Global Industrial Crane Market

Market Size in USD Billion

USD

51.77 Billion

USD

83.39 Billion

2024

2032

USD

51.77 Billion

USD

83.39 Billion

2024

2032

| 2025 - 2032 | |

| USD 51.77 Billion | |

| USD 83.39 Billion | |

| % | |

|

Industrial Crane Market Size

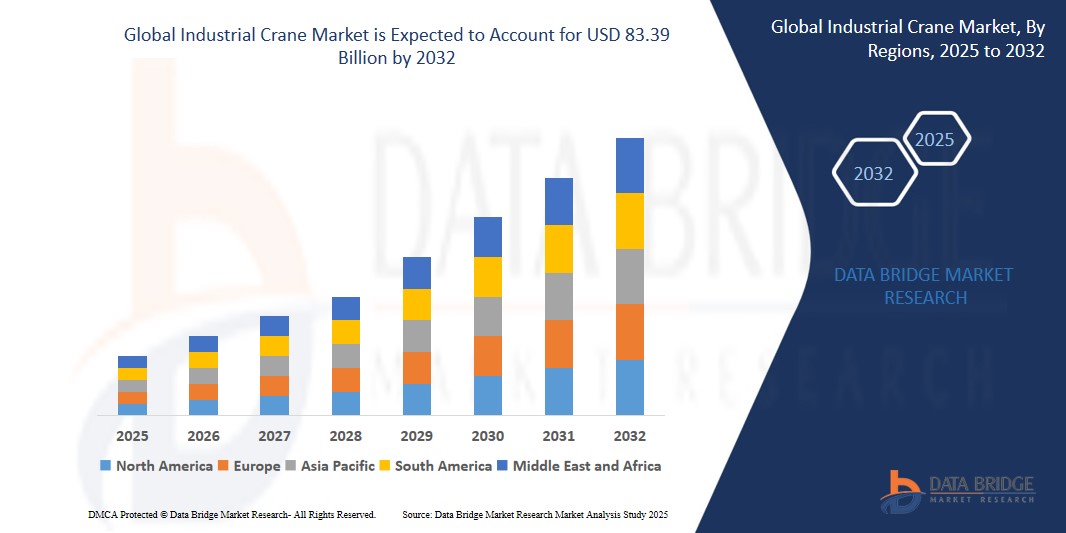

- The Global Industrial Crane Market size was valued at USD 51.77 billion in 2024 and is expected to reach USD 83.39 billion by 2032, at a CAGR of 6.14% during the forecast period

- The market growth is primarily driven by the increasing industrial automation, the expansion of infrastructure projects, and technological advancements in crane control systems. These trends are significantly enhancing operational efficiency and safety, making industrial cranes indispensable across industries such as construction, manufacturing, shipping, and logistics.

- Additionally, the surging demand for energy-efficient and IoT-enabled cranes is transforming the crane landscape, with smart cranes offering real-time monitoring, predictive maintenance, and remote operation features. These innovations are improving uptime, reducing operational costs, and aligning with the global shift towards smart factories and Industry 4.0 initiatives.

Industrial Crane Market Analysis

- Industrial cranes, including overhead cranes, gantry cranes, jib cranes, and tower cranes, are becoming increasingly essential across various sectors such as construction, manufacturing, mining, and logistics. Their role in enhancing material handling efficiency, operational safety, and automated load movement has made them a core component in large-scale industrial operations and infrastructure development projects.

- The escalating demand for industrial cranes is primarily driven by the global trend towards industrial automation, the surge in urbanization and infrastructure projects, and the need for high-capacity lifting equipment that reduces manual labor and enhances productivity. Governments and private sectors are heavily investing in smart factories, transportation infrastructure, renewable energy installations, and shipbuilding, all of which require advanced crane solutions to meet heavy-duty lifting and precision handling needs.

- Asia-Pacific dominates the Industrial Crane Market with the largest revenue share of 38.32% in 2025, driven by rapid industrialization, expansive infrastructure development, and the increasing deployment of cranes in construction, manufacturing, and logistics sectors.

- North America holds the second-largest revenue share in the global Industrial Crane Market, accounting for approximately 28.5% in 2024. The region benefits from a highly developed industrial base, strict workplace safety regulations, and strong demand for high-load handling solutions.

- The double girder cranes segment is projected to dominate the market in 2025 with the largest revenue share, due to their higher load-bearing capacity, suitability for long-span applications, and usage in heavy industrial environments like steel mills, foundries, and power plants. These cranes are preferred in situations demanding precise material handling and maximum hook height.

Report Scope and Industrial Crane Market Segmentation

|

Attributes |

Industrial Crane Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Industrial Crane Market Trends

“Expanding Infrastructure and Industrialization Across Emerging Economies”

- The global industrial crane market is being significantly driven by accelerated infrastructure development and industrial expansion, particularly in developing economies like China, India, Indonesia, Brazil, and several African nations. Rapid urbanization, growth in transportation networks, and industrial policy reforms are increasing demand for advanced material handling systems.

- Governments are prioritizing megaprojects such as smart cities, high-speed rail networks, ports, and manufacturing corridors.

