Global Infrastructure Monitoring Market

Market Size in USD Billion

CAGR :

%

USD

7.53 Billion

USD

27.47 Billion

2025

2033

USD

7.53 Billion

USD

27.47 Billion

2025

2033

| 2026 –2033 | |

| USD 7.53 Billion | |

| USD 27.47 Billion | |

| % | |

|

Infrastructure Monitoring Market Size

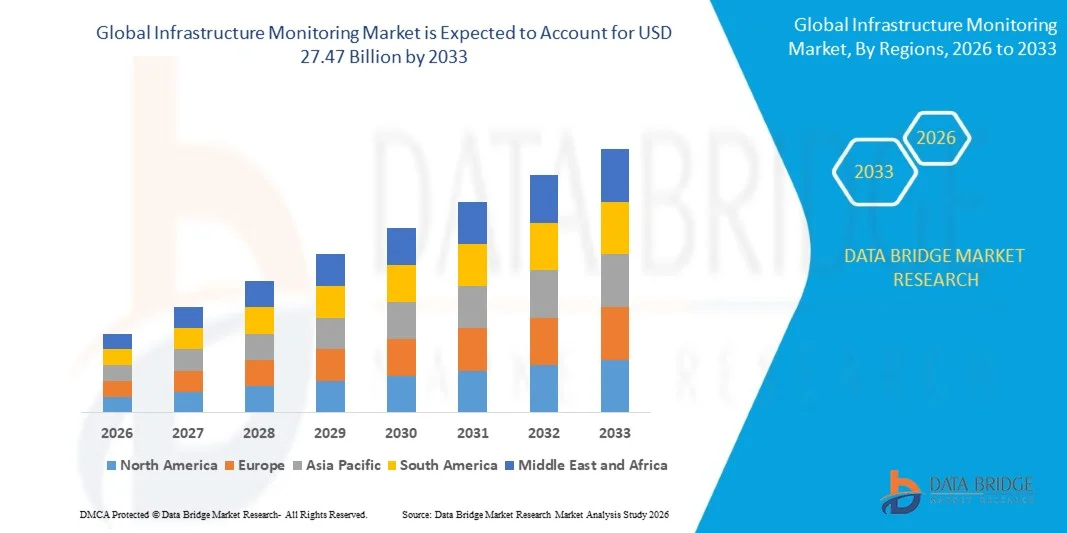

- The global infrastructure monitoring market size was valued at USD 7.53 billion in 2025 and is expected to reach USD 27.47 billion by 2033, at a CAGR of 17.55% during the forecast period

- The market growth is largely fueled by the increasing adoption of IoT-enabled devices, advanced sensors, and real-time analytics, leading to enhanced visibility and control across industrial, IT, and civil infrastructure systems

- Furthermore, rising enterprise demand for predictive maintenance, operational efficiency, and risk mitigation is driving the deployment of integrated monitoring solutions. These converging factors are accelerating the adoption of infrastructure monitoring systems, thereby significantly boosting the market’s growth

Infrastructure Monitoring Market Analysis

- Infrastructure monitoring solutions encompass hardware, software, and services that enable real-time tracking, condition assessment, and performance management of assets across sectors such as IT, manufacturing, civil, and transportation. These systems integrate sensors, cloud platforms, and analytics tools to provide actionable insights for optimizing operations, ensuring safety, and reducing downtime

- The escalating demand for infrastructure monitoring is primarily fueled by digital transformation initiatives, increasing investments in smart cities and industrial automation, and growing regulatory requirements for safety, efficiency, and compliance across critical infrastructure sectors

- North America dominated the infrastructure monitoring market with a share of 29.90% in 2025, due to increasing investments in IT infrastructure, smart buildings, and industrial automation

- Asia-Pacific is expected to be the fastest growing region in the infrastructure monitoring market during the forecast period due to rapid urbanization, industrial expansion, and government investments in smart and resilient infrastructure

- Hardware segment dominated the market with a market share of 59.3% in 2025, due to the critical role of physical devices such as sensors, servers, and network equipment in ensuring accurate real-time monitoring and data collection. Hardware components provide the foundation for infrastructure monitoring systems, enabling seamless integration with software platforms and services for analytics and reporting

