Global Industrial Silica Sand Market

Market Size in USD Billion

USD

14.64 Billion

USD

22.98 Billion

2025

2033

USD

14.64 Billion

USD

22.98 Billion

2025

2033

| 2026 - 2033 | |

| USD 14.64 Billion | |

| USD 22.98 Billion | |

| % | |

|

Industrial Silica Sand Market Overview

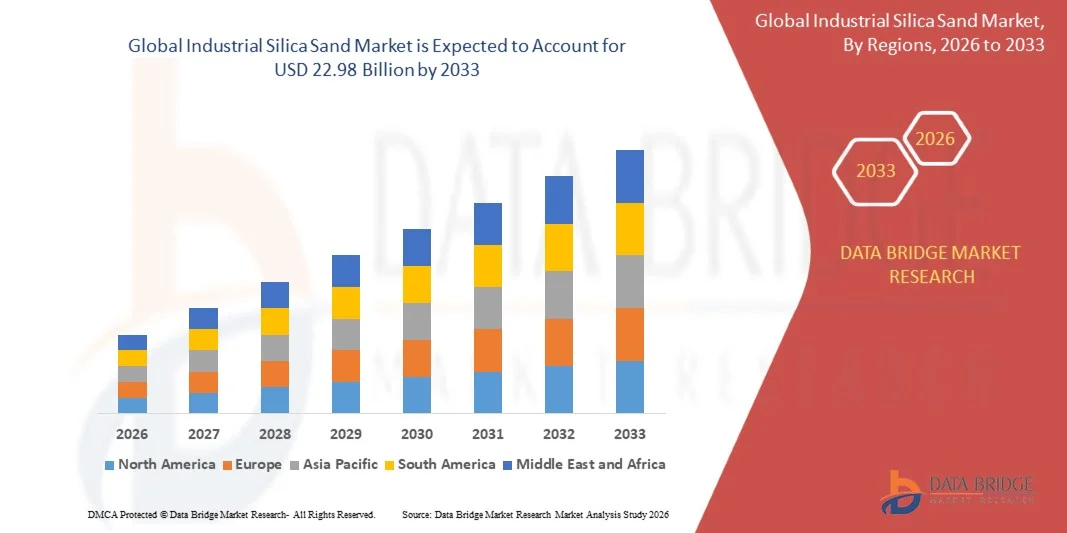

The Industrial Silica Sand Market was valued at USD 14.64 billion in 2025 and is projected to reach USD 22.98 billion by 2033, growing at a CAGR of 5.80% from 2026 to 2033. The market is witnessing steady expansion driven by rising demand from glass manufacturing, foundry casting, construction, and oil and gas industries, where silica sand is a critical raw material due to its high purity, strength, and chemical resistance.

The growth of the construction sector, particularly in emerging economies, is significantly increasing the consumption of silica sand in concrete production, mortars, and infrastructure development projects. In addition, the expanding glass industry, supported by rising demand for packaging glass, flat glass, and specialty glass, is further accelerating market growth. Technological advancements in sand processing and purification are also enhancing product quality, enabling wider adoption across high-performance industrial applications.

Key Market Trends & Insights

- North America dominated the industrial silica sand market with the largest revenue share of 38.6% in 2025, supported by strong demand from hydraulic fracturing activities, well-established mining infrastructure, and high consumption across glass and construction industries.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 6.7% from 2026 to 2033. Growth is driven by rapid urbanization, expanding construction activities, rising automotive production, and increasing glass manufacturing capacity in countries such as China, India, and Japan.

- The 40–70 Mesh segment held the largest market revenue share of approximately 46.2% in 2025 driven by its extensive use in hydraulic fracturing, glass manufacturing, and foundry applications due to its optimal balance of grain size, permeability, and strength. This grade is widely preferred in oil and gas operations, particularly in shale basins, where consistent particle distribution enhances reservoir conductivity and extraction efficiency.

- The Less Than 40 Mesh segment accounted for approximately 28.5% market share in 2025, supported by strong demand in construction applications such as concrete production, road building, and industrial infrastructure development where coarser sand grades are required for structural strength and bulk filling purposes.

