Global Implantable Drug Delivery Market

Market Size in USD Billion

CAGR :

%

USD

13.29 Billion

USD

24.78 Billion

2025

2033

USD

13.29 Billion

USD

24.78 Billion

2025

2033

| 2026 –2033 | |

| USD 13.29 Billion | |

| USD 24.78 Billion | |

| % | |

|

Implantable Drug Delivery Market Size

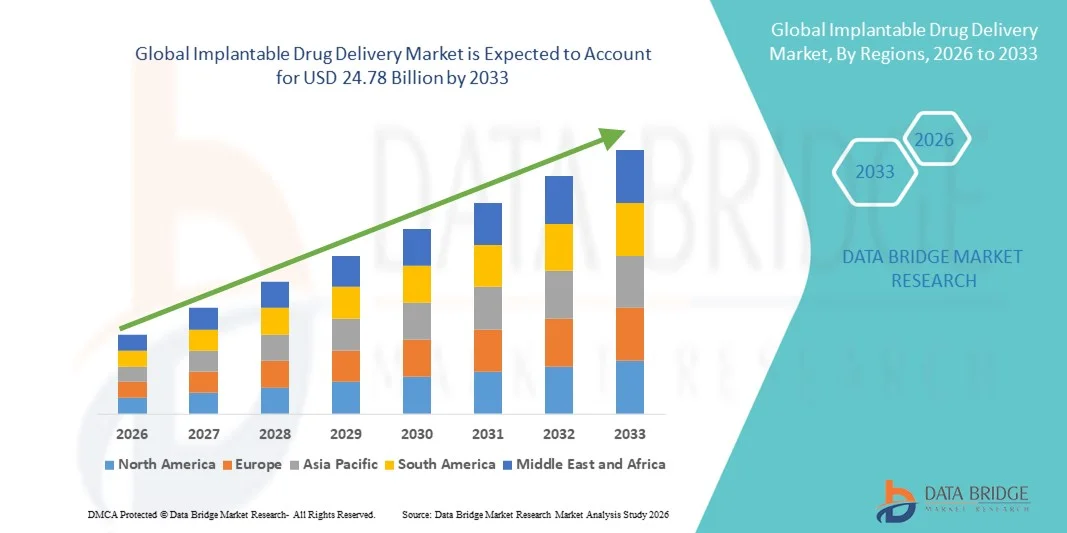

- The global implantable drug delivery market size was valued at USD 13.29 billion in 2025 and is expected to reach USD 24.78 billion by 2033, at a CAGR of 8.10% during the forecast period

- The market growth is largely fueled by the growing adoption and technological progress in advanced drug delivery systems, leading to improved treatment outcomes, patient compliance, and precision therapy in both chronic and acute conditions

- Furthermore, rising demand for minimally invasive treatment options, longer-acting therapeutic solutions, and patient-centric healthcare is establishing implantable drug delivery devices as a preferred method for targeted therapy. These converging factors are accelerating the uptake of Implantable Drug Delivery solutions, thereby significantly boosting the industry's growth

Implantable Drug Delivery Market Analysis

- Implantable drug delivery systems, offering controlled and targeted release of therapeutics, are increasingly vital components of modern healthcare, enabling long-term treatment for chronic diseases and improving patient compliance in both hospital and homecare settings due to their precision, safety, and convenience

- The escalating demand for implantable drug delivery solutions is primarily fueled by technological advancements, rising prevalence of chronic diseases, and a growing preference for minimally invasive and patient-friendly therapy options

- North America dominated the implantable drug delivery market with the largest revenue share of 37.8% in 2025, characterized by advanced healthcare infrastructure, high adoption of minimally invasive therapies, and strong presence of key medical device manufacturers, with the U.S. experiencing substantial growth in implantable drug delivery solutions driven by innovations in long-acting therapeutics and precision delivery systems

- Asia-Pacific is expected to be the fastest growing region in the implantable drug delivery market during the forecast period, with a projected CAGR of 9.7%, due to increasing healthcare expenditure, rising prevalence of chronic diseases, and growing adoption of advanced drug delivery technologies in emerging markets