- For instance, India's National Infrastructure Pipeline (NIP), with an investment target of over USD 1.4 trillion by 2030, includes multiple sectors that require cranes for construction, assembly, and logistics.

- Industrial cranes such as gantry, overhead, and jib cranes—are vital to executing these projects efficiently, as they improve productivity, reduce manual labor, and support high-load lifting in harsh conditions.

Industrial Crane Market Dynamics

Driver

“Integration of IoT and Automation in Crane Systems”

- Another significant growth driver is the integration of advanced technologies such as the Internet of Things (IoT), Artificial Intelligence (AI), machine vision, and automation in crane systems. Smart cranes now offer remote monitoring, load optimization, predictive maintenance, and real-time diagnostics. These features improve operational safety, reduce downtime, and optimize energy consumption.

- Companies like Konecranes and Liebherr are investing in the digital transformation of cranes, introducing intelligent control systems that alert operators to overload risks or maintenance requirements.

- For instance, in 2024, Konecranes launched its next-generation “TRUCONNECT Remote Monitoring” system, which enables fleet-wide analytics and proactive service scheduling, drastically improving uptime and reducing unplanned stoppages.

Restraint/Challenge

“High Capital Investment and Skilled Labor Dependency”

- A major restraint for the industrial crane market is the high capital expenditure associated with purchasing and installing cranes. Large cranes especially overhead, gantry, and crawler variants require significant upfront investment, often ranging from thousands to millions of dollars depending on capacity and customization.

- Furthermore, operating advanced crane systems requires skilled technicians and certified operators. The shortage of such labor, especially in developing regions, poses a barrier to adoption.

- In addition, operational costs such as periodic maintenance, inspection compliance, safety training, and insurance also impact the total cost of ownership (TCO), making it less attractive for small and medium enterprises (SMEs) to invest in cranes without external funding or leasing options.

Industrial Crane Market Scope

The market is segmented on the basis of configuration, hoist arrangement, movability, and end-use industries.

- By Configuration

On the basis of configuration, the Industrial Crane Market is segmented into single girder cranes, double girder cranes, gantry cranes, jib cranes, shipyard cranes, stacker cranes, and others. The double girder cranes segment is projected to dominate the market in 2025 with the largest revenue share, due to their higher load-bearing capacity, suitability for long-span applications, and usage in heavy industrial environments like steel mills, foundries, and power plants. These cranes are preferred in situations demanding precise material handling and maximum hook height.

The gantry cranes segment is anticipated to grow at the fastest CAGR from 2025 to 2032, driven by their versatile usage in outdoor applications such as shipyards, container terminals, and large-scale construction sites. Their mobility and ability to operate without building modifications make them ideal for temporary or semi-permanent lifting solutions.

- By Hoist Arrangement

On the basis of hoist arrangement, the market is segmented into top running type and under hung type. The top running hoist arrangement accounted for the largest market share in 2025, owing to its ability to handle heavier loads, greater height clearance, and integration in high-capacity industrial facilities. These systems are commonly deployed in manufacturing, heavy fabrication, and maintenance workshops.

The under hung type hoist is expected to witness steady growth due to its suitability for smaller facilities and lighter loads. Their ease of installation and compatibility with ceiling-mounted tracks make them popular in light manufacturing and warehousing sectors.

- By Movability

On the basis of movability, the Industrial Crane Market is segmented into mobile cranes, fixed cranes, and others. The mobile cranes segment held the largest revenue share in 2025, attributed to their flexibility, ability to be quickly relocated, and wide use in construction, logistics, and utility sectors. These cranes are vital for tasks requiring frequent repositioning and lifting across different site locations.

The fixed cranes segment is projected to grow significantly through 2032, especially in factories, ports, and assembly lines where consistent material handling is needed. Their stability and load precision are key advantages in repetitive industrial operations.

- By End-Use Industry

On the basis of end-use industry, the Industrial Crane Market is segmented into metal production industries, waste management industries, ports and ship terminals, railway, manufacturing industries, construction and infrastructure, petrochemical industries, and other industries. The construction and infrastructure industries segment captured the largest market revenue share in 2025, driven by massive global infrastructure investments, urbanization, and the increasing demand for mechanized lifting solutions at high-rise and large-area construction sites.

The ports and ship terminals segment is anticipated to register the fastest CAGR from 2025 to 2032, due to the rising global trade volume, containerization, and modernization of port facilities. Cranes such as RTGs (rubber-tired gantry) and ship-to-shore cranes are increasingly deployed for efficient cargo handling and automation in logistics.

Industrial Crane Market Regional Analysis

- Asia-Pacific dominates the Industrial Crane Market with the largest revenue share of 38.32% in 2025, driven by rapid industrialization, expansive infrastructure development, and the increasing deployment of cranes in construction, manufacturing, and logistics sectors.

- Governments across the region are investing heavily in megaprojects and smart city initiatives, particularly in China, India, and Southeast Asia, creating robust demand for heavy-duty material handling equipment like industrial cranes.

- The region’s status as a global manufacturing hub further supports the proliferation of advanced crane technologies, including automated and remote-operated systems.