Report Scope and Infrastructure Monitoring Market Segmentation

|

Attributes |

Infrastructure Monitoring Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Infrastructure Monitoring Market Trends

“Increasing Adoption of IoT-Enabled Monitoring Solutions”

- A significant trend in the infrastructure monitoring market is the growing adoption of IoT-enabled devices, sensors, and cloud-connected platforms, driven by the rising need for real-time operational visibility, predictive maintenance, and data-driven decision-making across critical infrastructure sectors. This trend is reinforcing infrastructure monitoring as an essential tool for managing IT, civil, industrial, and transportation systems efficiently

- For instance, Cisco Systems and SolarWinds provide network and IT infrastructure monitoring solutions that integrate IoT sensors and real-time analytics, enabling enterprises to track system performance, detect anomalies, and maintain operational continuity. Such platforms enhance reliability, reduce downtime, and support strategic planning in complex environments

- The adoption of smart sensors and connected devices in industrial and manufacturing facilities is growing rapidly, with companies such as Datadog enabling real-time monitoring of servers, applications, and network infrastructure. These solutions help organizations proactively address faults, optimize resource usage, and improve overall operational efficiency

- Civil infrastructure projects are increasingly deploying structural health monitoring systems to ensure safety and longevity. Companies such as GEOKON and Campbell Scientific supply sensors and monitoring platforms for bridges, dams, and tunnels, allowing engineers to detect structural changes early and plan maintenance interventions

- The market is witnessing rising interest in cloud-based infrastructure monitoring solutions where real-time data from geographically distributed assets can be analyzed centrally. Providers such as Oracle Corporation and Inspirisys Solutions Limited offer scalable platforms that integrate software, hardware, and analytics to monitor IT and industrial systems continuously

- Integration of edge-compute technologies with monitoring systems is gaining momentum, as seen with Schneider Electric and Sixense, allowing localized data processing, faster anomaly detection, and reduced network latency. This is driving demand for advanced, connected infrastructure monitoring solutions across global industries

Infrastructure Monitoring Market Dynamics

Driver

“Rising Demand for Predictive Maintenance and Operational Efficiency”

- The increasing reliance on predictive maintenance and operational efficiency is driving the demand for infrastructure monitoring solutions, as organizations seek to minimize downtime, extend asset life, and optimize resource allocation across IT, industrial, and civil sectors

- For instance, Datadog and Netmagic Solutions provide monitoring platforms that enable predictive analytics for IT and data-center infrastructure, helping companies anticipate failures and improve service uptime. These capabilities reduce maintenance costs and enhance operational reliability

- Growing investments in smart city projects, transportation networks, and industrial automation are fueling the adoption of comprehensive monitoring systems. Companies such as Zabbix LLC. and Pure Technologies provide platforms that combine hardware sensors and software analytics to manage large-scale infrastructure assets efficiently

- The push for energy efficiency and sustainability in industrial and civil infrastructures is increasing the use of monitoring solutions to track consumption patterns, environmental conditions, and system performance. Organizations can implement timely interventions to conserve energy and comply with regulatory standards

- The rising complexity of infrastructure networks, coupled with the need for centralized oversight of distributed assets, is driving enterprises to adopt integrated monitoring solutions. Companies such as Paessler and Inspirisys Solutions Limited enable unified dashboards that provide actionable insights for faster decision-making and risk mitigation

Restraint/Challenge

“High Implementation Costs and Complexity”

- The infrastructure monitoring market faces challenges due to the high costs associated with deploying end-to-end monitoring solutions, including hardware sensors, software platforms, and integration services. These financial barriers can limit adoption, particularly for small and medium-sized enterprises

- For instance, implementing comprehensive monitoring systems from companies such as Campbell Scientific Inc. or GEOKON requires significant investment in sensors, data acquisition units, and analytics platforms. The complexity of integrating these systems into existing infrastructure further increases project timelines and expenses

- Specialized expertise is required to configure, maintain, and interpret data from monitoring systems, adding operational costs and dependency on skilled personnel. This challenge affects adoption rates in regions with limited technical resources

- In addition, the deployment of IoT-enabled monitoring solutions involves network security and data privacy considerations. Ensuring compliance with regulatory standards and protecting sensitive operational data adds further complexity and cost burdens

- Scaling monitoring systems for large or geographically dispersed infrastructure networks can be technically challenging, requiring robust data management and connectivity solutions. These factors collectively pose barriers to rapid market expansion despite growing demand

Infrastructure Monitoring Market Scope

The market is segmented on the basis of component, operating system, deployment, connectivity technology, and industry.

