Global Hyperoxaluria Drug Market

Market Size in USD Million

USD

19.43 Million

USD

32.30 Million

2024

2032

USD

19.43 Million

USD

32.30 Million

2024

2032

| 2025 - 2032 | |

| USD 19.43 Million | |

| USD 32.30 Million | |

| % | |

|

Hyperoxaluria Drug Market Size

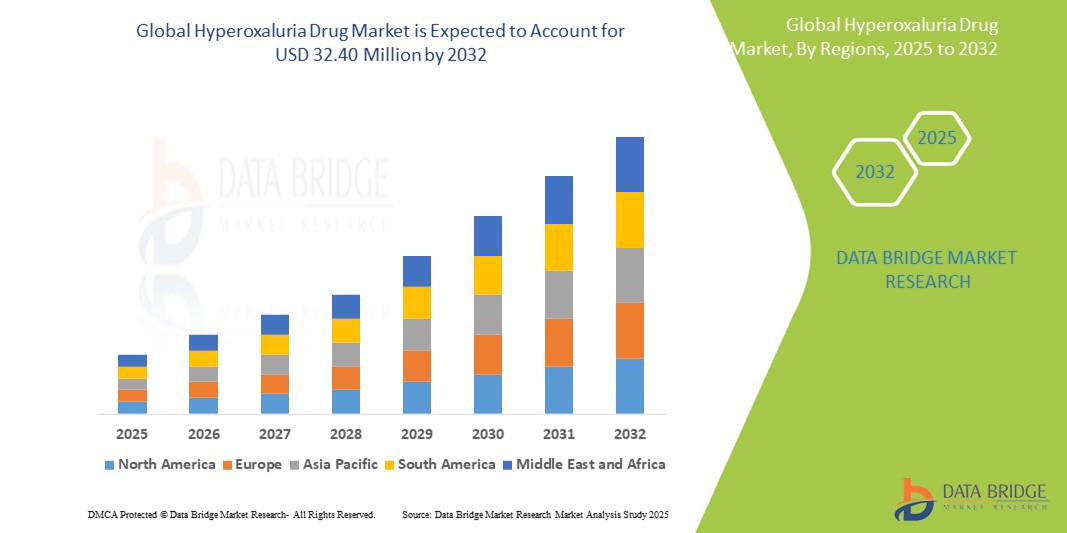

- The global hyperoxaluria drug market size was valued at USD 19.43 million in 2024 and is expected to reach USD 32.40 million by 2032, at a CAGR of 6.6% during the forecast period

- The market growth is primarily driven by increasing prevalence of rare kidney disorders, greater awareness of primary and secondary hyperoxaluria, and the rising availability of novel treatment options, including RNAi-based therapies and enzyme replacement products

- Furthermore, strong R&D pipelines, supportive regulatory frameworks for orphan drugs, and growing patient advocacy are contributing to a surge in innovation and approvals. These combined factors are accelerating therapeutic development and uptake, thereby significantly propelling the expansion of the hyperoxaluria drug industry

Hyperoxaluria Drug Market Analysis

- Hyperoxaluria drugs, aimed at reducing excess oxalate accumulation in the body, have become increasingly essential in managing primary and secondary hyperoxaluria—rare but serious conditions that can lead to recurrent kidney stones and renal failure if untreated. These drugs range from enzyme replacement therapies to RNA interference (RNAi) treatments and small molecule inhibitors

- The growing demand for hyperoxaluria treatments is primarily driven by increased disease awareness, improved diagnostic capabilities, and the expanding availability of orphan drugs that target rare metabolic disorders. Advancements in precision medicine and genomics are also enabling more personalized treatment approaches

- North America dominates the hyperoxaluria drug market with the largest revenue share of 41.5% in 2024, characterized by well-established healthcare infrastructure, high diagnosis rates, favorable reimbursement policies, and strong R&D activities

- Asia-Pacific is expected to be the fastest growing region in the hyperoxaluria drug market during the forecast period due to growing healthcare awareness, expansion of rare disease registries, and pharmaceutical investment in emerging markets

- Primary Hyperoxaluria segment dominates the hyperoxaluria drug market with a market share of 50.7% in 2024, driven by its higher prevalence, particularly of Type I, and the availability of targeted therapies such as RNAi-based treatments

Report Scope and Hyperoxaluria Drug Market Segmentation

|

Attributes |

Hyperoxaluria Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hyperoxaluria Drug Market Trends

“Advancements in RNAi Therapies and Precision Medicine Driving Market Growth”

