Global Intraventricular Neuroendoscopy Devices Market

Market Size in USD Million

USD

290.36 Million

USD

462.78 Million

2025

2033

USD

290.36 Million

USD

462.78 Million

2025

2033

| 2026 - 2033 | |

| USD 290.36 Million | |

| USD 462.78 Million | |

| % | |

|

Intraventricular Neuroendoscopy Devices Market Overview

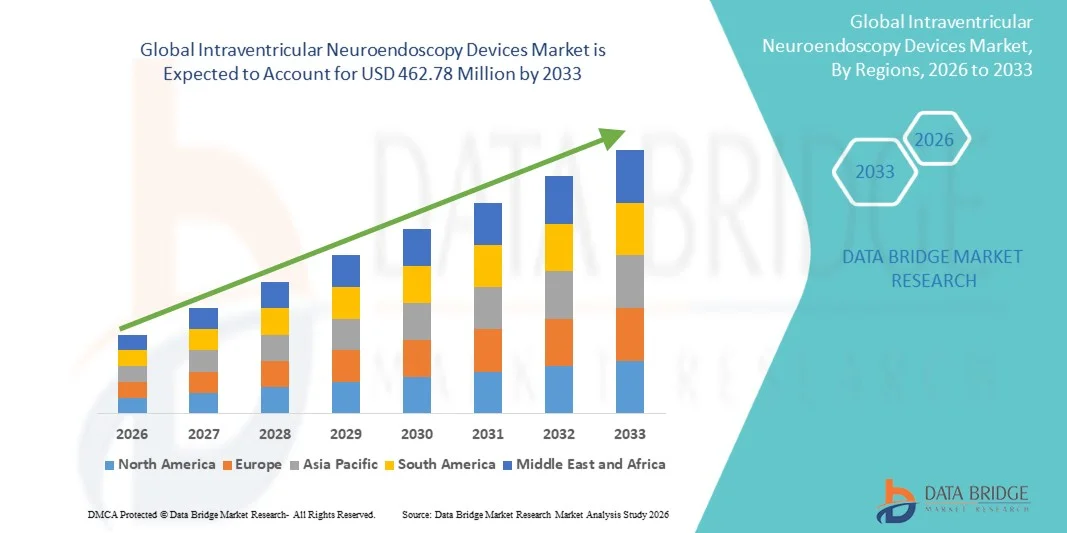

The Intraventricular Neuroendoscopy Devices Market was valued at USD 290.36 million in 2025 and is projected to reach USD 462.78 million by 2033, growing at a CAGR of 6.00% from 2026 to 2033. The market is witnessing steady expansion driven by the rising prevalence of intraventricular brain tumors, hydrocephalus, and other cerebrospinal fluid (CSF)-related disorders, along with increasing preference for minimally invasive neurosurgical procedures. Advancements in high-definition endoscopic imaging systems, improved visualization tools, and precision-guided surgical instruments are further supporting clinical adoption across neurosurgery centers and hospitals.

The growing burden of neurological disorders globally, coupled with increasing geriatric population and higher rates of neurotrauma cases, is significantly boosting demand for intraventricular neuroendoscopy procedures. In addition, the shift toward minimally invasive neurosurgery is reducing patient recovery time, hospital stay duration, and surgical complications, encouraging wider clinical acceptance. Expanding healthcare infrastructure, rising neurosurgical capabilities in emerging economies, and continuous innovation in fiber-optic and 3D endoscopic technologies are further accelerating market growth across both developed and developing regions.

Key Market Trends & Insights

- North America dominated the Intraventricular Neuroendoscopy Devices Market with the largest revenue share of 37.6% in 2025, supported by advanced neurosurgical infrastructure, high adoption of minimally invasive procedures, and strong presence of specialized neurosurgery centers.

- The Intraventricular segment led the market with a 58.4% share in 2025, driven by its widespread use in treating hydrocephalus, intraventricular tumors, and cerebrospinal fluid (CSF) flow abnormalities.

