Global Indirect Debris Removal Market

Market Size in USD Million

USD

48.77 Million

USD

238.43 Million

2024

2032

USD

48.77 Million

USD

238.43 Million

2024

2032

| 2025 - 2032 | |

| USD 48.77 Million | |

| USD 238.43 Million | |

| % | |

|

Indirect Debris Removal Market Size

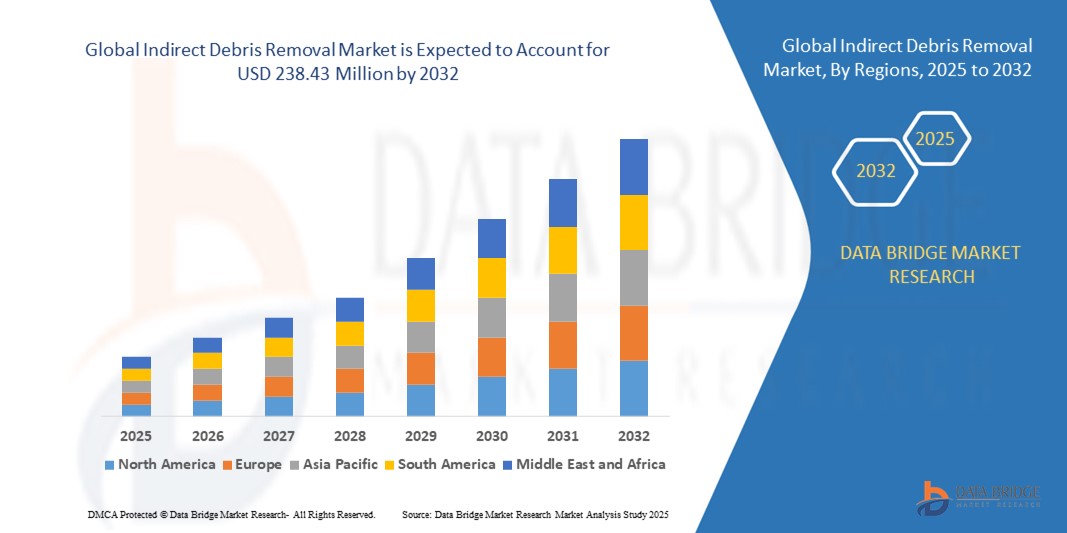

- The global indirect debris removal market size was valued at USD 48.77 million in 2024 and is expected to reach USD 238.43 million by 2032, at a CAGR of 21.94% during the forecast period

- The market growth is largely fuelled by the increasing need for space sustainability and collision risk mitigation as satellite launches and space exploration activities accelerate globally

- Growing investments by government agencies and private space companies in orbital debris tracking, removal, and recycling technologies are further boosting market demand

Indirect Debris Removal Market Analysis

- The market is witnessing rapid technological advancements such as robotic arms, tether systems, and laser-based debris removal methods, enabling safe and cost-effective orbital cleanup operations

- Strategic partnerships between aerospace organizations, defense agencies, and commercial space operators are creating new opportunities for large-scale debris removal missions and regulatory framework development

- North America dominated the indirect debris removal market with the largest revenue share in 2024, driven by increasing satellite launches, advanced aerospace infrastructure, and growing investments in space sustainability programs

- Asia-Pacific region is expected to witness the highest growth rate in the global indirect debris removal market, driven by rapid satellite deployment, rising investments in space research, and strong policy frameworks promoting space sustainability

- The LEO segment held the largest market revenue share in 2024, driven by the rapid growth in satellite constellations and the high density of debris concentrated in low Earth orbit. LEO-based missions require robust debris mitigation solutions due to increased collision risks with operational satellites and future launch plans

Report Scope and Indirect Debris Removal Market Segmentation

|

Attributes |

Indirect Debris Removal Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Growing Demand For Sustainable Space Operations |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Indirect Debris Removal Market Trends

Technological Advancements in Space Debris Mitigation

• The growing focus on sustainable space exploration is driving the adoption of indirect debris removal technologies designed to prevent collision risks in orbit. With satellite deployments rising sharply, indirect systems help reduce space clutter while enabling the long-term safety of space operations, ensuring that future missions can operate without interference from uncontrolled debris

• Demand for non-contact debris mitigation solutions such as laser-based systems and ion-beam shepherd technologies is increasing due to their precision and ability to handle smaller fragments that pose high operational risks to spacecraft. These systems can target high-velocity particles that are difficult to track, reducing the probability of catastrophic collisions in low Earth orbit

• Cost-efficient debris mitigation frameworks, supported by public-private partnerships, are accelerating research into scalable, automated solutions to prevent the formation of new debris clouds in low Earth orbit (LEO). Such collaborations are enabling cross-border funding initiatives, lowering entry barriers for startups, and integrating sustainability goals into space policy discussions

• For instance, in 2023, several aerospace agencies in Europe initiated collaborative programs to integrate indirect debris removal technologies into upcoming satellite constellations to minimize future collision threats. These programs included simulation-based testing, shared data analytics platforms, and funding mechanisms to fast-track early adoption by commercial operators

