Global Intraocular Lens Iol Market

Market Size in USD Billion

CAGR :

%

USD

4.28 Billion

USD

6.32 Billion

2025

2033

USD

4.28 Billion

USD

6.32 Billion

2025

2033

| 2026 –2033 | |

| USD 4.28 Billion | |

| USD 6.32 Billion | |

| % | |

|

Intraocular Lens (IOL) Market Size

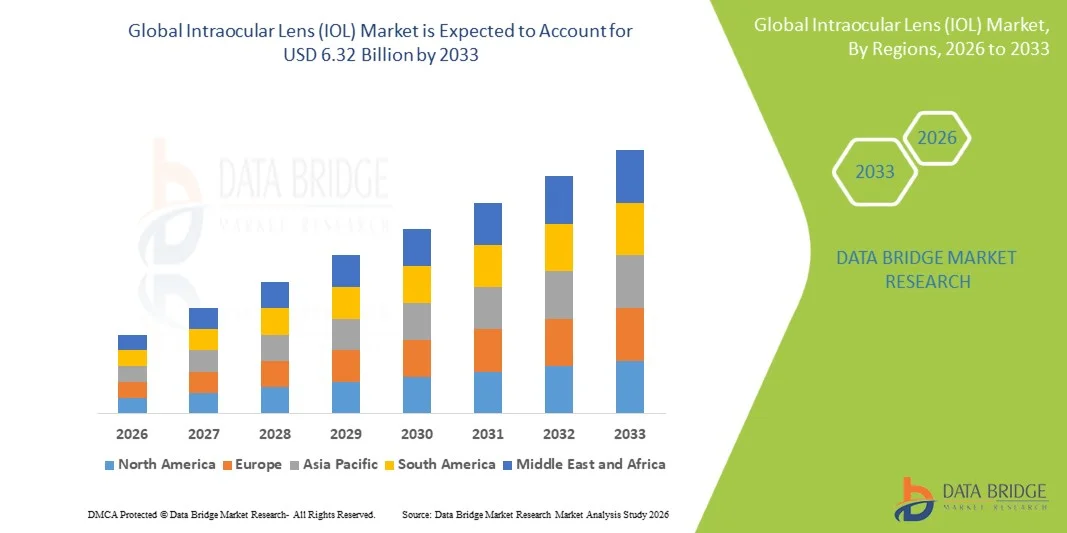

- The global Intraocular Lens (IOL) market size was valued at USD 4.28 billion in 2025 and is expected to reach USD 6.32 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of cataracts and age-related vision disorders, along with the rising number of cataract surgeries performed globally, which is driving the demand for advanced intraocular lens implants

- Furthermore, technological advancements in premium intraocular lenses, such as multifocal, toric, and extended depth-of-focus (EDOF) lenses, along with growing patient preference for improved post-surgery vision quality and reduced dependency on glasses, are accelerating the adoption of Intraocular Lens (IOL) solutions, thereby significantly boosting the industry's growth

Intraocular Lens (IOL) Market Analysis

- Intraocular lenses (IOLs), artificial lenses implanted in the eye to replace the natural lens removed during cataract surgery or to correct refractive errors, are increasingly vital components of modern ophthalmic treatment due to their effectiveness in restoring vision and improving patients’ quality of life following cataract procedure

- The escalating demand for intraocular lenses is primarily fueled by the rising prevalence of cataracts, increasing global geriatric population, and the growing volume of cataract surgeries worldwide, along with expanding access to advanced ophthalmic care and improved awareness regarding vision restoration procedures

- North America dominated the intraocular lens (IOL) market with the largest revenue share of 39.8% in 2025, characterized by well-established healthcare infrastructure, high adoption of premium intraocular lenses such as multifocal and toric lenses, and the strong presence of leading ophthalmic device manufacturers, with the U.S. witnessing significant growth in advanced cataract surgery procedures

- Asia-Pacific is expected to be the fastest growing region in the intraocular lens (IOL) market during the forecast period, driven by the rapidly aging population, rising incidence of cataracts, improving healthcare infrastructure, and increasing government initiatives aimed at reducing vision impairment and preventable blindness

- Monofocal intraocular lens segment dominated the market with a share of 62.4% in 2025, driven by their extensive use in cataract surgeries, cost-effectiveness compared to premium lenses, and strong clinical reliability in restoring clear distance vision for patients worldwide

Report Scope and Intraocular Lens (IOL) Market Segmentation

|

Attributes |

Intraocular Lens (IOL) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Intraocular Lens (IOL) Market Trends

