Global Hyponatremia Treatment Market

Market Size in USD Billion

USD

2.49 Billion

USD

3.62 Billion

2024

2032

USD

2.49 Billion

USD

3.62 Billion

2024

2032

| 2025 - 2032 | |

| USD 2.49 Billion | |

| USD 3.62 Billion | |

| % | |

|

Hyponatremia Treatment Market Size

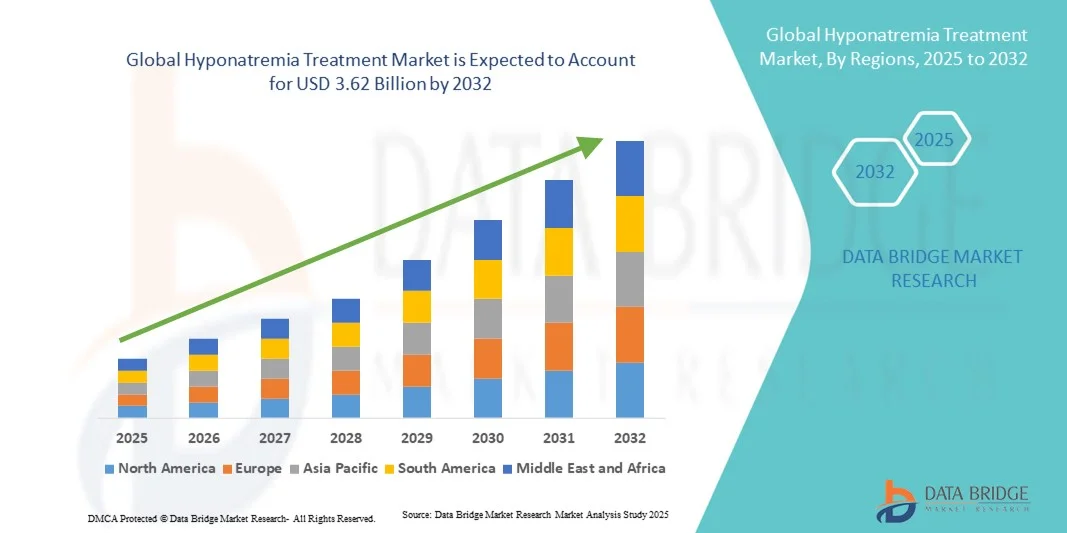

- The global hyponatremia treatment market size was valued at USD 2.49 billion in 2024 and is expected to reach USD 3.62 billion by 2032, at a CAGR of 4.80% during the forecast period

- The market growth is largely fueled by the increasing prevalence of hyponatremia across the globe, coupled with the rising awareness regarding early diagnosis and treatment. Technological advancements in diagnostic methods and the development of novel therapeutic approaches are further driving market expansion

- In addition, the growing geriatric population, increasing hospital admissions due to chronic diseases, and the introduction of advanced drug formulations are creating strong demand for effective hyponatremia treatment solutions. These combined factors are significantly accelerating the adoption of Hyponatremia Treatment products and boosting the overall market growth

Hyponatremia Treatment Market Analysis

- The Hyponatremia Treatment market, addressing the management of abnormally low sodium levels in the blood, is becoming increasingly important in modern healthcare settings due to the growing prevalence of chronic diseases, expanding elderly population, and rising awareness regarding electrolyte disorders

- The market growth is primarily driven by the increasing incidence of conditions such as heart failure, liver cirrhosis, and kidney diseases, which often lead to hyponatremia, along with advancements in diagnostic techniques and the development of more effective therapeutic options

- North America dominated the hyponatremia treatment market with the largest revenue share of 41.7% in 2024, supported by strong healthcare infrastructure, higher diagnosis rates, and widespread adoption of advanced treatment options. The U.S. led the region due to robust research activities, high healthcare expenditure, and the availability of branded as well as generic therapies

- Asia-Pacific is expected to be the fastest-growing region in the hyponatremia treatment market during the forecast period, attributed to the growing patient pool, increasing healthcare investments, and improved access to medical care in countries such as China, India, and Japan

- The Medication segment dominated the hyponatremia treatment market with the largest revenue share of 49.3% in 2024, driven by the widespread use of vasopressin receptor antagonists, loop diuretics, and demeclocycline in both acute and chronic cases

Report Scope and Hyponatremia Treatment Market Segmentation

|

Attributes |

Hyponatremia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Hyponatremia Treatment Market Trends

