Global Implantable Pulse Generators Market

Market Size in USD Billion

USD

5.39 Billion

USD

11.39 Billion

2025

2033

USD

5.39 Billion

USD

11.39 Billion

2025

2033

| 2026 - 2033 | |

| USD 5.39 Billion | |

| USD 11.39 Billion | |

| % | |

|

Implantable Pulse Generators Market Size

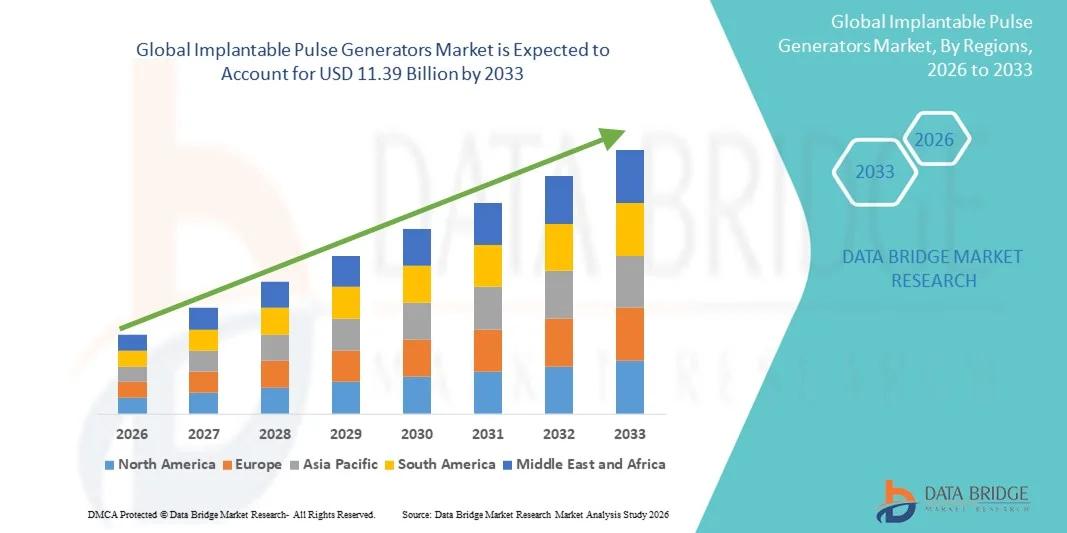

- The global implantable pulse generators market size was valued at USD 5.39 billion in 2025 and is expected to reach USD 11.39 billion by 2033, at a CAGR of 9.81% during the forecast period

- The market growth is largely fueled by the growing prevalence of chronic disorders such as Parkinson’s disease, chronic pain, and epilepsy, coupled with increasing adoption of advanced neuromodulation therapies for effective long-term management

- Furthermore, rising demand for minimally invasive treatment options, continuous technological advancements in implantable devices, and growing healthcare expenditure are accelerating the uptake of Implantable Pulse Generators solutions, thereby significantly boosting the industry's growth

Implantable Pulse Generators Market Analysis

- Implantable pulse generators (IPGs), which deliver electrical stimulation to specific nerves or brain regions, are becoming increasingly vital components in modern neuromodulation therapies due to their precision, programmability, and compatibility with minimally invasive surgical techniques

- The escalating demand for implantable pulse generators is primarily driven by the rising prevalence of chronic neurological and pain-related disorders, increasing geriatric population, and continuous advancements in battery technology and device miniaturization

- North America dominated the implantable pulse generators market with the largest revenue share of 41.6% in 2025, characterized by advanced healthcare infrastructure, strong presence of key medical device manufacturers, and growing adoption of neuromodulation therapies for conditions such as Parkinson’s disease, chronic pain, and epilepsy. The U.S. market is witnessing significant growth, supported by favorable reimbursement policies, increasing R&D investments, and expanding clinical applications of IPGs

- Asia-Pacific is expected to be the fastest-growing region in the implantable pulse generators market during the forecast period, registering a robust CAGR driven by increasing healthcare expenditure, improving access to advanced medical technologies, and growing patient awareness in countries such as China, Japan, and India

- The Cardiovascular Diseases segment accounted for the largest market share of 46.5% in 2025, driven by the escalating global incidence of heart failure, arrhythmias, and ischemic heart disease

Report Scope and Implantable Pulse Generators Market Segmentation

|

Attributes |

Implantable Pulse Generators Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Implantable Pulse Generators Market Trends

Rising Advancements in Miniaturization and Battery Efficiency

- A significant and accelerating trend in the global implantable pulse generators market is the continuous advancement in miniaturization and energy-efficient designs. Manufacturers are developing smaller, more powerful devices that can deliver precise stimulation with longer battery life, improving patient comfort and reducing the frequency of replacement surgeries