- The non-biodegradable segment held the largest market revenue share of 55.2% in 2025, attributed to its extensive use across cardiovascular, oncology, and ophthalmology applications

Report Scope and Implantable Drug Delivery Market Segmentation

|

Attributes |

Implantable Drug Delivery Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Implantable Drug Delivery Market Trends

Enhanced Convenience Through Advanced Implantable Drug Delivery Systems

- A significant and accelerating trend in the global Implantable Drug Delivery market is the development of long-acting and minimally invasive delivery systems that improve patient adherence and comfort. These systems allow controlled, sustained drug release, reducing the frequency of hospital visits and enhancing treatment convenience

- For instance, advanced implantable devices for chronic conditions such as diabetes and cardiovascular diseases are being engineered for precision dosing over several weeks or months, offering patients a more consistent and reliable therapy

- Innovations in biodegradable materials and micro-implant technologies are enabling safer, targeted, and efficient drug delivery, while reducing risks associated with repeated injections or oral medications

- The integration of implantable devices with monitoring systems allows healthcare providers to track patient progress and optimize treatment plans, creating a more personalized therapeutic experience

- This trend towards more patient-centric, precise, and convenient drug delivery systems is reshaping expectations for chronic disease management. Consequently, companies such as Medtronic and Boston Scientific are developing next-generation implantable drug delivery solutions with enhanced safety, longer durations, and targeted release capabilities

- The demand for advanced implantable drug delivery systems is growing rapidly across both developed and emerging markets, as healthcare providers and patients prioritize treatment efficiency, safety, and improved quality of life

Implantable Drug Delivery Market Dynamics

Driver

Rising Prevalence of Chronic Diseases and Need for Improved Treatment Compliance

- The global increase in chronic diseases, including diabetes, cardiovascular disorders, cancer, and neurological conditions, is creating a sustained demand for long-term and reliable therapies. Implantable drug delivery systems offer consistent dosing over extended periods, reducing the risk of missed doses and improving overall treatment outcomes

- The shift towards patient-centric care is driving a preference for home-based treatments and outpatient management

- For instance, Patients increasingly seek solutions that minimize hospital visits, reduce dependency on caregivers, and allow greater independence in managing their therapies. Implantable devices provide an ideal solution, offering convenience, safety, and adherence while enabling real-time monitoring by healthcare professionals

- Continuous innovation in drug formulations, biodegradable implants, and micro-pump technologies is enhancing controlled and targeted drug release. This not only improves the efficacy of treatments but also minimizes side effects and systemic exposure, encouraging adoption in hospitals, clinics, and home-care settings

- Healthcare systems and providers are actively investing in technologies that optimize treatment efficiency, reduce complications, and improve patient quality of life. This includes the integration of implantable devices into disease management programs, electronic health records, and remote monitoring systems, ensuring better clinical outcomes

- Rising awareness among patients and caregivers about the benefits of implantable drug delivery—such as convenience, adherence, and improved disease management—is contributing to faster market acceptance. Patient education campaigns, clinical demonstrations, and professional endorsements are further strengthening demand globally

Restraint/Challenge

High Costs and Regulatory Challenges

- The relatively high cost of implantable drug delivery systems compared to conventional oral or injectable treatments presents a financial barrier, particularly in developing regions and among price-sensitive patient populations. High upfront costs can delay adoption despite long-term clinical benefits

- Stringent regulatory approvals and complex clinical trial requirements can significantly delay the market entry of new devices. Regulatory bodies demand extensive safety and efficacy data, including long-term follow-ups, which can limit small or emerging players from launching innovative products quickly

- For instance, Safety concerns, such as implant-related complications, infections, or device malfunctions, require extensive monitoring and risk mitigation. These concerns can reduce physician confidence and patient willingness to adopt implantable solutions without robust safety records

- The need for specialized healthcare infrastructure and trained personnel to implant and monitor these devices can restrain adoption in regions lacking skilled professionals or advanced clinical settings. In addition training programs and hospital investments are often necessary to support widespread use

- To address these challenges, manufacturers are focusing on cost-effective designs, improving device safety, and generating comprehensive clinical data to secure regulatory approvals. Strategic partnerships with healthcare providers and patient education initiatives are also being implemented to build trust, promote market acceptance, and ensure successful adoption of implantable drug delivery systems globally

Implantable Drug Delivery Market Scope

The market is segmented on the basis of product types, technology, and application.

