Global Intracranial Stents Market

Market Size in USD Billion

USD

1,189.06 Billion

USD

2,441.51 Billion

2025

2033

USD

1,189.06 Billion

USD

2,441.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 1,189.06 Billion | |

| USD 2,441.51 Billion | |

| % | |

|

Intracranial Stents Market Size

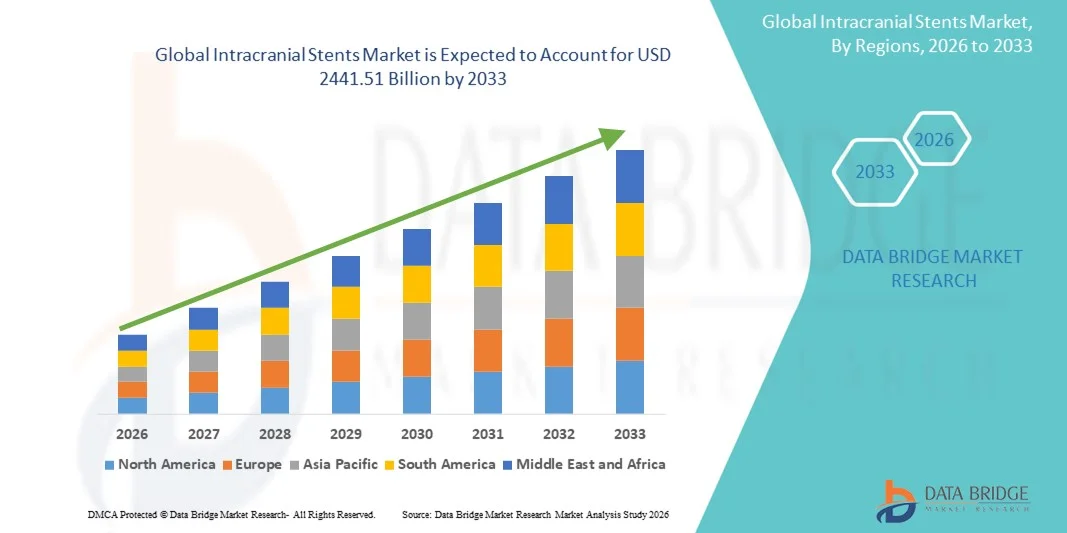

- The global Intracranial Stents market size was valued at USD 1189.06 billion in 2025 and is expected to reach USD 2441.51 billion by 2033, at a CAGR of 9.41% during the forecast period

- The market growth is largely driven by the rising prevalence of intracranial aneurysms and ischemic stroke, along with continuous technological advancements in neurovascular devices, which are enhancing the safety, efficacy, and clinical outcomes of intracranial stent procedures across hospitals and specialized neurological centers

- Furthermore, increasing adoption of minimally invasive endovascular treatments, growing awareness among clinicians about early intervention, and expanding access to advanced neurointerventional care are accelerating the uptake of intracranial stents, thereby significantly boosting the overall growth of the Intracranial Stents market

Intracranial Stents Market Analysis

- Intracranial stents, used in the treatment of cerebral aneurysms and ischemic stroke, are increasingly becoming essential devices in modern neurointerventional care due to their role in enabling minimally invasive procedures, improving cerebral blood flow, and reducing long-term neurological complications

- The demand for intracranial stents is driven by the rising global burden of stroke and intracranial aneurysms, growing preference for endovascular therapies over conventional surgery, and continuous advancements in stent technologies such as flow diverters, braided stents, and next-generation self-expanding designs

- North America dominated the intracranial stents market with a revenue share of approximately 35.4% in 2025, supported by advanced neurovascular treatment infrastructure, high adoption of innovative stent technologies, favorable reimbursement policies, and a strong presence of leading medical device manufacturers, particularly in the United States

- Asia-Pacific is projected to be the fastest growing region in the intracranial stents market during the forecast period, with an estimated CAGR of around 8.7%, driven by a rapidly expanding patient pool, increasing incidence of stroke, improving access to specialized neurointerventional care, and rising healthcare investments across China, India, and Southeast Asia

