Global Implantable Continuous Cardiac Monitoring Devices Market

Market Size in USD Billion

USD

3.48 Billion

USD

8.92 Billion

2025

2033

USD

3.48 Billion

USD

8.92 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.48 Billion | |

| USD 8.92 Billion | |

| % | |

|

Implantable Continuous Cardiac Monitoring Devices Market Overview

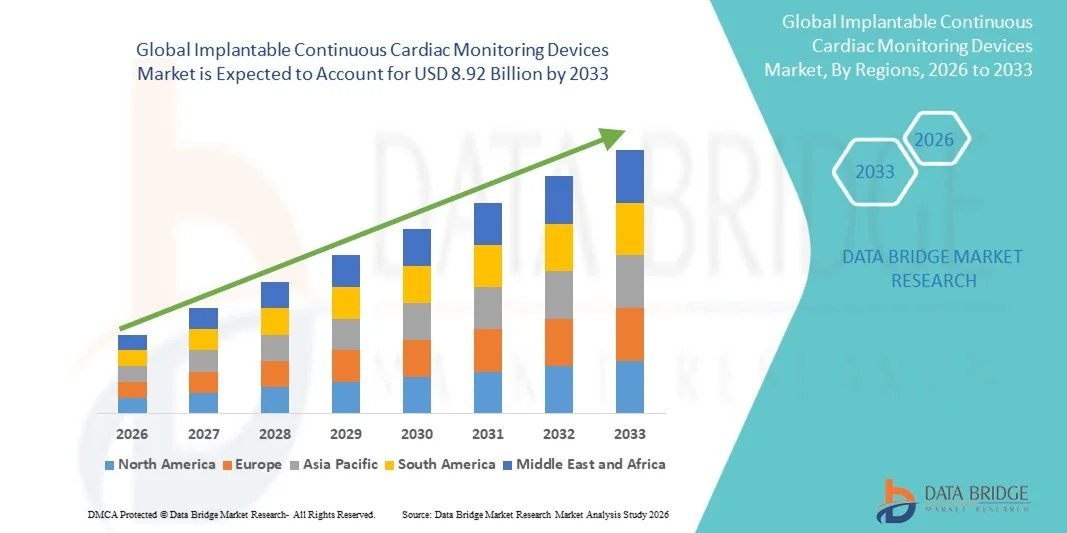

The Implantable Continuous Cardiac Monitoring Devices Market was valued at USD 3.48 billion in 2025 and is projected to reach USD 8.92 billion by 2033, growing at a CAGR of 12.50% from 2026 to 2033. The Implantable Continuous Cardiac Monitoring Devices Market is experiencing steady growth driven by the rising prevalence of cardiovascular diseases, increasing incidence of cardiac arrhythmias, and growing demand for continuous, real-time heart rhythm monitoring. Advancements in miniaturized implantable devices, improved sensor accuracy, and longer battery life are further enhancing clinical adoption across healthcare systems. Expanding applications in early diagnosis, post-operative monitoring, and long-term cardiac surveillance are strengthening market penetration across developed and emerging regions.

The increasing burden of heart-related disorders, coupled with a growing aging population and higher risk of atrial fibrillation and sudden cardiac events, is driving strong demand for implantable cardiac monitoring solutions. Supportive healthcare infrastructure development and rising adoption of minimally invasive diagnostic technologies are further accelerating growth. In addition, favorable reimbursement policies in several countries, along with increasing physician preference for continuous monitoring over traditional episodic diagnostics, are encouraging widespread adoption of implantable cardiac monitoring devices in hospitals and cardiac care centers.

Key Market Trends & Insights

- North America dominated the Implantable Continuous Cardiac Monitoring Devices Market and accounted for the largest revenue share of 39.42% in 2025, supported by advanced cardiovascular care infrastructure, high adoption of implantable cardiac monitoring technologies, strong presence of leading medtech companies, and increasing prevalence of atrial fibrillation and other cardiac arrhythmias. The region also benefits from favorable reimbursement policies, rapid adoption of remote patient monitoring systems, and strong integration of AI-enabled cardiac data analytics in clinical workflows.

