Global Inherited Retinal Diseases Market

Market Size in USD Billion

USD

21.74 Billion

USD

39.94 Billion

2024

2032

USD

21.74 Billion

USD

39.94 Billion

2024

2032

| 2025 - 2032 | |

| USD 21.74 Billion | |

| USD 39.94 Billion | |

| % | |

|

Inherited Retinal Diseases Market Size

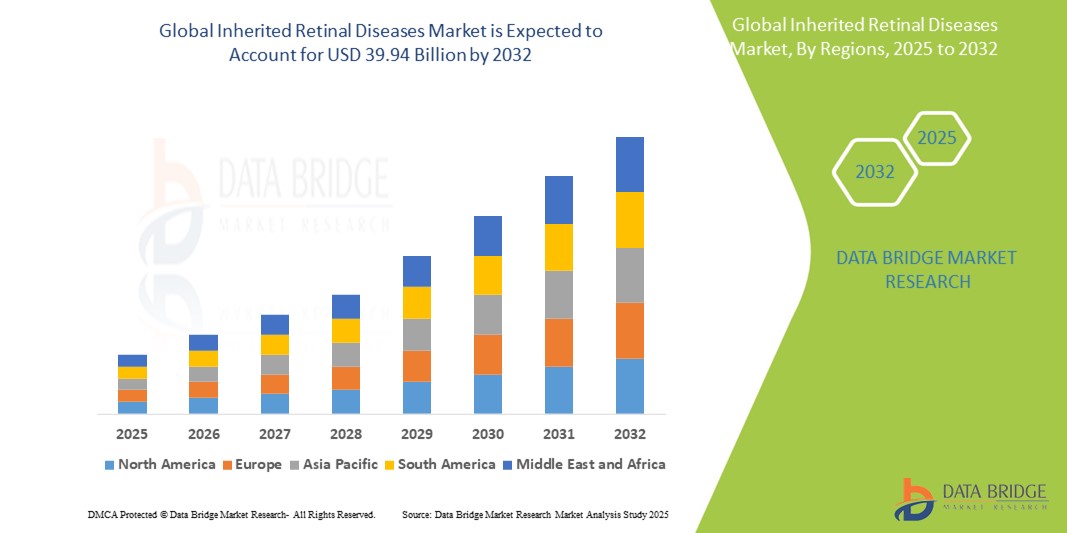

- The global inherited retinal diseases market size was valued at USD 21.74% Billion in 2024 and is expected to reach USD 39.94 Billion by 2032, at a CAGR of 7.90% during the forecast period

- The market growth is primarily driven by the increasing demand for innovative therapies and diagnostic solutions targeting genetic mutations responsible for vision impairment and blindness. Inherited retinal diseases (IRDs), including conditions such as retinitis pigmentosa, Leber congenital amaurosis, and Stargardt disease, are gaining increased attention due to advancements in gene therapy, making IRD treatment a rapidly evolving area within ophthalmology and precision medicine

- Furthermore, the rising prevalence of rare genetic eye disorders, along with growing investment in genomic research and personalized medicine, is contributing to the expansion of the IRD market. Enhanced diagnostic tools such as next-generation sequencing (NGS) and the emergence of CRISPR-based gene-editing technologies are facilitating earlier and more accurate identification of inherited retinal conditions, driving adoption across both clinical and research settings

Inherited Retinal Diseases Market Analysis

- The inherited retinal diseases market is witnessing substantial growth, primarily driven by increasing awareness, advancements in genetic diagnostics, and the growing need for targeted therapies to treat rare retinal disorders. Innovations in gene therapy and retinal implants are further accelerating market expansion by offering hope to patients with previously untreatable genetic vision conditions

- The growing emphasis on personalized medicine and advancements in genomic technologies is increasing the demand for accurate and early diagnosis of IRDs. Tools such as next-generation sequencing (NGS), CRISPR gene editing, and adeno-associated virus (AAV)-based gene delivery systems are contributing significantly to the development of novel treatment approaches tailored to individual genetic profiles

- North America dominated the global inherited retinal diseases market, with the largest revenue share of 38.9% in 2024. This leadership is due to the region’s strong healthcare infrastructure, high prevalence of retinal diseases, robust R&D funding, and the presence of key players actively engaged in gene therapy trials