Report Scope and Intracranial Stents Market Segmentation

|

Attributes |

Intracranial Stents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Intracranial Stents Market Trends

Advancements in Minimally Invasive Neurovascular Treatment Technologies

- A significant and accelerating trend in the global Intracranial Stents market is the increasing adoption of minimally invasive neurovascular interventions for the treatment of intracranial aneurysms and complex cerebrovascular diseases

- These procedures offer reduced surgical trauma, shorter hospital stays, and improved patient recovery outcomes compared to traditional open surgical methods

- For instance, advanced self-expanding and flow-diverting intracranial stents are increasingly being adopted in neurointerventional centers across North America, Europe, and parts of Asia to treat wide-neck and complex aneurysms with higher precision and safety

- Ongoing innovations in stent materials, including nitinol-based alloys and bio-compatible coatings, are enhancing flexibility, durability, and long-term vessel compatibility, improving clinical outcomes

- The growing availability of hybrid stent systems that combine support with flow diversion capabilities is expanding the range of treatable neurovascular conditions

- Globally, increasing investments in neurovascular research and improvements in imaging and catheter-based delivery technologies are further supporting the evolution and adoption of next-generation intracranial stents

Intracranial Stents Market Dynamics

Driver

Rising Prevalence of Cerebrovascular Disorders and Aging Population

- The increasing incidence of cerebrovascular diseases such as intracranial aneurysms, ischemic strokes, and arterial stenosis is a major driver for the growth of the Intracranial Stents market worldwide

- For instance, in 2024, several tertiary care hospitals in the United States and Europe expanded their neurointerventional programs to accommodate the growing number of patients requiring endovascular treatment using intracranial stents

- The global aging population is particularly susceptible to neurovascular conditions, leading to higher demand for effective and less invasive treatment options

- Furthermore, improved awareness, early diagnosis, and advancements in neuroimaging technologies are enabling timely intervention, increasing the adoption of intracranial stent-based procedures

- Supportive reimbursement policies in developed regions and the expansion of specialized stroke and neurovascular centers are further accelerating market growth across both developed and emerging economies

Restraint/Challenge

High Procedure Costs and Technical Complexity of Neurointerventional Procedures

- The high cost associated with intracranial stent devices and related neurointerventional procedures remains a significant challenge, particularly in low- and middle-income countries. Expenses related to advanced imaging, specialized equipment, and skilled clinical expertise can limit accessibility

- For instance, hospitals in certain regions of Asia-Pacific and Latin America face challenges in adopting advanced intracranial stent technologies due to budget constraints and limited reimbursement coverage

- The technical complexity of intracranial stent placement requires highly trained neurointerventional specialists, and the shortage of skilled professionals can restrict market growth

- Strict regulatory requirements and lengthy approval processes for neurovascular devices can delay product commercialization and increase development costs for manufacturers

- Addressing these challenges through cost-optimized device designs, expanded physician training programs, and improved healthcare infrastructure will be essential for the sustained growth of the global Intracranial Stents market

Intracranial Stents Market Scope

The market is segmented on the basis of product type, disease indication, and end-user.

- By Product Type

On the basis of product type, the Intracranial Stents market is segmented into self-expanding intracranial stents and embolization coil support intracranial stents. The self-expanding intracranial stents segment dominated the largest market revenue share of approximately 61.4% in 2025, driven by their superior flexibility, adaptability to complex cerebral vasculature, and widespread use in neurointerventional procedures. These stents are extensively adopted in the treatment of intracranial stenosis and wide-neck aneurysms due to their ability to maintain vessel patency while minimizing trauma. Their compatibility with minimally invasive procedures, high clinical success rates, and continuous technological advancements further support dominance. Growing preference among neurovascular surgeons, increasing stroke prevalence, and rising adoption in tertiary care hospitals also contribute significantly. In addition, favorable reimbursement policies in developed markets and strong clinical evidence validating safety and efficacy continue to reinforce market leadership.