- A significant and accelerating trend in the global hyperoxaluria drug market is the rapid adoption of RNA interference (RNAi) therapies and precision medicine approaches, which are transforming treatment paradigms by targeting the genetic root causes of the disease

- For instance, lumasiran and nedosiran have emerged as pioneering RNAi-based drugs that effectively reduce oxalate production, offering patients safer and more targeted options compared to conventional treatments

- RNAi therapies enable personalized treatment regimens based on specific gene mutations such as AGXT and GRHPR, enhancing therapeutic outcomes and minimizing adverse effects. Complementary approaches including enzyme replacement therapies and small molecule inhibitors are also gaining traction

- The integration of genetic testing and companion diagnostics into clinical practice is facilitating earlier diagnosis and better patient stratification, supporting more precise treatment decisions

- Companies such as Alnylam Pharmaceuticals and Dicerna Therapeutics are leading innovation by advancing next-generation therapies that leverage gene silencing and enzyme modulation technologies

- The demand for hyperoxaluria drugs that offer targeted, effective, and safer treatment options is growing rapidly across both developed and emerging markets, as patients and healthcare providers increasingly focus on long-term disease management and improved quality of life

Hyperoxaluria Drug Market Dynamics

Driver

“Increasing Prevalence of Hyperoxaluria and Advances in Targeted Therapies”

- The rising incidence of primary and secondary hyperoxaluria, along with growing awareness and diagnosis rates, is a significant driver fueling demand for effective hyperoxaluria drug treatments globally

- For instance, in 2024, Alnylam Pharmaceuticals advanced its RNAi-based drug lumasiran by expanding its approval for broader patient populations, signaling growing industry focus on innovative, targeted therapies to manage hyperoxaluria. Such developments by leading companies are expected to propel market growth during the forecast period

- As patients and healthcare providers increasingly prioritize treatments that can reduce oxalate accumulation and prevent kidney damage, hyperoxaluria drugs offering disease-modifying effects, including RNAi therapies and enzyme replacement options, are gaining rapid acceptance over traditional symptomatic treatments

- Furthermore, the integration of genetic testing and precision medicine is enabling tailored treatment approaches, improving patient outcomes and supporting the adoption of personalized hyperoxaluria therapies

- The expanding pipeline of novel drugs and growing investment in research and development are driving the availability of more effective and safer treatment options, thereby boosting demand across hospitals, specialty clinics, and homecare settings worldwide

Restraint/Challenge

“High Treatment Costs and Limited Awareness in Rare Disease Market”

- The high cost of innovative hyperoxaluria drugs, particularly RNAi therapies such as lumasiran and nedosiran, poses a significant challenge to broader patient access and market penetration, especially in regions with limited healthcare funding or insurance coverage.

- For instance, the expensive nature of these advanced treatments can limit affordability for many patients, leading to slower adoption despite their clinical benefits

- In addition, the rarity of hyperoxaluria and limited awareness among healthcare providers and patients often result in delayed diagnosis and underutilization of available therapies. This lack of awareness can hinder timely treatment initiation and restrict market growth

- While efforts are ongoing to improve reimbursement policies and expand patient assistance programs, the overall burden of cost remains a critical barrier, particularly in emerging markets and lower-income populations

- Overcoming these challenges through enhanced healthcare provider education, expanded diagnostic capabilities, and development of cost-effective therapeutic options will be essential to drive wider adoption and sustained growth in the hyperoxaluria drug market

Hyperoxaluria Drug Market Scope

The market is segmented on the basis of type, gene type, treatment type, drugs, mode of administration, distribution channel, and end user.

- By Type

On the basis of type, the hyperoxaluria drug market is segmented into primary hyperoxaluria and secondary hyperoxaluria. The primary hyperoxaluria segment held the largest market share of 50.7% share in 2024, primarily driven by its genetic origin and the significant clinical burden it imposes. This segment benefits from increased awareness and the development of gene-targeted therapies.

The secondary hyperoxaluria segment is expected to witness the fastest growth during the forecast period, due to rising incidence linked to metabolic disorders, gastrointestinal diseases, and dietary factors, which are becoming more prevalent globally.

- By Gene Type

On the basis of gene type, the market is segmented into AGXT, GRHPR, and others. The AGXT gene type segment lead the market in 2024, largely because it is the most common mutation in primary hyperoxaluria type 1 (PH1), resulting in a higher patient population and focused treatment efforts.

The others gene type segment is anticipated to register the fastest growth from 2025 to 2032, supported by advancements in genetic research that are identifying rarer mutations and enabling the development of novel therapeutics to target these less common genetic variations.

