Global Insomnia Market

Market Size in USD Billion

USD

6.15 Billion

USD

9.36 Billion

2025

2033

USD

6.15 Billion

USD

9.36 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.15 Billion | |

| USD 9.36 Billion | |

| % | |

|

Insomnia Market Size

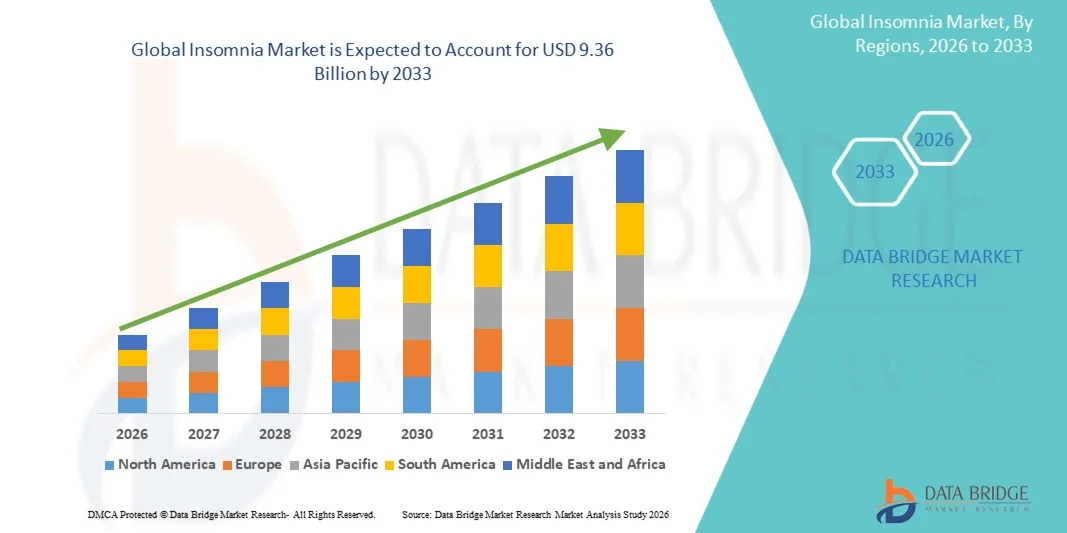

- The global insomnia market size was valued at USD 6.15 billion in 2025and is expected to reach USD 9.36 billion by 2033, at a CAGR of 5.40% during the forecast period

- The market growth is largely fueled by the increasing prevalence of sleep disorders and rising awareness about the importance of sleep health, leading to greater demand for effective diagnosis and treatment solutions across healthcare settings

- Furthermore, growing adoption of digital health tools, advancements in pharmacological and non-pharmacological therapies, and rising consumer preference for personalized and convenient treatment options are establishing insomnia solutions as essential components of modern healthcare. These converging factors are accelerating the uptake of insomnia treatments, thereby significantly boosting the industry's growth

Insomnia Market Analysis

- Insomnia treatments, including pharmacological therapies, cognitive behavioral therapy for insomnia (CBT-I), and digital therapeutics, are increasingly vital components of modern healthcare across hospitals, sleep clinics, and home care settings due to their ability to improve sleep quality and overall well-being

- The escalating demand for insomnia treatments is primarily fueled by rising stress levels, increasing prevalence of mental health disorders, growing awareness about sleep health, and a strong preference for effective and convenient treatment options

- North America dominated the insomnia market with the largest revenue share of 36.8% in 2025, characterized by advanced healthcare infrastructure, high awareness levels, and strong adoption of both prescription therapies and digital sleep solutions, with the U.S. experiencing substantial growth driven by ongoing innovations and increasing diagnosis rates

- Asia-Pacific is expected to be the fastest growing region in the Insomnia market during the forecast period due to rising urbanization, increasing work-related stress, growing middle-class population, and improving access to healthcare services

- The oral segment dominated the market with a revenue share of approximately 81.5% in 2025, driven by its convenience, ease of administration, and high patient compliance