- For instance, in May 2024, Medtronic introduced a next-generation rechargeable implantable pulse generator with an extended battery life of nearly 15 years, aimed at improving patient experience and reducing surgical intervention frequency. This innovation reflects the industry’s focus on long-term performance and patient-centric design

- The demand for compact, durable, and highly efficient IPGs is increasing across applications such as deep brain stimulation (DBS), spinal cord stimulation (SCS), and cardiac rhythm management. These devices not only enhance therapy precision but also offer significant improvements in wireless programming and recharging convenience

- The integration of adaptive stimulation algorithms and real-time feedback technology is revolutionizing neuromodulation therapy, allowing devices to adjust automatically to physiological changes. These enhancements significantly improve treatment outcomes and quality of life for patients suffering from chronic pain, epilepsy, Parkinson’s disease, and heart rhythm disorders

- Manufacturers are investing heavily in developing biocompatible materials and novel power solutions, such as wireless recharging and energy harvesting technologies, to extend device longevity and minimize invasiveness. Such developments are setting new standards in implantable device engineering

- This trend toward intelligent, compact, and energy-optimized IPGs is transforming the therapeutic landscape by making neuromodulation and cardiac stimulation therapies more accessible, efficient, and comfortable for patients globally

Implantable Pulse Generators Market Dynamics

Driver

Growing Prevalence of Chronic Diseases and Expanding Neuromodulation Applications

- The rising incidence of neurological and cardiovascular disorders, coupled with the expanding use of neuromodulation therapy, is a primary driver fueling the global Implantable Pulse Generators market. As chronic conditions like Parkinson’s disease, chronic pain, and epilepsy become more prevalent, the demand for advanced IPG systems continues to accelerate

- For instance, in April 2025, Abbott announced the launch of its new Proclaim Plus neurostimulation system for pain management, featuring continuous therapy adaptability to help patients achieve long-term relief with fewer manual adjustments. Such innovations highlight the growing clinical relevance of neuromodulation technologies

- The increasing global geriatric population and the rising preference for minimally invasive treatments are further boosting the adoption of implantable pulse generators. These devices enable precise stimulation of target nerves, offering effective symptom control with reduced surgical risks and shorter recovery times

- Furthermore, growing awareness among healthcare professionals about the therapeutic benefits of electrical stimulation is encouraging the expansion of IPG applications beyond traditional domains, including bladder control, migraine management, and gastrointestinal regulation

- Technological advancements such as wireless communication, improved electrode designs, and software-based therapy customization have enhanced device usability and patient compliance. These developments are fostering broader acceptance of IPG therapy in clinical practice

- The global demand for IPGs is expected to witness substantial growth over the next decade as healthcare systems increasingly adopt advanced neuromodulation solutions to manage chronic, treatment-resistant conditions efficiently

Restraint/Challenge

High Cost of Devices and Reimbursement Limitations

- The high initial cost of implantable pulse generators, coupled with limited reimbursement coverage in several emerging markets, remains a major restraint to widespread adoption. The cost includes not only the device but also the surgical implantation procedure and ongoing maintenance

- For instance, in several developing countries, reimbursement frameworks for neurostimulation therapies remain underdeveloped, discouraging both patients and hospitals from adopting such advanced treatment options despite their proven clinical benefits

- The complexity of approval and reimbursement processes for implantable devices adds to the challenge, as manufacturers must navigate multiple regulatory environments and pricing pressures across regions. This often results in delayed product launches and restricted patient access

- Furthermore, device replacement due to battery depletion or mechanical malfunction contributes additional costs to patients and healthcare systems. Although rechargeable and long-lasting models have mitigated this issue, affordability remains a significant concern, particularly in low- and middle-income economies

- The shortage of skilled surgeons trained in neurostimulation procedures and the requirement for advanced infrastructure also limit the penetration of IPG therapies in certain regions. Addressing these gaps through specialized training programs and improved healthcare funding is essential for market expansion

- To overcome these challenges, leading manufacturers are focusing on cost-optimized production, reimbursement partnerships, and educational initiatives to enhance physician awareness and expand treatment accessibility across different income segments

Implantable Pulse Generators Market Scope

The market is segmented on the basis of product type, application, and end-user.

