Global Industrial Starch Market

Market Size in USD Billion

USD

90.20 Billion

USD

119.90 Billion

2024

2032

USD

90.20 Billion

USD

119.90 Billion

2024

2032

| 2025 - 2032 | |

| USD 90.20 Billion | |

| USD 119.90 Billion | |

| % | |

|

Industrial Starch Market Size

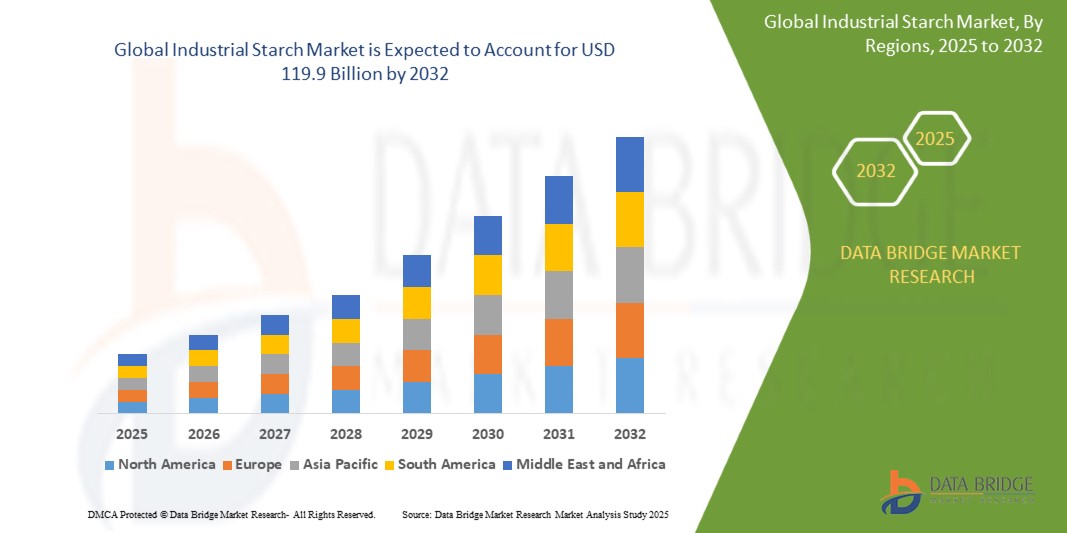

- The Global Industrial Starch Market size was valued at USD 90.20 billion in 2024 and is expected to reach USD 119.9 billion by 2032, at a CAGR of 6.6% during the forecast period

- The growth of the Industrial Starch Market is driven by several key factors, including the increasing demand for starch-based products across various industries, the growing need for sustainable and eco-friendly alternatives, and the rising demand for processed food and beverages

Industrial Starch Market Analysis

- Industrial starch is increasingly being recognized as a crucial ingredient in various industries, including food, beverages, pharmaceuticals, and textiles, driving the market's expansion. The demand for starch is particularly rising due to its versatility, cost-effectiveness, and natural origin, which align with current consumer preferences for clean-label and sustainable products

- The market for industrial starch is rapidly expanding as manufacturers in the food and beverage industry, as well as non-food sectors, seek to enhance product textures, stability, and functionality. Starch is commonly used in applications such as food thickening, binding agents, and stabilizers, and is gaining popularity as a natural alternative to synthetic additives

- North America is expected to dominate the Industrial Starch Market with a substantial share in 2025, driven by the region's established food processing infrastructure, consumer demand for healthier and more natural food products, and a strong presence of major food manufacturers. The clean-label trend, coupled with the demand for minimally processed and natural ingredients, supports starch's growth in the food industry

- Asia-Pacific is projected to register the highest growth rate in the Industrial Starch Market due to rising disposable incomes, increasing health consciousness, and expanding functional food consumption. Key countries such as China, India, and Japan are seeing a rise in demand for starch-based products, fueled by the growing focus on health and wellness and the adoption of western-style processed foods

Report Scope and Industrial Starch Market Segmentation

|

Attributes |

Industrial Starch Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Industrial Starch Market Trends

Increasing Adoption of Modified Starch in Clean-Label and Health-Conscious Products

- A key trend in the Industrial Starch Market is the growing adoption of modified starches in clean-label, health-conscious food products, as consumers demand natural, minimally processed ingredients in their diets

- Modified starches, which are often derived from plant-based sources like corn, potato, and tapioca, are being increasingly used in food applications to improve texture, stability, and shelf life while still maintaining the clean-label appeal