Enhanced Convenience Through Advanced Therapeutic Innovations

- A significant and accelerating trend in the global hyponatremia treatment market is the growing integration of advanced therapeutic technologies, innovative drug delivery systems, and digital health tools that enhance treatment precision and patient convenience. This convergence is enabling healthcare providers to deliver more personalized and effective care for individuals suffering from sodium imbalance disorders

- For instance, modern formulations such as tolvaptan-based therapies are increasingly being utilized for their targeted mechanism of action in managing hyponatremia associated with heart failure and SIADH (Syndrome of Inappropriate Antidiuretic Hormone Secretion). Similarly, the introduction of ready-to-use intravenous saline formulations and controlled-release oral therapies has streamlined hospital workflows while improving treatment safety and accuracy

- Recent advancements in point-of-care diagnostic systems have also improved the ability to monitor serum sodium levels in real time, enabling clinicians to make timely and precise therapeutic adjustments. Furthermore, digitally integrated treatment monitoring platforms are being adopted in clinical settings to help physicians track patient progress and adjust therapy regimens based on individual responses

- The seamless integration of such advanced therapeutic solutions with clinical decision-support tools facilitates centralized and efficient patient management. Through a single digital interface, healthcare professionals can monitor fluid balance, analyze laboratory results, and adjust medication doses, ensuring optimized treatment outcomes

- This trend toward data-driven, personalized, and patient-centric treatment approaches is fundamentally reshaping the management landscape for hyponatremia. Consequently, leading pharmaceutical companies such as Otsuka Pharmaceutical Co., Ltd., and Ferring Pharmaceuticals are investing heavily in research and development of next-generation therapies aimed at improving efficacy, reducing adverse effects, and enhancing patient compliance

- The demand for therapies that offer greater treatment precision, ease of administration, and improved patient experience is rising rapidly across hospitals and outpatient care facilities worldwide, as clinicians and healthcare systems increasingly emphasize the importance of comprehensive electrolyte management

Hyponatremia Treatment Market Dynamics

Driver

Growing Need Due to Rising Incidence and Awareness of Electrolyte Disorders

- The increasing global incidence of hyponatremia, driven by a growing elderly population, a higher prevalence of chronic diseases such as heart failure, liver cirrhosis, and kidney disorders, and increased hospitalization rates, is a key driver of market growth

- For instance, in April 2024, Otsuka Pharmaceutical Co., Ltd. expanded clinical trials for its vasopressin receptor antagonist therapy to evaluate its long-term efficacy and safety in managing chronic hyponatremia. Such developments underscore the rising need for innovative and reliable treatment options in this therapeutic area

- As clinicians and patients become more aware of the potential risks associated with untreated or mismanaged sodium imbalance, the demand for effective pharmacological and non-pharmacological interventions is increasing

- Furthermore, the growing focus on hospital-based electrolyte management programs and integrated diagnostic protocols is promoting the adoption of standardized treatment regimens that enhance both clinical outcomes and patient safety

- The convenience of novel formulations, including oral vasopressin antagonists and hypertonic saline infusions designed for controlled correction of sodium levels, is driving uptake in both inpatient and outpatient settings. In addition, the availability of evidence-based clinical guidelines and increased healthcare spending on electrolyte disorder management continue to strengthen market expansion

Restraint/Challenge

Concerns Regarding Adverse Effects, Treatment Costs, and Limited Access in Developing Regions

- Despite the growing demand, certain challenges—such as adverse side effects associated with specific drug classes, high treatment costs, and uneven healthcare access—pose constraints to broader adoption. For example, therapies like tolvaptan require close monitoring of liver function, which may limit their use in certain patient populations

- Moreover, high costs related to advanced pharmacological therapies can act as a barrier in low- and middle-income countries where healthcare budgets and reimbursement frameworks remain limited.

- Addressing these concerns through cost-effective generic drug production, expanded clinical awareness programs, and optimized dosage protocols is crucial to ensuring equitable treatment access. Pharmaceutical companies are increasingly emphasizing safety data transparency and affordability initiatives to build greater confidence among both clinicians and patients

- While healthcare infrastructure improvements are underway globally, disparities in diagnostic capabilities and medication availability continue to hinder consistent management of hyponatremia, particularly in rural or underdeveloped healthcare systems

- Overcoming these barriers through enhanced clinical education, robust pharmacovigilance programs, and strategic collaborations between pharmaceutical companies and healthcare organizations will be essential for achieving sustainable market growth

Hyponatremia Treatment Market Scope

The market is segmented on the basis of type, treatment, route of administration, end-users, and distribution channel.