- The Implantable Loop Recorders (ILRs) segment dominated the market in 2025 with a share of 42.6%, owing to their widespread clinical adoption for long-term cardiac rhythm monitoring in patients with unexplained syncope and intermittent arrhythmias.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.6% from 2026 to 2033, fueled by a rapidly increasing burden of cardiovascular diseases, expanding healthcare infrastructure, rising adoption of advanced cardiac monitoring technologies, and growing investments in digital health ecosystems across China, India, Japan, and South Korea. Government initiatives to improve early diagnosis and remote cardiac care access are further accelerating regional growth.

- Implantable Cardiac Monitors are witnessing strong adoption as hospitals increasingly shift toward continuous, long-duration cardiac surveillance for high-risk patients, especially in post-stroke monitoring and unexplained syncope cases. Rising demand for real-time cardiac rhythm assessment and remote monitoring integration is further strengthening segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 3.48 Billion

- Expected Market Value (2033): USD 8.92 Billion

- Forecast CAGR (2026–2033): 12.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Implantable Continuous Cardiac Monitoring Devices Market Segmentation

|

Attributes |

Implantable Continuous Cardiac Monitoring Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Medtronic plc (Ireland) |

|

Market Opportunities |

· Expansion of Remote Patient Monitoring and Digital Healthcare Ecosystems · Rising Adoption in Aging Population and High-Risk Patient Groups · Technological Advancements in Miniaturization and AI-Enabled Diagnostics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Implantable Continuous Cardiac Monitoring Devices Market Trends

Trend: Growth in Remote Cardiac Monitoring and Digital Health Integration

Healthcare providers are increasingly adopting implantable continuous cardiac monitoring devices integrated with remote patient monitoring platforms to enable real-time detection of arrhythmias and long-term cardiac rhythm tracking. These devices are widely used in patients with unexplained syncope, atrial fibrillation risk, and post-stroke monitoring. For instance, hospitals across the U.S. and Europe are increasingly connecting insertable cardiac monitors with cloud-based cardiology platforms, enabling clinicians to review cardiac events remotely and reduce in-person follow-ups by up to 30–40%, significantly improving care efficiency and early intervention outcomes.

Implantable Continuous Cardiac Monitoring Devices Market Dynamics

Key Market Driver: Rising Burden of Cardiovascular Diseases and Demand for Early Diagnosis

The increasing global prevalence of cardiovascular diseases, particularly atrial fibrillation and cardiac arrhythmias, is driving strong demand for implantable continuous cardiac monitoring devices. According to global health estimates, atrial fibrillation affects over 37 million people worldwide, with a significant portion remaining undiagnosed due to intermittent symptoms. Implantable loop recorders and cardiac monitors enable long-duration, continuous ECG monitoring, improving diagnostic yield in patients with unexplained fainting episodes and cryptogenic stroke. Hospitals are increasingly adopting these devices as part of preventive cardiology programs to enable earlier diagnosis and reduce long-term treatment costs.

Key Restraint/Challenge: High Device Cost and Limited Access in Emerging Markets

A major challenge in the global implantable cardiac monitoring market is the high cost of devices and associated implantation procedures, which limits accessibility in low- and middle-income regions. In addition constraints include the need for specialized cardiology expertise, procedural infrastructure, and follow-up monitoring systems. In many emerging economies, limited reimbursement coverage and lack of advanced electrophysiology labs further restrict adoption. These factors collectively slow penetration outside high-income healthcare systems despite strong clinical demand.

Key Market Opportunity: Expansion of AI-Enabled Remote Monitoring and Cloud-Based Cardiac Analytics

The integration of artificial intelligence, cloud computing, and remote cardiac data analytics presents a major growth opportunity for the market. Modern implantable cardiac monitors increasingly support wireless data transmission to cardiology platforms, enabling automated arrhythmia detection and predictive risk scoring. For instance, AI-assisted cardiac monitoring systems are being used in some U.S. and European hospitals to prioritize high-risk alerts, reducing clinician workload and improving response times in critical cardiac events. Expanding telecardiology infrastructure across Asia-Pacific is further expected to enhance access to continuous cardiac monitoring, particularly in rural and underserved populations.

Implantable Continuous Cardiac Monitoring Devices Market Scope

The Implantable Continuous Cardiac Monitoring Devices market is segmented on the basis of device type and end user.