- For example, modified starches are used to enhance the mouthfeel of dairy alternatives, such as almond milk, and to improve the texture of gluten-free baked goods

- This trend is helping manufacturers cater to the rising demand for products with simple ingredient lists, meeting consumer preferences for foods free from artificial additives and preservatives while still offering desirable functionality and performance

Industrial Starch Market Dynamics

Driver

Growing Demand for Clean-Label, Natural Ingredients in Processed Foods

- The rising consumer demand for clean-label foods, free from artificial additives and preservatives, is driving growth in the Industrial Starch Market

- As consumers increasingly prioritize transparency and health-conscious choices, food manufacturers are turning to natural, minimally processed starches to meet these demands without compromising the quality or shelf life of their products

- Starches, such as modified starch and native starches, are being used to enhance texture, stability, and consistency in a wide range of food applications, from snacks and baked goods to dairy alternatives and sauces

For instance:

- Modified starches are helping manufacturers improve the texture of gluten-free products, while native starches are used in dairy substitutes to provide creaminess and mouthfeel.

- The clean-label movement is also pushing companies to innovate with starch-based solutions that are not only natural but also sustainable, addressing growing concerns over environmental impact.

- As the demand for healthy and clean-label products continues to rise, the use of industrial starches as a natural ingredient is expected to expand, with a focus on products that promote both wellness and sustainability.

Opportunity

Rising Demand for Sustainable, Plant-Based Starch Ingredients

- The increasing demand for plant-based, sustainable food ingredients is creating significant opportunities in the Industrial Starch Market.

- As consumers become more environmentally conscious, food manufacturers are seeking plant-derived starches that are sustainable and offer clean-label benefits. These starches are used across a variety of applications, including gluten-free, vegan, and organic food products.

- The shift towards plant-based diets is encouraging the use of starches from renewable sources like corn, potatoes, and tapioca, which are seen as more eco-friendly alternatives to synthetic or animal-derived ingredients.

For instance:

- Companies are increasingly using potato starch in snacks and baked goods, and tapioca starch in dairy alternatives, to cater to the growing consumer demand for plant-based, allergen-free, and sustainable products.

- This trend is expected to continue as food companies focus on eco-friendly sourcing and creating products that appeal to the health-conscious and environmentally aware consumer. The need for sustainably sourced, plant-based ingredients is anticipated to drive further growth in the Industrial Starch Market.

Restraint/Challenge

High Cost of Extraction and Processing of Industrial Starch

- One of the key restraints in the Industrial Starch Market is the high cost associated with extracting and processing starch from plant sources

- The process of refining and extracting starch from crops such as corn, potatoes, and tapioca often requires specialized equipment, energy-intensive procedures, and stringent quality controls, all of which contribute to elevated production costs

- These high processing costs can make plant-based starches more expensive than alternatives, potentially hindering their widespread use, particularly among small and medium-sized food manufacturers and in price-sensitive markets

For instance,

- Small food producers may find it challenging to compete with larger companies that have access to economies of scale, which can afford to process starch at a lower cost

- This cost barrier can limit the adoption of natural and organic starch ingredients, especially in developing economies where lower-priced options dominate the market

Industrial Starch Market Scope

The market is segmented on the basis source, type, form, application.

|

Segmentation |

Sub-Segmentation |

|

By Type |

|

|

By Source |

|

|

By Application |

|

|

By Form

|

|

In 2025, the native starch is projected to dominate the market with a largest share in type segment

In 2025, native starch is projected to dominate the Global Industrial Starch Market with the largest share in the type segment, accounting for 58.7%. This dominance is attributed to the increasing demand for native starches in food and beverage applications, as they provide excellent texture, stability, and binding properties without the need for further modification.

The Food is expected to account for the largest share during the forecast period in application segment

In 2025, the food segment is expected to account for the largest share in the Global Industrial Starch Market, with a projected market share of 51.2%. This dominance is driven by the growing consumer preference for clean-label, minimally processed food products and the increasing demand for healthier, natural ingredients in food manufacturing.

Industrial Starch Market Regional Analysis

Asia-Pacific is Projected to Register the Highest Growth in the Industrial Starch Market

- The Asia-Pacific region is expected to register the highest growth rate in the Global Industrial Starch Market, driven by rapid urbanization, rising health consciousness, and increasing consumer demand for plant-based, natural food ingredients across countries such as China, India, and Japan

- With large populations and rising disposable incomes, countries like China and India are key markets for industrial starch, as consumers are increasingly opting for healthier, clean-label food options and seeking alternatives to synthetic ingredients in food products.