- Asia-Pacific is expected to be the fastest-growing region from 2026 to 2033, expanding at a CAGR of 7.4%, fueled by rising neurological disorder prevalence, expanding neurosurgical capabilities, and increasing healthcare investments in China, India, and Southeast Asia.

- Transnasal are the fastest-growing surgery type, projected to register a CAGR of 6.8%, reflecting the surge in use in minimally invasive skull base and ventricular-adjacent tumor access procedures.

- The Rigid Neuroendoscopes segment dominated the device type category with a 61.2% revenue share in 2025, led by their superior image clarity, higher durability, and widespread use in standard intraventricular procedures such as hydrocephalus treatment and tumor biopsy.

- Hydrocephalus Treatment deployment accounted for 42.6% of the market, preferred by the high global prevalence of cerebrospinal fluid circulation disorders, particularly among pediatric and elderly populations.

- The Intraventricular Tumor Resection segment is the fastest-growing application category, with a CAGR of 7.5%, driven by rising incidence of brain tumors and growing preference for minimally invasive tumor removal techniques.

Market Size & Forecast

- Global Market Value (2025): USD 290.36 Million

- Expected Market Value (2033): USD 462.78 Million

- Forecast CAGR (2026–2033): 6.00%

- Leading Region in 2025:

- Fastest Growing Region:

Report Scope and Intraventricular Neuroendoscopy Devices Market Segmentation

|

Attributes |

Intraventricular Neuroendoscopy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Karl Storz SE & Co. KG (Germany) · Richard Wolf GmbH (Germany) · Olympus Corporation (Japan) · Stryker (U.S.) · Medtronic (Ireland) · B. Braun SE (Germany) · Aesculap, Inc. (Germany) · Integra LifeSciences Holdings Corporation (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Zimmer Biomet (U.S.) · Natus Medical Incorporated (U.S.) · FUJIFILM Holdings Corporation (Japan) · Smith & Nephew (U.K.) · GE HealthCare (U.S.) · CANON MEDICAL SYSTEMS CORPORATION (Japan) · Brainlab AG (Germany) · Micromar Indústria e Comércio Ltda. (Brazil) · Claron Technology Inc. (Canada) · Inomed Medizintechnik GmbH (Germany) · Schölly Fiberoptic GmbH (Germany) |

|

Market Opportunities |

· Rising adoption of minimally invasive neurosurgery in emerging economies · Integration of AI-driven surgical navigation and real-time imaging · Increasing use of neuroendoscopy in pediatric hydrocephalus and congenital brain disorders |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Intraventricular Neuroendoscopy Devices Market Trends

Trend: Advancements in Neuroendoscopic Visualization & Imaging Systems

The market is witnessing a strong shift toward next-generation visualization technologies that significantly enhance surgical clarity and precision during intraventricular procedures. Modern neuroendoscopic systems now incorporate ultra-high-definition (4K and beyond) imaging, 3D stereoscopic visualization, and improved illumination technologies that allow surgeons to clearly differentiate between delicate neural structures and pathological tissues. In addition, the integration of digital enhancement tools such as real-time image sharpening, contrast optimization, and fluorescence-guided visualization is improving accuracy in tumor resection and cerebrospinal fluid pathway management. These advancements are also reducing intraoperative risks such as accidental tissue damage and improving overall procedural efficiency in complex neurosurgical cases.

For instance, adoption of advanced 4K 3D neuroendoscopic platforms in tertiary neurosurgical centers has significantly improved precision in intraventricular tumor excision and reduced postoperative neurological complications.

Intraventricular Neuroendoscopy Devices Market Dynamics

Key Market Driver: Rising Prevalence of Hydrocephalus and Intraventricular Tumors

The increasing global incidence of neurological disorders such as hydrocephalus, brain tumors, and ventricular cysts is one of the strongest drivers of market growth. This burden is particularly high among neonates, pediatric patients, and the aging population, all of whom are more susceptible to cerebrospinal fluid circulation abnormalities. As awareness of minimally invasive neurosurgical options grows, clinicians are increasingly opting for neuroendoscopic procedures such as endoscopic third ventriculostomy over traditional shunt surgeries due to lower infection risks, fewer long-term complications, and improved patient outcomes. In addition, improved diagnostic imaging capabilities are enabling earlier detection of intraventricular pathologies, further increasing procedural volumes and device demand.

