Global Integrated Chronic Care Pathway Services Market

Market Size in USD Billion

USD

3.28 Billion

USD

10.67 Billion

2025

2033

USD

3.28 Billion

USD

10.67 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.28 Billion | |

| USD 10.67 Billion | |

| % | |

|

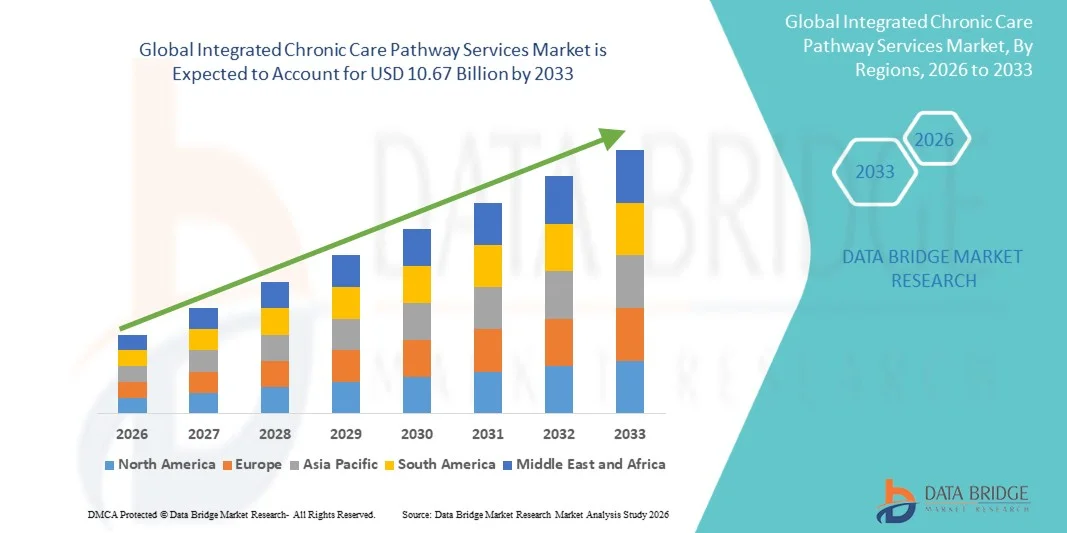

Integrated Chronic Care Pathway Services Market Size

- The global Integrated Chronic Care Pathway Services market size was valued at USD 3.28 billion in 2025 and is expected to reach USD 10.67 billion by 2033, at a CAGR of 15.90% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions, leading to higher demand for coordinated and continuous care management solutions across healthcare systems

- Furthermore, rising adoption of value-based healthcare models, along with growing integration of digital health technologies, telemedicine, and patient-centric care approaches, is establishing Integrated Chronic Care Pathway Services as a key component of modern healthcare delivery. These converging factors are accelerating the uptake of Integrated Chronic Care Pathway Services solutions, thereby significantly boosting the industry's growth

Integrated Chronic Care Pathway Services Market Analysis

- Integrated Chronic Care Pathway Services, encompassing coordinated care plans, remote patient monitoring, disease management programs, and multidisciplinary healthcare approaches, are increasingly vital in improving long-term outcomes for patients with chronic conditions such as diabetes, cardiovascular diseases, and respiratory disorders

- The escalating demand for these services is primarily driven by the rising global burden of chronic diseases, increasing aging population, and growing need for continuous, patient-centric, and cost-effective care delivery models. Advancements in digital health, telemedicine, and data analytics are further enhancing care coordination and efficiency

- North America dominated the integrated chronic care pathway services market with the largest revenue share of 41.22% in 2025, supported by advanced healthcare infrastructure, widespread adoption of value-based care models, strong reimbursement frameworks, and high integration of digital health technologies

- Asia-Pacific is expected to be the fastest growing region in the integrated chronic care pathway services market during the forecast period due to increasing healthcare expenditure, rising chronic disease prevalence, expanding telehealth adoption, and improving healthcare access in emerging economies

- The Care Coordination Services segment dominated the largest market revenue share of 44.7% in 2025, driven by the increasing need for streamlined patient management across multiple healthcare providers

Report Scope and Integrated Chronic Care Pathway Services Market Segmentation

|

Attributes |

Integrated Chronic Care Pathway Services Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Integrated Chronic Care Pathway Services Market Trends