Report Scope and Insomnia Market Segmentation

|

Attributes |

Insomnia Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Idorsia Pharmaceuticals Ltd. (Switzerland) · Eisai Co., Ltd. (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Pfizer Inc. (U.S.) · Eli Lilly and Company (U.S.) · Merck & Co., Inc. (U.S.) · Sanofi S.A. (France) · GlaxoSmithKline plc (U.K.) · Teva Pharmaceutical Industries Ltd. (Israel) · Sun Pharmaceutical Industries Ltd. (India) · Lupin Limited (India) · Aurobindo Pharma Limited (India) · Dr. Reddy’s Laboratories Ltd. (India) · Cipla Limited (India) · Zydus Lifesciences Ltd. (India) · Johnson & Johnson (U.S.) · Bristol-Myers Squibb Company (U.S.) · AbbVie Inc. (U.S.) · Amneal Pharmaceuticals, Inc. (U.S.) · Mylan N.V. (U.S.) |

|

Market Opportunities |

· Growing Demand for Digital Therapeutics and Sleep Apps · Rising Awareness and Diagnosis of Sleep Disorders |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Insomnia Market Trends

“Rising Adoption of Digital Therapeutics and Personalized Treatment Approaches”

- A significant and accelerating trend in the global Insomnia market is the increasing adoption of digital therapeutics and personalized treatment solutions aimed at improving sleep health outcomes. These innovations are transforming how insomnia is diagnosed, monitored, and managed across patient populations

- For instance, mobile-based cognitive behavioral therapy for insomnia (CBT-I) applications and wearable sleep trackers are enabling continuous monitoring of sleep patterns, allowing healthcare providers to tailor treatment strategies based on individual patient data

- The integration of digital health platforms with sleep management is facilitating remote patient engagement, improving adherence to therapy, and reducing dependency on pharmacological interventions

- Furthermore, advancements in precision medicine are enabling clinicians to design customized treatment regimens based on genetic, behavioral, and lifestyle factors influencing sleep disorders

- The growing preference for non-pharmacological therapies, such as behavioral interventions and mindfulness-based treatments, is also shaping market trends, as patients seek safer and long-term solutions without side effects associated with sleep medications

- This shift toward personalized and technology-enabled care is significantly enhancing patient outcomes and redefining treatment standards in the insomnia market

Insomnia Market Dynamics

Driver

“Increasing Prevalence of Sleep Disorders and Growing Awareness of Mental Health”

- The rising global prevalence of sleep disorders, particularly insomnia, is a major factor driving market growth. Increasing stress levels, changing lifestyles, excessive screen time, and work-related pressures are contributing to a higher incidence of sleep disturbances across all age groups

- In addition, growing awareness regarding the importance of mental health and sleep quality is encouraging individuals to seek diagnosis and treatment, thereby boosting demand for insomnia therapies

- Governments and healthcare organizations are actively promoting sleep health awareness campaigns, which is further supporting early diagnosis and treatment adoption

- The expanding geriatric population, which is more prone to chronic insomnia and comorbid conditions, is also significantly contributing to the increased demand for effective treatment options

- Moreover, the availability of a wide range of treatment options, including pharmacological therapies, behavioral therapies, and over-the-counter sleep aids, is enhancing accessibility and driving market expansion

- The continuous development of novel therapeutics with improved efficacy and safety profiles is further strengthening the growth trajectory of the insomnia market

Restraint/Challenge

“Concerns Regarding Side Effects of Medications and Underdiagnosis of Insomnia”

- Concerns surrounding the cybersecurity vulnerabilities of connected devices, including smart locks, pose a significant challenge to broader market penetration. As smart locks rely on network connectivity and software, they are susceptible to hacking attempts and data breaches, raising anxieties among potential consumers about the security of their homes and data

- For instance, high-profile reports of vulnerabilities in IoT devices have made some consumers hesitant to adopt smart home security solutions, including smart locks

- Addressing these cybersecurity concerns through robust encryption, secure authentication protocols, and regular software updates is crucial for building consumer trust. Companies such as August and Level Home emphasize their advanced encryption methods and security features in their marketing to reassure potential buyers. In addition, the relatively high initial cost of some advanced Insomnia systems compared to traditional locks can be a barrier to adoption for price-sensitive consumers, particularly in developing regions or for budget-conscious homeowners. While basic smart locks from brands such as Wyze have become more affordable, premium features such as integrated cameras or advanced biometric scanning often come with a higher price tag

- While prices are gradually decreasing, the perceived premium for smart technology can still hinder widespread adoption, especially for those who do not see an immediate need for the advanced features offered

- Overcoming these challenges through enhanced cybersecurity measures, consumer education on security best practices, and the development of more affordable Insomnia options will be vital for sustained market growth

Insomnia Market Scope

The market is segmented on the basis of therapy type, drug class, route of administration, end-users, and distribution channel.