“Rising Adoption of Premium and Advanced Intraocular Lens Technologies”

- A significant and accelerating trend in the global intraocular lens (IOL) market is the growing adoption of premium intraocular lenses such as multifocal, toric, and extended depth-of-focus (EDOF) lenses, which are designed to provide improved visual outcomes and reduce dependency on corrective eyewear after cataract surgery. This advancement is significantly enhancing the overall quality of postoperative vision for patients

- For instance, Alcon introduced advanced presbyopia-correcting lenses such as the AcrySof IQ PanOptix Trifocal IOL, which allows patients to achieve clear vision at near, intermediate, and distance ranges. Similarly, Johnson & Johnson Vision offers the TECNIS Synergy Intraocular Lens, designed to deliver continuous vision while reducing the need for spectacles

- Technological innovation in intraocular lenses enables features such as improved optical designs, enhanced contrast sensitivity, and better correction for astigmatism. For instance, newer premium lenses are engineered with advanced diffractive optics and toric designs to improve visual clarity and stability following cataract surgery. Furthermore, innovations in material technology allow lenses to provide better biocompatibility and long-term durability within the eye

- The seamless integration of advanced intraocular lens technology with modern cataract surgical techniques facilitates improved surgical precision and patient outcomes. Through advanced diagnostic tools and surgical planning systems, ophthalmologists can now select and implant lenses tailored to the patient’s specific vision needs, creating a more personalized vision correction approach

- This trend toward more advanced, patient-centric vision restoration solutions is fundamentally reshaping expectations for cataract surgery outcomes. Consequently, companies such as Bausch + Lomb are developing innovative intraocular lens systems with improved optical performance and expanded vision ranges to address evolving patient demands

- The demand for intraocular lenses offering enhanced visual performance and reduced dependency on glasses is growing rapidly across both developed and emerging healthcare markets, as patients increasingly prioritize improved quality of life and long-term visual independence

- In addition, the growing awareness of refractive cataract surgery and the rising preference for customized vision correction solutions are encouraging patients to opt for premium intraocular lenses, further strengthening market growth globally

Intraocular Lens (IOL) Market Dynamics

Driver

“Growing Need Due to Rising Cataract Prevalence and Aging Population”

- The increasing prevalence of cataracts among aging populations, coupled with the rising number of cataract surgeries performed globally, is a significant driver for the heightened demand for intraocular lenses

- For instance, in May 2024, Johnson & Johnson Vision announced expanded availability of its TECNIS Eyhance IOL, designed to enhance intermediate vision performance while maintaining excellent distance vision. Such strategies by key companies are expected to drive the intraocular lens industry growth in the forecast period

- As life expectancy increases worldwide, a larger portion of the population is entering age groups more susceptible to cataracts and other vision impairments, creating a growing demand for surgical interventions involving intraocular lens implantation

- Furthermore, the expanding availability of advanced ophthalmic surgical facilities and improved access to eye care services are making cataract surgery more accessible, particularly in emerging markets with rising healthcare investments

- The increasing awareness about the benefits of early cataract treatment and the effectiveness of intraocular lenses in restoring vision are key factors propelling the adoption of IOLs in hospitals and specialized ophthalmology centers. The introduction of advanced surgical technologies such as femtosecond laser-assisted cataract surgery further contributes to improved surgical outcomes and market growth

- Growing government initiatives and public health programs aimed at reducing preventable blindness are encouraging early diagnosis and treatment of cataracts, thereby increasing the number of surgical procedures and boosting demand for intraocular lenses

- In addition, continuous technological advancements in lens design, including aspheric and blue-light filtering intraocular lenses, are further supporting improved postoperative vision quality and strengthening overall market expansion

Restraint/Challenge

“High Cost of Premium Lenses and Surgical Complication Risks”

- Concerns surrounding the high cost of premium intraocular lenses and potential postoperative complications pose a significant challenge to broader market adoption. While cataract surgery is widely performed, the cost of advanced premium lenses can limit accessibility for some patients

- For instance, patients opting for premium lenses such as multifocal or toric IOLs often face additional out-of-pocket expenses beyond standard cataract surgery coverage, making affordability a concern in certain healthcare systems

- Addressing these cost-related barriers through improved reimbursement policies and broader insurance coverage is crucial for expanding access to advanced intraocular lens technologies. Companies such as Carl Zeiss Meditec AG and Alcon continue to invest in innovation to improve clinical outcomes and justify the value of premium lens technologies