- Japan is a leader in the region's industrial starch market, with a high demand for functional foods, clean-label products, and health-focused food items. The country’s strong focus on wellness and food innovation is propelling market growth

- China and India are witnessing a surge in the adoption of plant-based diets and health-conscious food trends, which is driving the demand for starch ingredients derived from natural sources for food processing and manufacturing

- Government initiatives promoting healthier eating habits, increasing investments in food processing technologies, and growing awareness of the benefits of plant-based, antioxidant-rich ingredients are supporting the expansion of the industrial starch market in the region

- As infrastructure improves and the food processing industry continues to evolve, Asia-Pacific is expected to see a significant rise in the demand for industrial starch as an essential component in the production of clean-label, natural, and functional food products.

North America is Projected to Dominate the Industrial Starch Market

-

North America is expected to hold the largest share of the Global Industrial Starch Market, driven by strong consumer preference for natural, clean-label, and sustainable food options across the region

- The U.S. is a major contributor to the market, accounting for a significant portion of North America’s market share. Consumers in the U.S. are increasingly demanding plant-based and antioxidant-rich ingredients, which has led to higher adoption of natural food starches, especially in the food and beverage industry

- The rising awareness around health benefits, such as the antioxidant properties of certain starches, is boosting the demand for products that support wellness, immune function, and anti-aging benefits

- North America’s market is further propelled by the increasing adoption of clean-label products, with consumers favoring those that are free from artificial preservatives, colors, and flavors, thus encouraging the demand for plant-based and natural starch solutions

- Additionally, North America’s well-established food processing infrastructure and favorable regulatory environment are key factors supporting market growth. The presence of leading food manufacturers investing in R&D to innovate and develop functional food products with added health benefits is also driving the market

- As the demand for sustainable and healthier food options continues to rise, investments from both local and international companies in the region are expected to accelerate market expansion. The growing preference for plant-based diets and healthier eating habits positions North America as a leader in the industrial starch market

Industrial Starch Market Share

The market competitive landscape provides details by competitor. Details included are company overview, company financials, revenue generated, market potential, investment in research and development, new market initiatives, global presence, production sites and facilities, production capacities, company strengths and weaknesses, product launch, product width and breadth, application dominance. The above data points provided are only related to the companies' focus related to market.

The Major Market Leaders Operating in the Market Are:

- Archer Daniels Midland Company (U.S.)

- Cargill, Incorporated (U.S.)

- DuPont de Nemours, Inc. (U.S.)

- Tate & Lyle PLC (U.K.)

- Ingredion Incorporated (U.S.)

- Bunge Limited (U.S.)

- Royal DSM (Netherlands)

- AGROFERT Group (Czech Republic)

- Corn Products International, Inc. (U.S.)

- MGP Ingredients, Inc. (U.S.)

- Kerry Group plc (Ireland)

- Emsland Group (Germany)

- Starch Solution (Germany)

- Manildra Group (Australia)

- Avebe (Netherlands)

Latest Developments in Global Industrial Starch Market

- In March 2025, Archer Daniels Midland Company (ADM) launched a new line of antioxidant-rich ingredients sourced from natural fruits and vegetables, specifically designed to meet the growing demand for clean-label, plant-based products. These ingredients offer enhanced antioxidant properties that help improve the nutritional profile and shelf life of a wide range of food products, including snacks, beverages, and packaged foods. This product launch is in line with the increasing consumer demand for products that offer natural health benefits and support overall wellness

- In February 2025, DuPont Nutrition & Biosciences unveiled a new formulation of antioxidant-rich extracts from natural sources like berries and citrus fruits. These ingredients are designed to preserve the freshness of food products while providing added health benefits, such as enhanced immunity and anti-aging properties. The new launch aims to expand the use of antioxidants in functional foods and beverages, catering to the rising demand for health-focused, clean-label products

- In January 2025, Cargill announced a strategic partnership with a leading global nutrition company to co-develop innovative antioxidant-enriched products. These products are designed to preserve the natural color, flavor, and nutritional value of plant-based food offerings. The collaboration focuses on antioxidants derived from natural sources, including green tea, pomegranate, and turmeric, to enhance food safety, reduce oxidative stress, and promote health benefits such as inflammation reduction