The embolization coil support intracranial stents segment is expected to witness the fastest growth, registering a CAGR of around 9.2% from 2026 to 2033, driven by increasing adoption in complex aneurysm treatments. These stents provide enhanced stability for coil placement in wide-neck and bifurcation aneurysms, reducing the risk of coil migration. Rising demand for advanced aneurysm management solutions, growing neurointerventional procedure volumes, and technological innovations in stent-assisted coiling are key growth drivers. Increased awareness among clinicians, expanding use in emerging economies, and improving patient outcomes further accelerate growth. In addition, expanding product pipelines and regulatory approvals support rapid market expansion.

- By Disease Indication

On the basis of disease indication, the Intracranial Stents market is segmented into brain aneurysm and intracranial stenosis. The brain aneurysm segment accounted for the largest revenue share of approximately 58.9% in 2025, driven by the rising global incidence of cerebral aneurysms and increasing detection through advanced imaging technologies. Growing preference for endovascular treatment over open surgical procedures has significantly boosted intracranial stent adoption. The segment benefits from increasing use of stent-assisted coiling techniques, improved procedural safety, and shorter hospital stays. Advancements in flow-diverter and self-expanding stents further strengthen demand. Rising healthcare expenditure, expanding neurovascular centers, and favorable clinical outcomes continue to support segment dominance across developed and emerging markets.

The intracranial stenosis segment is projected to grow at the fastest CAGR of approximately 8.7% from 2026 to 2033, driven by the increasing prevalence of ischemic stroke and atherosclerotic disease. Growing awareness regarding early intervention, expanding geriatric population, and improvements in minimally invasive neurovascular procedures are key contributors. Enhanced stent designs offering better radial strength and reduced restenosis rates further drive adoption. Increasing investments in stroke care infrastructure and rising screening programs in developing regions also support accelerated growth.

- By End-User

On the basis of end-user, the Intracranial Stents market is segmented into hospitals and ambulatory surgical centers. The hospitals segment dominated the market with a revenue share of approximately 69.6% in 2025, supported by the availability of advanced neurointerventional facilities and skilled neurosurgeons. Hospitals serve as primary centers for complex intracranial procedures, including aneurysm repair and stroke management. Higher patient inflow, access to advanced imaging systems, and the ability to manage post-procedural complications strengthen dominance. In addition, favorable reimbursement structures and government investments in hospital infrastructure further contribute to sustained leadership.

The ambulatory surgical centers segment is expected to witness the fastest growth, registering a CAGR of nearly 9.5% from 2026 to 2033, driven by the shift toward minimally invasive procedures and cost-effective care settings. Improvements in procedural efficiency, reduced hospitalization time, and advancements in outpatient neurointerventional techniques are fueling adoption. Growing patient preference for shorter recovery times and expanding ASC capabilities in developed regions further accelerate growth. Increasing regulatory approvals and investments in outpatient neurovascular services also support rapid expansion.

Intracranial Stents Market Regional Analysis

- North America dominated the intracranial stents market with a revenue share of approximately 35.4% in 2025, supported by a well-established neurovascular treatment infrastructure, widespread adoption of advanced intracranial stent technologies, and strong clinical expertise across hospitals and specialized stroke centers

- The region benefits from early access to innovative stent designs, including flow diverters and self-expanding stents, which are widely used in the treatment of complex intracranial aneurysms and cerebrovascular disorders

- Favorable reimbursement frameworks, high healthcare expenditure, and a strong presence of leading medical device manufacturers, particularly in the United States, further reinforce North America’s leading position in the global Intracranial Stents market

U.S. Intracranial Stents Market Insight

The U.S. intracranial stents market accounted for the largest share within North America in 2025, driven by a high prevalence of stroke and intracranial aneurysms, advanced neurointerventional capabilities, and the presence of specialized comprehensive stroke centers. Strong regulatory support for innovation, extensive clinical research activity, and rapid adoption of next-generation stent technologies continue to fuel market growth. Additionally, well-defined reimbursement policies and a high level of physician awareness contribute significantly to the expansion of the intracranial stents industry in the country.