- By Treatment Type

On the basis of treatment type, the market is segmented into medication and surgery. Medication segment held the largest market revenue share in 2024 due to the increasing availability of pharmaceutical options such as RNA interference (RNAi) therapies and enzyme inhibitors, which offer non-invasive treatment alternatives.

The surgery segment, is expected to witness the fastest CAGR from 2025 to 2032, as the number of organ transplants, such as kidney and liver transplants, rises, along with improvements in surgical techniques that increase patient survival and quality of life.

- By Drugs

On the basis of drugs, the market is segmented into calcium oxalate urinary inhibitors, thiazide diuretics, and others. Calcium oxalate urinary inhibitors dominated the market in 2024 because they directly reduce the formation of oxalate stones, which are a major complication in hyperoxaluria patients.

The others drug segment, which includes emerging treatments such as RNAi therapies and enzyme modulators, is expected to witness the fastest growth in 2025 to 2032, due to their targeted mechanisms and promising clinical outcomes, making them increasingly preferred among healthcare providers.

- By Mode Of Administration

On the basis of mode of administration, the market is segmented into injectable, oral, and others. The oral segment held the largest market share in 2024 because oral medications are generally preferred for their convenience, ease of use, and better patient adherence.

The injectable segment is anticipated to witness the fastest growth from 2025 to 2032, driven by the growing adoption of RNAi-based injectable therapies that offer higher efficacy and longer-lasting effects in controlling oxalate production

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, and online pharmacies. Hospital pharmacies held the largest revenue share in 2024, reflecting the specialized treatment and monitoring needs of hyperoxaluria patients that are best managed in clinical settings.

Online pharmacies are expected to experience the fastest growth during forecast period, fueled by increasing patient preference for convenient access to medications, especially in remote areas, and the expanding e-commerce infrastructure supporting pharmaceutical distribution.

- By End User

On the basis of end user, the market is segmented into hospitals, homecare, specialty clinics, and others. Hospitals are the largest end users in 2024 due to their critical role in diagnosis, treatment, and management of hyperoxaluria, including complex therapies and surgeries.

The homecare segment is anticipated to register the fastest growth during forecast period, bolstered by advancements in patient monitoring technologies and the development of user-friendly medications that facilitate treatment adherence outside traditional healthcare facilities.

Hyperoxaluria Drug Market Regional Analysis

- North America dominates the hyperoxaluria drug market with the largest revenue share of 41.5% in 2024, driven by well-established healthcare infrastructure, high diagnosis rates, favorable reimbursement policies, and strong R&D activities

- The region benefits from the presence of leading pharmaceutical companies actively engaged in research and development of novel therapies, such as RNA interference (RNAi) drugs and enzyme replacement therapies specifically targeting hyperoxaluria subtypes

- Moreover, favorable reimbursement policies, a well-established diagnostic framework, and higher adoption of precision medicine contribute to the strong market performance in North America. The growing focus on orphan drug development and increasing government funding for rare disease research further solidify the region’s leadership in the hyperoxaluria drug market

U.S. Hyperoxaluria Drug Market Insight

The U.S. hyperoxaluria drug market captured the largest revenue share within North America in 2024, driven by a high incidence of primary hyperoxaluria and a robust diagnostic infrastructure that facilitates early detection. Increased awareness campaigns for rare genetic diseases and the availability of cutting-edge therapies, including RNAi-based drugs such as lumasiran, are major contributors to market expansion. Moreover, strong support from regulatory agencies such as the FDA for orphan drug development, along with favorable reimbursement scenarios, continues to fuel growth in the U.S. market.

Europe Hyperoxaluria Drug Market Insight

The Europe hyperoxaluria drug market is projected to grow at a substantial CAGR during the forecast period, owing to increasing research activities on rare metabolic disorders and heightened collaboration between pharmaceutical companies and academic institutions. The rise in genetic screening programs across countries such as Germany, France, and Italy is also facilitating earlier diagnosis and treatment. In addition, strong healthcare infrastructure and rising investments in the development of novel therapeutics are expected to contribute significantly to the market’s growth.

U.K. Hyperoxaluria Drug Market Insight

The U.K. hyperoxaluria drug market is anticipated to experience a notable CAGR over the forecast period, backed by proactive governmental initiatives in rare disease management and improved accessibility to advanced treatments. Growing patient advocacy and a focus on early genetic testing are strengthening the healthcare system’s ability to manage hyperoxaluria effectively. The expansion of clinical trials and the presence of leading biotech firms in the country are also playing a pivotal role in boosting the market.