- In December 2024, the Natural Antioxidants Association (NAA) launched a global awareness campaign aimed at highlighting the benefits of antioxidants from natural sources. The campaign focuses on managing chronic diseases such as heart disease, cancer, and diabetes. Through educational seminars, research papers, and partnerships with health organizations, the initiative emphasizes the importance of incorporating antioxidant-rich foods like fruits, vegetables, and nuts into daily diets, further boosting the market for natural antioxidants in food products

- In November 2024, Ingredion Incorporated introduced a new line of natural antioxidant-rich extracts for food manufacturers focused on sustainability. These ingredients, sourced from organic farming practices, help improve product quality and maintain freshness while supporting the growing demand for clean-label, environmentally friendly foods. The new range includes antioxidants from sources like acai berries, elderberries, and grapeseed, which are gaining popularity for their potent health benefits and versatility in food applications.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Table of Content

1 INTRODUCTION

1.1 OBJECTIVES OF THE STUDY

1.2 MARKET DEFINITION

1.3 OVERVIEW OF GLOBAL INDUSTRIAL STARCH MARKET

1.4 CURRENCY AND PRICING

1.5 LIMITATION

1.6 MARKETS COVERED

2 MARKET SEGMENTATION

2.1 KEY TAKEAWAYS

2.2 ARRIVING AT THE GLOBAL INDUSTRIAL STARCH MARKET SIZE

2.2.1 VENDOR POSITIONING GRID

2.2.2 TECHNOLOGY LIFE LINE CURVE

2.2.3 MARKET GUIDE

2.2.4 COMPANY POSITIONING GRID

2.2.4.1. KEY PLAYERS

2.2.4.2. DISRUPTORS

2.2.4.3. NICHE PLAYERS

2.2.4.4. PROSPECT LEADERS

2.2.5 COMPANY MARKET SHARE ANALYSIS

2.2.6 MULTIVARIATE MODELLING

2.2.7 DEMAND AND SUPPLY-SIDE VARIABLES

2.2.8 TOP TO BOTTOM ANALYSIS

2.2.9 STANDARDS OF MEASUREMENT

2.2.10 VENDOR SHARE ANALYSIS

2.2.11 DATA POINTS FROM KEY PRIMARY INTERVIEWS

2.2.12 DATA POINTS FROM KEY SECONDARY DATABASES

2.3 GLOBAL INDUSTRIAL STARCH MARKET : RESEARCH SNAPSHOT

2.4 ASSUMPTIONS

3 MARKET OVERVIEW

3.1 DRIVERS

3.2 RESTRAINTS

3.3 OPPORTUNITIES

3.4 CHALLENGES

4 EXECUTIVE SUMMARY

5 PREMIUM INSIGHTS

5.1 EXPORT AND IMPORT TRADE ANALYSIS

5.2 VALUE CHAIN ANALYSIS

5.3 SUPPLY CHAIN ANALYSIS

5.4 FACTORS INFLUENCING PURCHASING DECISION OF END USERS

5.5 GROWTH STRATEGIES ADOPTED BY KEY MARKET PLAYERS

5.6 INDUSTRY TRENDS AND FUTURE PERSPECTIVE

5.7 TECHNOLOGICAL ADAVANCEMENT

6 REGULATORY FRAMEWORK AND GUIDELINES

7 GLOBAL INDUSTRIAL STARCH MARKET, BY TYPE OF STARCH

7.1 OVERVIEW

7.2 NATIVE STARCH

7.3 MODIFIED STARCH

7.3.1 MODIFIED STARCH, BY TYPE

7.3.1.1. OXIDIZED STARCH

7.3.1.2. DEXTRINIZED STARCH

7.3.1.3. CROSSLINKED STARCH

7.3.1.3.1. ACETYLATED STARCH

7.3.1.3.2. PHOSPHATE MONOESTER STARCH

7.3.1.4. PREGELATINIZED STARCH

7.3.1.5. ACID THINNED STARCH

7.3.1.6. STARCH ETHER

7.3.1.7. STARCH ESTER

7.3.1.8. ACETYLATED STARCH

7.3.1.9. OTHERS

