Global Icu Devices Market

Market Size in USD Billion

CAGR :

%

USD

9.14 Billion

USD

13.97 Billion

2025

2033

USD

9.14 Billion

USD

13.97 Billion

2025

2033

| 2026 –2033 | |

| USD 9.14 Billion | |

| USD 13.97 Billion | |

| % | |

|

Intensive Care Unit (ICU) Devices Market Size

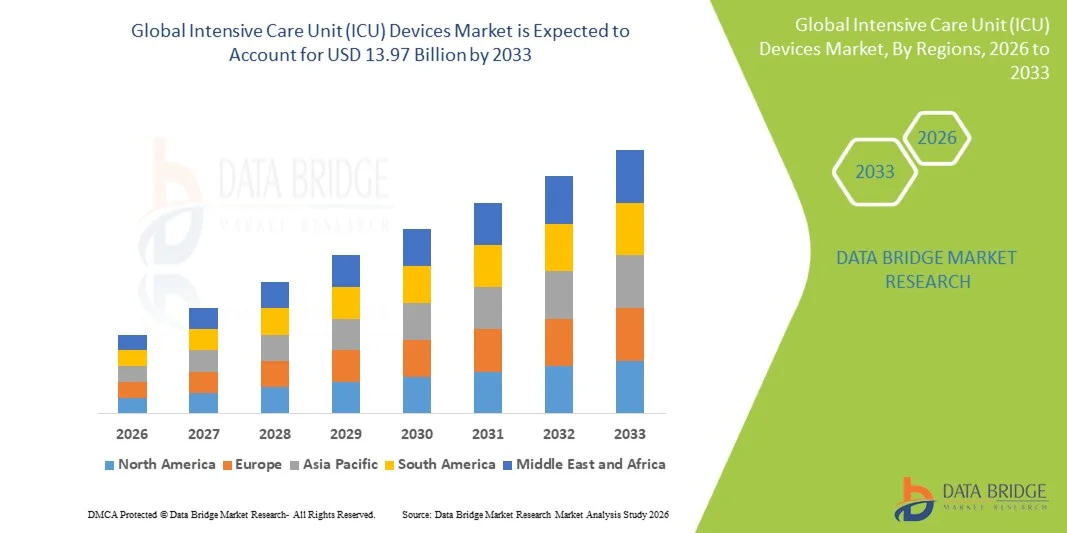

- The global Intensive Care Unit (ICU) devices market size was valued at USD 9.14 billion in 2025and is expected to reach USD 13.97 billion by 2033, at a CAGR of 5.45% during the forecast period

- The market growth is largely fueled by the rising incidence of critical illnesses, increasing surgical procedures, and the growing burden of chronic diseases, which is driving demand for advanced life-support and patient monitoring equipment in ICU settings

- Furthermore, continuous technological advancements in ventilators, patient monitoring systems, infusion pumps, and dialysis equipment, along with increasing healthcare infrastructure expansion and ICU capacity worldwide, are establishing advanced ICU devices as essential components of critical care delivery. These converging factors are accelerating the adoption of ICU technologies, thereby significantly boosting the industry's growth

Intensive Care Unit (ICU) Devices Market Analysis

- Intensive Care Unit (ICU) devices, offering advanced life-support, monitoring, and patient management solutions such as ventilators, cardiac monitors, feeding tubes, and vascular access devices, are critical components of modern healthcare infrastructure, widely deployed in hospital ICUs to manage critically ill patients requiring continuous and specialized care

- The increasing demand for Intensive Care Unit (ICU) devices is primarily driven by the rising prevalence of chronic diseases, growing incidence of respiratory and cardiovascular conditions, and an increasing number of surgeries and trauma cases requiring intensive post-operative monitoring and life-support intervention

- North America dominated the Intensive Care Unit (ICU) devices market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, high ICU bed capacity, strong adoption of advanced critical care technologies, and the presence of leading medical device manufacturers, with the U.S. witnessing significant utilization of ICU systems in emergency and tertiary care hospitals

- Asia-Pacific is expected to be the fastest growing region in the Intensive Care Unit (ICU) devices market during the forecast period due to rapid healthcare infrastructure expansion, increasing government investments in critical care facilities, rising patient population, and improving access to advanced hospital care in emerging economies such as China and India