- In addition, concerns related to postoperative complications such as glare, halos, or lens misalignment may influence patient decision-making when selecting premium intraocular lenses. While technological advancements have reduced these risks, awareness of potential side effects may still impact adoption rates

- While the clinical effectiveness of intraocular lenses continues to improve, the perceived cost burden and surgical risks can still hinder broader adoption, especially in cost-sensitive healthcare markets where affordability remains a major consideration

- Limited reimbursement coverage for premium intraocular lenses in several healthcare systems can further restrict patient access, particularly in developing regions where healthcare budgets and insurance penetration remain limited

- Moreover, variability in surgical expertise and access to advanced ophthalmic equipment in certain regions may affect the optimal implantation and performance of premium lenses, creating additional challenges for consistent adoption

- Overcoming these challenges through continued technological innovation, improved surgeon training, and expanded reimbursement frameworks will be vital for sustaining long-term market growth

Intraocular Lens (IOL) Market Scope

The market is segmented on the basis of type, material, and end user.

- By Type

On the basis of type, the global intraocular lens (IOL) market is segmented into monofocal intraocular lens, premium intraocular lens, toric intraocular lens, multifocal intraocular lens, accommodating intraocular lens, and others. The monofocal intraocular lens segment dominated the market with the largest revenue share of 62.4% in 2025, primarily due to its widespread use in standard cataract surgeries and its cost-effectiveness compared to premium lens options. Monofocal lenses are designed to provide clear vision at a single focal point, usually distance vision, making them the most commonly implanted lens type globally. Their long-standing clinical reliability and ease of implantation make them a preferred choice among ophthalmic surgeons. In addition, monofocal lenses are widely covered by insurance and healthcare reimbursement programs in several countries, which further increases their adoption. The high volume of cataract surgeries performed worldwide also supports the continued demand for monofocal lenses. As a result, this segment maintains a dominant position in both developed and emerging healthcare markets.

The multifocal intraocular lens segment is anticipated to witness the fastest growth rate during the forecast period from 2026 to 2033, driven by increasing demand for advanced vision correction solutions that reduce dependency on eyeglasses. Multifocal lenses allow patients to achieve clear vision at multiple distances, including near, intermediate, and far. Rising patient awareness regarding premium cataract surgery options is encouraging more individuals to opt for multifocal lenses. Technological improvements in lens optics and design are also enhancing visual outcomes and reducing issues such as glare and halos. In addition, the growing popularity of refractive cataract surgery is further boosting the adoption of multifocal lenses globally. Increasing disposable incomes and willingness to pay for improved postoperative vision are expected to accelerate the expansion of this segment.

- By Material

On the basis of material, the intraocular lens market is segmented into polymethylmethacrylate (PMMA), silicone, and hydrophobic acrylic. The hydrophobic acrylic segment dominated the market with the largest revenue share in 2025, owing to its superior optical clarity, flexibility, and biocompatibility compared to other materials. Hydrophobic acrylic lenses are foldable, allowing them to be implanted through smaller surgical incisions during cataract procedures. This contributes to faster patient recovery and improved surgical outcomes. In addition, these lenses demonstrate a lower incidence of posterior capsule opacification, a common complication after cataract surgery. Their long-term stability and compatibility with advanced lens designs also support their widespread adoption. As cataract surgeries increasingly shift toward minimally invasive procedures, hydrophobic acrylic lenses continue to be the preferred material among ophthalmic surgeons worldwide.

The silicone segment is expected to witness the fastest growth rate during the forecast period, supported by ongoing innovations in lens material technology and optical performance. Silicone lenses offer excellent flexibility and can be easily folded during implantation, enabling minimally invasive surgical techniques. These lenses also provide good refractive stability and optical transparency, contributing to favorable postoperative vision outcomes. Increasing adoption of advanced cataract surgery techniques in emerging healthcare markets is further driving demand for silicone-based intraocular lenses. Moreover, improvements in lens coatings and designs are enhancing their clinical performance and patient satisfaction. As ophthalmic device manufacturers continue to refine silicone lens materials, the segment is expected to expand steadily in the coming years.

