Global Industrial Bulk Packaging Market

Market Size in USD Billion

USD

27.51 Billion

USD

37.07 Billion

2025

2033

USD

27.51 Billion

USD

37.07 Billion

2025

2033

| 2026 - 2033 | |

| USD 27.51 Billion | |

| USD 37.07 Billion | |

| % | |

|

Industrial Bulk Packaging Market Size

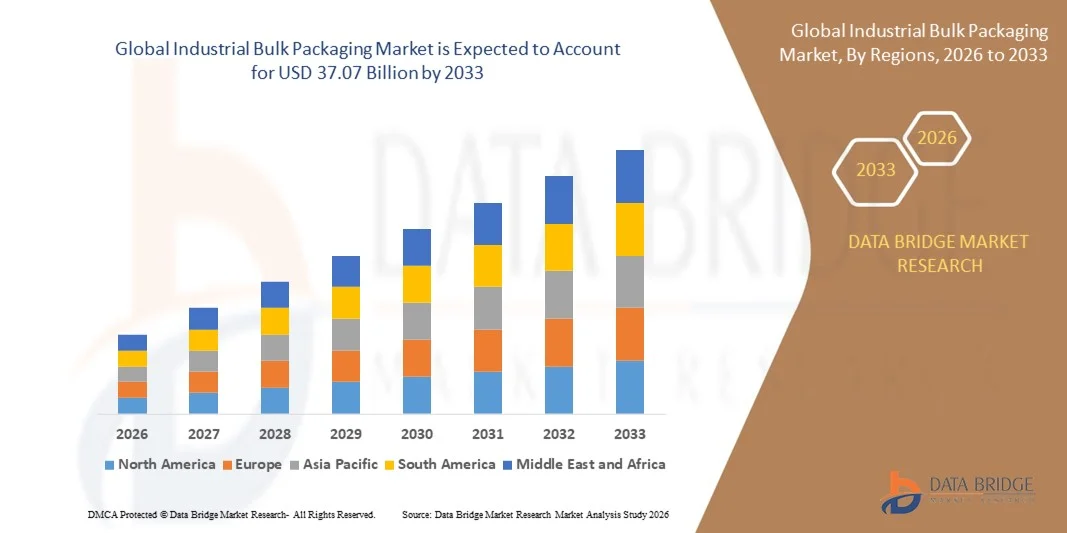

- The global industrial bulk packaging market size was valued at USD 27.51 billion in 2025 and is expected to reach USD 37.07 billion by 2033, at a CAGR of 3.80% during the forecast period

- The market growth is largely fuelled by the rising demand for efficient transportation and storage solutions across industries such as chemicals, food & beverages, and pharmaceuticals

- Increasing global trade and the expansion of manufacturing sectors are further propelling the adoption of durable and reusable bulk packaging materials

Industrial Bulk Packaging Market Analysis

- The industrial bulk packaging market is witnessing steady growth due to the growing preference for sustainable packaging solutions that minimize waste and optimize logistics efficiency

- The adoption of flexible intermediate bulk containers (FIBCs) and rigid bulk containers is increasing, driven by their cost-effectiveness, versatility, and ability to handle large volumes of materials safely and efficiently

- North America dominated the industrial bulk packaging market with the largest revenue share of 38.72% in 2025, driven by the strong presence of established chemical, food, and pharmaceutical industries that demand efficient and sustainable packaging solutions

- Asia-Pacific region is expected to witness the highest growth rate in the global industrial bulk packaging market, driven by expanding trade activities, increasing demand for flexible and cost-efficient packaging, and supportive government initiatives promoting industrial development

- The drums segment held the largest market revenue share in 2025, driven by their widespread use across chemical, oil & gas, and food industries for the safe transportation and storage of liquids and semi-solids. Their robust design, reusability, and compatibility with hazardous materials make them a preferred choice for industrial users seeking durability and compliance with international safety standards

Report Scope and Industrial Bulk Packaging Market Segmentation

|

Attributes |

Industrial Bulk Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Industrial Bulk Packaging Market Trends

Rising Focus on Sustainable and Eco-Friendly Packaging Solutions

- The global shift toward sustainability is reshaping the industrial bulk packaging landscape, with manufacturers increasingly adopting recyclable, reusable, and biodegradable materials. Companies are transitioning from traditional plastics to eco-friendly polymers and fiber-based packaging to reduce environmental impact and comply with regulatory mandates. This trend is also driven by growing consumer and industrial demand for greener supply chains, with industries emphasizing transparency and lifecycle impact reduction across production and logistics stages