- Mechanical Ventilators segment dominated the Intensive Care Unit (ICU) devices market with a market share of 44.1% in 2025, driven by their essential role in supporting patients with respiratory failure, increasing prevalence of pulmonary disorders, and continuous technological advancements in ventilatory support systems used in ICU settings

Report Scope and Intensive Care Unit (ICU) Devices Market Segmentation

|

Attributes |

Intensive Care Unit (ICU) Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· The increasing integration of AI-enabled predictive monitoring systems in Intensive Care Unit (ICU) devices · Growing expansion of modular and mobile ICU setups in emerging economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Intensive Care Unit (ICU) Devices Market Trends

“Integration of AI-Driven Predictive Monitoring in Critical Care Systems”

- A significant and accelerating trend in the global Intensive Care Unit (ICU) devices market is the increasing integration of artificial intelligence (AI) and predictive analytics into patient monitoring and life-support systems, enhancing early detection of patient deterioration and improving clinical decision-making in ICU settings

- For instance, advanced ICU monitoring platforms are now being integrated with AI-enabled ventilators and cardiac monitors that continuously analyze patient vitals in real time and provide automated risk alerts to healthcare professionals

- AI integration in Intensive Care Unit (ICU) devices enables features such as predictive deterioration scoring, automated alarm reduction, and intelligent adjustment of ventilation or infusion parameters based on patient response trends over time

- The seamless integration of ICU devices with hospital information systems and centralized monitoring platforms allows clinicians to manage multiple critically ill patients through unified dashboards, improving workflow efficiency and response time in emergency situations

- The growing use of advanced sensor-enabled ICU devices is improving continuous data capture accuracy, supporting more precise clinical interventions and reducing the risk of human error in intensive care environments

- This trend toward intelligent, interconnected, and data-driven ICU ecosystems is fundamentally reshaping critical care delivery, with companies such as GE HealthCare and Philips developing AI-powered ICU monitoring solutions with enhanced decision-support capabilities

- The demand for AI-integrated Intensive Care Unit (ICU) devices is growing rapidly across hospitals and emergency care centers, as healthcare providers increasingly prioritize precision care, operational efficiency, and improved patient survival outcomes

Intensive Care Unit (ICU) Devices Market Dynamics

Driver

“Rising Burden of Critical Illnesses and Expanding ICU Infrastructure”

- The increasing prevalence of chronic diseases, respiratory disorders, and multi-organ failure cases, coupled with the expansion of ICU infrastructure in hospitals, is a significant driver for the growing demand for Intensive Care Unit (ICU) devices

- For instance, in April 2025, several hospital networks expanded their critical care capacity by adding advanced ventilators and multiparameter monitors to strengthen emergency preparedness and intensive care response systems

- As the global patient population requiring critical care continues to rise, Intensive Care Unit (ICU) devices provide essential support through continuous monitoring, life-support functions, and real-time physiological assessment

- Furthermore, the increasing number of surgical procedures and trauma cases is making ICU devices essential in post-operative care management, ensuring patient stability and reducing mortality risks in hospitals

- The growing focus on healthcare modernization and expansion of ICU bed capacity in both developed and emerging economies is further driving the adoption of advanced Intensive Care Unit (ICU) devices across clinical settings

- Rising healthcare expenditure and government initiatives to strengthen critical care infrastructure are further accelerating procurement of advanced ICU equipment in public and private hospitals

- Increasing demand for emergency preparedness following infectious disease outbreaks is pushing hospitals to upgrade and expand ICU capabilities with advanced monitoring and ventilation systems

Restraint/Challenge

“High Equipment Cost and Complex Regulatory Compliance Requirements”

- Concerns surrounding the high cost of advanced ICU devices and stringent regulatory approval processes pose a significant challenge to wider market penetration, particularly in cost-sensitive and developing healthcare systems

- For instance, high investment requirements for advanced ventilators, multiparameter monitors, and integrated ICU systems often limit adoption in smaller hospitals and underfunded healthcare facilities

- The complex regulatory approval pathways for Intensive Care Unit (ICU) devices, including strict clinical validation and safety standards, can delay product launches and increase development timelines for manufacturers