- By Type

On the basis of type, the hyponatremia treatment market is segmented into pseudo hyponatremia, true hyponatremia, translocational hyponatremia, and others. The True Hyponatremia segment dominated the market with the largest revenue share of 46.8% in 2024, driven by its high prevalence among patients suffering from chronic kidney disease, congestive heart failure, and liver cirrhosis. True hyponatremia represents actual low serum sodium levels, making it the most clinically significant type requiring immediate medical management. Hospitals and specialized clinics prioritize the treatment of true hyponatremia due to its direct association with morbidity and mortality risk. Increasing awareness among healthcare professionals and better diagnostic capabilities further contribute to market dominance. The segment benefits from rising usage of vasopressin receptor antagonists, hypertonic saline infusions, and other pharmacological interventions. Advanced monitoring techniques in ICU and critical care units enhance early detection and treatment efficiency. Government and private initiatives for electrolyte disorder awareness are reinforcing its adoption. Treatment protocols are standardized globally, making this segment central to overall market revenue. Growing geriatric populations and lifestyle-related chronic diseases add to the prevalence. Clinical research and new therapy approvals continuously support its strong market presence. Pharmaceutical innovations focusing on safety and efficacy of targeted therapies boost segment leadership. The combination of high disease burden and reliable treatment options ensures steady market growth and investment.

The Translocational Hyponatremia segment is anticipated to witness the fastest CAGR of 7.9% from 2025 to 2032, driven by increasing incidence of hyperglycemia-related sodium dilution and metabolic disorders. Translocational hyponatremia arises due to fluid shifts from hyperosmolar conditions, which are increasingly diagnosed in ICU and diabetic populations. Improved laboratory diagnostics help differentiate it from true hyponatremia, allowing timely intervention and preventing complications. Early detection and proper treatment guidelines have increased physician confidence in managing this type effectively. Growing awareness among healthcare professionals about its distinct pathophysiology fuels adoption. Hospitals and specialty clinics are increasingly implementing protocols for precise fluid management. Advances in point-of-care testing and monitoring equipment aid in faster diagnosis. Pharmaceutical options, combined with proper fluid therapy, provide effective outcomes. The prevalence of translocational hyponatremia in emergency care and surgical patients supports demand. Continuous medical education programs highlight its importance, driving adoption. Increasing urbanization and healthcare access in emerging economies add to growth opportunities. Investment in research for better therapeutic approaches is expected to accelerate market expansion. Rising outpatient monitoring and homecare options also contribute to segment growth, ensuring a rapid CAGR.

- By Treatment

On the basis of treatment, the hyponatremia treatment market is segmented into intravenous fluid therapy, medication, and others. The Medication segment dominated the market with the largest revenue share of 49.3% in 2024, driven by the widespread use of vasopressin receptor antagonists, loop diuretics, and demeclocycline in both acute and chronic cases. Medications offer targeted control of serum sodium levels with predictable outcomes, making them the first choice for physicians. Hospitals, clinics, and specialized care centers widely prefer pharmacological intervention for managing severe hyponatremia. Branded drugs such as tolvaptan and conivaptan are extensively prescribed due to proven efficacy. Increasing R&D investment for novel therapeutics further enhances segment leadership. The segment also benefits from strong regulatory approvals and insurance coverage in developed regions. Adoption of evidence-based treatment protocols improves clinical outcomes. High prevalence of comorbidities requiring long-term medication supports steady demand. Continuous medical education and clinical guidelines reinforce their usage. Growing patient awareness about drug therapies contributes to adoption. Pharmaceutical companies are expanding distribution channels globally. The combination of efficacy, accessibility, and standardized treatment pathways ensures dominance. Hospitals and outpatient facilities heavily rely on medications for both acute and preventive care.

The Intravenous Fluid Therapy segment is projected to witness the fastest CAGR of 8.2% from 2025 to 2032, as it remains essential for acute hyponatremia management. Hypertonic and isotonic saline solutions allow rapid correction of dangerously low sodium levels. ICU and emergency departments increasingly depend on fluid therapy for immediate stabilization. Improved clinical protocols ensure safe administration, minimizing the risk of osmotic demyelination syndrome. Adoption is rising in developing countries with growing hospital infrastructure. Integration with advanced infusion systems enhances precision and treatment outcomes. Healthcare providers are trained to customize therapy based on patient conditions. Hospitals prefer IV therapy for patients with severe comorbidities requiring constant monitoring. Telemedicine-supported monitoring and home infusion services contribute to outpatient adoption. Pharmaceutical innovations for safer IV formulations further boost growth. Rising prevalence of acute hyponatremia in surgical and oncology patients supports segment expansion. Awareness campaigns highlight timely fluid therapy intervention. Increasing focus on patient-centric care and faster hospital discharge drives sustained adoption.