- The adoption of circular economy principles is encouraging the use of returnable and refillable bulk containers such as intermediate bulk containers (IBCs) and drums. These solutions help reduce waste generation and carbon emissions while optimizing logistics efficiency. The movement toward sustainability is further supported by corporate ESG goals and government policies promoting green packaging initiatives, ensuring long-term savings and brand value enhancement for industrial players

- For instance, in 2024, several chemical and food processing industries in Europe replaced single-use containers with reusable IBC systems, significantly cutting waste disposal costs and improving sustainability metrics. Such efforts are expected to set benchmarks for other regions to follow in industrial packaging optimization. The adoption of such systems also improves operational efficiency and enables compliance with emerging environmental certification standards

- The use of post-consumer recycled (PCR) resins in bulk packaging production is gaining traction, with manufacturers investing in advanced recycling technologies to enhance material quality. This not only reduces dependence on virgin materials but also aligns with global carbon reduction targets and brand sustainability commitments. Moreover, the integration of chemical recycling and closed-loop recovery processes ensures higher-grade material output suitable for industrial use

- While the sustainability trend is accelerating, challenges remain in ensuring consistent quality, cost-efficiency, and global scalability of eco-friendly materials. Collaboration between raw material suppliers, manufacturers, and regulatory bodies will be critical to sustaining long-term market transformation. Overcoming technological and infrastructural gaps will further determine the pace at which sustainable packaging becomes mainstream

Industrial Bulk Packaging Market Dynamics

Driver

Growth in Chemical and Food & Beverage Industries

- The expansion of the chemical and food & beverage industries is a primary driver of the industrial bulk packaging market. These sectors rely heavily on durable and secure packaging solutions such as drums, IBCs, and flexitanks for storage and transportation of liquids, powders, and semi-solids. The need to maintain product integrity and prevent contamination further fuels demand for specialized bulk packaging, ensuring compliance with global transport and safety standards

- Rising industrialization, particularly in emerging economies, has resulted in higher consumption of chemicals, lubricants, and food-grade products, which depend on efficient bulk handling systems. Packaging providers are increasingly developing customized solutions to meet industry-specific requirements and safety standards. The rising demand from export-oriented industries has also strengthened the need for cost-effective and compliant packaging formats

- The growing global trade of chemical intermediates, edible oils, and beverages has expanded the demand for high-performance packaging that ensures durability and compliance with international transport regulations. This trend is also supported by improvements in supply chain infrastructure and container handling technologies. The integration of smart tracking systems and automated filling solutions further enhances operational reliability and reduces wastage

- For instance, in 2023, several multinational chemical companies upgraded their bulk transport operations with multilayer IBCs to minimize product loss during long-distance shipments, enhancing efficiency and profitability. These innovations not only improved performance but also aligned with sustainability initiatives through reduced material usage and recyclability enhancements

- While chemical and food sectors continue to drive growth, packaging manufacturers must focus on material innovation, design optimization, and automation to keep pace with evolving end-user requirements and sustainability mandates. Continuous R&D investment, coupled with strategic partnerships, will be crucial to maintain market competitiveness in the evolving industrial packaging ecosystem

Restraint/Challenge

Volatility in Raw Material Prices and Environmental Regulations

- The fluctuating prices of raw materials such as plastic resins, steel, and aluminum significantly impact the production cost of industrial bulk packaging. These cost variations challenge manufacturers in maintaining price competitiveness and profitability, particularly in markets with low-margin operations. Price instability also affects long-term supply contracts and investment planning, creating uncertainty in procurement and budgeting processes

- Stringent environmental regulations concerning plastic waste management and emissions are compelling manufacturers to modify production processes and adopt sustainable alternatives. Compliance with regional and international packaging standards often requires high investment in new machinery and research, increasing operational costs. The growing regulatory emphasis on recyclability and producer responsibility adds further complexity to manufacturing operations

- The limited availability of recycled materials and the complexity of sourcing sustainable feedstock further restrict the scalability of eco-friendly packaging solutions. This creates a gap between growing sustainability goals and real-world implementation capacity. Manufacturers are therefore exploring partnerships with recyclers and investing in material recovery facilities to secure consistent raw material supplies