- Addressing these cost and compliance challenges through scalable manufacturing, reimbursement support, and streamlined regulatory frameworks is crucial for improving accessibility and adoption of ICU technologies

- In addition, variability in healthcare budgets across regions further restricts uniform deployment of advanced Intensive Care Unit (ICU) devices, particularly in emerging markets with limited critical care funding

- Shortage of skilled critical care professionals capable of operating advanced ICU systems also limits effective utilization of sophisticated devices in many healthcare facilities

- Integration challenges with existing hospital infrastructure and legacy systems further complicate adoption, requiring additional investment in digital upgrades and interoperability solutions

Intensive Care Unit (ICU) Devices Market Scope

The market is segmented on the basis of type, end-user, and application.

- By Type

On the basis of type, the Intensive Care Unit (ICU) Devices market is segmented into mechanical ventilators, cardiac monitors, equipment for constant monitoring, feeding tubes, nasogastric tubes, suction pumps, drains, and catheters. The mechanical ventilators segment dominated the market with the largest revenue share of 44.1% in 2025, driven by their critical role in supporting patients with respiratory failure and multi-organ complications in ICU settings. Hospitals widely prioritize ventilators due to their life-saving functionality, especially in emergency and post-operative care. In addition, technological advancements such as portable ventilators and AI-assisted respiratory support systems are further strengthening their dominance. Increasing cases of respiratory diseases and pandemic preparedness initiatives also continue to reinforce demand for this segment across global healthcare systems.

The cardiac monitors segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising prevalence of cardiovascular diseases and the growing need for continuous real-time cardiac monitoring in critically ill patients. These devices are increasingly integrated with advanced telemetry and AI-based arrhythmia detection systems, improving early intervention capabilities in ICU environments. Hospitals are rapidly adopting multi-parameter cardiac monitoring systems to enhance patient safety and reduce mortality risks. The expansion of cardiac ICUs and increasing focus on early diagnosis of heart-related complications are further accelerating segment growth. Moreover, integration with centralized hospital monitoring networks is making cardiac monitors more efficient and widely deployed in modern ICU setups.

- By End-User

On the basis of end-user, the Intensive Care Unit (ICU) Devices market is segmented into hospitals and ambulatory surgical centers. The hospitals segment dominated the market with the largest revenue share in 2025, driven by the high concentration of ICU beds, availability of advanced critical care infrastructure, and presence of specialized healthcare professionals. Hospitals are the primary centers for managing severe and life-threatening conditions requiring continuous monitoring and life-support systems. The increasing number of emergency admissions, trauma cases, and complex surgeries further strengthens hospital demand for ICU devices. In addition, large-scale investments in hospital modernization and expansion of critical care units globally continue to reinforce this dominance.

The ambulatory surgical centers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the rising shift toward minimally invasive procedures and outpatient surgical care. These centers are increasingly adopting compact ICU-grade monitoring and support devices to manage post-operative recovery and emergency stabilization. The cost-effectiveness and shorter patient stay associated with ambulatory care facilities are encouraging rapid adoption of essential ICU technologies. Furthermore, growing demand for decentralized healthcare services and expansion of surgical centers in emerging markets are boosting segment growth. Integration of portable monitoring systems and lightweight ICU devices is also supporting their increasing utilization in these facilities.

- By Application

On the basis of application, the Intensive Care Unit (ICU) Devices market is segmented into adult ICU and neonatal ICU. The adult ICU segment dominated the market with the largest revenue share in 2025, driven by the high burden of chronic diseases, cardiovascular disorders, respiratory failures, and trauma cases among the adult population. Adult ICUs account for the majority of critical care admissions globally, requiring continuous use of ventilators, cardiac monitors, and infusion systems. The rising aging population and increasing incidence of lifestyle-related diseases further contribute to sustained demand in this segment. In addition, hospitals prioritize adult ICU expansion due to higher patient inflow and complexity of critical care cases.