For instance, rising adoption of neuroendoscopic third ventriculostomy in pediatric hydrocephalus management has reduced long-term dependence on ventriculoperitoneal shunt procedures in specialized neurosurgical centers.

Key Restraint/Challenge: Limited Surgical Expertise and High Procedural Complexity

Despite technological advancements, the market faces significant challenges due to the complexity of intraventricular procedures and the limited availability of highly trained neuroendoscopic surgeons. Operating within the ventricular system requires extreme precision, as even minor deviations can lead to severe neurological damage or complications such as hemorrhage and infection. The steep learning curve associated with mastering neuroendoscopic techniques restricts adoption to specialized tertiary care hospitals and academic neurosurgery centers. Moreover, the requirement for integrated operating room setups, advanced imaging support systems, and continuous training programs increases the operational burden for healthcare facilities, particularly in resource-constrained regions.

For instance, many hospitals in developing countries continue to rely on conventional neurosurgical methods due to a shortage of trained neuroendoscopic specialists and limited access to advanced surgical training infrastructure.

Key Market Opportunity: Integration of AI and Image-Guided Neuroendoscopic Navigation Systems

The integration of artificial intelligence and advanced image-guided navigation technologies is creating transformative opportunities in the intraventricular neuroendoscopy devices market. AI-powered systems can assist neurosurgeons by providing real-time anatomical mapping, automated trajectory optimization, and predictive surgical guidance based on patient-specific brain models. These systems enhance precision, reduce cognitive load on surgeons, and minimize intraoperative risks, especially in complex or high-risk cases. Furthermore, cloud-based surgical planning platforms and machine learning algorithms trained on large datasets are enabling continuous improvement in procedural accuracy and outcome prediction. This is also driving the development of semi-automated and robotic-assisted neuroendoscopic systems, which are expected to expand accessibility and standardization of complex neurosurgical procedures globally.

For instance, AI-integrated neuro-navigation platforms used in complex ventricular tumor surgeries have demonstrated improved accuracy in surgical targeting and reduced postoperative complication rates in high-volume neurosurgical institutes.

Intraventricular Neuroendoscopy Devices Market Scope

The intraventricular neuroendoscopy devices market is segmented on the basis of surgery type, device type, application, and end user.

- By Surgery Type

On the basis of surgery type, the Intraventricular Neuroendoscopy Devices Market is segmented into intraventricular procedures, transcranial approaches, and transnasal neurosurgical procedures. The Intraventricular Surgery segment dominated the market with a 58.4% share in 2025, owing to its widespread use in treating hydrocephalus, intraventricular tumors, and cerebrospinal fluid (CSF) flow abnormalities. These procedures are considered the gold standard for minimally invasive access to deep brain ventricles, offering reduced surgical trauma, lower infection risk, and faster recovery compared to open cranial surgeries. Growing adoption of endoscopic third ventriculostomy and tumor biopsy procedures has further strengthened this segment’s dominance. Hospitals and neurosurgical centers increasingly prefer intraventricular approaches due to improved safety profiles and better patient outcomes. Continuous advancements in endoscopic visualization and navigation systems are further enhancing procedural precision and expanding clinical acceptance.

The Transnasal Surgery segment is expected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing use in minimally invasive skull base and ventricular-adjacent tumor access procedures. This approach avoids cranial opening, significantly reducing postoperative complications, hospital stay duration, and patient recovery time. Advancements in angled endoscopes and high-definition imaging systems are making transnasal routes more feasible for complex neurosurgical cases. Increasing adoption in pituitary and anterior skull base interventions is further supporting growth. Rising demand for cosmetically favorable, less invasive surgical techniques is also accelerating clinical preference. In addition, improved surgical training and navigation technologies are expanding surgeon confidence in transnasal neuroendoscopic procedures.