- For instance, in 2024, packaging producers in North America reported a 20% increase in production costs due to rising resin prices and new compliance requirements related to extended producer responsibility (EPR) laws. The resulting cost pressure is prompting a reevaluation of production efficiency, material substitution, and regional sourcing strategies to mitigate volatility risks

- Although raw material volatility and regulatory pressures present challenges, they are also driving innovation toward material efficiency, alternative polymers, and closed-loop packaging systems that could redefine the market’s long-term sustainability and cost dynamics. Companies adopting adaptive strategies, such as hybrid material usage and modular designs, are expected to gain a competitive advantage in this evolving environment

Industrial Bulk Packaging Market Scope

The industrial bulk packaging market is segmented on the basis of product, application, and material

- By Product

On the basis of product, the industrial bulk packaging market is segmented into drums, IBC, pails, totes/cracks, and others. The drums segment held the largest market revenue share in 2025, driven by their widespread use across chemical, oil & gas, and food industries for the safe transportation and storage of liquids and semi-solids. Their robust design, reusability, and compatibility with hazardous materials make them a preferred choice for industrial users seeking durability and compliance with international safety standards.

The IBC segment is expected to witness the fastest growth rate from 2026 to 2033, fuelled by increasing demand for cost-efficient, reusable, and space-saving packaging solutions. IBCs are gaining traction due to their high capacity, ease of handling, and suitability for both liquid and bulk solid applications. Their adaptability to automation and tracking systems further enhances their efficiency across logistics and supply chain operations.

- By Application

On the basis of application, the industrial bulk packaging market is segmented into chemicals and petrochemicals, food and beverages, pharmaceuticals, and others. The chemicals and petrochemicals segment dominated the market in 2025 owing to the sector’s extensive use of industrial-grade packaging for transporting corrosive, flammable, and high-value materials. The need for leak-proof, compliant, and temperature-resistant containers is driving the adoption of specialized bulk packaging formats in this sector.

The food and beverages segment is projected to witness the fastest growth rate from 2026 to 2033, supported by rising demand for hygienic and contamination-free bulk storage and transportation solutions. The growing export of edible oils, beverages, and processed food products is boosting the adoption of FDA-approved and recyclable bulk containers. Furthermore, increasing emphasis on sustainability and food safety standards is driving innovation in packaging materials within this segment.

- By Material

On the basis of material, the industrial bulk packaging market is segmented into plastic, steel, fiber/paperboard, and other materials. The plastic segment held the largest market revenue share in 2025, driven by its lightweight, corrosion-resistant, and cost-effective properties. Plastic-based packaging is widely used across multiple industries due to its versatility, durability, and compatibility with a variety of products ranging from chemicals to food ingredients.

The fiber/paperboard segment is expected to register the fastest growth rate from 2026 to 2033, propelled by the growing focus on eco-friendly and recyclable packaging materials. The use of fiber-based materials aligns with global sustainability goals and offers a biodegradable alternative to traditional plastic and metal packaging. Advancements in coating and lamination technologies are further enhancing the performance and durability of fiber/paperboard bulk packaging solutions.

Industrial Bulk Packaging Market Regional Analysis

- North America dominated the industrial bulk packaging market with the largest revenue share of 38.72% in 2025, driven by the strong presence of established chemical, food, and pharmaceutical industries that demand efficient and sustainable packaging solutions

- The region’s well-developed logistics and transportation infrastructure, coupled with stringent regulatory standards on product safety and handling, has further strengthened market growth

- Moreover, the increasing focus on recyclable materials and bulk packaging innovations designed to reduce environmental impact supports continued expansion in the North American industrial bulk packaging market

U.S. Industrial Bulk Packaging Market Insight

The U.S. industrial bulk packaging market captured the largest revenue share in 2025 within North America, driven by a robust chemical and petrochemical industry and high consumption of packaged goods. Rising adoption of reusable and sustainable packaging materials is further propelling market growth. Furthermore, strong export activity, coupled with advanced manufacturing capabilities and the presence of major packaging solution providers, contributes to the country's dominance in the global market.

Europe Industrial Bulk Packaging Market Insight

The Europe industrial bulk packaging market is expected to witness steady growth from 2026 to 2033, driven by strict environmental regulations and the rising emphasis on circular economy practices. European manufacturers are adopting eco-friendly materials and reusable containers to comply with sustainability targets. In addition, the food, pharmaceutical, and specialty chemical industries in countries such as Germany, France, and the U.K. are major consumers of bulk packaging, promoting further market expansion across the region.