The neonatal ICU segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing focus on infant mortality reduction and improving neonatal healthcare infrastructure worldwide. Rising cases of premature births and birth complications are significantly increasing demand for specialized neonatal monitoring and respiratory support systems. Governments and healthcare organizations are investing heavily in neonatal intensive care facilities to improve survival rates of newborns. Advanced neonatal ventilators and incubators with integrated monitoring systems are gaining rapid adoption. Furthermore, growing awareness of neonatal health and expansion of maternity hospitals in emerging economies are strongly supporting segment growth.

Intensive Care Unit (ICU) Devices Market Regional Analysis

- North America dominated the Intensive Care Unit (ICU) devices market with the largest revenue share of 38.5% in 2025, supported by advanced healthcare infrastructure, high ICU bed capacity, strong adoption of advanced critical care technologies, and the presence of leading medical device manufacturers

- Healthcare providers in the region highly value advanced ICU devices such as ventilators, cardiac monitors, and multiparameter patient monitoring systems due to their critical role in improving patient survival and enabling real-time clinical decision-making

- This widespread adoption is further supported by high healthcare expenditure, rapid integration of advanced medical technologies, and strong presence of leading global medical device manufacturers, establishing Intensive Care Unit (ICU) Devices as a core component of critical care delivery

U.S. Intensive Care Unit (ICU) Devices Market Insight

The U.S. Intensive Care Unit (ICU) Devices market captured the largest revenue share in 2025 within North America, driven by a high prevalence of chronic diseases, advanced hospital infrastructure, and strong ICU bed capacity across healthcare facilities. Healthcare providers are increasingly prioritizing advanced life-support systems such as ventilators, cardiac monitors, and multiparameter monitoring devices to improve patient survival outcomes. The growing adoption of AI-enabled critical care solutions, combined with strong investments in hospital modernization and emergency preparedness, is further propelling market growth. Moreover, continuous integration of digital health platforms and real-time patient monitoring systems is significantly contributing to the expansion of Intensive Care Unit (ICU) Devices in the country.

Europe Intensive Care Unit (ICU) Devices Market Insight

The Europe Intensive Care Unit (ICU) Devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by an aging population, rising incidence of respiratory and cardiovascular diseases, and strong public healthcare systems. Increasing demand for advanced critical care infrastructure is fostering the adoption of ICU devices such as ventilators, infusion pumps, and cardiac monitoring systems across hospitals. European healthcare facilities are highly focused on patient safety and continuous monitoring, further accelerating device utilization. In addition, government initiatives aimed at expanding ICU capacity and upgrading hospital infrastructure are significantly supporting market growth across the region.

U.K. Intensive Care Unit (ICU) Devices Market Insight

The U.K. Intensive Care Unit (ICU) Devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for advanced critical care services and rising concerns over emergency preparedness. Growing cases of chronic illnesses and infectious diseases are encouraging hospitals to expand ICU capacity and adopt modern life-support systems. The country’s strong healthcare system and increasing investments in hospital digitalization are further supporting market expansion. Moreover, the integration of advanced monitoring systems and connected ICU technologies is improving patient management efficiency across healthcare facilities.

Germany Intensive Care Unit (ICU) Devices Market Insight

The Germany Intensive Care Unit (ICU) Devices market is expected to expand at a considerable CAGR during the forecast period, driven by strong healthcare infrastructure, increasing geriatric population, and rising demand for technologically advanced medical equipment. Germany’s emphasis on precision medicine and hospital innovation is accelerating the adoption of ICU devices such as ventilators, monitoring systems, and catheter-based care equipment. The country’s focus on high-quality patient care and digital health integration is further supporting market growth. In addition, increasing investments in hospital modernization and critical care upgrades are enhancing ICU device penetration across healthcare facilities.

Asia-Pacific Intensive Care Unit (ICU) Devices Market Insight

The Asia-Pacific Intensive Care Unit (ICU) Devices market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid healthcare infrastructure expansion, rising ICU admissions, and increasing burden of chronic and infectious diseases. Growing government investments in hospital development and critical care capacity are significantly boosting demand for ICU devices. The region’s expanding middle-class population and improving access to advanced healthcare services are further supporting market adoption. In addition, increasing focus on digital healthcare transformation and affordable critical care solutions is accelerating market growth across emerging economies.