- By Therapy Type

On the basis of therapy type, the Insomnia market is segmented into non-pharmacological and pharmacological therapy. The pharmacological therapy segment dominated the largest market revenue share of approximately 62.3% in 2025, driven by the widespread use of prescription medications for immediate symptom relief. Patients with moderate to severe insomnia often rely on drug-based treatments due to their faster onset of action and effectiveness in improving sleep quality. Increasing prevalence of sleep disorders globally has significantly contributed to the demand for pharmacological solutions. Growing awareness among patients regarding available treatment options further supports segment dominance. Physicians often prescribe medications as first-line treatment in acute cases, boosting usage. Advancements in drug formulations with fewer side effects have enhanced patient compliance. Rising stress levels and lifestyle changes also increase dependency on medication-based therapies. Strong presence of branded and generic drugs in the market ensures accessibility. Expanding healthcare infrastructure in emerging regions further supports adoption. Continuous research and development in sleep therapeutics strengthens segment growth.

The non-pharmacological therapy segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, driven by increasing preference for safer and long-term treatment approaches. Therapies such as cognitive behavioral therapy for insomnia (CBT-I) are gaining popularity due to their effectiveness without side effects. Rising awareness about the risks associated with prolonged drug use supports this shift. Healthcare providers are increasingly recommending behavioral therapies as first-line treatment for chronic insomnia. Growth in digital health platforms offering online CBT programs further accelerates adoption. Increasing patient inclination toward holistic and lifestyle-based treatments also drives demand. Government initiatives promoting mental health awareness contribute to segment growth. Expansion of sleep clinics and therapy centers enhances accessibility. Improved clinical outcomes and long-term benefits support wider acceptance. Continuous innovation in digital therapeutics further boosts market expansion.

- By Drug Class

On the basis of drug class, the market is segmented into melatonin antagonists, antidepressants, benzodiazepines, non-benzodiazepines, and others. The non-benzodiazepines segment held the largest market revenue share of around 36.7% in 2025, driven by their improved safety profile and lower risk of dependency compared to traditional benzodiazepines. Drugs such as zolpidem and eszopiclone are widely prescribed due to their effectiveness in inducing sleep with fewer side effects. Increasing physician preference for safer alternatives supports segment growth. Growing patient awareness regarding drug safety further boosts demand. The availability of multiple formulations enhances treatment flexibility. Favorable clinical guidelines recommending non-benzodiazepines also contribute to dominance. Rising number of insomnia cases globally increases prescription rates. Continuous product innovation improves efficacy and tolerability. Strong presence of generic versions ensures affordability. Expansion of healthcare services in emerging markets further supports adoption.

The melatonin antagonist segment is projected to witness the fastest CAGR of 10.6% from 2026 to 2033, driven by increasing demand for drugs that regulate the sleep-wake cycle. These drugs target specific receptors, offering a novel mechanism of action with minimal side effects. Rising awareness about circadian rhythm disorders supports segment growth. Increasing adoption of personalized medicine further enhances demand. Pharmaceutical companies are investing in the development of advanced melatonin-based therapies. Favorable safety profiles make these drugs suitable for long-term use. Growing geriatric population with sleep disorders also contributes to expansion. Improved clinical outcomes and reduced dependency risks drive physician preference. Expanding regulatory approvals further boost market penetration. Continuous research and innovation strengthen future growth prospects.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral, parenteral, and others. The oral segment dominated the market with a revenue share of approximately 81.5% in 2025, driven by its convenience, ease of administration, and high patient compliance. Most insomnia medications are available in oral formulations such as tablets and capsules, making them widely accessible. Patients prefer oral drugs due to their non-invasive nature and ease of use. Increasing availability of over-the-counter sleep aids further supports segment dominance. Strong distribution through retail and online pharmacies enhances accessibility. Pharmaceutical companies focus on developing improved oral formulations with extended-release properties. Rising prevalence of chronic insomnia ensures continuous demand. Favorable reimbursement policies in developed markets also contribute to growth. High patient acceptance and familiarity with oral medications further strengthen the segment. Continuous innovation in drug delivery technologies enhances effectiveness.