• By Component

On the basis of component, the infrastructure monitoring market is segmented into software, hardware, and services. The hardware segment dominated the largest market revenue share of 59.3% in 2025, driven by the critical role of physical devices such as sensors, servers, and network equipment in ensuring accurate real-time monitoring and data collection. Hardware components provide the foundation for infrastructure monitoring systems, enabling seamless integration with software platforms and services for analytics and reporting. The growing demand for robust, reliable, and high-performance monitoring solutions across IT, industrial, and civil sectors further supports the dominance of hardware. Enterprises prioritize hardware investments to enhance operational efficiency, prevent downtime, and maintain system integrity, reinforcing its leading market position.

The services segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for managed monitoring services, consultancy, and maintenance support. For instance, companies such as Schneider Electric offer infrastructure monitoring services that include predictive maintenance and performance optimization for clients across industries. Outsourced services allow organizations to leverage expert knowledge without heavy capital investment, making them attractive for small and medium enterprises. Increasing awareness about infrastructure resilience and operational efficiency is further boosting adoption of professional monitoring services.

• By Operating System

On the basis of operating system, the market is segmented into UNIX, LINUX, MS Windows, and MacOS. The LINUX segment held the largest market revenue share in 2025, owing to its high stability, security, and compatibility with open-source monitoring tools. LINUX-based infrastructure monitoring solutions support extensive customization, integration with cloud and on-premises systems, and strong community support for troubleshooting and updates. Enterprises favor LINUX platforms for mission-critical monitoring where reliability and cost efficiency are key priorities. The robustness and flexibility of LINUX operating systems make them a preferred choice for large-scale deployments across IT and industrial sectors.

The MS Windows segment is projected to witness the fastest CAGR from 2026 to 2033, driven by its widespread enterprise adoption and ease of integration with existing corporate IT ecosystems. For instance, Microsoft’s System Center Operations Manager provides comprehensive monitoring for Windows-based infrastructures, enabling automated alerting and reporting. The user-friendly interface, combined with strong vendor support and frequent updates, makes Windows-based monitoring solutions highly appealing for small and medium-sized organizations. Increasing reliance on Windows servers in corporate networks continues to drive the growth of this segment.

• By Deployment

On the basis of deployment, the infrastructure monitoring market is segmented into premises infrastructure and cloud-based infrastructure. The premises infrastructure segment dominated the largest market revenue share in 2025, owing to enterprises’ preference for on-site control, high data security, and compliance with industry regulations. Organizations with critical operations, such as data centers and energy plants, rely on on-premises monitoring for real-time alerts, redundancy management, and integration with existing IT systems. Premises-based deployments also offer low-latency data processing and direct control over hardware and software configurations.

The cloud-based infrastructure segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increasing adoption of cloud computing, IoT, and remote monitoring capabilities. For instance, IBM Cloud Monitoring provides scalable solutions for monitoring distributed infrastructures with centralized dashboards and AI-based analytics. Cloud deployments reduce upfront capital costs, enable rapid scalability, and allow organizations to access monitoring insights from anywhere. The flexibility and cost-effectiveness of cloud solutions continue to drive their accelerated adoption across various sectors.

• By Connectivity Technology

On the basis of connectivity technology, the market is segmented into wireless and wired. The wired segment held the largest market revenue share in 2025, driven by its reliability, minimal interference, and suitability for large-scale industrial and IT infrastructure monitoring. Wired connections ensure continuous data flow for critical systems, providing consistent performance for operations that require high uptime. Organizations often prefer wired solutions in facilities with dense infrastructure networks, ensuring stable and secure monitoring. The ability to integrate wired systems with existing sensor networks further strengthens its market position.

The wireless segment is projected to witness the fastest CAGR from 2026 to 2033, driven by the rising adoption of IoT-enabled devices, mobile monitoring, and flexible deployment needs. For instance, Honeywell’s wireless infrastructure monitoring solutions offer remote asset monitoring and predictive maintenance capabilities for civil and industrial applications. Wireless connectivity eliminates extensive cabling costs, simplifies installation, and enables scalability across distributed sites. Increasing demand for smart and connected infrastructure accelerates the adoption of wireless monitoring technologies.

