Global Industrial Robotics Ai Software Market

Market Size in USD Billion

USD

9.00 Billion

USD

80.47 Billion

2025

2033

USD

9.00 Billion

USD

80.47 Billion

2025

2033

| 2026 - 2033 | |

| USD 9.00 Billion | |

| USD 80.47 Billion | |

| % | |

|

Industrial Robotics AI Software Market Overview

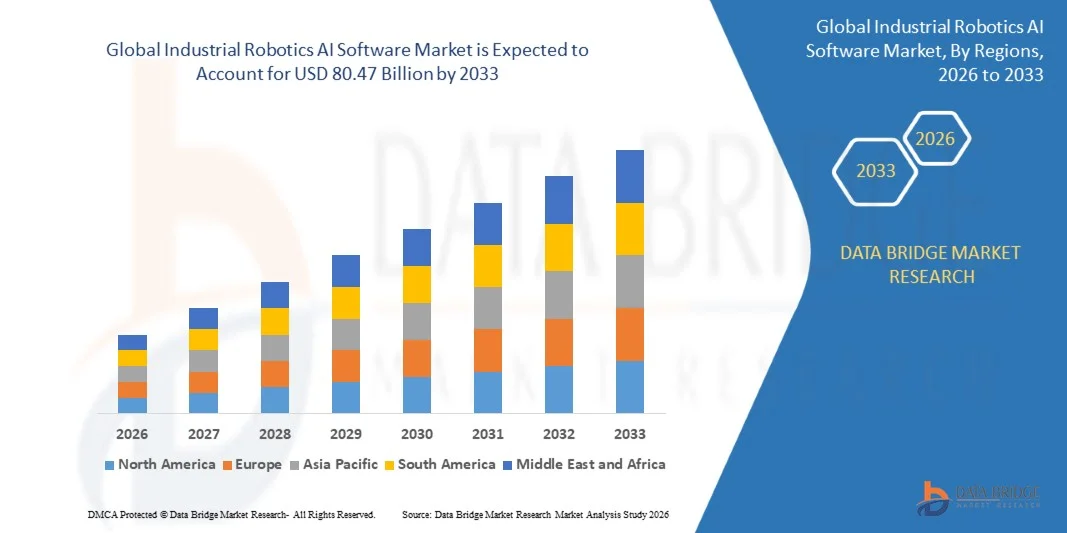

The Industrial Robotics AI Software Market was valued at USD 9 billion in 2025 and is projected to reach USD 80.47 billion by 2033, growing at a CAGR of 31.5% from 2026 to 2033. The market is experiencing rapid expansion driven by the accelerating adoption of intelligent automation, AI-enabled robotics, and smart manufacturing systems across industrial sectors.

The increasing integration of artificial intelligence into robotics software is transforming traditional industrial automation into adaptive, self-learning systems capable of real-time decision-making, predictive maintenance, and autonomous operation. Key technologies such as machine learning, computer vision, reinforcement learning, and digital twin platforms are enabling robots to perform complex tasks with higher precision, flexibility, and efficiency.

Key Market Trends & Insights

- North America is the leading region in the Industrial Robotics AI Software Market, accounting for a dominant share of 36.8% in 2025, driven by strong adoption of AI-driven automation, advanced manufacturing infrastructure, and presence of leading robotics and AI software vendors.

- Asia-Pacific is the fastest-growing region in the market, projected to expand at a CAGR of 34.2%, supported by rapid industrialization, expansion of electronics manufacturing hubs, and large-scale deployment of robotics in China, Japan, South Korea, and India.

- Computer Vision & Perception Software is the dominant segment by software type, accounting for 27.4% market share in 2025, due to its critical role in object detection, quality inspection, and real-time robotic navigation in industrial environments.

- Digital Twin & Simulation Platforms are the fastest-growing software segment, projected to grow at a CAGR of 35.6%, driven by increasing demand for virtual factory modeling, predictive analytics, and real-time robotic system optimization.

- By robot type, Industrial Robotic Arms remain the dominant segment with a 32.1% market share in 2025, widely used in automotive assembly, welding, material handling, and precision manufacturing applications.

- Autonomous Mobile Robots (AMRs) represent the fastest-growing robot segment, expanding at a CAGR of 36.8%, fueled by rising adoption in warehouse automation, last-mile logistics, and flexible intralogistics operations.

- By deployment mode, On-Premise deployment dominates the market with a 52.6% share in 2025, particularly in large-scale manufacturing and defense applications requiring high data security and low-latency processing.