- By Product Types

On the basis of product types, the Implantable Drug Delivery market is segmented into implantable bio-absorbable stents, implantable contraceptive drug delivery devices, implantable intraocular drug delivery devices, implantable coronary drug-eluting stents, implantable brachytherapy seeds, and implantable drug infusion pumps. The implantable bio-absorbable stents segment dominated the largest market revenue share of 38.6% in 2025, driven by their widespread adoption in cardiovascular therapies due to their ability to provide temporary scaffolding and gradually degrade within the body. These stents reduce the long-term risk of complications compared to permanent implants, leading to increased preference among cardiologists. The segment benefits from advancements in biomaterials and polymer technologies that enhance biocompatibility and therapeutic efficiency. Growing awareness about minimally invasive procedures and favorable reimbursement policies also drive demand. Bio-absorbable stents are increasingly used in both hospital and outpatient settings for coronary artery disease management. Research and development in next-generation stents further strengthens the market. Patient preference for safer, less invasive solutions continues to fuel adoption. Increasing prevalence of cardiovascular disorders globally supports the segment’s growth. Moreover, collaborations between device manufacturers and healthcare providers are expanding access to these devices. The rise in aging populations requiring cardiovascular interventions also contributes significantly. Continuous innovation in stent design and deployment techniques sustains market dominance.

The implantable contraceptive drug delivery devices segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, fueled by increasing demand for long-term, reversible contraception options. These devices, including subdermal implants, provide controlled hormone release over several years, offering convenience and reducing user compliance issues associated with oral contraceptives. Rising awareness of family planning and reproductive health initiatives globally is driving adoption. Governments and NGOs are promoting access to implantable contraceptives in emerging markets. Technological innovations in hormone delivery and biocompatible materials improve safety and efficacy. Women are increasingly seeking discreet and maintenance-free contraceptive options. The growing acceptance of women’s health technologies in both developed and developing countries supports segment growth. Healthcare providers are emphasizing implantable devices for family planning consultations. Private clinics and hospitals are investing in device availability and training. Online and direct-to-consumer awareness campaigns also contribute to adoption. Rising disposable incomes and urbanization further boost uptake. This segment is anticipated to experience rapid expansion due to global emphasis on reproductive health and wellness.

- By Technology

On the basis of technology, the market is segmented into biodegradable implantable drug delivery device technology and non-biodegradable implantable drug delivery device technology. The non-biodegradable segment held the largest market revenue share of 55.2% in 2025, attributed to its extensive use across cardiovascular, oncology, and ophthalmology applications. Non-biodegradable implants provide long-term therapeutic delivery, especially for conditions requiring sustained drug release or mechanical support. These devices benefit from established clinical efficacy and regulatory approvals. Hospitals and specialty centers often prefer non-biodegradable devices for predictable performance and patient outcomes. The segment also includes widely used coronary stents and brachytherapy seeds for oncology applications. Strong adoption in developed markets, supported by high healthcare expenditure, further strengthens the segment. The presence of a robust device manufacturing ecosystem contributes to market dominance. Regulatory frameworks in regions like North America and Europe favor the safe deployment of non-biodegradable implants. Training programs and professional expertise also facilitate adoption. Patient preference for reliable, long-term interventions supports market share. Established clinical guidelines frequently recommend non-biodegradable devices.