- The Hydraulic Fracturing segment held the largest market revenue share of approximately 35.6% in 2025 driven by extensive shale gas exploration activities and increasing demand for high-quality frac sand to enhance well productivity and hydrocarbon recovery efficiency. Large-scale shale developments in North America continue to drive significant consumption volumes, with multi-well drilling operations requiring continuous sand supply.

- The Glassmaking segment accounted for approximately 27.4% market share in 2025 supported by rising demand for flat glass, container glass, and specialty glass products used in construction, automotive, and solar energy applications. Increasing adoption of high-purity silica sand in solar panel manufacturing is further strengthening this segment.

Market Size & Forecast

- Global Market Value (2025): USD 14.64 Billion

- Expected Market Value (2033): USD 22.98 Billion

- Forecast CAGR (2026–2033): 5.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Industrial Silica Sand Market Segmentation

|

Attributes |

Industrial Silica Sand Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Sibelco (Belgium) |

|

Market Opportunities |

• Expansion Of Hydraulic Fracturing Activities |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Industrial Silica Sand Market Trends

Trend: Rising Demand For High Purity Silica Sand In Advanced Industrial Applications

Increasing demand for high purity industrial silica sand across glass manufacturing, foundry casting, construction materials, and oil and gas operations is reshaping global supply requirements. Conventional low-grade sand is increasingly being replaced due to strict quality standards in float glass production, high-performance ceramics, and precision casting applications, driving demand for processed and washed silica sand with controlled grain size and low impurity content.

In modern glass manufacturing, producers are increasingly using high silica content sand, such as for flat glass used in solar panels and architectural glazing, to improve optical clarity and thermal resistance. In the construction sector, silica sand is being used in ready-mix concrete and engineered building materials to enhance durability and structural strength, particularly in large-scale infrastructure projects across Asia-Pacific. In oil and gas operations, high-purity silica sand is widely used as a proppant in hydraulic fracturing, with U.S. shale basins consuming millions of tons annually to improve well productivity and hydrocarbon recovery efficiency. In addition, growing demand from foundry industries for metal casting applications is supporting stable consumption, especially in automotive and heavy machinery manufacturing hubs in Germany, China, and India. Recent industrial benchmarks indicate that high purity silica sand with SiO₂ content above 99% is increasingly preferred in advanced glass and semiconductor-grade applications due to its superior chemical stability and low iron content.

Industrial Silica Sand Market Dynamics

Key Market Driver: Expanding Construction And Industrial Manufacturing Activities

Rapid urbanization, infrastructure expansion, and industrial development are significantly increasing the consumption of industrial silica sand across emerging and developed economies. Governments are investing heavily in transportation networks, smart cities, and commercial infrastructure, creating strong demand for cement, concrete, and glass-based construction materials.

In countries such as India, large-scale infrastructure programs including highway development, metro rail expansion, and housing initiatives are driving continuous demand for silica sand in construction-grade applications. In the U.S., shale gas exploration and hydraulic fracturing activities consume significant volumes of frac sand, with some major basins requiring several million tons annually for well stimulation. Similarly, the automotive and manufacturing sectors are increasing demand for silica sand in metal casting processes, particularly for engine components and industrial machinery production. Industrial reports indicate that construction applications account for a dominant share of global silica sand consumption, with Asia-Pacific contributing the highest incremental demand growth due to ongoing urban expansion and industrialization.

Key Restraint/Challenge: Environmental Regulations And Supply Chain Constraints

Industrial silica sand mining and processing face increasing regulatory scrutiny due to environmental concerns such as land degradation, groundwater disruption, and dust emissions. Strict mining regulations and permitting delays in several countries are limiting new project development and restricting supply expansion in key producing regions.