- Cloud-Based deployment is the fastest-growing segment, expected to grow at a CAGR of 33.9%, driven by scalability, remote monitoring, and reduced infrastructure costs for robotics AI workloads.

- By AI technology, Machine Learning (ML) Systems hold the largest share in 2025 at 29.3%, enabling adaptive robotics behavior, predictive maintenance, and process optimization.

- Reinforcement Learning (RL) and Edge AI / Embedded Intelligence are emerging as the fastest-growing technologies, supporting autonomous decision-making and real-time robotic control in dynamic environments.

Market Size & Forecast

- Global Market Value (2025): USD 9 Billion

- Expected Market Value (2033): USD 80.47 Billion

- Forecast CAGR (2026–2033): 31.5%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Industrial Robotics AI Software Market Segmentation

|

Attributes |

Industrial Robotics AI Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Siemens AG (Germany) · ABB Ltd. (Switzerland) · Rockwell Automation, Inc. (U.S.) · NVIDIA Corporation (U.S.) · Microsoft Corporation (U.S.) · Alphabet Inc. (U.S.) · Amazon Web Services, Inc. (U.S.) · FANUC Corporation (Japan) · Yaskawa Electric Corporation (Japan) · KUKA AG (Germany) · Autodesk, Inc. (U.S.) · PTC Inc. (U.S.) · Siemens Digital Industries Software (Germany) · Dassault Systèmes SE (France) · Omron Corporation (Japan) |

|

Market Opportunities |

· Expansion of AI-powered autonomous robotics in smart factories and Industry 4.0 ecosystems · Rising adoption of cloud-native robotics AI platforms and Robotics-as-a-Service (RaaS) models · Integration of edge AI for real-time robotic decision-making and ultra-low latency control |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Industrial Robotics AI Software Market Trends

Trend: Rapid Adoption of AI-Driven Autonomous Robotics Systems

Industrial robotics software is rapidly evolving toward fully autonomous systems powered by AI models capable of perception, reasoning, and adaptive learning. Computer vision, reinforcement learning, and edge AI are enabling robots to perform complex industrial tasks with minimal human intervention. Companies are increasingly deploying AI-enabled robotic systems in automotive assembly, semiconductor fabrication, and warehouse automation. Leading technology providers such as Siemens AG and NVIDIA Corporation are integrating AI frameworks into robotics platforms to enable real-time simulation, motion planning, and predictive decision-making.

Industrial Robotics AI Software Market Dynamics

Key Market Driver: Rising Demand for Intelligent Automation and Smart Manufacturing

The Industrial Robotics AI Software Market is being strongly driven by the rising demand for intelligent automation and smart manufacturing across industries such as automotive, electronics, logistics, and industrial production. Companies are increasingly focusing on improving operational efficiency, reducing production costs, and achieving higher precision in manufacturing processes, which is accelerating the adoption of AI-powered robotics software. Technologies such as machine learning, computer vision, and reinforcement learning are enabling robots to perform complex tasks with greater autonomy, accuracy, and adaptability. As a result, industries like automotive and electronics are rapidly deploying intelligent robotic systems to enhance productivity, minimize defects, optimize supply chain operations, and improve overall production flexibility in highly competitive global markets.

Key Restraint/Challenge: High Integration Complexity and Skilled Workforce Shortage

Despite strong market growth, the industry faces significant challenges related to the high complexity of integrating advanced AI robotics software with existing legacy industrial systems. Many manufacturing facilities still rely on traditional automation infrastructure, making seamless integration of AI-driven robotics both technically difficult and time-consuming. Additionally, the shortage of skilled robotics AI engineers and automation specialists is limiting the speed of adoption, particularly in emerging economies and small to mid-sized enterprises. High implementation and maintenance costs, combined with interoperability issues across multi-vendor robotic ecosystems, further complicate large-scale deployment, creating barriers for organizations that lack sufficient technical expertise and financial resources to fully transition to AI-enabled automation systems.