- By Device Type

On the basis of device type, the market is segmented into rigid neuroendoscopes and flexible neuroendoscopes. The Rigid Neuroendoscopes segment dominated the market with a 61.2% share in 2025, due to their superior image clarity, higher durability, and widespread use in standard intraventricular procedures such as hydrocephalus treatment and tumor biopsy. These devices provide excellent optical precision and are preferred in procedures requiring stable, straight-line access to ventricular structures. Their robust design allows better control during surgical manipulation, making them the most widely adopted tool in neurosurgery. Rigid systems are also more cost-effective and easier to sterilize, contributing to their dominance in hospital settings. Continuous improvements in optical resolution and ergonomic design are further enhancing usability. Strong integration with advanced visualization platforms is reinforcing their clinical importance.

The Flexible Neuroendoscopes segment is expected to grow at the fastest CAGR of 7.2% from 2026 to 2033, driven by their ability to navigate complex and curved ventricular anatomy. These devices allow surgeons to access difficult-to-reach brain regions with minimal tissue disruption, making them highly valuable in complex tumor and cyst procedures. Increasing use in pediatric neurosurgery, where anatomical constraints are more challenging, is further supporting adoption. Technological advancements in miniaturization, fiber-optic imaging, and articulation control are significantly improving performance. Flexible scopes also enable multi-angle visualization, improving diagnostic and therapeutic accuracy. Rising preference for highly versatile surgical tools is accelerating their adoption across advanced neurosurgical centers.

- By Application

On the basis of application, the market is segmented into hydrocephalus treatment, intraventricular tumor resection, cyst fenestration, hemorrhage management, and biopsy procedures. The Hydrocephalus Treatment segment dominated the market with a 42.6% share in 2025, driven by the high global prevalence of cerebrospinal fluid circulation disorders, particularly among pediatric and elderly populations. Endoscopic third ventriculostomy has become a widely accepted alternative to shunt-based procedures due to lower infection rates and improved long-term outcomes. Increasing early diagnosis through advanced neuroimaging is further driving procedural volumes. Hospitals prefer neuroendoscopic solutions for hydrocephalus due to reduced surgical complications and shorter recovery times. Strong clinical guidelines supporting minimally invasive CSF diversion procedures are reinforcing this dominance. Continuous technological improvements in endoscopic precision tools are further enhancing treatment success rates.

The Intraventricular Tumor Resection segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by rising incidence of brain tumors and growing preference for minimally invasive tumor removal techniques. Neuroendoscopy allows direct visualization and targeted removal of intraventricular tumors with minimal damage to surrounding brain tissue. Increasing use of biopsy-guided resection techniques is improving diagnostic accuracy and surgical planning. Advancements in navigation-assisted surgery and intraoperative imaging are enhancing tumor localization. Growing demand for precision oncology and early intervention is further supporting adoption. In addition, expanding neurosurgical expertise in emerging markets is accelerating procedural uptake.

- By End Users

On the basis of end users, the market is segmented into hospitals, specialty clinics, and others (including academic and research institutes). The Hospitals segment dominated the market with a 68.9% share in 2025, due to the availability of advanced neurosurgical infrastructure, highly skilled surgeons, and integrated imaging systems required for complex intraventricular procedures. Hospitals handle the majority of hydrocephalus treatments, tumor resections, and emergency neurosurgical cases, making them the primary adoption centers for neuroendoscopy devices. Strong investment in neurosurgical operating rooms and hybrid surgical suites is further strengthening hospital dominance. In addition, higher patient inflow and reimbursement support are contributing to increased procedural volumes. Hospitals also benefit from continuous training programs and multidisciplinary neurosurgical teams. Growing adoption of advanced neuro-navigation systems is further enhancing procedural efficiency in hospital settings.

