosis rates due to enhanced healthcare access and patient education programs. Investment in research and development for novel treatment options is additionally fostering market growth across Europe, particularly in urban healthcare centers and specialty clinics.

U.K. Hypercoagulable Treatment Market Insight

The U.K. hypercoagulable treatment market is expected to grow at a noteworthy CAGR during the forecast period, driven by increasing prevalence of coagulation disorders and strong healthcare infrastructure. The NHS and private healthcare sectors are actively promoting early diagnosis and effective management through anticoagulant therapies. Clinical guidelines recommending structured treatment regimens for high-risk patients further encourage adoption. Rising patient awareness about thrombotic risks, coupled with ongoing research programs and availability of innovative therapies, supports growth. Additionally, the presence of specialized hematology centers and collaboration between hospitals and research institutes enhances treatment accessibility and quality, contributing to steady market expansion in the U.K.

Germany Hypercoagulable Treatment Market Insight

The Germany hypercoagulable treatment market is anticipated to expand at a considerable CAGR during the forecast period, driven by increasing awareness about coagulation disorders and rising demand for innovative therapies. Germany’s well-developed healthcare infrastructure and strong emphasis on research and development support the adoption of advanced treatment options. Hospitals and specialty centers are equipped with state-of-the-art diagnostic tools, enabling accurate detection and timely intervention. Patient education programs and preventive care initiatives are further fostering market growth. Additionally, insurance coverage and favorable reimbursement policies for anticoagulant therapies encourage broader adoption among high-risk populations, reinforcing sustained market expansion.

Asia-Pacific Hypercoagulable Treatment Market Insight

The Asia-Pacific hypercoagulable treatment market is expected to witness the fastest CAGR during the forecast period, estimated at, driven by increasing prevalence of thrombotic disorders, improving healthcare infrastructure, and rising disposable incomes in countries such as China, India, and Japan. The region is experiencing enhanced access to hospitals, specialty clinics, and diagnostic centers, facilitating timely detection and treatment. Growing government initiatives to improve healthcare coverage, coupled with increased patient awareness programs, are contributing to higher adoption of advanced therapies. Investments by pharmaceutical companies in the region are also accelerating the availability of innovative treatment options. Rapid urbanization and expanding middle-class populations are further driving the demand for accessible and effective hypercoagulable treatments.

Japan Hypercoagulable Treatment Market Insight

The Japan hypercoagulable treatment market is gaining momentum due to rising prevalence of coagulation disorders, an aging population, and strong healthcare infrastructure. Advanced hospitals and specialty centers equipped with sophisticated diagnostic and treatment technologies are facilitating early detection and effective therapy management. High patient awareness and government initiatives promoting preventive care and adherence to treatment guidelines are further boosting market growth. Additionally, Japan’s focus on research and development in hematology and anticoagulant therapies is supporting the introduction of innovative treatments, thereby enhancing patient outcomes and expanding the market steadily.

China Hypercoagulable Treatment Market Insight

The China hypercoagulable treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to increasing prevalence of thrombotic disorders, rapid urbanization, rising disposable income, and expanding healthcare infrastructure. Improved access to hospitals, specialty clinics, and diagnostic centers has enhanced early diagnosis and adoption of effective treatments. Government initiatives promoting healthcare modernization and the availability of advanced anticoagulant therapies further support market growth. Increasing awareness among patients and healthcare providers, coupled with investment in research and development of innovative therapies, is driving market expansion. China’s growing middle class and focus on quality healthcare delivery continue to propel the adoption of hypercoagulable treatments across the country.

Hypercoagulable Treatment Market Share

The Hypercoagulable Treatment industry is primarily led by well-established companies, including:

- Sanofi (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Novartis AG (Switzerland)

- F. Hoffmann-La Roche Ltd. (Switzerland)

- Pfizer Inc. (U.S.)

- Hikma Pharmaceuticals PLC (U.K.)

- Fresenius Kabi AG (Germany)

- Eisai Co., Ltd. (Japan)

- Bristol-Myers Squibb Company (U.S.)

- Johnson & Johnson and its afiliates (U.S.)

- Bayer AG (Germany)

- AbbVie Inc. (U.S.)

- Amgen Inc. (U.S.)

- Lilly (U.S.)

Latest Developments in Global Hypercoagulable Treatment Market

- In April 2024, the FDA approved Beqvez (fidanacogene elaparvovec) for the treatment of adults with moderate to severe hemophilia B. This gene therapy provides a long-term solution by addressing the underlying genetic cause of the disorder, representing a significant milestone in hemophilia treatment

- In August 2025, the European Society of Cardiology reported that extended treatment with apixaban 2.5 mg twice daily significantly reduced the recurrence of symptomatic venous thromboembolism (VTE) in patients with provoked events. This finding underscores the importance of extended anticoagulation therapy in preventing VTE recurrence

- In September 2025, the National Bleeding Disorders Foundation highlighted new developments in bleeding disorder care, including the introduction of extended half-life therapies and rebalancing agents. These innovations aim to improve treatment efficacy and patient quality of life

- In March 2025, Sanofi announced the approval of Qfitlia (fitusiran) by the U.S. Food and Drug Administration (FDA) as the first therapy in the U.S. to treat hemophilia A or B, with or without inhibitors. This approval marks a significant advancement in the treatment of bleeding disorders, offering a novel approach to managing these conditions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.