Japan Intensive Care Unit (ICU) Devices Market Insight

The Japan Intensive Care Unit (ICU) Devices market is gaining momentum due to its advanced healthcare system, aging population, and high demand for technologically sophisticated medical solutions. The country places strong emphasis on patient safety and precision monitoring, driving adoption of advanced ICU devices such as ventilators and cardiac monitoring systems. Integration of IoT-enabled healthcare technologies and automated monitoring systems is further enhancing critical care efficiency. Moreover, increasing cases of age-related diseases are contributing to sustained demand for ICU support systems across hospitals and specialized care centers.

India Intensive Care Unit (ICU) Devices Market Insight

The India Intensive Care Unit (ICU) Devices market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expanding healthcare infrastructure, and rising prevalence of chronic and infectious diseases. The country is witnessing strong growth in ICU capacity expansion across public and private hospitals. Increasing government initiatives such as healthcare modernization and smart hospital projects are further driving adoption of ICU devices. In addition, growing availability of cost-effective medical technologies and rising awareness of critical care management are significantly propelling market growth in India.

Intensive Care Unit (ICU) Devices Market Share

The Intensive Care Unit (ICU) Devices industry is primarily led by well-established companies, including:

- GE HealthCare (U.S.)

- Koninklijke Philips N.V. (Netherlands)

- Medtronic (Ireland)

- Drägerwerk AG & Co. KGaA (Germany)

- Hamilton Medical AG (Switzerland)

- Getinge AB (Sweden)

- Vyaire Medical, Inc. (U.S.)

- Mindray Medical International Limited (China)

- BD (U.S.)

- Smiths Medical (U.K.)

- ResMed Inc. (U.S.)

- Fisher & Paykel Healthcare Corporation Limited (New Zealand)

- B. Braun SE (Germany)

- NIHON KOHDEN CORPORATION (Japan)

- ZOLL Medical Corporation (U.S.)

- Hill-Rom Holdings, Inc. (U.S.)

- Löwenstein Medical Technology GmbH + Co. KG (Germany)

- Stryker (U.S.)

- Inovytec Medical Solutions Ltd. (Israel)

What are the Recent Developments in Global Intensive Care Unit (ICU) Devices Market?

- In November 2025, GE HealthCare launched next-generation ICU monitoring and anesthesia solutions designed for high-acuity care environments, featuring advanced patient monitoring capabilities, improved hemodynamic tracking, and AI-enabled decision support. These systems are aimed at enhancing real-time clinical insights, improving workflow efficiency, and strengthening critical care outcomes in Intensive Care Unit (ICU) settings. The launch highlights the growing shift toward integrated ICU ecosystems combining monitoring, analytics, and life-support technologies

- In October 2025, leading companies including GE HealthCare, Dräger, and B. Braun advanced “Silent ICU” concepts with integrated monitoring solutions aimed at reducing alarm fatigue in Intensive Care Unit (ICU) settings. These systems centralize alerts and transmit critical notifications to mobile devices and control stations, improving response efficiency and patient safety. The innovation represents a major step toward smarter and more efficient ICU environments

- In June 2025, researchers introduced AI-based reinforcement learning models for optimizing mechanical ventilation in Intensive Care Unit (ICU) settings, enabling personalized respiratory support based on real-time patient physiological data. The system enhances ventilator performance by dynamically adjusting settings to improve safety and treatment efficiency. This innovation marks a significant advancement in AI-assisted critical care management

- In January 2025, Philips introduced an upgraded IntelliVue patient monitoring platform for Intensive Care Unit (ICU) environments, incorporating enhanced AI-driven analytics, wireless connectivity, and real-time clinical dashboards. The system is designed to support continuous patient surveillance and improve decision-making accuracy in critical care units. This development reflects the increasing adoption of digital and connected monitoring solutions in ICU infrastructure globally

- In March 2024, major medical device companies including Philips, Medtronic, ResMed, and GE HealthCare introduced enhanced ICU-grade ventilator technologies with improved hybrid ventilation modes, AI-assisted monitoring, and advanced safety features. These innovations are designed to support patients with severe respiratory failure and improve adaptability in Intensive Care Unit (ICU) settings. The development underscores continuous advancement in life-support systems as a core ICU requirement.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.