The Specialty Clinics segment is expected to grow at the fastest CAGR of 7.0% from 2026 to 2033, driven by increasing demand for focused neurosurgical care and outpatient minimally invasive procedures. These clinics are becoming preferred centers for follow-up surgeries, diagnostic neuroendoscopy, and low-risk interventions. Rising patient preference for shorter hospital stays and cost-effective treatment options is supporting growth. Technological advancements in portable neuroendoscopic systems are enabling procedures outside large hospital settings. Increasing establishment of specialized neurology and neurosurgery centers in urban regions is further accelerating adoption. In addition, growing availability of skilled neuroendoscopic surgeons in private practice is contributing to segment expansion.

Intraventricular Neuroendoscopy Devices Market Regional Analysis

North America dominated the Intraventricular Neuroendoscopy Devices Market with the largest revenue share of 37.6% in 2025, supported by advanced neurosurgical infrastructure, high adoption of minimally invasive procedures, and strong presence of specialized neurosurgery centers. The region also benefits from early adoption of high-definition neuroendoscopic visualization systems, strong healthcare expenditure, and widespread use of image-guided and AI-assisted neurosurgical platforms. Increasing prevalence of hydrocephalus, brain tumors, and traumatic brain injuries, along with continuous advancements in surgical technologies and trained neurosurgical workforce, continues to strengthen North America’s leadership position in the global market.

U.S. Intraventricular Neuroendoscopy Devices Market Insight

The U.S. intraventricular neuroendoscopy devices market is witnessing robust growth due to high prevalence of neurological disorders, strong healthcare expenditure, and rapid adoption of advanced minimally invasive neurosurgical techniques. The country’s highly developed neurosurgical infrastructure, along with early integration of AI-driven navigation systems and 3D neuroendoscopic visualization technologies, is significantly boosting procedural accuracy and safety. In addition, increasing clinical research activities, strong presence of leading medical device companies, and continuous innovation in surgical imaging systems are further driving market expansion across hospitals and specialized neurosurgical centers.

Europe Intraventricular Neuroendoscopy Devices Market Insight

The Europe intraventricular neuroendoscopy devices market remains a major contributor to global revenue, driven by strong healthcare systems, early adoption of minimally invasive neurosurgical techniques, and robust clinical training infrastructure. The widespread use of neuroendoscopy in hydrocephalus management, tumor biopsy, and cyst fenestration procedures is supporting market expansion across the region. Increasing investments in advanced visualization technologies and AI-based surgical planning tools, coupled with strict clinical safety standards, continue to enhance adoption across leading neurosurgical centers.

U.K. Intraventricular Neuroendoscopy Devices Market Insight

The U.K. intraventricular neuroendoscopy devices market is experiencing steady growth, supported by increasing adoption of advanced neurosurgical procedures, strong presence of specialized neuroscience hospitals, and rising demand for minimally invasive brain surgeries. Growing investments in surgical training programs and neuroendoscopic research are contributing to improved clinical expertise. Furthermore, integration of high-definition imaging systems and image-guided navigation technologies is enhancing surgical precision, positioning the U.K. as an important innovation hub in the European neurosurgery landscape.

Germany Intraventricular Neuroendoscopy Devices Market Insight

The Germany intraventricular neuroendoscopy devices market is expanding steadily due to strong medical device manufacturing capabilities, advanced neurosurgical research infrastructure, and increasing adoption of precision surgical technologies. Hospitals and academic institutes are increasingly using neuroendoscopy for hydrocephalus treatment, intraventricular tumor resection, and complex diagnostic procedures. Continuous advancements in visualization systems, fiber-optic technologies, and AI-assisted navigation are further improving surgical outcomes and driving market growth in Germany.

Asia-Pacific Intraventricular Neuroendoscopy Devices Market Insight

The Asia-Pacific intraventricular neuroendoscopy devices market is expected to witness rapid growth, driven by rising prevalence of neurological disorders, expanding healthcare infrastructure, and increasing investments in neurosurgical capabilities across countries such as China, India, and Japan. Growing awareness of minimally invasive brain surgery and improving access to advanced neuroimaging technologies are supporting regional market expansion. In addition, rising demand for cost-effective surgical solutions and increasing establishment of specialty neurosurgery centers are accelerating adoption across both public and private healthcare systems.