“Expansion of Digital Health Integration, Personalized Care Models, and Remote Patient Monitoring”

- A significant and accelerating trend in the global Integrated Chronic Care Pathway Services market is the growing adoption of digital health technologies and data-driven care coordination models to improve long-term patient outcomes

- For instance, healthcare providers are increasingly implementing integrated care platforms that combine electronic health records (EHRs), telehealth services, and patient monitoring tools to streamline chronic disease management

- The use of remote patient monitoring (RPM) solutions is expanding, enabling continuous tracking of patient vitals such as blood pressure, glucose levels, and heart rate, which supports proactive intervention and reduces hospital readmissions

- For instance, patients with chronic conditions such as diabetes and cardiovascular diseases are increasingly managed through connected care pathways that allow real-time communication between patients and healthcare providers

- The shift toward personalized care plans based on patient history, lifestyle, and comorbidities is further enhancing treatment effectiveness and patient engagement

- In addition, multidisciplinary care teams involving physicians, nurses, physiotherapists, and care coordinators are becoming central to delivering comprehensive and continuous care

- This transition toward integrated, patient-centric, and technology-enabled care delivery models is fundamentally reshaping chronic disease management globally

Integrated Chronic Care Pathway Services Market Dynamics

Driver

“Rising Burden of Chronic Diseases and Growing Demand for Coordinated Care”

- The increasing global prevalence of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions is a major driver for the integrated chronic care pathway services market

- For instance, aging populations and lifestyle changes are contributing to a higher incidence of long-term health conditions, necessitating continuous and coordinated care management

- Healthcare systems are increasingly shifting from episodic treatment to value-based care models that emphasize long-term patient outcomes and cost efficiency

- For instance, hospitals and healthcare providers are adopting integrated care pathways to reduce hospital admissions and improve care continuity across different treatment stages

- Government initiatives aimed at improving chronic disease management and reducing healthcare costs are further supporting market growth

- Increasing awareness among patients regarding the benefits of structured care pathways is also driving adoption

Restraint/Challenge

“High Implementation Costs and Interoperability Issues Across Healthcare Systems”

- One of the major challenges in the integrated chronic care pathway services market is the high cost associated with implementing advanced digital health infrastructure and care coordination systems

- For instance, smaller healthcare providers may face financial constraints in adopting comprehensive care management platforms and integrating them with existing systems

- Interoperability issues between different healthcare IT systems, such as EHRs and patient monitoring devices, can hinder seamless data sharing and care coordination

- For instance, lack of standardized data formats and integration protocols may lead to inefficiencies in patient data exchange across providers

- Data privacy and security concerns also pose challenges, particularly when managing large volumes of sensitive patient information across digital platforms

- In addition, limited digital literacy among patients and healthcare professionals in certain regions can restrict adoption of integrated care solutions

- Addressing these challenges will require investment in interoperable systems, policy support for digital health adoption, and enhanced training programs for healthcare professionals and patients

Integrated Chronic Care Pathway Services Market Scope

The market is segmented on the basis of service type and end-users.

• By Service Type

On the basis of service type, the Integrated Chronic Care Pathway Services market is segmented into Care Coordination Services, Disease Management Programs, Remote Patient Monitoring, and Others. The Care Coordination Services segment dominated the largest market revenue share of 44.7% in 2025, driven by the increasing need for streamlined patient management across multiple healthcare providers. Rising prevalence of chronic diseases such as diabetes, cardiovascular disorders, and respiratory conditions is significantly boosting demand. Healthcare systems are increasingly focusing on reducing hospital readmissions and improving patient outcomes through coordinated care. Growing adoption of value-based care models further supports segment growth. Integration of electronic health records enhances communication between providers. Increasing healthcare expenditure globally contributes to service expansion. Governments and healthcare organizations are promoting integrated care frameworks. Improved patient engagement and continuity of care strengthen adoption. Technological advancements in healthcare IT systems further drive efficiency. Expanding aging population increases long-term care needs. Overall, care coordination services dominate due to their central role in managing chronic conditions.