U.K. Industrial Bulk Packaging Market Insight

The U.K. industrial bulk packaging market is expected to witness significant growth from 2026 to 2033, driven by the rising demand for sustainable packaging in the food and beverage sector and expanding chemical exports. The growing preference for lightweight, durable, and recyclable packaging materials is encouraging manufacturers to innovate and upgrade existing solutions. Furthermore, strong logistics infrastructure and the ongoing shift toward environmentally responsible production are supporting market growth in the U.K.

Germany Industrial Bulk Packaging Market Insight

The Germany industrial bulk packaging market is expected to witness notable growth from 2026 to 2033, propelled by the country’s strong industrial base and stringent safety standards for transporting chemicals and hazardous materials. The growing adoption of smart and reusable packaging solutions aligns with Germany’s commitment to sustainability and efficiency. The presence of leading packaging manufacturers and continuous R&D investments in advanced materials further enhance the country’s market position.

Asia-Pacific Industrial Bulk Packaging Market Insight

The Asia-Pacific industrial bulk packaging market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid industrialization, expanding manufacturing activities, and increasing demand for bulk storage solutions in countries such as China, India, and Japan. The growing food processing, pharmaceutical, and chemical industries in the region are major contributors to this expansion. Furthermore, the availability of cost-effective materials and government initiatives supporting industrial growth are expected to accelerate market development in APAC.

China Industrial Bulk Packaging Market Insight

The China industrial bulk packaging market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large-scale manufacturing base, export-oriented economy, and growing demand for efficient bulk transport systems. China’s robust chemical and food industries heavily rely on industrial bulk packaging for both domestic and international logistics. The presence of major packaging producers and increasing investments in sustainable packaging technologies are further driving the market in China.

Japan Industrial Bulk Packaging Market Insight

The Japan industrial bulk packaging market is expected to witness steady growth from 2026 to 2033, driven by the country’s advanced manufacturing sector and strong emphasis on quality, safety, and sustainability. The demand for high-performance packaging solutions is increasing across industries such as chemicals, food processing, and pharmaceuticals. Furthermore, Japan’s commitment to environmental protection and waste reduction is accelerating the adoption of reusable and recyclable bulk containers, supporting long-term market expansion.

Industrial Bulk Packaging Market Share

The Industrial Bulk Packaging industry is primarily led by well-established companies, including:

• Greif (U.S.)

• Cleveland Steel Container (U.S.)

• Composite Containers, LLC (U.S.)

• Hoover Ferguson Group, Inc. (U.S.)

• International Paper (U.S.)

• BWAY Corporation (U.S.)

• Myers Container (U.S.)

• Time Technoplast Ltd. (India)

• Peninsula Drums (Australia)

• Eagle Manufacturing (U.S.)

• Menasha Corporation (U.S.)

• Berry Global Inc. (U.S.)

• Amcor plc (U.K.)

• Mondi (U.K.)

• WestRock Company (U.S.)

• Schütz GmbH & Co. KGaA (Germany)

• The Cary Company (U.S.)

• TPL Plastech Limited (India)

• DS Smith (U.K.)

• Snyder Industries (U.S.)

Latest Developments in Global Industrial Bulk Packaging Market

- In November 2020, Sonoco introduced a new line of lightweight, recyclable packaging designed specifically for heavyweight products. This development aims to enhance product protection while optimizing storage and transportation efficiency. By reducing material use and improving sustainability, Sonoco’s innovation aligns with the growing industry focus on eco-friendly packaging solutions. The launch is expected to strengthen the company’s market position and influence other manufacturers to adopt sustainable alternatives in industrial bulk packaging

- In April 2020, Greif expanded its intermediate bulk container business in North America through the acquisition of a minority stake in Centurion Container LLC. This strategic move enables Greif to leverage Centurion’s operational network and enhance its product portfolio with advanced container technologies. The partnership not only boosts Centurion’s global visibility but also promotes innovation and scalability in sustainable packaging systems. The acquisition is anticipated to reinforce Greif’s leadership in the industrial packaging market by improving capacity and regional reach

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Industrial Bulk Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Industrial Bulk Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Industrial Bulk Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.