Germany Hyperoxaluria Drug Market Insight

The Germany hyperoxaluria drug market is expected to expand steadily, driven by an emphasis on precision medicine and the increasing application of genomic diagnostics. Germany’s leadership in clinical research and its structured healthcare system support the development and adoption of innovative treatment solutions. Moreover, heightened awareness among nephrologists and pediatric specialists about metabolic kidney disorders is positively influencing the demand for targeted hyperoxaluria therapies.

Asia-Pacific Hyperoxaluria Drug Market Insight

The Asia-Pacific hyperoxaluria drug market is projected to grow at the fastest CAGR during the forecast period of 2025 to 2032, propelled by the rising prevalence of kidney-related disorders, growing healthcare investments, and improved genetic testing capabilities in countries such as China, India, and Japan. Government-led initiatives for rare disease registries and access to international funding are helping bridge treatment gaps in the region. In addition, collaborations between multinational pharmaceutical firms and local healthcare providers are improving access to hyperoxaluria treatments across the region.

Japan Hyperoxaluria Drug Market Insight

The Japan hyperoxaluria drug market is gaining traction due to the country’s strong emphasis on genetic screening and personalized medicine. The government's proactive approach to rare disease research and its robust pharmaceutical R&D ecosystem are contributing significantly to market growth. Japan’s aging population and increasing awareness of kidney-related complications are also driving demand for novel treatment options, particularly among specialists and tertiary care institutions

India Hyperoxaluria Drug Market Insight

The India hyperoxaluria drug market accounted for the largest revenue share in Asia-Pacific in 2024, supported by a growing burden of chronic kidney diseases and expanding access to molecular diagnostics. The increasing focus on rare disease policies and the emergence of biotechnology firms dedicated to orphan drug development are propelling market expansion. Moreover, rising health awareness, expanding private healthcare facilities, and affordability of therapies due to local manufacturing are key drivers shaping the hyperoxaluria drug landscape in India.

Hyperoxaluria Drug Market Share

The hyperoxaluria drug industry is primarily led by well-established companies, including:

- Alnylam Pharmaceuticals, Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- OxThera (Sweden)

- Recordati Industria Chimica e Farmaceutica S.p.A (Italy)

- AbbVie Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Bayer AG (Germany)

- AstraZeneca (U.K.)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- BioMarin Pharmaceutical Inc. (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Ionis Pharmaceuticals, Inc. (U.S.)

- Silence Therapeutics plc (U. K.)

- Synlogic (U.S.)

- Biocodex (France)

- Intellia Therapeutics, Inc. (U.S.)

Latest Developments in Global Hyperoxaluria Drug Market

- In February 2025, YolTech Therapeutics announced promising results from an ongoing investigator-initiated trial of YOLT-203, an investigational in vivo gene-editing therapy for PH1. The data showed an almost 70% reduction of 24-hour urinary oxalate levels in patients who received the high dose, sustained through a 16-week observation period. The therapy was well-tolerated with no serious adverse events

- In February 2025, Alnylam Pharmaceuticals reported continued market momentum for Oxlumo® (lumasiran), the first FDA-approved RNAi therapy for PH1, with global net product revenues reaching approximately USD 167 million for the full year of 2024, reflecting a 29% increase compared to the previous year. This growth underscores the expanding global adoption of Oxlumo and reinforces Alnylam's leadership in RNAi-based treatments for hyperoxaluria

- In December 2024, The FDA accepted an Investigational New Drug (IND) application for ABO-101, a liver-targeting gene editing therapeutic developed by Arbor Biotechnologies, to initiate a Phase 1/2 trial (redePHine) in adult and pediatric patients with PH1. ABO-101 is designed as a one-time treatment to permanently deactivate the HAO1 gene, thereby reducing oxalate production

- In September 2023, Novo Nordisk received FDA approval for Rivfloza (nedosiran), a novel RNA interference (RNAi) therapy targeting lactate dehydrogenase A (LDHA) for the treatment of primary hyperoxaluria type 1 (PH1). This approval marks a significant advancement in the management of PH1, offering a new therapeutic option for patients aged nine years and older

- In April 2023, Chinook Therapeutics voluntarily paused dosing in its Phase 1 clinical trial of CHK-336, an investigational oral LDH inhibitor for PH1, following a serious adverse event of anaphylaxis in a participant. The company is conducting a thorough investigation to assess the safety profile of CHK-336 before proceeding further

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.