Europe Intracranial Stents Market Insight

The Europe intracranial stents market is expected to grow at a steady CAGR during the forecast period, supported by increasing awareness of minimally invasive neurovascular treatments and a rising burden of cerebrovascular diseases. Countries across Western and Northern Europe are witnessing greater adoption of intracranial stents due to improved access to specialized neurointerventional care, supportive healthcare policies, and advancements in medical imaging technologies.

U.K. Intracranial Stents Market Insight

The U.K. intracranial stents market is projected to grow at a notable pace, driven by the expansion of stroke care programs, rising diagnosis rates of intracranial aneurysms, and increasing preference for endovascular treatment approaches. Ongoing investments in public healthcare infrastructure and the growing availability of trained neurointerventional specialists are further supporting market growth.

Germany Intracranial Stents Market Insight

The Germany intracranial stents market is anticipated to expand at a considerable CAGR over the forecast period, supported by the country’s strong medical technology ecosystem and high standards of neurological care. Germany’s focus on innovation, clinical research, and adoption of advanced minimally invasive procedures contributes to the increasing utilization of intracranial stents in both public and private healthcare settings.

Asia-Pacific Intracranial Stents Market Insight

The Asia-Pacific intracranial stents market is projected to be the fastest-growing region, registering an estimated CAGR of around 8.7% during the forecast period, driven by a rapidly expanding patient population and a rising incidence of stroke and other cerebrovascular disorders. Improving healthcare infrastructure, increasing availability of specialized neurointerventional centers, and rising healthcare expenditure across emerging economies are key growth drivers in the region.

China Intracranial Stents Market Insight

China intracranial stents market accounted for the largest revenue share within the Asia-Pacific Intracranial Stents market in 2025, attributed to its large population base, increasing prevalence of stroke, and expanding access to advanced neurovascular treatments. Government initiatives aimed at strengthening healthcare infrastructure, coupled with the presence of domestic and international medical device manufacturers, are accelerating the adoption of intracranial stents across major hospitals.

Japan Intracranial Stents Market Insight

The Japan intracranial stents market is witnessing steady growth due to the country’s aging population and high incidence of cerebrovascular diseases. Japan’s advanced healthcare system, strong emphasis on minimally invasive treatments, and continuous technological innovation are driving the adoption of intracranial stents in both acute and preventive neurovascular care settings.

Intracranial Stents Market Share

The Intracranial Stents industry is primarily led by well-established companies, including:

- Medtronic (Ireland)

- Stryker Corporation (U.S.)

- Terumo Corporation (Japan)

- Johnson & Johnson (U.S.)

- Penumbra, Inc. (U.S.)

- Balt Extrusion (France)

- Phenox GmbH (Germany)

- Acandis GmbH (Germany)

- Rapid Medical (Israel)

- Merit Medical Systems (U.S.)

- Lepu Medical Technology (China)

- Shanghai MicroPort NeuroTech (China)

- Nanjing Wallaby Medical (China)

- Integer Holdings Corporation (U.S.)

Latest Developments in Global Intracranial Stents Market

- In February 2023, Medtronic launched a new Intracranial Stent System designed to treat intracranial aneurysms with enhanced flexibility and patient outcomes, marking a significant advancement in neurovascular interventions

- In April 2023, Abbott Laboratories completed the acquisition of the neurovascular division of Cardiovascular Systems Inc., expanding its portfolio in intracranial intervention devices and strengthening its position in stent technologies for complex neurovascular applications

- In November 2024, Medtronic announced FDA approval for its next-generation Pipeline Vantage Embolization Device, featuring enhanced deliverability and fluoroscopic visibility for aneurysm treatment, enhancing clinical utility in the U.S. market

- In May 2025, MicroVention launched the LVIS EVO Stent in Europe following CE Mark clearance. This device offers improved fluoroscopic visibility and navigation in difficult vessel anatomies, supporting stent-assisted coiling treatments

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.