In regions such as Europe and parts of North America, environmental compliance requirements have increased operational costs for mining companies, particularly for washing, drying, and grading processes needed to achieve high purity standards. Transportation bottlenecks and rising logistics costs further impact price stability, especially for cross-border silica sand trade used in glass and oilfield applications. In addition, depletion of easily accessible high-quality sand reserves is forcing producers to invest in deeper and more complex mining operations, increasing production complexity and cost structure. Industry estimates suggest that transportation can account for a significant portion of delivered silica sand cost in landlocked regions, particularly for oil and gas proppant applications requiring large-volume shipments.

Key Market Opportunity: Rising Demand From Solar Energy And Advanced Manufacturing

Growing adoption of solar energy systems, semiconductor manufacturing, and high-performance glass applications is creating strong long-term opportunities for industrial silica sand producers. High-purity silica sand is a critical raw material for photovoltaic glass used in solar panels, as well as for specialty glass in electronics and precision engineering applications.

Solar capacity expansion projects across China, India, and the U.S. are increasing demand for ultra-clear flat glass, where silica sand with very low iron content is essential for maximizing light transmission efficiency. In semiconductor manufacturing, silica-based materials are used in wafer processing and high-purity glass components, supporting demand for refined sand grades. In addition, advanced manufacturing industries are increasingly using silica sand in precision casting and additive manufacturing applications to achieve higher dimensional accuracy and material performance. Recent industry developments indicate that solar glass manufacturing capacity expansions announced in 2025 across Asia-Pacific are expected to significantly boost demand for high-grade silica sand, particularly in regions with strong renewable energy targets and industrial investment programs.

Industrial Silica Sand Market Scope

The market is segmented on the basis of classification and application.

• By Classification

On the basis of classification, the industrial silica sand market is segmented into Less Than 40 Mesh, 40–70 Mesh, and More Than 70 Mesh. The 40–70 Mesh segment held the largest market revenue share of approximately 46.2% in 2025 driven by its extensive use in hydraulic fracturing, glass manufacturing, and foundry applications due to its optimal balance of grain size, permeability, and strength. This grade is widely preferred in oil and gas operations, particularly in shale basins, where consistent particle distribution enhances reservoir conductivity and extraction efficiency.

The Less Than 40 Mesh segment accounted for approximately 28.5% market share in 2025, supported by strong demand in construction applications such as concrete production, road building, and industrial infrastructure development where coarser sand grades are required for structural strength and bulk filling purposes.

• By Application

On the basis of application, the industrial silica sand market is segmented into Hydraulic Fracturing, Glassmaking, Foundry, Ceramics and Refractories, and Others. The Hydraulic Fracturing segment held the largest market revenue share of approximately 35.6% in 2025 driven by extensive shale gas exploration activities and increasing demand for high-quality frac sand to enhance well productivity and hydrocarbon recovery efficiency. Large-scale shale developments in North America continue to drive significant consumption volumes, with multi-well drilling operations requiring continuous sand supply.

The Glassmaking segment accounted for approximately 27.4% market share in 2025 supported by rising demand for flat glass, container glass, and specialty glass products used in construction, automotive, and solar energy applications. Increasing adoption of high-purity silica sand in solar panel manufacturing is further strengthening this segment.

Industrial Silica Sand Market Regional Analysis

North America Industrial Silica Sand Market Insight

North America dominated the industrial silica sand market with the largest revenue share of 38.6% in 2025, supported by strong demand from hydraulic fracturing, glass manufacturing, and construction activities. The region benefits from abundant high-quality silica reserves, well-established mining infrastructure, and large-scale consumption in oil and gas shale formations. The increasing use of frac sand in unconventional drilling operations across major basins such as Permian and Eagle Ford is further strengthening regional demand. In addition, the presence of advanced glass manufacturing and automotive industries continues to support steady consumption of high-purity silica sand.

U.S. Industrial Silica Sand Market Insight

The U.S. industrial silica sand market captured the largest revenue share of 81.2% within North America in 2025, driven primarily by extensive shale gas exploration and hydraulic fracturing activities. The country remains one of the world’s largest consumers of frac sand, with millions of tons used annually to enhance oil and gas recovery efficiency. Rising demand from flat glass production, construction materials, and foundry applications further supports market growth. Moreover, increasing investments in infrastructure modernization and renewable energy projects, such as solar panel manufacturing, are expanding the use of high-purity silica sand in advanced industrial applications.