7.4 STARCH HYDROLYSATE

7.4.1 STARCH HYDROLYSATE, BY TYPE

7.4.1.1. STARCH DERIVATIVE SUGAR

7.4.1.2. GLUCOSE

7.4.1.3. MALTOSE

7.4.1.4. HIGH-FRUCTOSE CORN SYRUP(HFCS)

7.4.1.5. MALTODEXTRIN

7.4.1.6. OTHERS

7.5 STARCH OLIGOSACCHARIDE DERIVATIVES

7.5.1 STARCH OLIGOSACCHARIDE DERIVATIVES, BY TYPE

7.5.2 XYLO-OLIGOSACCHARIDE

7.5.3 FRUCTO-OLIGOSACCHARIDE

7.5.4 OTHERS

7.6 OTHERS

8 GLOBAL INDUSTRIAL STARCH MARKET, BY SOURCE

8.1 OVERVIEW

8.2 CORN

8.3 WHEAT

8.4 BARLEY

8.5 POTATO

8.6 RICE

8.7 CASSAVA/TAPIOCA

8.8 OTHERS

9 GLOBAL INDUSTRIAL STARCH MARKET, BY NATURE OF SOURCE

9.1 OVERVIEW

9.2 GMO

9.3 NON-GMO

10 GLOBAL INDUSTRIAL STARCH MARKET, BY FORM

10.1 OVERVIEW

10.2 DRY

10.3 LIQUID

10.4 GRANULES

10.5 PELLETS

10.6 OTHERS (IF ANY)

11 GLOBAL INDUSTRIAL STARCH MARKET, BY FUNCTION

11.1 OVERVIEW

11.2 THICKENING

11.3 TEXTURING

11.4 STABILIZING

11.5 MOISTURE-RETENTION

11.6 GELLING

11.7 BINDING / ADHESION

11.8 COATING/DUSTING

11.9 OTHERS

12 GLOBAL INDUSTRIAL STARCH MARKET, BY APPLICATION

12.1 OVERVIEW

12.2 FOOD & BEVERAGES

12.2.1 FOOD AND BEVERAGES, BY TYPE

12.2.1.1. BAKERY

12.2.1.1.1. BAKERY, BY TYPE

12.2.1.1.1.1 BREAD & ROLLS

12.2.1.1.1.2 CAKES, PASTRIES & TRUFFLE

12.2.1.1.1.3 TART & PIES

12.2.1.1.1.4 BROWNIES

12.2.1.1.1.5 BISCUIT, COOKIES & CRACKERS

12.2.1.1.1.6 OTHERS

12.2.1.2. DAIRY PRODUCTS

12.2.1.2.1. DAIRY PRODUCTS, BY TYPE

12.2.1.2.1.1 YOGURT

12.2.1.2.1.2 ICE CREAM

12.2.1.2.1.3 CHEESE

12.2.1.2.1.4 OTHERS

12.2.1.3. PROCESSED FOOD

12.2.1.3.1. PROCESSED FOOD, BY TYPE

12.2.1.3.1.1 READY MEALS

12.2.1.3.1.2 SAUCES, DRESSINGS AND CONDIMENTS

12.2.1.3.1.3 SOUPS

12.2.1.3.1.4 JAMS, PRESERVES & MARMALADES

12.2.1.3.1.5 OTHERS

12.2.1.4. CONFECTIONERY

12.2.1.4.1. CONFECTIONERY, BY TYPE

12.2.1.4.1.1 HARD-BOILED SWEETS

12.2.1.4.1.2 MINTS

12.2.1.4.1.3 GUMS & JELLIES

12.2.1.4.1.4 CHOCOLATE

12.2.1.4.1.5 CHOCOLATE SYRUPS

12.2.1.4.1.6 CARAMELS & TOFFEES

12.2.1.4.1.7 OTHERS

12.2.1.5. FROZEN DESSERTS

12.2.1.5.1. FROZEN DESSERTS, BY TYPE

12.2.1.5.1.1 GELATO

12.2.1.5.1.2 CUSTARD

12.2.1.5.1.3 OTHERS

12.2.1.6. FUCNTIONAL FOOD

12.2.1.7. MEAT PRODUCTS

12.2.1.8. MEAT ALTERNATIVE

12.2.1.9. CONVENIENCE FOOD

12.2.1.9.1. CONVENIENCE FOOD, BY TYPE

12.2.1.9.1.1 INSTANT NOODLES

12.2.1.9.1.2 PIZZA & PASTA

12.2.1.9.1.3 SANCKS& EXTRUDED SNACKS

12.2.1.9.1.4 OTHERS

12.2.1.10. BEVERAGES

12.2.1.10.1. BEVERAGES, BY TYPE

12.2.1.10.1.1 SMOOTHIES

12.2.1.10.1.2 JUICES

12.2.1.10.1.3 SPORTS DRINKS

12.2.1.10.1.4 ENERGY DRINKS

12.2.1.10.1.5 DAIRY BASED DRINKS

12.2.1.10.1.5.1. REGULAR PROCESSED MILK

12.2.1.10.1.5.2. FLVORED MILK

12.2.1.10.1.5.3. MILK SHAKES

12.2.1.10.1.5.4. FUNCTIONAL BEVERAGES

12.2.1.10.1.6 DAIRY ALTERNATIVE BEVERAGES

12.2.1.10.1.7 OTHERS

12.2.2 FOOD AND BEVERAGES, BY STARCH TYPE

12.2.2.1. NATIVE STARCH

12.2.2.2. MODIFIED STARCH

12.2.2.3. STARCH HYDROLYSATE

12.2.2.4. STARCH OLIGOSACCHARIDE DERIVATIVES