China Industrial Crane Market Insight

China holds the largest share of the Asia-Pacific market, driven by expansive infrastructure projects under the Belt and Road Initiative, robust manufacturing capabilities, and rising investments in automation. The adoption of advanced overhead and gantry cranes in ports, logistics hubs, and smart factories supports continued growth. China's "Made in China 2025" strategy further accelerates high-tech equipment deployment, including cranes in heavy industries.

Japan Industrial Crane Market Insight

Japan’s market benefits from its precision-focused industrial sector and high safety standards. Demand is strong in shipbuilding, automotive, and electronics industries. The country's aging workforce also spurs automation, leading to investments in automated and remote-controlled crane systems. Japan’s innovation in compact cranes for restricted spaces sets it apart.

India Industrial Crane Market Insight

India shows rapid market expansion due to government initiatives like “Make in India” and large-scale infrastructure projects such as Smart Cities and dedicated freight corridors. The booming construction and energy sectors drive the need for tower, mobile, and crawler cranes. The market is further supported by increased FDI and adoption of mechanized material handling.

North America Industrial Crane Market Insight

North America holds the second-largest revenue share in the global Industrial Crane Market, accounting for 29.55% in 2024. The region benefits from a highly developed industrial base, strict workplace safety regulations, and strong demand for high-load handling solutions. Growth is sustained by the integration of smart technologies and automation across oil & gas, manufacturing, and construction industries..

U.S. Industrial Crane Market Insight

The U.S. dominates North America with over 74.56% market share, driven by technological innovation, rapid adoption of automated systems, and continued investment in infrastructure upgrades. The country sees strong demand for overhead and mobile cranes in logistics and energy sectors, especially in shale gas extraction and wind power.

Europe Industrial Crane Market Insight

Europe ranks third with a market share of approximately 21.5% in 2024, characterized by sustainable construction practices, high safety standards, and a push towards smart automation in logistics and industry. Investment in renewable energy and green buildings is prompting crane adoption for wind energy and sustainable infrastructure projects.

Germany Industrial Crane Market Insight

Germany leads Europe with its advanced manufacturing ecosystem and dominance in the automotive sector. The demand for precision handling equipment and integration with Industry 4.0 is strong. Mobile and overhead cranes are widely used in logistics and automation-heavy industries.

U.K Industrial Crane Market Insight

The U.K. market is driven by post-Brexit infrastructure investment and emphasis on construction safety. Smart cranes integrated with IoT for real-time tracking are gaining traction. Growth is also supported by increased maritime activity and urban redevelopment.

Industrial Crane Market Share

The Industrial Crane industry is primarily led by well-established companies, including:

- Konecranes(Finland)

- Sumitomo Heavy Industries Material Handling Systems Co., Ltd.(Japan)

- GORBEL INC.(United States)

- North American Industries(United States)

- ElectroMech(India)

- Terex Corporation(United States)

- Street Crane Company Limited(United Kingdom)

- Kundel Industries(United States)

- American Crane (United States)

- Uesco Cranes(United States)

- Whiting Corporation(United States)

- Asian Cranes & Elevators(India)

- Lampson International LLC(United States)

- Liebherr Group (Switzerland)

- JCB(United Kingdom)

- Manitowoc(United States)

- XCMG Group(China)

- Zoomlion Heavy Industry Science & Technology Co., Ltd. (China)

Latest Developments in Global Industrial Crane Market

- In April 2024, Konecranes, a global leader in the material handling industry, announced the launch of its new E-VER electric overhead crane series. Designed for energy efficiency and smart automation, these cranes feature regenerative drives, remote diagnostics, and integrated digital tools to enhance safety and uptime. This launch reflects Konecranes’ focus on sustainability and Industry 4.0 capabilities, reinforcing its position in the smart lifting solutions market.

- In March 2024, Liebherr Group inaugurated its expanded manufacturing and logistics facility in Rostock, Germany, to meet the rising global demand for heavy-duty maritime and offshore cranes. The expansion includes enhanced testing and assembly areas to support new generations of electric and hybrid crane models, aligning with global decarbonization efforts and next-gen port infrastructure.

- In February 2024, Terex Corporation introduced a next-generation crawler crane with modular boom systems and advanced telematics, aimed at improving flexibility in construction and infrastructure projects. The new model enables seamless adaptation across different terrains and lifting requirements. Terex also announced new partnerships with rental fleet operators to expand regional distribution across Asia-Pacific and Latin America.

- In January 2024, Zoomlion Heavy Industry Science & Technology Co., Ltd. launched its 5G-enabled tower crane in China, capable of remote real-time control, load analytics, and safety diagnostics. Developed as part of the country’s smart construction initiative, the crane improves site efficiency and reduces labor dependency, showcasing China’s leap toward fully digitized construction operations.

- In December 2023, Manitowoc revealed a strategic collaboration with Siemens Digital Industries to incorporate predictive maintenance algorithms and cloud-based performance tracking into its tower cranes. The alliance aims to increase crane lifespan, reduce operational downtime, and align Manitowoc products with the digital transformation trend in construction and industrial sectors.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.