• While innovation in debris prevention is advancing, long-term adoption depends on standardized global regulations, financial incentives, and continued investment in early-stage space sustainability projects. Policymakers and industry leaders are now focusing on risk-sharing frameworks to encourage long-term commercial participation in debris mitigation activities

Indirect Debris Removal Market Dynamics

Driver

Rising Satellite Launches and Growing Concern Over Orbital Safety

• The rapid expansion of satellite constellations for communication, navigation, and Earth observation is increasing congestion in low Earth orbit, fueling demand for indirect debris removal technologies to reduce collision risks. With mega-constellations such as Starlink and OneWeb expanding rapidly, the potential for collision-induced debris events has grown exponentially

• Space agencies and private operators are prioritizing debris mitigation as a key component of mission planning to protect valuable assets and ensure the sustainability of outer space operations. This is leading to more frequent collaborations between government bodies, aerospace companies, and insurers to develop risk-reduction protocols and certification standards

• International collaborations between space-faring nations are encouraging the development of shared guidelines for debris monitoring and preventive technologies. Such initiatives are paving the way for unified debris-tracking systems and real-time collision prediction models across multiple space agencies worldwide

• For instance, in 2022, the European Space Agency (ESA) announced funding for next-generation debris monitoring systems to improve early detection and removal strategies for orbital debris. This program introduced AI-driven orbital tracking algorithms capable of predicting debris trajectories with far greater accuracy than existing systems

• While rising awareness supports growth, the market still requires cost-effective, automated solutions that can be scaled for frequent satellite launches. This includes designing modular, reusable systems that can be easily integrated into satellites at the manufacturing stage, reducing operational costs over time

Restraint/Challenge

High Implementation Costs and Regulatory Uncertainty

• The deployment of indirect debris removal systems involves significant upfront investment in research, engineering, and testing, limiting adoption among smaller commercial satellite operators. Many emerging companies struggle to meet these financial requirements, slowing the pace of innovation across the industry

• Lack of standardized international regulations and unclear liability frameworks make it challenging for private players to justify long-term investments in debris mitigation infrastructure. Without clear global policies, operators face legal uncertainties regarding responsibility in case of accidental damage during debris removal missions

• Technological complexity and the absence of proven large-scale demonstrations further delay commercial adoption and funding opportunities in emerging markets. This results in a lack of investor confidence and limited access to private capital for early-stage debris removal technology developers

• For instance, in 2023, multiple space startups in Asia postponed planned debris mitigation projects due to high operational costs and limited regulatory support for debris removal missions. Delays in government funding approvals and a lack of standardized testing protocols further hampered project timelines

• To address these challenges, stakeholders must collaborate on cost-sharing models, technology demonstrators, and clear global policies to encourage private-sector participation in space sustainability initiatives. A unified international framework would help accelerate commercial adoption and build investor confidence

Indirect Debris Removal Market Scope

The market is segmented on the basis of orbit, debris size, and technique.

- By Orbit

On the basis of orbit, the indirect debris removal market is segmented into LEO, MEO, and GEO. The LEO segment held the largest market revenue share in 2024, driven by the rapid growth in satellite constellations and the high density of debris concentrated in low Earth orbit. LEO-based missions require robust debris mitigation solutions due to increased collision risks with operational satellites and future launch plans.

The MEO segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the rising adoption of navigation and communication satellites in this orbital range. Indirect debris removal solutions in MEO are gaining attention as satellite deployments increase, necessitating sustainable orbital management practices.

- By Debris Size

On the basis of debris size, the indirect debris removal market is segmented into 1mm to 10mm, 10mm to 100mm, and Greater than 100mm. The 1mm to 10mm segment held the largest market revenue share in 2024, as smaller debris particles are the most difficult to track and pose significant collision risks at orbital speeds. Advanced detection and indirect removal technologies are increasingly focused on this segment to ensure space safety.

The 10mm to 100mm segment is expected to witness the fastest growth rate from 2025 to 2032, driven by the rising threat of medium-sized debris capable of causing severe damage to spacecraft. Indirect mitigation technologies targeting this range are gaining investment support due to the operational importance of protecting high-value space assets.

- By Technique

On the basis of technique, the indirect debris removal market is segmented into Drag Sail, Electrodynamic Tether, and Other Indirect Debris Removal Techniques. The Drag Sail segment held the largest market revenue share in 2024, driven by its ability to passively deorbit satellites at end-of-life while offering a cost-effective solution for low Earth orbit missions. Its simplicity and scalability make it a preferred option for satellite operators.

The Electrodynamic Tether segment is expected to witness the fastest growth rate from 2025 to 2032, fueled by its potential for continuous deorbiting without propellant use, reducing long-term mission costs. Ongoing research programs are accelerating its adoption for both commercial and defense-related space missions.

Indirect Debris Removal Market Regional Analysis

• North America dominated the indirect debris removal market with the largest revenue share in 2024, driven by increasing satellite launches, advanced aerospace infrastructure, and growing investments in space sustainability programs.