- By Product Type

On the basis of product type, the Implantable Pulse Generators market is segmented into Implantable Cardiac Pacemakers, Implantable Defibrillators, Cochlear Implants, Implantable Nerve Stimulators (FES), Implantable Infusion Pumps, and Implantable Active Monitoring Devices. The Implantable Cardiac Pacemakers segment dominated the market with the largest revenue share of 37.6% in 2025, owing to the rising prevalence of cardiac arrhythmias and bradycardia among the elderly population. Technological advancements, including MRI-compatible and wireless telemetry-enabled pacemakers, have increased clinical acceptance. Their reliability, long battery life, and improved remote monitoring capabilities have also strengthened their dominance. In addition, strong healthcare infrastructure in developed regions and supportive reimbursement frameworks have accelerated adoption. Increasing awareness about early cardiac rhythm management and the growing burden of cardiovascular diseases globally continue to sustain demand for advanced cardiac pacemakers.

The Implantable Nerve Stimulators (FES) segment is expected to register the fastest CAGR of 13.8% from 2026 to 2033, fueled by growing applications in pain management, spinal cord stimulation, and treatment of neurological disorders such as Parkinson’s disease and epilepsy. These devices deliver targeted stimulation to nerves, improving mobility and reducing pain. The introduction of miniaturized, rechargeable, and adaptive FES devices is further driving their popularity. Rising investments in neurostimulation research and increasing physician awareness regarding functional restoration therapies are expected to propel growth. Their expanding use in both clinical and home care environments is positioning this segment as a major growth driver in the coming years.

- By Application

On the basis of application, the Implantable Pulse Generators market is segmented into Neurovascular Diseases, Cardiovascular Diseases, and Orthopedic Applications. The Cardiovascular Diseases segment accounted for the largest market share of 46.5% in 2025, driven by the escalating global incidence of heart failure, arrhythmias, and ischemic heart disease. Implantable devices such as pacemakers and defibrillators are now essential components of modern cardiac care, offering life-saving interventions and real-time monitoring capabilities. Advancements in telemetry, remote diagnostics, and biocompatible materials have improved patient outcomes. In addition, growing government initiatives promoting early detection and management of cardiac conditions are boosting device adoption. The availability of compact, long-lasting, and easy-to-implant pulse generators has further solidified this segment’s leadership in the global market.

The Neurovascular Diseases segment is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, owing to increasing utilization of neurostimulation therapies for epilepsy, chronic pain, depression, and movement disorders. Rapid progress in neuromodulation science, coupled with favorable clinical outcomes, is driving adoption. The emergence of closed-loop stimulation technologies and brain-responsive IPGs is improving therapeutic precision. Moreover, growing awareness of alternative non-pharmacological treatments and supportive reimbursement policies in developed markets are fueling demand. The rising prevalence of neurological disorders and the development of minimally invasive implantation techniques are expected to maintain strong momentum in this segment over the forecast period.

- By End User

On the basis of end user, the Implantable Pulse Generators market is segmented into Hospitals, Ambulatory Surgical Centers, Home Care Settings, and Clinics. The Hospitals segment dominated the market with the largest share of 55.8% in 2025, driven by the high volume of implant procedures performed in hospital settings due to availability of advanced surgical infrastructure and skilled professionals. Hospitals remain the primary sites for cardiac and neurological implant surgeries owing to their access to specialized diagnostic and post-operative monitoring facilities. Continuous patient follow-ups, immediate emergency support, and comprehensive post-implant care reinforce hospital dominance. In addition, government-funded hospital programs and strong reimbursement coverage for complex implantation procedures are further contributing to their leading position in the global market.

The Ambulatory Surgical Centers (ASCs) segment is projected to record the fastest CAGR of 14.1% from 2026 to 2033, propelled by the increasing shift toward cost-effective and outpatient-based implant procedures. ASCs offer shorter recovery times, lower infection risks, and reduced overall costs compared to traditional hospital surgeries. Rising technological integration, such as minimally invasive IPG implantation and wireless postoperative monitoring, enhances patient safety and operational efficiency. Furthermore, supportive policies promoting same-day discharge and patient comfort are attracting both patients and physicians toward ASC-based interventions. Growing investments in expanding ASC infrastructure worldwide are expected to strengthen this segment’s rapid growth trajectory in the years ahead.

Implantable Pulse Generators Market Regional Analysis

- North America dominated the implantable pulse generators market with the largest revenue share of 41.6% in 2025

- Characterized by advanced healthcare infrastructure, strong presence of key medical device manufacturers, and growing adoption of neuromodulation therapies for conditions such as Parkinson’s disease, chronic pain, and epilepsy

- The region’s dominance is further strengthened by favorable reimbursement frameworks, robust clinical research programs, and increasing demand for miniaturized, rechargeable devices that improve patient comfort and treatment outcomes.

U.S. Implantable Pulse Generators Market Insight

The U.S. implantable pulse generators market captured the largest revenue share in 2025 within North America, supported by strong R&D initiatives, rising prevalence of neurological disorders, and a high rate of technology adoption in healthcare systems. The country benefits from favorable reimbursement structures, a growing elderly population, and the availability of advanced implantable devices from major players such as Medtronic, Abbott, and Boston Scientific. Increasing utilization of implantable neurostimulators for pain and movement disorder management continues to drive the market’s expansion.