- Asia-Pacific is projected to be the fastest-growing region in the global inherited retinal diseases market during the forecast period (2025–2032), driven by increasing investments in healthcare infrastructure, growing awareness of genetic eye disorders, improved access to genetic testing, and the emergence of research collaborations in countries such as China, India, and Japan

- Retinitis Pigmentosa dominated the disease type segment, with a market share of 41.2% share in 2024. Its high prevalence among inherited retinal conditions, coupled with focused research efforts and targeted gene therapies, makes it the most extensively studied and treated IRD subtype, driving its leading position in the market

Report Scope and Inherited Retinal Diseases Market Segmentation

|

Attributes |

Inherited Retinal Diseases Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Inherited Retinal Diseases Market Trends

“Technological Advancements Driving Precision and Efficiency”

- A significant and accelerating trend in the global inherited retinal diseases market is the growing integration of advanced genetic testing platforms and imaging technologies into clinical workflows. These innovations are greatly improving diagnostic precision, enabling earlier detection of genetic mutations responsible for retinal degeneration, and enhancing patient eligibility for emerging gene and cell therapies

- For instance, next-generation sequencing (NGS) panels customized for retinal disorders are increasingly used by specialized ophthalmic clinics and research institutions. These tools allow simultaneous analysis of multiple IRD-related genes, accelerating diagnosis while minimizing the need for invasive procedures and trial-and-error testing

- Advancements in retinal imaging systems, such as optical coherence tomography (OCT) and adaptive optics scanning laser ophthalmoscopy (AOSLO), enable high-resolution, non-invasive visualization of retinal layers and photoreceptors. These technologies are instrumental in monitoring disease progression, evaluating treatment efficacy, and supporting patient selection in gene therapy trials

- The integration of genetic diagnostics with electronic health record (EHR) systems is facilitating seamless data access and management across multidisciplinary teams. This centralized approach enhances patient monitoring, supports clinical decision-making, and improves care coordination in complex IRD cases

- As ophthalmic research laboratories and clinics move toward more data-driven and automation-capable environments, manufacturers such as Novartis, Spark Therapeutics, and Roche are expanding their diagnostic and therapeutic platforms. These expansions focus on scalable precision medicine solutions tailored to the unique genetic makeup of each IRD patient

- The demand for advanced, integrated diagnostic and monitoring systems is rising rapidly across academic hospitals, specialty clinics, and commercial gene therapy providers. This trend is redefining standards in retinal care, accelerating time-to-treatment, and boosting confidence in long-term therapeutic outcomes

Inherited Retinal Diseases Market Dynamics

Driver

“Growing Need for Accurate Genetic Diagnosis and Targeted Therapies”

- The rising prevalence of rare inherited retinal disorders, combined with advancements in genomic medicine, has significantly increased the demand for accurate, early-stage genetic testing. Inherited Retinal Diseases (IRDs) require precise molecular diagnosis to guide eligibility for gene therapies and targeted treatment strategies, making next-generation sequencing (NGS) and gene panels essential tools in ophthalmology

- For instance, in February 2024, Roche expanded its IRD diagnostic portfolio with a rapid genetic testing solution co-developed with a leading genomics lab, aimed at improving diagnosis timelines and patient access to emerging gene therapies. Such initiatives are expected to drive significant market growth in the coming years

- As personalized medicine becomes a standard in ophthalmic care, regulatory agencies and payers are pushing for genotype-based treatment alignment. This trend is reinforcing the integration of IRD testing into standard clinical workflows

- Moreover, the increasing number of clinical trials for IRD treatments—particularly gene and cell therapies—necessitates precise patient stratification, further positioning advanced diagnostic technologies as a cornerstone of therapeutic development and clinical success

- The expanding use of telemedicine and remote diagnostics in retinal care is also boosting demand for digital tools and portable genetic testing kits, increasing reach in underserved and rural populations

Restraint/Challenge

“High Costs of Genetic Testing and Limited Access in Low-Income Regions”

- Despite technological advancements, the high cost associated with comprehensive IRD genetic testing remains a key barrier, particularly in developing economies. Whole exome sequencing (WES) and targeted gene panels often require substantial investments in equipment, software, and skilled personnel

- For instance, small or community-based clinics may struggle to afford specialized testing platforms or to maintain bioinformatics support required for interpreting complex genetic data—limiting the widespread adoption of IRD diagnostics

- In addition, limited insurance coverage and reimbursement for rare disease diagnostics in many countries hinder accessibility for patients, creating disparities in early detection and treatment eligibility

- While some manufacturers are introducing low-cost test kits and direct-to-consumer platforms, these often lack the comprehensive genetic coverage needed for diagnosing a broad range of IRDs, leading to incomplete or inconclusive results

Inherited Retinal Diseases Market Scope

The market is segmented on the basis of disease type, type, end user, and distribution channel.