- By End User

On the basis of end user, the intraocular lens market is segmented into hospitals, ambulatory surgery centres, ophthalmology clinics, and eye research institutes. The hospitals segment dominated the market with the largest revenue share in 2025, largely due to the high volume of cataract surgeries performed in hospital settings. Hospitals typically have advanced ophthalmic surgical infrastructure, experienced ophthalmologists, and comprehensive patient care facilities, which make them the primary centers for intraocular lens implantation procedures. In addition, hospitals often handle complex cataract cases that require specialized surgical expertise and advanced equipment. The availability of reimbursement coverage and government healthcare programs in hospitals also supports patient access to cataract surgery. Furthermore, hospitals frequently collaborate with medical device manufacturers for clinical training and adoption of innovative IOL technologies. These factors collectively contribute to the dominant position of hospitals in the intraocular lens market.

The ambulatory surgery centres segment is expected to witness the fastest growth rate during the forecast period from 2026 to 2033, driven by the increasing shift toward outpatient surgical procedures. Ambulatory surgery centres offer cost-effective cataract surgery services with shorter hospital stays and faster patient turnover. The streamlined operational environment in these facilities enables efficient scheduling and quicker surgical procedures. Many ophthalmologists prefer ambulatory centers for routine cataract surgeries due to their specialized focus and reduced administrative complexity. Patients also benefit from shorter waiting times and lower treatment costs compared to traditional hospital settings. As healthcare systems increasingly emphasize cost efficiency and outpatient care, the role of ambulatory surgery centres in cataract surgery and intraocular lens implantation is expected to grow rapidly.

Intraocular Lens (IOL) Market Regional Analysis

- North America dominated the intraocular lens (IOL) market with the largest revenue share of 39.8% in 2025, characterized by well-established healthcare infrastructure, high adoption of premium intraocular lenses such as multifocal and toric lenses, and the strong presence of leading ophthalmic device manufacturers

- Patients and healthcare providers in the region highly value the improved visual outcomes, advanced optical technologies, and reduced dependency on eyeglasses offered by modern intraocular lenses, particularly premium options such as multifocal and toric lenses

- This widespread adoption is further supported by advanced healthcare infrastructure, favorable reimbursement frameworks, a high number of cataract surgery procedures, and the strong presence of leading ophthalmic device manufacturers, establishing intraocular lenses as a critical component of modern cataract treatment across hospitals and specialized eye care centers

U.S. Intraocular Lens (IOL) Market Insight

The U.S. intraocular lens (IOL) market captured the largest revenue share within North America in 2025, fueled by the high prevalence of cataracts and the increasing number of cataract surgery procedures performed annually. Patients and ophthalmologists in the country are increasingly prioritizing advanced vision correction through premium intraocular lenses that improve postoperative visual outcomes. The growing preference for multifocal, toric, and extended depth-of-focus lenses, combined with strong adoption of advanced ophthalmic surgical technologies, further propels the intraocular lens industry. Moreover, the strong presence of leading ophthalmic device manufacturers and well-established reimbursement systems is significantly contributing to the market's expansion.

Europe Intraocular Lens (IOL) Market Insight

The Europe intraocular lens market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the rising prevalence of age-related eye disorders and increasing demand for cataract surgeries across the region. The growth of advanced healthcare infrastructure, coupled with expanding access to ophthalmic care, is fostering the adoption of intraocular lenses. European patients are also drawn to the improved visual outcomes and long-term vision correction these lenses offer. The region is experiencing significant growth across hospitals and specialized ophthalmology clinics, with intraocular lenses being widely adopted in both routine cataract surgeries and advanced refractive procedures.

U.K. Intraocular Lens (IOL) Market Insight

The U.K. intraocular lens market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness regarding cataract treatment and the availability of advanced ophthalmic technologies. In addition, the growing elderly population and rising demand for improved vision quality are encouraging patients to opt for cataract surgeries with intraocular lens implantation. The country’s strong healthcare system and emphasis on early diagnosis and treatment of eye disorders are expected to continue stimulating market growth. Furthermore, increasing adoption of premium intraocular lenses is supporting the expansion of the market in the United Kingdom.

Germany Intraocular Lens (IOL) Market Insight

The Germany intraocular lens market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing demand for technologically advanced ophthalmic solutions and the growing aging population. Germany’s well-developed healthcare infrastructure and strong focus on medical innovation promote the adoption of advanced intraocular lenses, particularly in specialized ophthalmology centers. The integration of modern cataract surgery techniques with high-quality intraocular lens implants is also becoming increasingly prevalent. In addition, a strong preference for high-performance medical devices aligns with local patient expectations and supports the market’s steady growth.