- By Route of Administration

On the basis of route of administration, the hyponatremia treatment market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with the largest revenue share of 45.6% in 2024, owing to preference for intravenous administration in acute and hospital-managed cases. Parenteral administration ensures rapid and controlled correction of serum sodium levels, critical in ICU and emergency care. Hospitals prioritize this route for hypertonic saline and injectable vasopressin antagonists due to reliable therapeutic outcomes. Skilled medical staff and advanced infusion facilities facilitate administration. Continuous monitoring allows precise dosage adjustment. Government and private healthcare initiatives support hospital-based parenteral treatment. Standardized protocols for parenteral therapy improve safety and reduce complications. High adoption in critical care and post-surgical care settings strengthens segment leadership. Clinical guidelines favor parenteral administration for severe hyponatremia. The segment benefits from strong hospital infrastructure in North America and Europe. Pharmaceutical advancements ensure sterile, safe, and effective formulations. Awareness among healthcare professionals reinforces consistent adoption. The segment’s dominance is supported by high prevalence and critical care requirements.

The oral segment is expected to register the fastest CAGR of 7.4% from 2025 to 2032, driven by convenience and non-invasive treatment options for chronic hyponatremia. Oral medications like tolvaptan tablets provide flexibility for outpatient care and home-based therapy. Patient adherence improves due to ease of use and minimal monitoring requirements. Expansion of homecare services and telehealth support enhances oral therapy adoption. Pharmaceutical innovations for improved bioavailability and sustained-release formulations drive growth. Chronic disease management programs encourage oral therapy for long-term treatment. Hospitals and clinics increasingly prescribe oral medications for mild-to-moderate hyponatremia. Awareness campaigns inform patients about safe home administration. Outpatient clinics support oral therapy as cost-effective and patient-friendly. Growth in emerging markets with improving healthcare access strengthens adoption. Combination therapy options increase clinical versatility. Overall, patient convenience and expanding homecare infrastructure fuel rapid adoption.

- By End-Users

On the basis of end-users, the hyponatremia treatment market is segmented into clinics, hospitals, homecare, and others. The Hospitals segment accounted for the largest revenue share of 53.1% in 2024, driven by inpatient management of acute and complex hyponatremia cases. Hospitals have advanced diagnostic, monitoring, and therapeutic infrastructure. Multidisciplinary teams in ICU and critical care units ensure effective management. Hospitals offer intravenous therapy, pharmacological interventions, and continuous monitoring. High patient footfall and prevalence of comorbidities increase hospital adoption. Insurance coverage and reimbursement policies favor hospital-based treatments. Hospitals also serve as primary sites for clinical trials and adoption of new therapies. Continuous staff training enhances proper management protocols. Government and private hospital initiatives support infrastructure expansion. Hospitals remain the central distribution point for critical care drugs. Adoption of evidence-based treatment protocols strengthens outcomes. Urbanization and increasing healthcare expenditure reinforce segment dominance. Hospitals continue to remain the most trusted end-user for hyponatremia management.

The Homecare segment is anticipated to record the fastest CAGR of 8.6% from 2025 to 2032, driven by the growing trend of at-home monitoring and treatment for mild or chronic hyponatremia. Patients increasingly prefer oral medications and portable monitoring devices. Telemedicine platforms enable physicians to remotely monitor sodium levels and adjust therapy. Homecare adoption reduces hospital readmissions and costs. Availability of patient education resources enhances compliance. Chronic disease management programs promote safe home therapy. Expansion of healthcare insurance coverage for homecare treatments supports growth. Technological advancements in portable infusion and diagnostic devices facilitate adoption. The segment benefits from growing awareness about the convenience of home-based care. Elderly and mobility-challenged patients particularly benefit. Online pharmacies and e-health services complement homecare. Urban and semi-urban areas witness higher adoption rates. Homecare’s flexibility and patient-centric approach drive rapid market growth.