The biodegradable segment is expected to witness the fastest CAGR of 11.7% from 2026 to 2033, driven by the increasing focus on minimizing long-term implant complications and improving patient outcomes. Biodegradable technologies are particularly relevant in cardiovascular interventions and ocular drug delivery. Advancements in polymers and bioresorbable materials allow controlled degradation and targeted therapy. Emerging markets are increasingly adopting biodegradable implants due to favorable reimbursement policies and growing healthcare infrastructure. The technology is gaining traction in minimally invasive procedures. Patients prefer biodegradable devices as they reduce the need for secondary interventions. Clinical trials and research are expanding applications across oncology and ophthalmology. Awareness programs by manufacturers and healthcare providers enhance adoption rates. Biodegradable implants align with sustainable healthcare practices and patient-centric care. Innovations in device design continue to broaden therapeutic indications. Integration with drug-eluting technologies improves efficacy. The segment is poised for rapid growth due to its clinical benefits and technological advancements.

- By Application

On the basis of application, the Implantable Drug Delivery market is segmented into cardiovascular, birth control and contraception, ophthalmology, oncology, and others. The cardiovascular segment accounted for the largest market revenue share of 41.9% in 2025, driven by the rising prevalence of coronary artery disease and heart-related disorders. Implantable stents, coronary drug-eluting devices, and bio-absorbable scaffolds are extensively used in hospitals and cardiac centers to prevent restenosis and improve patient outcomes. Increased adoption of minimally invasive cardiovascular procedures boosts segment growth. The segment also benefits from favorable insurance coverage and reimbursement schemes. Clinical efficacy and long-term patient benefits further support demand. Hospitals and cardiac specialty centers are investing in advanced implantable devices. Cardiologists are adopting next-generation stents and drug delivery pumps. Awareness campaigns on cardiovascular health contribute to increased procedures. Innovations in device coatings and drug formulations improve therapeutic outcomes. Technological integration, such as monitoring sensors in stents, enhances patient safety. Growing aging populations with cardiovascular risks continue to support market dominance.

The birth control and contraception segment is expected to witness the fastest CAGR of 13.5% from 2026 to 2033, fueled by rising awareness of family planning and the advantages of long-term reversible contraception. Implantable contraceptive devices offer convenience, efficacy, and minimal maintenance, increasing their acceptance globally. Government initiatives and healthcare programs promoting women’s reproductive health drive adoption. Urbanization and rising disposable incomes support device accessibility. Increasing healthcare provider endorsements and training improve adoption rates. Technological improvements in hormone delivery systems enhance efficacy and safety. Private clinics and hospitals are expanding services for implantable contraceptive procedures. Direct-to-consumer awareness campaigns educate patients on device benefits. Emerging markets show growing acceptance due to accessibility and affordability. Cultural shifts toward reproductive autonomy support uptake. Online and telehealth consultations are facilitating awareness and usage. As a result, the segment is expected to be the fastest-growing application within the implantable drug delivery market.

Implantable Drug Delivery Market Regional Analysis

- North America dominated the implantable drug delivery market with the largest revenue share of 37.8% in 2025

- Characterized by advanced healthcare infrastructure, high adoption of minimally invasive therapies, and strong presence of key medical device manufacturers

- The region’s growth is driven by innovations in long-acting therapeutics, precision drug delivery systems, and increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and cancer

U.S. Implantable Drug Delivery Market Insight

The U.S. implantable drug delivery market captured the largest revenue share within North America in 2025, fueled by substantial growth in implantable solutions driven by advancements in precision drug delivery and long-acting therapeutics. Adoption is supported by strong healthcare infrastructure, ongoing R&D initiatives, patient-centric care models, and the rising prevalence of chronic diseases. Increasing demand for minimally invasive treatments and outpatient management is encouraging the use of implantable devices in hospitals, clinics, and home-care settings. Furthermore, government healthcare programs and private sector initiatives aimed at improving treatment adherence and clinical outcomes are contributing to market expansion.