Asia-Pacific Intraocular Lens (IOL) Market Insight

The Asia-Pacific intraocular lens market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing healthcare investments, rising prevalence of cataracts, and expanding access to ophthalmic treatment in countries such as China, Japan, and India. The region's rapidly aging population and growing awareness regarding vision correction procedures are driving the adoption of intraocular lenses. Furthermore, government initiatives aimed at reducing preventable blindness and improving eye care services are supporting market expansion. As Asia-Pacific continues to strengthen its healthcare infrastructure, the availability and affordability of cataract surgery and intraocular lenses are expanding to a broader patient population.

Japan Intraocular Lens (IOL) Market Insight

The Japan intraocular lens market is gaining momentum due to the country’s rapidly aging population and increasing demand for advanced ophthalmic treatments. The Japanese market places a strong emphasis on high-quality healthcare solutions, and the adoption of intraocular lenses is driven by the rising number of cataract surgeries performed each year. The integration of advanced surgical technologies and premium intraocular lenses is supporting improved visual outcomes for patients. Moreover, Japan's strong focus on medical innovation and precision healthcare is likely to spur demand for advanced vision correction solutions across both hospitals and specialized eye care clinics.

India Intraocular Lens (IOL) Market Insight

The India intraocular lens market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large patient population suffering from cataracts and other age-related eye disorders. India stands as one of the largest markets for cataract surgeries, and intraocular lenses are increasingly used in both public and private healthcare facilities. Government initiatives aimed at eliminating preventable blindness, along with expanding healthcare infrastructure and improving access to ophthalmic care, are driving market growth. The availability of affordable intraocular lenses and the presence of strong domestic manufacturers are key factors propelling the market in India.

Intraocular Lens (IOL) Market Share

The Intraocular Lens (IOL) industry is primarily led by well-established companies, including:

- Alcon Inc. (Switzerland)

- Johnson & Johnson Services, Inc. (U.S.)

- Bausch + Lomb Corporation (Canada)

- Carl Zeiss Meditec AG (Germany)

- HOYA Corporation (Japan)

- STAAR Surgical Company (U.S.)

- Rayner Intraocular Lenses Limited (U.K.)

- HumanOptics Holding AG (Germany)

- Lenstec, Inc. (U.S.)

- Ophtec BV (Netherlands)

- SIFI S.p.A. (Italy)

- Medicontur Medical Engineering Ltd. (Hungary)

- Aurolab (India)

- Biotech Vision Care Pvt. Ltd. (India)

- Hanita Lenses (Israel)

- SAV-IOL SA (Switzerland)

- Care Group (India)

- Omni Lens Pvt Ltd (India)

- Visioncare Ophthalmic Technologies (India)

- Eyekon Medical, Inc. (U.S.)

What are the Recent Developments in Global Intraocular Lens (IOL) Market?

- In October 2025, Johnson & Johnson announced that more than 100,000 TECNIS Odyssey intraocular lenses had been implanted since the product’s launch, marking a significant adoption milestone in cataract surgery. The achievement demonstrates the growing acceptance of advanced presbyopia-correcting intraocular lenses that help patients achieve improved vision without relying heavily on glasses after surgery

- In June 2025, Johnson & Johnson expanded the launch of its TECNIS Odyssey intraocular lens across Europe, the Middle East, and Canada following its earlier introduction in the U.S. The lens is designed to deliver clear and continuous vision at all distances using a unique diffractive surface technology. The rollout reflects the company’s strategy to strengthen its presence in advanced presbyopia-correcting intraocular lens solutions worldwide

- In April 2025, Alcon, a global leader in eye care, announced the launch of the Clareon PanOptix Pro intraocular lens in the U.S., designed to improve trifocal vision performance with reduced light scatter and higher light utilization. The lens uses advanced optical technology to provide improved contrast and uninterrupted vision across near, intermediate, and distance ranges, supporting better visual outcomes for cataract patients undergoing lens replacement surgery. This development highlights Alcon’s continued innovation in premium intraocular lens technology

- In April 2023, Carl Zeiss Meditec AG announced that the CT LUCIA 621P monofocal intraocular lens received approval from the U.S. Food and Drug Administration (FDA). The lens features the ZEISS optic design and is intended to improve visual outcomes for cataract patients undergoing lens replacement surgery. This regulatory approval strengthened ZEISS’s portfolio in the U.S. ophthalmic surgical device market

- In January 2023, Bausch + Lomb announced the acquisition of AcuFocus, Inc., a medical device company specializing in small-aperture intraocular lens technology used for cataract and refractive surgery. The acquisition expanded Bausch + Lomb’s ophthalmic surgical portfolio and strengthened its capabilities in advanced intraocular lens technologies designed to enhance vision correction outcomes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.