Europe Implantable Pulse Generators Market Insight

The Europe implantable pulse generators market is projected to expand at a significant CAGR during the forecast period, driven by increasing incidence of chronic diseases, government support for medical innovation, and strong demand for minimally invasive therapies. European countries are witnessing a steady rise in neurostimulation and cardiac pacing procedures, especially across Germany, the U.K., and France. The region’s focus on patient safety, regulatory compliance, and clinical efficacy continues to promote market growth, supported by technological integration in healthcare systems.

U.K. Implantable Pulse Generators Market Insight

The U.K. implantable pulse generators market is anticipated to grow at a notable CAGR during the forecast period, driven by rising prevalence of cardiovascular and neurological conditions, growing investments in healthcare infrastructure, and adoption of advanced implantable medical devices. Increased patient preference for personalized therapies and government support for digital health initiatives are further enhancing market penetration.

Germany Implantable Pulse Generators Market Insight

The Germany implantable pulse generators market is expected to witness steady growth, driven by strong clinical research programs, a well-established healthcare system, and a high adoption rate of innovative implantable technologies. German manufacturers and hospitals are increasingly focusing on developing and using MRI-compatible and rechargeable pulse generators for long-term neurological care.

Asia-Pacific Implantable Pulse Generators Market Insight

The Asia-Pacific implantable pulse generators market is poised to grow at the fastest CAGR during 2026–2033, driven by increasing healthcare expenditure, improving access to advanced neuromodulation therapies, and rising prevalence of chronic pain and neurological disorders. Countries such as China, Japan, and India are leading regional growth, supported by government healthcare reforms, rapid medical device manufacturing advancements, and growing awareness of implantable therapeutic options.

Japan Implantable Pulse Generators Market Insight

The Japan implantable pulse generators market is gaining momentum due to the country’s advanced healthcare infrastructure, strong research base, and growing elderly population. Japan’s emphasis on precision medicine and the integration of digital monitoring systems with implantable pulse generators are key growth drivers. Increasing prevalence of neurodegenerative and cardiac conditions continues to stimulate demand for innovative IPG devices.

China Implantable Pulse Generators Market Insight

The China implantable pulse generators market accounted for the largest revenue share in the Asia-Pacific region in 2025, attributed to growing government investment in healthcare modernization, expanding manufacturing capabilities, and a large patient base requiring cardiac and neurological implants. The increasing presence of domestic manufacturers and collaborations with global medtech leaders are further propelling market expansion in China.

Implantable Pulse Generators Market Share

The Implantable Pulse Generators industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Abbott (U.S.)

- Boston Scientific Corporation (U.S.)

- LivaNova PLC (U.K.)

- Biotronik SE & Co. KG (Germany)

- Nevro Corp. (U.S.)

- Synapse Biomedical Inc. (U.S.)

- NeuroPace, Inc. (U.S.)

- SynCardia Systems, LLC (U.S.)

- Cochlear Limited (Australia)

- Austin Medical, Inc. (U.S.)

- Stimwave Technologies (U.S.)

- Greatbatch Medical (U.S.)

- Axonics, Inc. (U.S.)

- NevroMedix GmbH (Germany)

Latest Developments in Global Implantable Pulse Generators Market

- In October 2022, Nevro Corp. received U.S. FDA approval for the Senza® HFX iQ™ Spinal Cord Stimulation (SCS) system, designed to use artificial intelligence for personalized chronic pain management. This new generation IPG continuously learns and adapts stimulation settings based on patient feedback, marking a key advancement in intelligent neuromodulation therapies

- In December 2022, Abbott Laboratories launched Eterna, one of the world’s smallest rechargeable spinal cord stimulation systems, offering extended therapy duration and improved patient comfort. The innovation focused on miniaturization and longer intervals between charges, reinforcing Abbott’s leadership in advanced implantable neurostimulation devices

- In August 2023, Medtronic plc obtained CE Mark approval for its Inceptiv™ Closed-Loop Spinal Cord Stimulator, the company’s first closed-loop SCS system in Europe. The device uses real-time sensing technology to automatically adjust stimulation based on patient physiology, representing a breakthrough in patient-specific pain therapy management

- In January 2024, Medtronic plc received U.S. FDA approval for its Percept™ RC Deep Brain Stimulation (DBS) system, the first rechargeable neurostimulator with BrainSense™ technology that records brain signals while delivering therapy. This development enhances precision treatment for neurological disorders such as Parkinson’s disease and essential tremor, strengthening Medtronic’s innovation in implantable pulse generators

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.