Europe Industrial Silica Sand Market Insight

The Europe industrial silica sand market is expected to witness steady growth from 2026 to 2033, driven by strict environmental regulations, rising demand for high-quality construction materials, and expansion of the glass manufacturing industry. The region’s strong automotive and industrial base supports consistent consumption in foundry and ceramics applications. Increasing adoption of renewable energy systems, particularly solar glass manufacturing, is also contributing to market expansion. In addition, sustainability-focused mining practices and recycling initiatives are shaping supply chain improvements across major European economies.

U.K. Industrial Silica Sand Market Insight

The U.K. industrial silica sand market is expected to witness moderate growth from 2026 to 2033, supported by demand from construction, glass production, and water filtration applications. Growing infrastructure development projects, including residential housing and commercial construction, are driving steady consumption of silica sand. The country’s expanding renewable energy sector, particularly offshore wind and solar installations, is also indirectly supporting demand for high-quality glass components. Furthermore, increasing focus on sustainable building materials is encouraging the use of processed silica sand in eco-friendly construction solutions.

Germany Industrial Silica Sand Market Insight

The Germany industrial silica sand market is expected to witness steady growth from 2026 to 2033, fueled by strong demand from automotive manufacturing, glass production, and advanced industrial applications. Germany’s well-developed industrial base and emphasis on high-precision engineering are driving consumption of high-purity silica sand in foundry and ceramics sectors. In addition, the country’s leadership in renewable energy and solar technology is increasing demand for flat glass manufacturing. Sustainability regulations and circular economy initiatives are further promoting efficient use and recycling of silica-based materials.

Asia-Pacific Industrial Silica Sand Market Insight

The Asia-Pacific industrial silica sand market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, industrial expansion, and increasing infrastructure investments in countries such as China, India, and Japan. Rising construction activities, growing automotive production, and expanding glass manufacturing industries are significantly driving regional demand. The availability of low-cost labor and abundant raw material resources is also strengthening APAC’s position as a key production and consumption hub. In addition, government-led smart city and renewable energy initiatives are boosting long-term market growth.

Japan Industrial Silica Sand Market Insight

The Japan industrial silica sand market is expected to witness steady growth from 2026 to 2033 due to strong demand from electronics, automotive, and precision manufacturing industries. The country’s advanced industrial ecosystem requires high-purity silica sand for specialized glass, semiconductor components, and high-performance ceramics. Increasing adoption of renewable energy systems, particularly solar glass applications, is further supporting demand. In addition, Japan’s focus on technological innovation and high-quality material standards is driving consistent usage of refined silica sand in advanced industrial applications.

China Industrial Silica Sand Market Insight

The China industrial silica sand market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, massive infrastructure development, and strong industrial production capacity. The country remains a global leader in glass manufacturing, construction materials, and electronics production, all of which require large volumes of silica sand. Expanding renewable energy projects, including large-scale solar panel manufacturing, are further boosting demand for high-purity silica sand. In addition, strong domestic mining capabilities and cost-efficient production infrastructure are supporting China’s dominant position in the regional market.

Industrial Silica Sand Market Share

The Industrial Silica Sand industry is primarily led by well-established companies, including:

• Sibelco (Belgium)

• U.S. Silica (U.S.)

• Covia Holdings LLC (U.S.)

• Quarzwerke GmbH (Germany)

• Badger Mining Corporation (U.S.)

• Chongqing Changjiang River Moulding Material (Group) Co., Ltd. (China)

• Mitsubishi Corporation (Japan)

• Tremco Incorporated (U.S.)

• TOCHU CORPORATION (Japan)

• JFE MINERAL Co., LTD. (Japan)

• Emerge Energy Services (U.S.)

• Euroquarz GmbH (Germany)

• Hi-Crush Inc. (U.S.)

• Preferred Sands (U.S.)

• Aggregate Industries (U.K.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Industrial Silica Sand Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Industrial Silica Sand Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Industrial Silica Sand Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.