Key Market Opportunity: Growth of Edge AI and Cloud Robotics Platforms

The convergence of edge computing, cloud infrastructure, and AI-powered robotics is creating substantial growth opportunities in the global market. Edge AI enables real-time, low-latency decision-making directly on robotic systems, which is critical for dynamic industrial environments such as warehouse automation, manufacturing lines, and autonomous mobile robotics. At the same time, cloud robotics platforms are allowing centralized control, remote monitoring, predictive analytics, and large-scale optimization of robotic fleets across multiple facilities and geographies. This hybrid model of edge and cloud-based robotics is enabling manufacturers to scale automation more efficiently while reducing infrastructure costs. As industries continue to adopt Industry 4.0 practices, the integration of cloud robotics with AI-driven simulation, digital twins, and predictive maintenance is expected to significantly transform global industrial automation ecosystems.

Industrial Robotics AI Software Market Scope

The industrial robotics AI software market is segmented on the basis of software type, robot type, deployment mode, AI technology, application and end user industry.

- By Software Type

On the basis of software type, the Industrial Robotics AI Software Market is segmented into robot operating systems (middleware platforms), AI motion planning & control software, computer vision & perception software, digital twin & simulation platforms, fleet management & coordination software, and predictive maintenance & safety software. The Computer Vision & Perception Software segment dominated the market with a 27.4% share in 2025, owing to its critical role in real-time object detection, quality inspection, defect identification, and robotic navigation across manufacturing and logistics environments. This segment remains essential for enabling autonomous decision-making and adaptive robotics performance in dynamic industrial settings.

The Digital Twin & Simulation Platforms segment is expected to witness the fastest growth at a CAGR of 35.6% from 2026 to 2033, driven by increasing adoption of virtual factory modeling, AI-enabled predictive simulation, and real-time optimization of robotic systems. The integration of digital twins with AI-based robotics software is further enhancing operational efficiency, reducing downtime, and enabling continuous performance monitoring across large-scale industrial automation networks.

- By Robot Type

On the basis of robot type, the Industrial Robotics AI Software Market is segmented into industrial robotic arms, collaborative robots (cobots), autonomous mobile robots (AMRs), automated guided vehicles (AGVs), and humanoid & service robots. The Industrial Robotic Arms segment dominated the market with a 32.1% share in 2025, driven by widespread use in automotive assembly, welding, material handling, packaging, and precision manufacturing applications. These systems remain the backbone of industrial automation due to their reliability, high payload capacity, and cost efficiency in repetitive tasks.

The Autonomous Mobile Robots (AMRs) segment is expected to witness the fastest growth at a CAGR of 36.8% from 2026 to 2033, fueled by rapid expansion of warehouse automation, e-commerce logistics, and flexible intralogistics systems. Increasing demand for intelligent, self-navigating robots capable of real-time path planning and dynamic obstacle avoidance is significantly accelerating AMR adoption across global supply chains.

- By Deployment Mode

On the basis of deployment mode, the Industrial Robotics AI Software Market is segmented into on-premise deployment, cloud-based deployment, and edge-based deployment. The On-Premise segment dominated the market with a 52.6% share in 2025, primarily due to strong adoption in large-scale manufacturing plants, automotive OEMs, and defense applications that require high data security, deterministic performance, and low-latency processing for mission-critical robotic operations.

The Cloud-Based segment is expected to witness the fastest growth at a CAGR of 33.9% from 2026 to 2033, driven by increasing demand for scalable computing infrastructure, remote fleet management, AI model training, and reduced capital expenditure. Cloud robotics platforms are enabling centralized control and analytics for distributed robotic systems across global production facilities.

- By AI Technology

On the basis of AI technology, the market is segmented into machine learning (ML) systems, deep learning & neural networks, reinforcement learning (RL), computer vision AI, edge AI / embedded intelligence, and hybrid / neurosymbolic AI systems. The Machine Learning (ML) Systems segment dominated the market with a 29.3% share in 2025, as it is widely used for predictive maintenance, process optimization, and adaptive robotic control across industrial applications.

The Reinforcement Learning (RL) and Edge AI / Embedded Intelligence segments are expected to witness the fastest growth during the forecast period, driven by increasing demand for autonomous decision-making, real-time robotic learning, and low-latency inference at the device level. These technologies are enabling robots to continuously improve performance in unstructured and dynamic environments without constant human intervention.

- By Application

On the basis of application, the Industrial Robotics AI Software Market is segmented into automotive manufacturing, electronics & semiconductor manufacturing, logistics & warehousing, metal & machinery production, food & beverage processing, chemicals, rubber & plastics, healthcare & pharmaceuticals, and others. The Automotive Manufacturing segment dominated the market with a 26.5% share in 2025, driven by extensive deployment of AI-powered robotics software in assembly lines, welding, painting, EV production, and autonomous vehicle component manufacturing. Automotive OEMs and suppliers are increasingly relying on intelligent robotics systems to enhance production speed, improve quality control, and reduce operational costs, making this segment the core revenue contributor in the global market.