12.2.2.5. OTHERS

12.3 ANIMAL FEED

12.3.1 ANIMAL FEED, BY TYPE

12.3.2 RUMINANT FEED

12.3.3 POULTRY FEED

12.3.4 SWINE FEED

12.3.5 AQUAFEED

12.3.6 ANIMAL FEED, BY STARCH TYPE

12.3.6.1. NATIVE STARCH

12.3.6.2. MODIFIED STARCH

12.3.6.3. STARCH HYDROLYSATE

12.3.6.4. STARCH OLIGOSACCHARIDE DERIVATIVES

12.3.6.5. OTHERS

12.4 PHARMACEUTICAL

12.4.1 PHARMACEUTICAL, BY TYPE

12.4.1.1. CAPSULES

12.4.1.2. TABLETS

12.4.1.3. OTHERS

12.4.2 PHARMACEUTICAL, BY STARCH TYPE

12.4.2.1. NATIVE STARCH

12.4.2.2. MODIFIED STARCH

12.4.2.3. STARCH HYDROLYSATE

12.4.2.4. STARCH OLIGOSACCHARIDE DERIVATIVES

12.4.2.5. OTHERS

12.5 PERSONAL CARE

12.5.1 PERSONAL CARE, BY TYPE

12.5.1.1. HAIR CARE

12.5.1.2. SKIN CARE

12.5.2 PERSONAL CARE, BY STARCH TYPE

12.5.2.1. NATIVE STARCH

12.5.2.2. MODIFIED STARCH

12.5.2.3. STARCH HYDROLYSATE

12.5.2.4. STARCH OLIGOSACCHARIDE DERIVATIVES

12.5.2.5. OTHERS

12.6 COSMETIC

12.6.1 COSMETIC, BY TYPE

12.6.1.1. FACE CREAM

12.6.1.2. FACE SERUMS

12.6.1.3. LIP CARE AND LIPSTICK PRODUCTS

12.6.1.4. OTHERS

12.6.2 COSMETIC, BY STARCH TYPE

12.6.2.1. NATIVE STARCH

12.6.2.2. MODIFIED STARCH

12.6.2.3. STARCH HYDROLYSATE

12.6.2.4. STARCH OLIGOSACCHARIDE DERIVATIVES

12.6.2.5. OTHERS

12.7 PAPER AND CORRUGATION INDUSTRY

12.7.1 PAPER AND CORRUGATION, BY STARCH TYPE

12.7.1.1. NATIVE STARCH

12.7.1.2. MODIFIED STARCH

12.7.1.3. STARCH HYDROLYSATE

12.7.1.4. STARCH OLIGOSACCHARIDE DERIVATIVES

12.7.1.5. OTHERS

12.8 OTHERS

13 GLOBAL INDUSTRIAL STARCH MARKET, BY DISTRIBUTION CHANNEL

13.1 OVERVIEW

13.2 DIRECT

13.3 INDIRECT

14 GLOBAL INDUSTRIAL STARCH MARKET , BY GEOGRAPHY

14.1 OVERVIEW (ALL SEGMENTATION PROVIDED ABOVE IS REPRESNTED IN THIS CHAPTER BY COUNTRY)

14.2 NORTH AMERICA

14.2.1 U.S.

14.2.2 CANADA

14.2.3 MEXICO

14.3 EUROPE

14.3.1 GERMANY

14.3.2 U.K.

14.3.3 ITALY

14.3.4 FRANCE

14.3.5 SPAIN

14.3.6 SWITZERLAND

14.3.7 NETHERLANDS

14.3.8 BELGIUM

14.3.9 RUSSIA

14.3.10 TURKEY

14.3.11 REST OF EUROPE

14.4 ASIA-PACIFIC

14.4.1 JAPAN

14.4.2 CHINA

14.4.3 SOUTH KOREA

14.4.4 INDIA

14.4.5 AUSTRALIA

14.4.6 SINGAPORE

14.4.7 THAILAND

14.4.8 INDONESIA

14.4.9 MALAYSIA

14.4.10 PHILIPPINES

14.4.11 REST OF ASIA-PACIFIC

14.5 SOUTH AMERICA

14.5.1 BRAZIL

14.5.2 ARGENTINA

14.5.3 REST OF SOUTH AMERICA

14.6 MIDDLE EAST AND AFRICA

14.6.1 SOUTH AFRICA

14.6.2 UAE

14.6.3 SAUDI ARABIA

14.6.4 KUWAIT

14.6.5 REST OF MIDDLE EAST AND AFRICA

15 GLOBAL INDUSTRIAL STARCH MARKET , COMPANY LANDSCAPE

15.1 COMPANY SHARE ANALYSIS: GLOBAL

15.2 COMPANY SHARE ANALYSIS: NORTH AMERICA

15.3 COMPANY SHARE ANALYSIS: EUROPE

15.4 COMPANY SHARE ANALYSIS: ASIA-PACIFIC

15.5 MERGERS & ACQUISITIONS

15.6 NEW PRODUCT DEVELOPMENT & APPROVALS

15.7 EXPANSIONS & PARTNERSHIP

15.8 REGULATORY CHANGES

16 GLOBAL INDUSTRIAL STARCH MARKET , SWOT & DBMR ANALYSIS

17 GLOBAL INDUSTRIAL STARCH MARKET , COMPANY PROFILE

(SWOT AND DBMR ANALYSIS OF TOP COMPANIES WILL BE PROVIDED)