- By Device Type

On the basis of device type, the Implantable Continuous Cardiac Monitoring Devices Market is segmented into Implantable Loop Recorders (ILRs), Implantable Cardiac Monitors, and Insertable Cardiac Monitors (ICMs). The Implantable Loop Recorders (ILRs) segment dominated the market in 2025 with a share of 42.6%, owing to their widespread clinical adoption for long-term cardiac rhythm monitoring in patients with unexplained syncope and intermittent arrhythmias. ILRs offer continuous ECG tracking with high diagnostic accuracy and minimal patient intervention, making them highly preferred in hospitals and cardiac centers. Growing incidence of atrial fibrillation and sudden cardiac arrest is further strengthening demand. Increasing physician preference for early and continuous diagnosis over episodic monitoring is supporting adoption. Technological improvements such as extended battery life and remote data transmission are enhancing usability. Rising geriatric population is also contributing significantly to segment dominance. Expansion of outpatient cardiac monitoring programs is boosting deployment. Integration with cloud-based cardiac analytics platforms is improving diagnostic efficiency. Overall, ILRs continue to dominate due to high clinical reliability and strong reimbursement support.

The Insertable Cardiac Monitors (ICMs) segment is expected to register the fastest growth with a CAGR of 9.4% from 2026 to 2033, driven by rising adoption of minimally invasive cardiac diagnostic solutions. Increasing demand for early detection of asymptomatic arrhythmias is significantly boosting ICM usage. Advancements in device miniaturization and wireless connectivity are improving patient comfort and compliance. Growing integration with AI-based cardiac monitoring platforms is enhancing diagnostic precision. Rising shift toward outpatient and home-based cardiac care is further accelerating demand. Hospitals are increasingly adopting ICMs for long-term post-stroke and high-risk patient monitoring. Expanding digital health ecosystems are enabling real-time remote cardiac tracking. Increasing awareness of preventive cardiology is also supporting adoption. Favorable regulatory approvals for next-generation devices are strengthening market expansion. These factors collectively are driving rapid growth of the ICM segment globally.

- By End User

On the basis of end user, the market is segmented into Hospitals, Cardiac Centers, Ambulatory Surgical Centers, and Home Healthcare Settings. The Hospitals segment dominated the market in 2025 with a share of 46.8%, due to strong availability of advanced diagnostic infrastructure and skilled cardiology professionals. Hospitals remain the primary point of implantation and long-term monitoring for cardiac patients. Increasing hospitalization rates for cardiovascular diseases are driving device utilization. Strong reimbursement frameworks in developed healthcare systems are supporting adoption. Integration of cardiac monitoring devices with hospital information systems is improving workflow efficiency. Rising emergency admissions for arrhythmias and syncope cases is further strengthening demand. Hospitals are also leveraging remote monitoring capabilities for post-discharge care. Expanding cardiology departments and specialized cardiac units are boosting usage. Increasing investments in advanced cardiac care technologies are enhancing diagnostic capabilities. Overall, hospitals remain the central hub for implantable cardiac monitoring procedures.

The Home Healthcare Settings segment is expected to witness the fastest growth with a CAGR of 10.1% from 2026 to 2033, driven by the rising shift toward decentralized and patient-centric healthcare delivery. Increasing preference for remote patient monitoring is reducing dependency on hospital stays. Growth in telecardiology platforms is enabling real-time data transmission from implanted devices to physicians. Expanding elderly population requiring long-term cardiac monitoring is further driving demand. Technological advancements in wireless connectivity and cloud-based analytics are enhancing home monitoring efficiency. Rising healthcare cost pressures are encouraging adoption of home-based care models. Increasing penetration of wearable and implantable hybrid monitoring systems is supporting growth. Government initiatives promoting home healthcare services are strengthening market expansion. Improved patient compliance and comfort are accelerating adoption. These factors collectively are making home healthcare the fastest-growing end-user segment.