The Remote Patient Monitoring segment is expected to witness the fastest CAGR of 12.6% from 2026 to 2033, driven by rapid adoption of digital health technologies and telehealth solutions. Increasing demand for home-based care and real-time health tracking is boosting growth. Rising smartphone and wearable device penetration supports remote monitoring adoption. Healthcare providers are leveraging remote tools to reduce hospital burden. Growing focus on preventive care enhances demand. Advancements in IoT-enabled medical devices improve patient monitoring accuracy. Increasing investments in digital healthcare infrastructure accelerate expansion. Favorable government initiatives promoting telemedicine support growth. Patients prefer convenient and continuous monitoring solutions. Improved data analytics capabilities enhance decision-making. Overall, remote patient monitoring is emerging as the fastest-growing segment.

• By End-Users

On the basis of end-users, the Integrated Chronic Care Pathway Services market is segmented into Hospitals, Homecare Settings, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 52.9% in 2025, driven by the high volume of chronic disease patients requiring continuous monitoring and coordinated treatment. Hospitals serve as primary centers for diagnosis, treatment planning, and integrated care delivery. Increasing hospital admissions for chronic conditions support demand. Availability of advanced healthcare infrastructure enhances service implementation. Strong presence of multidisciplinary teams improves patient outcomes. Rising healthcare expenditure strengthens hospital capabilities. Insurance coverage improves accessibility of integrated care services. Hospitals are adopting digital platforms to streamline care pathways. Government funding supports hospital-based chronic care programs. Increasing prevalence of lifestyle-related diseases boosts patient inflow. Overall, hospitals remain the dominant end-user segment.

The Homecare Settings segment is expected to witness the fastest CAGR of 13.4% from 2026 to 2033, driven by increasing preference for personalized and cost-effective care at home. Rising aging population and chronic disease burden support demand. Patients prefer home-based care to avoid frequent hospital visits. Advancements in remote monitoring technologies enable effective homecare services. Growing awareness about patient-centric care models boosts adoption. Expansion of home healthcare providers enhances accessibility. Cost advantages compared to hospital stays further drive demand. Increasing telehealth integration supports service delivery. Government initiatives promoting home-based care strengthen growth. Improved patient comfort and convenience enhance preference. Overall, homecare settings are rapidly emerging as the fastest-growing segment.

Integrated Chronic Care Pathway Services Market Regional Analysis

- North America dominated the integrated chronic care pathway services market with the largest revenue share of 41.22% in 2025, supported by advanced healthcare infrastructure, widespread adoption of value-based care models, strong reimbursement frameworks, and high integration of digital health technologies. The region benefits from well-established care coordination systems, robust healthcare IT infrastructure, and early adoption of integrated care delivery models aimed at improving long-term patient outcomes

- Healthcare providers in the region increasingly emphasize coordinated, patient-centric care approaches that integrate multiple services such as diagnostics, treatment, monitoring, and follow-up within a unified framework

- This widespread adoption is further supported by high healthcare expenditure, a technologically advanced ecosystem, and strong presence of leading healthcare service providers, establishing North America as a key contributor to market growth

U.S. Integrated Chronic Care Pathway Services Market Insight

The U.S. integrated chronic care pathway services market captured the largest revenue share within North America in 2025, driven by a high burden of chronic diseases, strong adoption of digital health solutions, and well-established value-based care initiatives. The country has a highly advanced healthcare system with extensive use of electronic health records (EHRs), telehealth platforms, and remote patient monitoring tools. For instance, healthcare providers in the U.S. are increasingly implementing integrated care pathways for conditions such as diabetes, cardiovascular diseases, and respiratory disorders to improve care continuity and reduce hospital readmissions. Strong investment in healthcare IT and supportive reimbursement policies are further accelerating market growth.

Europe Integrated Chronic Care Pathway Services Market Insight

The Europe integrated chronic care pathway services market is projected to expand at a substantial CAGR during the forecast period, supported by increasing prevalence of chronic diseases, aging population, and strong public healthcare systems. For instance, European countries are increasingly adopting integrated care models to improve efficiency and reduce healthcare costs associated with long-term disease management. Government initiatives promoting coordinated care and digital health integration are further supporting market expansion across the region.

U.K. Integrated Chronic Care Pathway Services Market Insight

The U.K. integrated chronic care pathway services market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by strong National Health Service (NHS) initiatives focused on integrated care systems and population health management. For instance, the U.K. is actively implementing coordinated care pathways that connect primary care, secondary care, and community services to enhance patient outcomes. Increasing investment in digital health and remote care services is further supporting market growth.