- By Distribution Channel

On the basis of distribution channel, the hyponatremia treatment market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment dominated the market with the largest revenue share of 47.8% in 2024, driven by centralized procurement and dispensing of critical medications. Hospitals ensure quality control and authenticity of therapies. Hospital pharmacies cater to inpatient and ICU requirements. Critical drugs such as vasopressin antagonists and hypertonic saline solutions are primarily sourced here. Clinical staff coordinate with hospital pharmacies for timely administration. Hospital pharmacies benefit from institutional trust and established supply chains. Bulk purchasing ensures availability of essential drugs. Regulatory compliance strengthens reliability and safety. Adoption of hospital pharmacy management systems improves operational efficiency. Integration with electronic health records facilitates prescription accuracy. Hospitals’ focus on patient safety enhances pharmacy utilization. Established relationships with pharmaceutical companies reinforce supply stability. Hospital pharmacies remain the primary distribution point for high-value medications.

The Online Pharmacy segment is projected to witness the fastest CAGR of 9.1% from 2025 to 2032, driven by convenience and growing e-commerce penetration in healthcare. Patients increasingly prefer online ordering of chronic therapy medications. Telemedicine services integrate with online pharmacies for home delivery. Digital platforms provide better price transparency, availability, and patient support. Online pharmacies enhance access in remote and underserved regions. Increased smartphone penetration and internet access drive usage. Subscription and auto-refill services improve adherence. Regulatory frameworks in developed countries support online pharmaceutical sales. Homecare and outpatient therapy expansion favor online distribution. Marketing and awareness campaigns boost patient confidence. Partnerships with logistics companies ensure timely delivery. Patient education and safety information are widely available digitally. The segment benefits from growth in digital health adoption globally, ensuring sustained high CAGR.

Hyponatremia Treatment Market Regional Analysis

- North America dominated the hyponatremia treatment market with the largest revenue share of 41.7% in 2024, supported by a well-established healthcare infrastructure, higher diagnosis and treatment rates, and the widespread adoption of advanced therapeutic options

- The region’s strong focus on clinical research, along with the presence of major pharmaceutical players, continues to accelerate the adoption of both branded and generic drugs for managing sodium imbalance disorders

- Moreover, favorable reimbursement policies and increased awareness among clinicians regarding the risks associated with hyponatremia are contributing to the region’s market leadership

U.S. Hyponatremia Treatment Market Insight

The U.S. hyponatremia treatment market captured the largest revenue share in 2024 within North America, driven by high healthcare expenditure, robust diagnostic capabilities, and strong demand for innovative therapies such as vasopressin receptor antagonists and hypertonic saline formulations. The country’s advanced clinical infrastructure and extensive research activities in electrolyte disorder management are fostering greater treatment adoption. In addition, a growing elderly population, increased hospital admissions, and the prevalence of chronic conditions such as heart failure and liver cirrhosis are driving consistent demand for hyponatremia management solutions across hospitals and outpatient care settings.

Europe Hyponatremia Treatment Market Insight

The Europe hyponatremia treatment market is projected to expand at a substantial CAGR throughout the forecast period, supported by rising awareness about electrolyte imbalance disorders and improvements in clinical management protocols across the region. The presence of well-structured healthcare systems and government-backed initiatives to enhance diagnostic accuracy are fueling the adoption of standardized treatment approaches. Moreover, an aging population and the growing incidence of chronic diseases such as kidney disorders are further increasing demand for targeted therapies. The region is also witnessing growing investments in hospital-based monitoring systems to ensure timely detection and management of hyponatremia cases.

U.K. Hyponatremia Treatment Market Insight

The U.K. hyponatremia treatment market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the rising burden of chronic illnesses, increasing hospital admissions, and greater clinical focus on managing electrolyte imbalances. The National Health Service (NHS) has emphasized improved screening and treatment for conditions that commonly lead to hyponatremia, such as heart failure and cirrhosis. Furthermore, growing public health awareness and ongoing research on cost-effective therapies are expected to strengthen market penetration. The integration of evidence-based guidelines in clinical practice is also enhancing treatment outcomes and supporting steady market growth.

Germany Hyponatremia Treatment Market Insight

The Germany hyponatremia treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by a strong focus on medical innovation, clinical research, and patient safety. Germany’s well-developed hospital infrastructure and emphasis on treatment optimization through precision medicine support increased adoption of advanced pharmacological therapies. The country’s large elderly demographic, combined with a high prevalence of cardiovascular and renal disorders, continues to drive demand for reliable hyponatremia management solutions. In addition, the growing use of real-world evidence and clinical data analytics in healthcare decision-making is improving treatment accuracy and patient outcomes.