Europe Implantable Drug Delivery Market Insight

The Europe implantable drug delivery market is projected to expand at a substantial CAGR throughout the forecast period, driven by modernization of hospital infrastructure, growing healthcare expenditure, and increasing adoption of minimally invasive therapies. The region’s growth is further supported by rising awareness of chronic disease management, investments in clinical research, and the need for patient-centric, home-based treatments. European countries are increasingly adopting implantable drug delivery devices in both hospitals and outpatient settings to enhance treatment efficacy and improve patient quality of life.

U.K. Implantable Drug Delivery Market Insight

The U.K. implantable drug delivery market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the rising prevalence of chronic diseases, increasing healthcare expenditure, and a shift toward patient-centric and home-based care. Adoption is supported by robust healthcare infrastructure, ongoing research in long-acting therapies, and the increasing preference for minimally invasive treatment options. The growing demand for improved treatment adherence, outpatient management, and enhanced clinical outcomes is further accelerating market expansion in the U.K.

Germany Implantable Drug Delivery Market Insight

The Germany implantable drug delivery market is expected to expand at a considerable CAGR during the forecast period, driven by advanced healthcare infrastructure, high investment in medical technology, and emphasis on innovative, minimally invasive treatment options. Increasing awareness of chronic disease management, strong hospital networks, and a focus on precision drug delivery are promoting adoption. Germany’s well-established regulatory and clinical ecosystem, along with technological innovations, supports market growth in both hospitals and home-care settings.

Asia-Pacific Implantable Drug Delivery Market Insight

The Asia-Pacific implantable drug delivery market is expected to be the fastest growing globally, with a projected CAGR of 9.7% during the forecast period, driven by increasing healthcare expenditure, rising prevalence of chronic diseases, and growing adoption of advanced drug delivery technologies. Rapid urbanization, improving healthcare infrastructure, and government initiatives promoting chronic disease management are key growth factors in the region.

Japan Implantable Drug Delivery Market Insight

The Japan implantable drug delivery market is witnessing strong growth due to the country’s aging population, high adoption of advanced medical technologies, and emphasis on minimally invasive treatments. Rising demand for patient-centric care and outpatient therapies, combined with government support for chronic disease management, is fueling the adoption of implantable drug delivery systems across hospitals and home-care settings.

China Implantable Drug Delivery Market Insight

The China implantable drug delivery market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, expanding middle-class population, and increasing prevalence of chronic diseases. Strong domestic medical device manufacturing, government initiatives for healthcare modernization, and the push toward smart healthcare solutions are accelerating adoption in both hospital and home-care settings..

Implantable Drug Delivery Market Share

The Implantable Drug Delivery industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Boston Scientific (U.S.)

- Becton Dickinson (U.S.)

- Abbott (U.S.)

- Teleflex Incorporated (U.S.)

- Stryker Corporation (U.S.)

- Intarcia Therapeutics (U.S.)

- Bayer AG (Germany)

- Ipsen (France)

- Roche Holding AG (Switzerland)

- GlaxoSmithKline (U.K.)

- Allergan (Ireland)

- Merck & Co. (U.S.)

- Johnson & Johnson (U.S.)

- Novo Nordisk (Denmark)

- Pfizer (U.S.)

- Sanofi (France)

- Endo International (Ireland)

- C.R. Bard (U.S.)

- Elan Corporation (Ireland)

Latest Developments in Global Implantable Drug Delivery Market

- In October 2022, Medtronic launched the Onyx Frontier drug‑eluting stent after receiving CE Mark approval, introducing an advanced implantable drug delivery system for cardiovascular applications with improved performance and clinical data support, reflecting innovation in drug‑eluting implantable devices

- In January 2025, ILUVIEN (fluocinolone acetonide intravitreal implant) received an expanded U.S. FDA label approval for the treatment of chronic non‑infectious uveitis affecting the posterior segment of the eye (NIU‑PS), representing a significant regulatory development for long‑acting implantable drug delivery products

- In March 2025, Encelto (revakinagene taroretcel) — an intravitreal implant gene therapy — was approved for medical use in the United States, providing a surgically implanted cell‑based approach to treat macular telangiectasia type 2, and reflecting the expanding clinical use of implantable drug delivery platforms for ophthalmologic conditions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.