• The region’s strong presence of private space companies, combined with government-led debris mitigation policies, is accelerating the adoption of indirect debris removal technologies.

• The rising concern for orbital safety, coupled with NASA’s ongoing research collaborations, is boosting demand for preventive debris removal systems in both commercial and defense applications.

U.S. Indirect Debris Removal Market Insight

The U.S. indirect debris removal market captured the largest revenue share within North America in 2024, supported by the rapid growth of satellite constellations, private sector innovation, and robust funding for orbital safety programs. Increasing collaboration between NASA, private aerospace firms, and academic institutions is fostering the development of scalable, automated debris mitigation systems. Furthermore, the country’s leadership in space policy and its emphasis on sustainable exploration missions are accelerating technology deployment.

Europe Indirect Debris Removal Market Insight

The Europe indirect debris removal market is expected to witness the fastest growth rate from 2025 to 2032, driven by rising investments from the European Space Agency (ESA) and the region’s commitment to international space sustainability agreements. European aerospace firms are actively participating in collaborative debris mitigation missions, aiming to integrate advanced non-contact technologies into satellite constellations. In addition, strict regulations on space safety and orbital debris monitoring are strengthening adoption across both commercial and governmental missions.

U.K. Indirect Debris Removal Market Insight

The U.K. indirect debris removal market is expected to witness the fastest growth rate from 2025 to 2032, fueled by government-backed space innovation programs and a rising number of private aerospace startups. The country’s focus on research and development, combined with initiatives promoting commercial satellite safety, is accelerating demand for indirect debris removal solutions. The U.K.’s participation in international debris mitigation collaborations further supports market expansion.

Germany Indirect Debris Removal Market Insight

The Germany indirect debris removal market is expected to witness the fastest growth rate from 2025 to 2032, supported by the country’s strong aerospace infrastructure and commitment to sustainable space exploration. German research institutes and private companies are investing heavily in advanced debris prevention technologies such as laser-based systems and drag sails. In addition, the country’s emphasis on engineering innovation and participation in ESA-led debris mitigation missions are driving technological advancements in the sector.

Asia-Pacific Indirect Debris Removal Market Insight

The Asia-Pacific indirect debris removal market is expected to witness the fastest growth rate from 2025 to 2032, driven by rapid satellite deployment programs in countries such as China, Japan, and India. Increasing government initiatives for space safety, combined with the region’s expanding commercial satellite industry, is accelerating technology adoption. Furthermore, Asia-Pacific’s emergence as a hub for cost-efficient aerospace manufacturing is boosting the availability of affordable debris mitigation solutions.

Japan Indirect Debris Removal Market Insight

The Japan indirect debris removal market is expected to witness the fastest growth rate from 2025 to 2032 due to the country’s leadership in space robotics, orbital research, and innovative debris mitigation missions. Japan’s focus on autonomous space systems, coupled with its commitment to international orbital safety agreements, is accelerating adoption. In addition, collaborative projects between JAXA and private aerospace companies are fostering the development of next-generation indirect debris removal technologies.

China Indirect Debris Removal Market Insight

The China indirect debris removal market accounted for the largest revenue share in the Asia-Pacific region in 2024, driven by rapid satellite network expansions, strong domestic manufacturing capabilities, and government-backed space safety initiatives. China’s ambitious space exploration agenda, combined with its growing commercial satellite sector, is propelling demand for debris mitigation systems. The country’s increasing investment in space sustainability technologies further strengthens its position in the global market.

Indirect Debris Removal Market Share

The Indirect Debris Removal industry is primarily led by well-established companies, including:

- Airbus (France)

- VOYAGER (U.S.)

- Astroscale (Japan)

- ClearSpace (Switzerland)

- D-ORBIT (Italy)

- Electro Optic Systems (Australia)

- Lockheed Martin Corporation (U.S.)

- Northrop Grumman (U.S.)

- Obruta Space Solutions Corp. (Canada)

- OrbitGuardians (U.S.)

- Aldoria (France)

- Surrey Satellite Technology Ltd (UK)

- Kall Morris Inc (U.S.)

Latest Developments in Global Indirect Debris Removal Market

- In February 2024, Astroscale Holdings, a Japanese startup, deployed a satellite to inspect a discarded rocket component in orbit, marking a major advancement in space debris management. Operating 600 kilometers above Earth, this initiative introduces the first technology designed for in-orbit debris assessment, enabling safer future removal missions and strengthening global space sustainability efforts

- In February 2024, Rocket Lab successfully launched the Astroscale Orbital Debris Removal Satellite Complex 1 from New Zealand, featuring the ADRAS-J module. Equipped with advanced inspection cameras, this system is engineered to maneuver around targeted rocket stages, providing critical data for orbital debris mitigation and supporting the development of efficient removal solutions

- In April 2024, Astroscale achieved a historic milestone by capturing the first-ever image of space debris through Rendezvous and Proximity Operations (RPO) using its ADRAS-J satellite. This breakthrough enhances debris tracking accuracy, promotes early detection, and accelerates the commercialization of space debris removal technologies, driving innovation and market growth in space sustainability

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.