• By Industry

On the basis of industry, the market is segmented into civil, IT, aerospace and defense, mining, marine, and transportation. The IT industry segment dominated the largest market revenue share in 2025, owing to the critical need for continuous monitoring of data centers, servers, and network infrastructure. Organizations depend on IT infrastructure monitoring to prevent downtime, optimize performance, and ensure secure operations across complex, distributed networks. The growing adoption of cloud computing, edge devices, and virtualization further reinforces the demand for advanced monitoring solutions. IT service providers also integrate infrastructure monitoring into managed services, strengthening the segment’s dominance.

The civil industry segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising investments in smart city projects, public infrastructure, and urban development initiatives. For instance, Siemens offers civil infrastructure monitoring solutions for bridges, tunnels, and urban utilities to ensure safety and operational efficiency. The focus on predictive maintenance, structural health monitoring, and real-time reporting drives demand in this sector. Increasing government regulations for infrastructure safety and modernization support the accelerated adoption of monitoring solutions in civil applications.

Infrastructure Monitoring Market Regional Analysis

- North America dominated the infrastructure monitoring market with the largest revenue share of 29.90% in 2025, driven by increasing investments in IT infrastructure, smart buildings, and industrial automation

- Organizations in the region prioritize real-time monitoring, predictive maintenance, and operational efficiency across commercial and critical infrastructure. This widespread adoption is further supported by advanced technological ecosystems, high digital literacy, and the growing need for reliable, secure, and scalable monitoring solutions

- Enterprises increasingly implement integrated software-hardware platforms to enhance system uptime, manage risk, and comply with regulatory standards, reinforcing the region’s market leadership

U.S. Infrastructure Monitoring Market Insight

The U.S. infrastructure monitoring market captured the largest revenue share in North America in 2025, driven by rapid adoption of IoT-enabled monitoring, cloud-based platforms, and advanced analytics solutions. Enterprises are focusing on enhancing operational reliability, reducing downtime, and improving resource management through real-time monitoring systems. The growing trend of smart city initiatives, along with investments in critical IT and industrial infrastructure, fuels demand. In addition, government programs supporting digital infrastructure, coupled with rising awareness of predictive maintenance benefits, contribute significantly to market expansion.

Europe Infrastructure Monitoring Market Insight

The Europe infrastructure monitoring market is projected to expand at a substantial CAGR during the forecast period, driven by stringent regulatory requirements, urbanization, and the adoption of smart and resilient infrastructure. The demand for reliable monitoring solutions spans residential, commercial, and industrial sectors, with increasing integration of IoT devices and cloud platforms. European organizations prioritize system efficiency, energy optimization, and proactive maintenance to meet sustainability targets and operational standards. The growing emphasis on digital transformation in public and private infrastructure further strengthens the market.

U.K. Infrastructure Monitoring Market Insight

The U.K. market is expected to grow at a notable CAGR, fueled by increased investment in smart city projects and modernized commercial infrastructure. Enterprises and government agencies are adopting integrated monitoring systems for energy, IT, and civil infrastructure to enhance safety and operational performance. The robust IT and telecommunications infrastructure in the U.K. supports seamless deployment of monitoring solutions, while regulatory compliance and sustainability initiatives encourage technology adoption.

Germany Infrastructure Monitoring Market Insight

Germany’s infrastructure monitoring market is projected to expand at a significant CAGR, driven by strong industrial automation, technological innovation, and demand for energy-efficient solutions. The country emphasizes reliability, safety, and sustainability across civil and industrial infrastructures, which promotes monitoring system adoption. Integration with IoT-enabled platforms and predictive analytics solutions further supports efficient infrastructure management. Germany’s commitment to Industry 4.0 initiatives and smart buildings accelerates market growth.

Asia-Pacific Infrastructure Monitoring Market Insight

The Asia-Pacific market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rapid urbanization, industrial expansion, and government investments in smart and resilient infrastructure. Countries such as China, Japan, and India are focusing on digitization, smart cities, and connected industrial facilities, fueling demand for monitoring solutions. The growing awareness of predictive maintenance, operational efficiency, and system reliability accelerates adoption. In addition, local manufacturing of monitoring hardware and software solutions improves affordability and accessibility, broadening market penetration.