Asia-Pacific Hyponatremia Treatment Market Insight

The Asia-Pacific hyponatremia treatment market is poised to grow at the fastest CAGR during the forecast period (2025–2032), driven by the rising prevalence of chronic diseases, growing healthcare investments, and improved access to diagnostic and treatment services across developing economies. Rapid urbanization, economic growth, and increasing health awareness in countries such as China, India, and Japan are boosting the demand for effective treatment options. In addition, government-led healthcare reforms, expansion of hospital networks, and a growing focus on early diagnosis are improving patient outcomes. The presence of local manufacturers offering cost-effective generic formulations further supports market expansion.

Japan Hyponatremia Treatment Market Insight

The Japan hyponatremia treatment market is gaining momentum due to the country’s aging population, strong emphasis on clinical quality, and growing demand for personalized treatment regimens. Japan’s healthcare system encourages early diagnosis and continuous monitoring of electrolyte disorders, which supports the adoption of advanced therapies. The country’s research-driven pharmaceutical sector and government initiatives aimed at managing chronic diseases are further stimulating growth. In addition, the focus on patient safety and innovation in hospital care continues to promote the utilization of both traditional and novel treatment approaches for hyponatremia.

China Hyponatremia Treatment Market Insight

The China hyponatremia treatment market accounted for the largest market revenue share in Asia-Pacific in 2024, attributed to the country’s vast patient pool, growing healthcare expenditure, and rapid improvement in hospital infrastructure. Increasing awareness of electrolyte disorders and government initiatives to strengthen diagnostic capacity are key growth drivers. China’s emergence as a leading hub for pharmaceutical manufacturing ensures wide availability of both branded and generic formulations at competitive prices. The integration of clinical data systems and digital health platforms is also enhancing treatment efficiency and accessibility, contributing to sustained market growth.

Hyponatremia Treatment Market Share

The Hyponatremia Treatment industry is primarily led by well-established companies, including:

- Otsuka Pharmaceutical Co., Ltd. (Japan)

- Pfizer, Inc. (U.S.)

- Baxter International Inc. (U.S.)

- Sanofi (France)

- Fresenius Kabi AG (Germany)

- Astellas Pharma US, Inc. (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Alkem Laboratories Ltd. (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Cumberland Pharmaceuticals Inc. (U.S.)

Latest Developments in Global Hyponatremia Treatment Market

- In October 2025, AstraZeneca announced that its experimental drug, baxdrostat, achieved the primary goal in a late-stage clinical trial for patients with treatment-resistant hypertension. Over a 12-week period, patients who received 2 mg of baxdrostat in addition to standard care showed significantly reduced blood pressure compared to those on a placebo. The treatment targets the hormone aldosterone, offering a novel approach distinct from traditional therapies. AstraZeneca plans to file for regulatory approval by the end of 2025 and anticipates baxdrostat could generate over USD 5 billion in peak annual sales

- In March 2025, the U.S. Food and Drug Administration (FDA) approved Samsca (tolvaptan) for the treatment of clinically significant hypervolemic and euvolemic hyponatremia. Samsca is a selective vasopressin V2-receptor antagonist indicated for the treatment of low serum sodium concentrations associated with conditions such as heart failure and the syndrome of inappropriate antidiuretic hormone secretion (SIADH)

- In October 2024, a study published in the Journal of Clinical Endocrinology & Metabolism compared the efficacy of tolvaptan versus fluid restriction in patients with moderate to profound hyponatremia. The study found that tolvaptan, an AVP V2 receptor antagonist, is an effective alternative treatment for hyponatremia, providing a significant therapeutic option for clinicians managing this condition

- In May 2024, a study published in the journal Kidney International examined the safety and efficacy of low-dose tolvaptan for the treatment of the syndrome of inappropriate antidiuretic hormone secretion (SIADH)-associated hyponatremia. The study concluded that low-dose tolvaptan is effective and safe for the treatment of SIADH-associated hyponatremia, offering a potential therapeutic option for this patient population

- In March 2024, a study published in Nephrology Dialysis Transplantation reviewed the standard treatment protocols for hyponatremia, emphasizing the importance of individualized treatment plans. The study highlighted that while fluid restriction is a common initial approach, the choice of second-line therapy, such as the use of vaptans, should be based on specific patient characteristics and underlying causes of hyponatremia

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.