Implantable Continuous Cardiac Monitoring Devices Market Regional Analysis

North America dominated the Implantable Continuous Cardiac Monitoring Devices market and accounted for the largest revenue share of 39.42% in 2025, supported by advanced cardiovascular care infrastructure, high adoption of implantable cardiac monitoring technologies, strong presence of leading medtech companies, and increasing prevalence of atrial fibrillation and other cardiac arrhythmias. The region also benefits from favorable reimbursement policies, rapid adoption of remote patient monitoring systems, and strong integration of AI-enabled cardiac data analytics in clinical workflows. Growing use of implantable loop recorders and insertable cardiac monitors in long-term arrhythmia detection and post-stroke surveillance continues to strengthen North America’s leadership position in the global market.

U.S. Implantable Continuous Cardiac Monitoring Devices Market Insight

The U.S. Implantable Continuous Cardiac Monitoring Devices market is witnessing strong growth due to rising incidence of atrial fibrillation, increasing adoption of remote cardiac monitoring platforms, and strong investments in digital health infrastructure. The country’s advanced electrophysiology centers and widespread availability of implantable loop recorders and insertable cardiac monitors are driving demand across hospitals and cardiac care centers. In addition, growing integration of AI-based arrhythmia detection tools and cloud-connected cardiac monitoring systems is improving early diagnosis rates and reducing hospital readmissions.

Europe Implantable Continuous Cardiac Monitoring Devices Market Insight

The Europe Implantable Continuous Cardiac Monitoring Devices market remains a major contributor to global revenue, driven by strong public healthcare systems, increasing cardiovascular disease burden, and rapid adoption of advanced cardiac monitoring technologies. The widespread use of implantable cardiac monitors in post-stroke patients and high-risk cardiac populations is supporting market expansion across the region. In addition, growing investment in remote patient monitoring infrastructure and AI-assisted ECG analytics is enhancing diagnostic efficiency and clinical decision-making across European healthcare systems.

U.K. Implantable Continuous Cardiac Monitoring Devices Market Insight

The U.K. Implantable Continuous Cardiac Monitoring Devices market is experiencing steady growth, supported by strong National Health Service (NHS) initiatives focused on early diagnosis of cardiac arrhythmias and expanding use of implantable loop recorders. Increasing demand for outpatient cardiac monitoring and remote follow-up systems is contributing to market growth. Furthermore, integration of digital cardiology platforms and AI-enabled diagnostic tools is improving patient monitoring efficiency and reducing long-term healthcare costs.

Germany Implantable Continuous Cardiac Monitoring Devices Market Insight

The Germany Implantable Continuous Cardiac Monitoring Devices market is expanding steadily due to strong hospital infrastructure, high adoption of advanced electrophysiology procedures, and increasing focus on early detection of cardiac disorders. Hospitals and cardiac centers are increasingly using implantable cardiac monitors for long-term rhythm tracking in patients with unexplained syncope and atrial fibrillation risk. Continuous advancements in minimally invasive implantation techniques and digital cardiac data integration are further supporting market growth.

Asia-Pacific Implantable Continuous Cardiac Monitoring Devices Market Insight

The Asia-Pacific Implantable Continuous Cardiac Monitoring Devices market is expected to witness rapid growth, driven by a rising burden of cardiovascular diseases, expanding healthcare infrastructure, and increasing awareness regarding early cardiac diagnosis. Growing adoption of implantable loop recorders and remote cardiac monitoring systems across China, India, Japan, and South Korea is supporting regional expansion. In addition, government initiatives aimed at improving access to cardiac care and strengthening digital health ecosystems are accelerating market growth across both urban and semi-urban healthcare settings.

Japan Implantable Continuous Cardiac Monitoring Devices Market Insight

The Japan Implantable Continuous Cardiac Monitoring Devices market is witnessing consistent growth due to an aging population, increasing prevalence of arrhythmias, and strong adoption of advanced cardiac monitoring technologies. Hospitals and cardiac centers are increasingly deploying implantable cardiac monitors for long-term rhythm surveillance in high-risk patients. Integration of AI-assisted diagnostics and remote monitoring platforms is further improving early detection and patient management outcomes.

China Implantable Continuous Cardiac Monitoring Devices Market Insight

The China Implantable Continuous Cardiac Monitoring Devices market is growing rapidly, driven by increasing cardiovascular disease burden, expanding hospital infrastructure, and rising adoption of advanced cardiac monitoring technologies. Growing use of implantable loop recorders and connected cardiac monitoring systems in large urban hospitals is improving early diagnosis of arrhythmias and stroke-related cardiac conditions. In addition, strong government support for digital healthcare transformation and increasing investments in cardiology care infrastructure are positioning China as one of the fastest-growing markets globally.