17.1 CARGILL,INCORPORATED

17.1.1 COMPANY OVERVIEW

17.1.2 REVENUE ANALYSIS

17.1.3 PRODUCT PORTFOLIO

17.1.4 GEOGRAPHIC PRESENCE

17.1.5 RECENT DEVELOPMENTS

17.2 ADM

17.2.1 COMPANY OVERVIEW

17.2.2 REVENUE ANALYSIS

17.2.3 PRODUCT PORTFOLIO

17.2.4 GEOGRAPHIC PRESENCE

17.2.5 RECENT DEVELOPMENTS

17.3 INGREDION, INCORPORATED

17.3.1 COMPANY OVERVIEW

17.3.2 REVENUE ANALYSIS

17.3.3 PRODUCT PORTFOLIO

17.3.4 GEOGRAPHIC PRESENCE

17.3.5 RECENT DEVELOPMENTS

17.4 TATE AND LYLE

17.4.1 COMPANY OVERVIEW

17.4.2 REVENUE ANALYSIS

17.4.3 PRODUCT PORTFOLIO

17.4.4 GEOGRAPHIC PRESENCE

17.4.5 RECENT DEVELOPMENTS

17.5 AGRANA BETEILIGUNGS-AG

17.5.1 COMPANY OVERVIEW

17.5.2 REVENUE ANALYSIS

17.5.3 PRODUCT PORTFOLIO

17.5.4 GEOGRAPHIC PRESENCE

17.5.5 RECENT DEVELOPMENTS

17.6 HL AGRO PRODUCTS PVT. LTD.

17.6.1 COMPANY OVERVIEW

17.6.2 REVENUE ANALYSIS

17.6.3 PRODUCT PORTFOLIO

17.6.4 GEOGRAPHIC PRESENCE

17.6.5 RECENT DEVELOPMENTS

17.7 SPAC STARCH PRODUCTS (INDIA) PRIVATE LIMITED

17.7.1 COMPANY OVERVIEW

17.7.2 REVENUE ANALYSIS

17.7.3 PRODUCT PORTFOLIO

17.7.4 GEOGRAPHIC PRESENCE

17.7.5 RECENT DEVELOPMENTS

17.8 TEREOS

17.8.1 COMPANY OVERVIEW

17.8.2 REVENUE ANALYSIS

17.8.3 PRODUCT PORTFOLIO

17.8.4 GEOGRAPHIC PRESENCE

17.8.5 RECENT DEVELOPMENTS

17.9 MANILDRA GROUP

17.9.1 COMPANY OVERVIEW

17.9.2 REVENUE ANALYSIS

17.9.3 PRODUCT PORTFOLIO

17.9.4 GEOGRAPHIC PRESENCE

17.9.5 RECENT DEVELOPMENTS

17.1 MGP

17.10.1 COMPANY OVERVIEW

17.10.2 REVENUE ANALYSIS

17.10.3 PRODUCT PORTFOLIO

17.10.4 GEOGRAPHIC PRESENCE

17.10.5 RECENT DEVELOPMENTS

17.11 GULSHAN POLYOLS LTD

17.11.1 COMPANY OVERVIEW

17.11.2 REVENUE ANALYSIS

17.11.3 PRODUCT PORTFOLIO

17.11.4 GEOGRAPHIC PRESENCE

17.11.5 RECENT DEVELOPMENTS

17.12 ROQUETTE FRÈRES

17.12.1 COMPANY OVERVIEW

17.12.2 REVENUE ANALYSIS

17.12.3 PRODUCT PORTFOLIO

17.12.4 GEOGRAPHIC PRESENCE

17.12.5 RECENT DEVELOPMENTS

17.13 THAI FLOUR INDUSTRY CO., LTD

17.13.1 COMPANY OVERVIEW