Germany Integrated Chronic Care Pathway Services Market Insight

The Germany integrated chronic care pathway services market is expected to expand at a considerable CAGR during the forecast period, fueled by a robust healthcare system, growing emphasis on chronic disease management, and increasing adoption of digital health solutions. For instance, German healthcare providers are integrating care pathways with advanced IT systems to ensure seamless patient data exchange and coordinated treatment planning. The country’s focus on efficiency and quality care delivery is further driving adoption.

Asia-Pacific Integrated Chronic Care Pathway Services Market Insight

The Asia-Pacific integrated chronic care pathway services market is poised to grow at the fastest CAGR during the forecast period due to increasing healthcare expenditure, rising chronic disease prevalence, expanding telehealth adoption, and improving healthcare access in emerging economies such as China, India, and Japan. For instance, governments across the region are investing in healthcare infrastructure and promoting digital health initiatives to enhance chronic disease management. Growing awareness regarding structured care pathways and increasing availability of healthcare services are further accelerating market growth.

Japan Integrated Chronic Care Pathway Services Market Insight

The Japan integrated chronic care pathway services market is gaining momentum due to its rapidly aging population, advanced healthcare infrastructure, and strong focus on chronic disease management. For instance, healthcare providers in Japan are increasingly implementing integrated care models that combine hospital care with home-based monitoring and rehabilitation services. The country’s emphasis on elderly care and long-term disease management is further supporting market expansion.

China Integrated Chronic Care Pathway Services Market Insight

The China integrated chronic care pathway services market accounted for the largest revenue share in Asia Pacific in 2025, driven by a growing burden of chronic diseases, expanding healthcare infrastructure, and strong government support for healthcare modernization. For instance, major hospitals and healthcare systems in China are increasingly adopting integrated care pathways and digital health platforms to improve patient management and reduce healthcare costs. Rising healthcare investments and ongoing reforms in the healthcare sector are further propelling market growth.

Integrated Chronic Care Pathway Services Market Share

The Integrated Chronic Care Pathway Services industry is primarily led by well-established companies, including:

- Optum, Inc. (U.S.)

- UnitedHealth Group (U.S.)

- CVS Health Corporation (U.S.)

- McKesson Corporation (U.S.)

- Oracle (U.S.)

- Epic Systems Corporation (U.S.)

- Philips Healthcare (Netherlands)

- Siemens Healthineers (Germany)

- GE HealthCare (U.S.)

- Allscripts Healthcare Solutions (U.S.)

- IBM Watson Health (U.S.)

- Oracle Health (U.S.)

- Athenahealth, Inc. (U.S.)

- Medtronic plc (Ireland)

- Baxter International Inc. (U.S.)

- Fresenius Medical Care (Germany)

- Teladoc Health, Inc. (U.S.)

- Amwell (U.S.)

- HCA Healthcare (U.S.)

- Ramsay Health Care (Australia)

Latest Developments in Global Integrated Chronic Care Pathway Services Market

- In July 2021, the National Health Service (NHS) in England formally established Integrated Care Systems (ICSs) across the country, bringing together healthcare providers, local authorities, and community organizations to deliver coordinated chronic care pathways and improve long-term condition management through system-wide collaboration

- In August 2023, healthcare systems globally accelerated the adoption of integrated care pathways, emphasizing coordinated, patient-centered services across multiple providers and care settings to improve outcomes and optimize resource utilization for chronic disease management

- In March 2024, policy research highlighted that the NHS and other health systems were advancing multidisciplinary integrated care models, incorporating structured care plans across specialties, diagnostics, treatment, and rehabilitation to enhance outcomes for patients with complex chronic conditions

- In August 2025, the Center for Health Care Strategies reported expanded efforts in the U.S. to integrate Medicare and Medicaid services through coordinated care programs such as PACE and Dual Eligible Special Needs Plans (D-SNPs), aiming to reduce fragmentation and improve outcomes for patients with multiple chronic conditions

- In November 2025, the OECD’s Health at a Glance 2025 report emphasized a global shift toward people-centered integrated care systems, highlighting increased adoption of digital health tools, preventive care strategies, and coordinated chronic care pathways to improve healthcare system performance and sustainability

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.