The parenteral segment is expected to witness the fastest CAGR of 8.7% from 2026 to 2033, driven by its use in severe insomnia cases requiring immediate intervention. Parenteral administration provides rapid onset of action, making it suitable for hospital settings. Increasing use in emergency and critical care scenarios supports growth. Hospitals rely on injectable therapies for patients who cannot take oral medications. Advancements in formulation technologies improve safety and efficacy. Growing number of hospital admissions due to sleep-related complications further boosts demand. Expansion of healthcare infrastructure in developing regions enhances accessibility. Increasing focus on acute care management contributes to segment growth. Continuous innovation in injectable therapies supports adoption. Rising awareness among healthcare professionals further accelerates market expansion.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment accounted for the largest market revenue share of approximately 49.8% in 2025, driven by the availability of advanced diagnostic and treatment facilities. Hospitals serve as primary centers for managing severe and chronic insomnia cases. Presence of specialized healthcare professionals enhances treatment outcomes. Increasing patient visits for sleep disorders further supports segment growth. Hospitals also offer integrated care, including psychological and pharmacological treatments. Rising healthcare expenditure and infrastructure development contribute to dominance. Expansion of sleep disorder units within hospitals boosts adoption. Strong referral networks ensure consistent patient inflow. Availability of advanced monitoring technologies further strengthens the segment. Growing awareness about sleep health also drives hospital visits. Continuous investment in healthcare systems ensures sustained growth.

The homecare segment is anticipated to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by the growing preference for at-home treatment and self-care solutions. Patients increasingly opt for home-based therapies due to convenience and cost-effectiveness. Rising adoption of wearable sleep monitoring devices supports this trend. Increasing awareness about sleep hygiene and lifestyle management boosts demand. Growth in telemedicine and digital health platforms enhances accessibility. Patients prefer homecare for long-term management of insomnia. Expansion of over-the-counter sleep aids further supports segment growth. Aging population with chronic sleep disorders contributes to demand. Continuous innovation in home-based treatment solutions accelerates adoption. Improved patient comfort and reduced hospital visits further drive expansion.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The retail pharmacy segment dominated the largest market revenue share of approximately 44.6% in 2025, driven by easy accessibility and widespread presence across urban and rural areas. Retail pharmacies serve as the primary point of purchase for both prescription and over-the-counter insomnia medications. Increasing consumer preference for convenient access to medicines supports segment growth. Strong distribution networks ensure product availability. Growing demand for OTC sleep aids further boosts sales. Retail pharmacies also benefit from direct patient interaction and guidance. Expansion of pharmacy chains enhances market reach. Rising healthcare awareness contributes to increased purchases. Competitive pricing and availability of generics further strengthen the segment. Continuous growth in pharmaceutical retail infrastructure supports dominance.

The online pharmacy segment is projected to witness the fastest CAGR of 11.5% from 2026 to 2033, driven by the rapid growth of e-commerce and digital healthcare platforms. Consumers increasingly prefer online channels for convenience, privacy, and competitive pricing. Expansion of internet penetration and smartphone usage supports segment growth. Online platforms offer a wide range of products and home delivery services. Increasing adoption of telemedicine further boosts online pharmacy demand. Regulatory support for e-pharmacy operations enhances market expansion. Growing awareness about digital healthcare solutions contributes to adoption. Discounts and subscription models attract more consumers. Rising preference for contactless purchasing post-pandemic accelerates growth. Continuous advancements in logistics and supply chain systems further support expansion.

Insomnia Market Regional Analysis

- North America dominated the insomnia market with the largest revenue share of 36.8% in 2025, characterized by advanced healthcare infrastructure, high awareness levels, and strong adoption of both prescription therapies and digital sleep solutions

- The region is witnessing increased utilization of pharmacological treatments such as sedative-hypnotics and melatonin receptor agonists, along with growing acceptance of cognitive behavioral therapy for insomnia (CBT-I)

- In addition, the rising prevalence of sleep disorders and increasing focus on mental health are further driving market growth, with the U.S. experiencing substantial expansion driven by ongoing innovations and increasing diagnosis rates

U.S. Insomnia Market Insight

The U.S. insomnia market captured the largest revenue share in 2025 within North America, fueled by the high prevalence of sleep disorders and strong adoption of advanced treatment options. Patients and healthcare providers are increasingly utilizing both prescription medications and digital therapeutics for effective sleep management. Furthermore, favorable reimbursement frameworks, extensive clinical research, and the presence of leading pharmaceutical companies are supporting market growth. The increasing use of wearable sleep trackers and mobile health applications is also contributing to improved diagnosis and personalized treatment approaches.