• By Disease Type

On the basis of disease type, the inherited retinal diseases market is segmented into retinitis pigmentosa, Stargardt’s disease, achromatopsia, cone-rod dystrophy, choroideremia, leber congenital amaurosis, macular edema, and others. The retinitis pigmentosa segment accounted for the largest market share of 41.2% in 2024, driven by high disease prevalence and significant clinical research activity focused on gene therapy. The increasing number of clinical trials and approvals for RP-targeted treatments is contributing to market dominance.

The leber congenital amaurosis segment is projected to witness the fastest growth from 2025 to 2032, propelled by early onset in patients, greater genetic understanding, and successful commercialization of gene therapies such as Luxturna. This trend reflects a shift toward early intervention in pediatric IRD cases.

• By Type

On the basis of type, the market is segmented into diagnosis and therapy. The diagnosis segment held the largest revenue share in 2024 due to the rising use of next-generation sequencing (NGS), genetic testing panels, and advanced imaging tools such as OCT for early detection and disease classification. Accurate diagnosis is key for selecting candidates for emerging gene therapies.

The therapy segment is expected to register the highest CAGR during the forecast period, driven by advancements in gene therapy, stem cell-based treatments, and pharmacological interventions aimed at slowing or reversing disease progression.

• By End-User

On the basis of end-user, the Inherited retinal diseases market is segmented into hospitals, specialty clinics, ambulatory surgical centers, home healthcare, and others. Hospitals dominated the market in 2024, supported by robust diagnostic infrastructure, access to gene therapy treatments, and a high patient inflow for IRD diagnosis and management.

The specialty clinics segment is expected to grow at the fastest pace during 2025–2032, as more patients seek specialized care for rare retinal diseases, and as advanced therapeutic offerings such as gene and cell therapies become concentrated in these focused care settings.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into retail sales and direct tender. The retail sales segment accounted for the highest market share in 2024, owing to increased availability of diagnostic kits, supportive medications, and digital health solutions through pharmacies and online channels.

The direct tender segment is anticipated to grow rapidly, particularly in public healthcare institutions and government-supported programs, as large-scale genetic testing and therapy procurement initiatives are facilitated through direct contractual agreements.

Inherited Retinal Diseases Market Regional Analysis

- North America dominated the inherited retinal diseases market with the largest revenue share of 38.9% in 2024, driven by the region’s advanced healthcare infrastructure, extensive clinical research activities, and early access to gene and cell therapies for rare retinal conditions

- Leading academic institutions, specialized eye care centers, and biotechnology firms across the U.S. and Canada are at the forefront of IRD diagnosis and therapeutic innovation, supported by favorable regulatory pathways such as the FDA’s Orphan Drug Designation and fast-track approvals for rare diseases

- This regional dominance is further reinforced by the presence of major market players, active clinical trial networks, and strong collaborations between hospitals, research institutes, and pharmaceutical companies. High patient awareness, government-funded genetic testing initiatives, and access to advanced imaging and genomic diagnostics also contribute to market leadership in North America

U.S. Inherited Retinal Diseases Market Insight

The U.S. inherited retinal diseases market captured the largest revenue share of 82% in 2024 within North America, fueled by the country’s robust pharmaceutical and biotechnology infrastructure, substantial R&D investments, and early adoption of genetic diagnostics and therapies. The strong presence of key industry players, combined with the widespread integration of advanced technologies such as LIMS and automated workflows, is significantly enhancing IRD testing efficiency and precision. In addition, IRD testing is widely used in both academic and commercial pipelines, particularly in gene therapy development, further cementing the U.S. as a global leader in this domain.

Europe Inherited Retinal Diseases Market Insight

The Europe inherited retinal diseases market is projected to grow at a substantial CAGR of 7.6% from 2025 to 2032, driven by increasing investments in precision medicine and rare disease diagnostics. Countries such as Germany, France, and the U.K. are at the forefront, supported by strong research infrastructure, favorable regulatory environments, and a surge in clinical trials. The growing partnerships between academic institutions and CROs, alongside compliance with EMA standards, are propelling the adoption of advanced IRD solutions across the continent.