Japan Infrastructure Monitoring Market Insight

Japan’s market growth is driven by high technological adoption, industrial automation, and demand for real-time monitoring across critical infrastructure. Integration with IoT, AI-based analytics, and smart building systems is increasing, while enterprises prioritize operational safety, energy efficiency, and predictive maintenance. The aging workforce also boosts demand for automated, user-friendly monitoring systems across residential and industrial applications.

China Infrastructure Monitoring Market Insight

China accounted for the largest revenue share in Asia-Pacific in 2025, fueled by government-led smart city initiatives, rapid urbanization, and expanding industrial and commercial infrastructure. The country’s focus on digitization, IoT integration, and predictive monitoring drives adoption. Affordable solutions from domestic manufacturers, combined with strong technological infrastructure, support widespread deployment across residential, commercial, and industrial sectors, propelling market growth.

Infrastructure Monitoring Market Share

The infrastructure monitoring industry is primarily led by well-established companies, including:

- Cisco Systems (U.S.)

- Nagios (U.S.)

- SolarWinds Worldwide LLC. (U.S.)

- Inspirisys Solutions Limited (India)

- Datadog Inc. (U.S.)

- Oracle Corporation (U.S.)

- Netmagic Solutions (India)

- Zabbix LLC. (Latvia)

- Pure Technologies (Canada)

- Sixense (U.S.)

- GEOKON (U.S.)

- First Sensor AG (Germany)

- COWI A/S (Denmark)

- Sisgeo S.r.l (Italy)

- Geomotion Singapore (Singapore)

- Campbell Scientific Inc. (U.S.)

- Acellent Technologies, Inc. (U.S.)

- AVT Reliability Ltd. (U.K.)

- Paessler (Germany)

Latest Developments in Global Infrastructure Monitoring Market

- In May 2025, DP World pledged USD 2.5 billion for logistics-infrastructure upgrades, embedding end-to-end sensor suites to enhance supply-chain visibility. This significant investment is expected to strengthen the infrastructure monitoring market by driving demand for real-time tracking, IoT-enabled sensors, and data analytics solutions. Enhanced visibility across logistics operations enables predictive maintenance, operational efficiency, and risk mitigation, encouraging adoption of advanced monitoring systems across ports and transportation networks

- In April 2025, Siemens inaugurated a USD 190 million facility in Fort Worth to localize production of AI-ready electrical equipment for data-center and infrastructure clients. This expansion is likely to accelerate market growth by increasing the availability of AI-integrated monitoring hardware and supporting edge-compute applications. Localized production reduces lead times, improves customization for enterprise clients, and promotes adoption of intelligent monitoring solutions in both commercial and industrial infrastructures

- In March 2025, Schneider Electric unveiled the Modicon M660 IPC motion controller and Altivar Process ATV6100 drive, deepening edge-compute integration in monitoring systems. This development strengthens the infrastructure monitoring market by enabling more precise, real-time data acquisition and control at the edge. Enterprises benefit from enhanced automation, predictive maintenance capabilities, and energy efficiency improvements, driving adoption of next-generation monitoring solutions across industrial, IT, and civil infrastructures

- In February 2025, Indutrade completed 16 acquisitions spanning sensors and civil-infrastructure services, broadening its monitoring portfolio. This consolidation is expected to expand the market’s technology offerings, providing integrated solutions for infrastructure monitoring and boosting competitiveness. The acquisitions enable Indutrade to offer end-to-end monitoring services, promoting adoption across civil, industrial, and commercial sectors while supporting growth in emerging markets

- In February 2022, Siemens and Desert Technologies launched a joint venture to develop solar and smart infrastructure by providing clean, reliable, and affordable energy in the MEA and Asia regions. This collaboration impacts the infrastructure monitoring market by driving demand for smart energy and renewable monitoring systems. Integration of solar and IoT-enabled solutions supports predictive maintenance, operational efficiency, and sustainable infrastructure, fostering adoption of advanced monitoring technologies across emerging regions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Infrastructure Monitoring Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Infrastructure Monitoring Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Infrastructure Monitoring Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.