Japan Intraventricular Neuroendoscopy Devices Market Insight

The Japan intraventricular neuroendoscopy devices market is witnessing consistent growth due to strong focus on advanced medical technologies, high healthcare standards, and increasing adoption of minimally invasive neurosurgical procedures. Leading hospitals and research institutes are increasingly utilizing neuroendoscopy for hydrocephalus management, tumor removal, and diagnostic interventions. Moreover, integration of AI-enabled navigation systems and high-precision imaging technologies is further enhancing surgical accuracy and supporting market expansion.

China Intraventricular Neuroendoscopy Devices Market Insight

The China intraventricular neuroendoscopy devices market is growing rapidly, driven by rising incidence of neurological disorders, expanding neurosurgical infrastructure, and increasing government focus on advanced healthcare modernization. Growing adoption of minimally invasive neurosurgical techniques across tertiary hospitals is significantly boosting demand. In addition, strong investments in medical technology innovation, increasing training of neurosurgeons, and rapid deployment of advanced imaging and navigation systems are positioning China as one of the fastest-growing markets globally.

Intraventricular Neuroendoscopy Devices Market Share

The intraventricular neuroendoscopy devices industry is primarily led by well-established companies, including:

- Karl Storz SE & Co. KG (Germany)

- Richard Wolf GmbH (Germany)

- Olympus Corporation (Japan)

- Stryker (U.S.)

- Medtronic (Ireland)

- Braun SE (Germany)

- Aesculap, Inc. (Germany)

- Integra LifeSciences Holdings Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Zimmer Biomet (U.S.)

- Natus Medical Incorporated (U.S.)

- FUJIFILM Holdings Corporation (Japan)

- Smith & Nephew (U.K.)

- GE HealthCare (U.S.)

- CANON MEDICAL SYSTEMS CORPORATION (Japan)

- Brainlab AG (Germany)

- Micromar Indústria e Comércio Ltda. (Brazil)

- Claron Technology Inc. (Canada)

- Inomed Medizintechnik GmbH (Germany)

- Schölly Fiberoptic GmbH (Germany)

Latest Developments in Intraventricular Neuroendoscopy Devices Market

- In September 2024, Olympus introduced the VISERA S imaging platform, an advanced endoscopic visualization system designed to deliver high-definition imaging and improved diagnostic accuracy for minimally invasive surgical procedures, including neuroendoscopy; the platform enhances visualization quality, supports integrated OR workflows, and strengthens precision in complex neurosurgical interventions

- In January 2023, Olympus launched the VISERA ELITE III surgical visualization platform featuring 4K imaging, 3D visualization, and fluorescence imaging support, significantly enhancing optical clarity and depth perception in minimally invasive neurosurgical procedures, including intraventricular neuroendoscopy applications; this system improved surgical precision and workflow efficiency in advanced operating room environment

- In July 2023, Stryker launched the Q Guidance System with cranial navigation software, improving image-guided neurosurgical procedures through enhanced anatomical mapping, surgical planning, and instrument positioning accuracy; this development supports neuroendoscopy-related workflows such as intraventricular tumor access and biopsy procedures, reinforcing precision-based neurosurgical approaches

- In June 2022, KARL STORZ expanded its IMAGE1 S imaging platform capabilities with enhanced 4K visualization and advanced digital image processing technologies, improving clarity and detail during minimally invasive endoscopic procedures, including neuroendoscopy; this upgrade strengthened surgical visualization performance and supported more precise intracranial interventions in neurosurgical applications

- In October 2021, Medtronic advanced its StealthStation surgical navigation platform with updated cranial guidance software, improving real-time surgical navigation, preoperative planning, and intraoperative accuracy in neurosurgical procedures; this enhancement supports neuroendoscopic workflows by enabling better orientation and safer access to deep brain structures during minimally invasive interventions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.