17.13.2 REVENUE ANALYSIS

17.13.3 PRODUCT PORTFOLIO

17.13.4 GEOGRAPHIC PRESENCE

17.13.5 RECENT DEVELOPMENTS

17.14 AMYLCO LLC

17.14.1 COMPANY OVERVIEW

17.14.2 REVENUE ANALYSIS

17.14.3 PRODUCT PORTFOLIO

17.14.4 GEOGRAPHIC PRESENCE

17.14.5 RECENT DEVELOPMENTS

17.15 SPAC STARCH PRODUCTS (INDIA) LTD.

17.15.1 COMPANY OVERVIEW

17.15.2 REVENUE ANALYSIS

17.15.3 PRODUCT PORTFOLIO

17.15.4 GEOGRAPHIC PRESENCE

17.15.5 RECENT DEVELOPMENTS

17.16 ALTIA INDUSTRIAL SERVICES

17.16.1 COMPANY OVERVIEW

17.16.2 REVENUE ANALYSIS

17.16.3 PRODUCT PORTFOLIO

17.16.4 GEOGRAPHIC PRESENCE

17.16.5 RECENT DEVELOPMENTS

17.17 STARPRO

17.17.1 COMPANY OVERVIEW

17.17.2 REVENUE ANALYSIS

17.17.3 PRODUCT PORTFOLIO

17.17.4 GEOGRAPHIC PRESENCE

17.17.5 RECENT DEVELOPMENTS

17.18 STARCH ASIA

17.18.1 COMPANY OVERVIEW

17.18.2 REVENUE ANALYSIS

17.18.3 PRODUCT PORTFOLIO

17.18.4 GEOGRAPHIC PRESENCE

17.18.5 RECENT DEVELOPMENTS

17.19 ASIA MODIFIED STARCH CO., LTD.

17.19.1 COMPANY OVERVIEW

17.19.2 REVENUE ANALYSIS

17.19.3 PRODUCT PORTFOLIO

17.19.4 GEOGRAPHIC PRESENCE

17.19.5 RECENT DEVELOPMENTS

17.2 NOVIDON NETHERLANDS

17.20.1 COMPANY OVERVIEW

17.20.2 REVENUE ANALYSIS

17.20.3 PRODUCT PORTFOLIO

17.20.4 GEOGRAPHIC PRESENCE

17.20.5 RECENT DEVELOPMENTS

17.21 SÜDZUCKER AG

17.21.1 COMPANY OVERVIEW

17.21.2 REVENUE ANALYSIS

17.21.3 PRODUCT PORTFOLIO

17.21.4 GEOGRAPHIC PRESENCE

17.21.5 RECENT DEVELOPMENTS

*NOTE: THE COMPANIES PROFILED IS NOT EXHAUSTIVE LIST AND IS AS PER OUR PREVIOUS CLIENT REQUIREMENT. WE PROFILE MORE THAN 100 COMPANIES IN OUR STUDY AND HENCE THE LIST OF COMPANIES CAN BE MODIFIED OR REPLACED ON REQUEST

18 RELATED REPORTS

19 QUESTIONNAIRE

20 ABOUT DATA BRIDGE MARKET RESEARCH

Global Industrial Starch Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Industrial Starch Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Industrial Starch Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.