U.K. Inherited Retinal Diseases Market Insight

The U.K. inherited retinal diseases market is anticipated to grow at a noteworthy CAGR of 8.2% during the forecast period, bolstered by its established biomedical hubs in London, Cambridge, and Oxford. These centers of innovation are actively engaged in ophthalmic genetic research and development, supported by public–private partnerships and strong government backing. The presence of early access programs and a proactive healthcare ecosystem is further accelerating the country’s position in the IRD diagnostics and therapeutics space.

Germany Inherited Retinal Diseases Market Insight

The Germany inherited retinal diseases market is expected to expand at a considerable CAGR of 7.9% through 2032. Renowned for its pharmaceutical innovation and compliance with GMP standards, Germany remains a pivotal market for IRD diagnostics and treatments. Its advanced infrastructure for protein-binding studies and receptor-ligand research continues to attract global interest, further boosting the demand for precision IRD testing tools.

Asia-Pacific Inherited Retinal Diseases Market Insight

The Asia-Pacific inherited retinal diseases market is poised to grow at the fastest CAGR of 9.8% during the forecast period of 2025 to 2032, driven by expanding healthcare infrastructure, rising investment in biotech, and increasing awareness of genetic disorders. Countries such as China, Japan, and India are key contributors, supported by government-led initiatives to promote diagnostics, the proliferation of CROs, and the growing availability of affordable genetic testing technologies.

Japan Inherited Retinal Diseases Market Insight

The Japan inherited retinal diseases market is gaining momentum, projected to grow at a CAGR of 8.4% during the forecast period. With its strong base in ophthalmic research and rapid advancements in diagnostic automation, Japan stands as a leading player in the regional market. The country's aging population and demand for accurate genetic testing are key growth drivers, bolstered by government support and robust healthcare innovation.

China Inherited Retinal Diseases Market Insight

The China inherited retinal diseases market accounted for the largest market revenue share in Asia-Pacific in 2024, contributing 43% of the regional total. This dominance is attributed to China’s rapidly growing biotech and diagnostics sectors, supportive regulatory policies, and expanding middle class. The country’s strategic push toward smart healthcare and its flourishing domestic IRD diagnostics companies are solidifying its position as a regional and global market leader.

Inherited Retinal Diseases Market Share

The inherited retinal diseases industry is primarily led by well-established companies, including:

- Spark Therapeutics, Inc. (U.S.)

- Novartis AG (Switzerland)

- Okuvision (Germany)

- Nidek Co. Ltd. (Japan)

- Labcorp (U.S.)

- Carl Zeiss SE (Germany)

- Optos (U.K.)

- Neurosoft (Russia)

- LKC TECHNOLOGIES, INC. (U.S.)

- Astellas Pharma Inc. (Japan)

- REGENXBIO Inc. (U.S.)

- Ionis Pharmaceuticals, Inc. (U.S.)

- SparingVision (France)

- Ocugen Inc. (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Coave Therapeutics (U.S.)

- MeiraGTx Limited (U.K.)

- Gensight Biologics (France)

- ProQR Therapeutics (Netherlands)

- Bionic Vision Technologies (Australia)

Latest Developments in Global Inherited Retinal Diseases Market

- In April 2025, Thermo Fisher Scientific launched a new automated equilibrium dialysis system tailored for biologics research. It integrates robotic liquid handling and LIMS connectivity to ensure compliant data capture and significantly higher throughput—accelerating pharmacokinetic workflows

- In February 2024, Stratagem Market Insights released an in-depth report projecting IRD market trends through 2030, including segmental forecasts, competitive analysis of key players (such as Harvard Apparatus, Thermo Fisher, Merck, and BioDuro), and regional dynamics

- In May 2025, Opus Genetics presented emerging data on its IRD gene therapy programs at several medical conferences. The company showcased ongoing clinical progress and novel pipeline candidates, signaling growing momentum in gene-based IRD treatments

- In May 2025, researchers at the University of Pennsylvania unveiled advanced tools and platforms aimed at treating late-stage IRDs—highlighting more versatile gene therapy and regenerative strategies for severe conditions such as retinitis pigmentosa

- In May 2025, Beacon Therapeutics shared interim 6-month data from its Phase 2 trial of laru-zova for X-linked retinitis pigmentosa (XLRP). The results provide early insights into therapeutic efficacy and safety in this underserved patient subgroup

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.