Implantable Continuous Cardiac Monitoring Devices Market Share

The Implantable Continuous Cardiac Monitoring Devices industry is primarily led by well-established companies, including:

- Medtronic plc (Ireland)

- Abbott Laboratories (U.S.)

- Biotronik SE & Co. KG (Germany)

- Boston Scientific Corporation (U.S.)

- Philips Healthcare (Netherlands)

- GE HealthCare Technologies Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- iRhythm Technologies, Inc. (U.S.)

- AliveCor Inc. (U.S.)

- LivaNova PLC (U.K.)

- Schiller AG (Switzerland)

- Hillrom (Baxter International Inc.) (U.S.)

- Spacelabs Healthcare (U.S.)

- Asahi Kasei Corporation (Japan)

- Osypka Medical GmbH (Germany)

- Medico S.p.A. (Italy)

- Biotricity Inc. (U.S.)

- Cardiac Insight Inc. (U.S.)

- VivaLNK Inc. (U.S.)

- Preventice Solutions (U.S.)

- BPL Medical Technologies (India)

- Tricog Health (India)

- Mindray Medical International (China)

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd. (China)

- Bittium Corporation (Finland)

- Compumedics Limited (Australia)

- Spencer Health Solutions (U.S.)

- InfoBionic Inc. (U.S.)

- Angel Medical Systems, Inc. (U.S.)

- BioTelemetry (Philips subsidiary) (U.S.)

- CardioNet (U.S.)

- Qardio Inc. (U.S.)

- VitalConnect Inc. (U.S.)

- LifeWatch AG (Switzerland)

- Rijuven Corp. (U.S.)

Latest Developments in Implantable Continuous Cardiac Monitoring Devices Market

- In February 2021, Abbott announced expanded real-world adoption of its Confirm Rx™ Insertable Cardiac Monitor (ICM), highlighting its Bluetooth-enabled remote monitoring capabilities and mobile app integration for continuous arrhythmia detection. The device strengthened the shift toward digitally connected cardiac monitoring, enabling physicians to receive near real-time cardiac data outside traditional hospital settings. This development marked a key step in expanding remote cardiac care and improving long-term monitoring for patients with unexplained syncope and atrial fibrillation risk

- In September 2022, Medtronic announced FDA clearance for expanded use of its LINQ II™ Insertable Cardiac Monitor in pediatric patients aged 2 years and older, significantly broadening its clinical application base. The LINQ II device, equipped with advanced algorithms and long-term monitoring capability of up to 4.5 years, supports continuous ECG recording for patients with suspected arrhythmias. This approval strengthened Medtronic’s leadership in the implantable cardiac monitoring segment and expanded diagnostic access for younger patient populations

- In March 2023, Biotronik continued global commercialization of its BIOMONITOR IV implantable cardiac monitor, enhancing remote data transmission and AI-assisted arrhythmia detection capabilities. The device is designed for long-term subcutaneous ECG monitoring and integrates advanced algorithms to improve diagnostic accuracy for atrial fibrillation and other cardiac rhythm disorders. This launch reinforced the growing trend of AI-enabled cardiac diagnostics and strengthened competition in the implantable monitoring device market

- In January 2024, Abbott advanced its next-generation Insertable Cardiac Monitor portfolio with enhanced AI-driven analytics through its Assert-IQ ICM platform, improving arrhythmia detection accuracy and reducing false-positive alerts. The system integrates Bluetooth connectivity and cloud-based data sharing, enabling seamless physician-patient interaction and continuous monitoring. This innovation highlighted the accelerating shift toward intelligent, data-driven cardiac monitoring ecosystems

- In June 2025, Boston Scientific expanded clinical deployment of its LUX-Dx Insertable Cardiac Monitor system, focusing on extended remote monitoring capabilities and improved diagnostic yield for patients with unexplained cardiac symptoms. The device supports long-term rhythm tracking with advanced detection algorithms and remote connectivity features, enabling efficient post-discharge monitoring. This expansion reflects the increasing demand for continuous, outpatient-based cardiac care solutions worldwide

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.