The Logistics & Warehousing segment is expected to witness the fastest growth at a CAGR of 36.1% from 2026 to 2033, fueled by rapid expansion of e-commerce platforms, rising demand for warehouse automation, and increasing adoption of AI-enabled autonomous mobile robots (AMRs) and intelligent fulfillment systems. The growing need for real-time inventory management, faster order processing, and optimized supply chain operations is significantly accelerating robotics AI software adoption in this sector, especially across large-scale distribution centers and third-party logistics providers.

- By End User Industry

On the basis of end user industry, the Industrial Robotics AI Software Market is segmented into automotive industry, electronics industry, industrial manufacturing, logistics & e-commerce, healthcare & life sciences, aerospace & defense, food & beverage industry, and others. The Automotive Industry segment dominated the market with a 26.5% share in 2025, driven by extensive adoption of AI-powered robotics in assembly lines, welding, painting, EV manufacturing, and autonomous vehicle component production.

The Logistics & E-commerce segment is expected to witness the fastest growth at a CAGR of 36.1% from 2026 to 2033, fueled by rapid expansion of warehouse automation, last-mile delivery systems, and AI-enabled fulfillment centers. The increasing need for speed, accuracy, and operational efficiency in global supply chains is significantly accelerating robotics AI software adoption in this sector.

Industrial Robotics AI Software Market Regional Analysis

North America dominated the industrial robotics AI software market and accounted for the largest revenue share of 36.8% in 2025, driven by strong presence of leading robotics and AI software companies, advanced manufacturing infrastructure, and early adoption of Industry 4.0 technologies. The region also benefits from high investment in AI research, cloud robotics platforms, and large-scale industrial automation across automotive, electronics, and logistics sectors.

U.S. Industrial Robotics AI Software Market Insight

The U.S. industrial robotics AI software market is experiencing strong growth due to increasing investments in smart manufacturing, autonomous systems, and AI-driven industrial automation. The country’s leadership in robotics innovation, semiconductor manufacturing, and logistics automation is significantly driving demand for advanced robotics software solutions. Companies such as NVIDIA Corporation, Microsoft Corporation, and Rockwell Automation are actively contributing to AI-powered robotics ecosystems. Additionally, rising adoption of cloud robotics platforms and edge AI computing is further accelerating market expansion.

Europe Industrial Robotics AI Software Market Insight

The Europe industrial robotics AI software market is a key contributor to global growth, supported by strong automotive manufacturing, industrial engineering capabilities, and advanced robotics research infrastructure. The region is witnessing rapid adoption of AI-enabled robotics systems in automotive production, aerospace engineering, and smart factories. Companies such as Siemens AG and ABB Ltd. are driving innovation in industrial automation and digital manufacturing ecosystems across Europe.

U.K. Industrial Robotics AI Software Market Insight

The U.K. industrial robotics AI software market is steadily growing, driven by increasing adoption of automation in manufacturing, logistics, and defense applications. Rising investment in AI research, robotics startups, and digital transformation initiatives is strengthening market expansion. Universities and industrial research centers are actively developing advanced AI robotics systems for precision manufacturing, autonomous navigation, and warehouse automation.

Germany Industrial Robotics AI Software Market Insight

The Germany industrial robotics AI software market is expanding steadily due to the country’s strong industrial automation base, engineering excellence, and leadership in automotive and advanced manufacturing sectors. German OEMs and Tier-1 suppliers extensively deploy AI-powered robotics software in production lines for welding, assembly, painting, and EV manufacturing. Companies such as BMW Group and Mercedes-Benz Group AG are increasingly integrating robotics AI software into smart factory ecosystems to enhance productivity, precision, and operational efficiency. In addition, strong adoption of Industry 4.0 frameworks, digital twins, edge AI, and cloud-based robotics platforms is further strengthening market growth across the country.

Asia-Pacific Industrial Robotics AI Software Market Insight

The Asia-Pacific industrial robotics AI software market is expected to witness rapid growth, driven by large-scale industrialization, expanding electronics and semiconductor manufacturing, and rising automotive production in countries such as China, India, Japan, and South Korea. Increasing investment in smart factories, AI infrastructure, and digital transformation initiatives is significantly boosting demand for advanced robotics software solutions. The region is also witnessing strong adoption of cloud robotics platforms, edge AI systems, and autonomous mobile robots (AMRs) due to their scalability, cost efficiency, and flexibility in large manufacturing and logistics operations.