Europe Insomnia Market Insight

The Europe insomnia market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by growing awareness of sleep health and the increasing burden of lifestyle-related disorders. The region benefits from well-established healthcare systems and rising adoption of non-pharmacological therapies such as behavioral interventions. In addition, supportive government initiatives and increasing availability of specialized sleep clinics are fostering market growth across Europe.

U.K. Insomnia Market Insight

The U.K. insomnia market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of mental health and sleep disorders. The growing adoption of digital therapeutics and structured sleep programs, along with strong healthcare support systems, is encouraging early diagnosis and treatment. Moreover, rising stress levels and changing lifestyles are contributing to the growing demand for effective insomnia management solutions.

Germany Insomnia Market Insight

The Germany insomnia market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing healthcare expenditure and rising awareness regarding sleep-related disorders. Germany’s robust healthcare infrastructure and emphasis on innovation are promoting the adoption of advanced treatment options, including both pharmacological and behavioral therapies. In addition, the growing aging population and focus on improving quality of life are supporting sustained market growth.

Asia-Pacific Insomnia Market Insight

The Asia-Pacific insomnia market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rising urbanization, increasing work-related stress, growing middle-class population, and improving access to healthcare services. The region is witnessing increasing awareness of sleep health and expanding availability of treatment options. Government initiatives aimed at strengthening healthcare systems and addressing mental health issues are further contributing to market growth.

Japan Insomnia Market Insight

The Japan insomnia market is gaining momentum due to the country’s aging population and high prevalence of sleep disorders. The market is characterized by strong adoption of both prescription medications and non-pharmacological therapies. In addition, increasing awareness of sleep hygiene and continuous advancements in sleep medicine are supporting market expansion.

China Insomnia Market Insight

The China insomnia market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large population base and rising prevalence of sleep disorders. Increasing awareness regarding mental health and sleep-related issues, along with improving healthcare infrastructure, is driving market growth. Furthermore, the growing availability of affordable treatment options and expansion of digital health platforms are key factors propelling the market in China.

Insomnia Market Share

The Insomnia industry is primarily led by well-established companies, including:

- Idorsia Pharmaceuticals Ltd. (Switzerland)

- Eisai Co., Ltd. (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Merck & Co., Inc. (U.S.)

- Sanofi S.A. (France)

- GlaxoSmithKline plc (U.K.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Lupin Limited (India)

- Aurobindo Pharma Limited (India)

- Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Zydus Lifesciences Ltd. (India)

- Johnson & Johnson (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- AbbVie Inc. (U.S.)

- Amneal Pharmaceuticals, Inc. (U.S.)\

- Mylan N.V. (U.S.)

Latest Developments in Global Insomnia Market

- In February 2022, Idorsia announced that the U.S. FDA approved Quviviq (daridorexant) for the treatment of adult insomnia characterized by difficulties with sleep onset and/or sleep maintenance. The drug, a dual orexin receptor antagonist, introduced a novel mechanism targeting wakefulness pathways rather than sedation, marking a significant advancement in insomnia pharmacotherapy

- In May 2022, Idorsia confirmed the commercial launch of Quviviq (daridorexant) in the United States following regulatory approval, providing a new treatment option designed to improve both nighttime sleep and daytime functioning in insomnia patients

- In May 2022, the European Commission granted approval for daridorexant for the treatment of chronic insomnia in adults, expanding access to this next-generation therapy across European markets and reinforcing global adoption of orexin-targeting drugs

- In September 2024, Idorsia’s partner announced that Quviviq (daridorexant) received regulatory approval in Japan, enabling commercialization in the Asia-Pacific region and strengthening the global footprint of dual orexin receptor antagonist therapies

- In April 2025, scientific publications in Nature highlighted emerging insomnia treatments including next-generation orexin-targeting drugs, neuromodulation technologies, and wearable-based sleep interventions, indicating a shift toward non-sedative and technology-integrated therapies

- In September 2025, healthcare systems in the United Kingdom reported increasing prescription uptake of daridorexant, highlighting its positioning as a non-addictive alternative to traditional sleep medications and reflecting growing clinical acceptance despite cost-related adoption challenges

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.