Japan Industrial Robotics AI Software Market Insight

The Japan industrial robotics AI software market is witnessing consistent growth due to the country’s strong focus on precision engineering, robotics innovation, and advanced manufacturing systems. Leading companies such as Toyota Motor Corporation, FANUC Corporation, and Yaskawa Electric Corporation are increasingly integrating AI-driven robotics software for automotive production, electronics manufacturing, and industrial automation. Applications such as quality inspection, autonomous robotic control, and predictive maintenance are widely deployed across factories. The integration of AI, digital twin technology, and high-performance computing is further enhancing operational efficiency and strengthening Japan’s leadership in robotics innovation.

China Industrial Robotics AI Software Market Insight

The China industrial robotics AI software market is growing rapidly, driven by large-scale industrial expansion, strong government support for advanced manufacturing, and rising investment in artificial intelligence and robotics technologies. The country is witnessing widespread deployment of AI-powered robotics systems across automotive, electronics, semiconductor, and logistics industries. Increasing adoption of smart manufacturing initiatives, cloud robotics platforms, and edge AI solutions is accelerating market penetration across enterprises and industrial parks. China is also emerging as a global hub for intelligent automation, supported by strong domestic manufacturing capacity and rapid digital transformation across industrial sectors.

Industrial Robotics AI Software Market Share

The industrial robotics AI software industry is primarily led by well-established companies, including:

- Siemens AG (Germany)

- ABB Ltd. (Switzerland)

- Rockwell Automation, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Microsoft Corporation (U.S.)

- Alphabet Inc. (U.S.)

- Amazon Web Services, Inc. (U.S.)

- FANUC Corporation (Japan)

- Yaskawa Electric Corporation (Japan)

- KUKA AG (Germany)

- Autodesk, Inc. (U.S.)

- PTC Inc. (U.S.)

- Siemens Digital Industries Software (Germany)

- Dassault Systèmes SE (France)

- Omron Corporation (Japan)

Latest Developments in Industrial Robotics AI Software Market

- In March 2026, NVIDIA Corporation strengthened its leadership in industrial robotics AI software by expanding its Physical AI ecosystem through the “Robot Brain” initiative, enabling deployment of AI models across industrial assembly lines in collaboration with partners such as Skild AI and Foxconn. The initiative integrates NVIDIA Omniverse simulation and Blackwell GPU infrastructure to accelerate real-world robotic learning, allowing adaptive automation across manufacturing environments and reinforcing NVIDIA’s role in end-to-end robotics AI software ecosystems.

- In March 2026, ABB Robotics enhanced its industrial robotics AI software capabilities by integrating NVIDIA Omniverse libraries into its RobotStudio platform, enabling advanced virtual-to-physical robot training and simulation-based deployment of autonomous industrial robots. This development significantly improves digital twin accuracy, reduces deployment time, and supports scalable AI-driven automation across automotive, electronics, and manufacturing industries.

- In March 2026, Siemens AG expanded its industrial AI and robotics software ecosystem by strengthening integration with NVIDIA technologies to accelerate digital twin-driven automation and intelligent manufacturing workflows. The collaboration focuses on combining simulation, AI, and industrial control systems to improve factory automation efficiency, reduce downtime, and enable next-generation smart manufacturing systems under Industry 4.0 frameworks.

- In March 2026, Rockwell Automation continued advancing its industrial robotics AI software portfolio by leveraging AI-driven automation and industrial control integration across manufacturing ecosystems. The company is increasingly focused on enabling predictive maintenance, intelligent production optimization, and connected factory systems powered by machine learning and edge-based industrial analytics.

- In March 2026, Fanuc Corporation expanded its AI-enabled industrial robotics systems by collaborating with NVIDIA and other technology partners to enhance autonomous robot deployment on production floors. The integration of AI models into Fanuc’s robotic platforms is improving precision manufacturing, adaptive control, and real-time decision-making capabilities in industrial environments.

- In March 2026, Yaskawa Electric Corporation advanced its robotics automation capabilities through integration of AI-driven control systems and collaboration with leading physical AI ecosystem developers. The company is focusing on improving motion control, predictive robotics intelligence, and adaptive manufacturing automation across automotive and electronics production lines.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.