Global Introducer Sheaths And Guidewires Market

Market Size in USD Billion

USD

2.88 Billion

USD

4.42 Billion

2025

2033

USD

2.88 Billion

USD

4.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.88 Billion | |

| USD 4.42 Billion | |

| % | |

|

Introducer Sheaths and Guidewires Market Overview

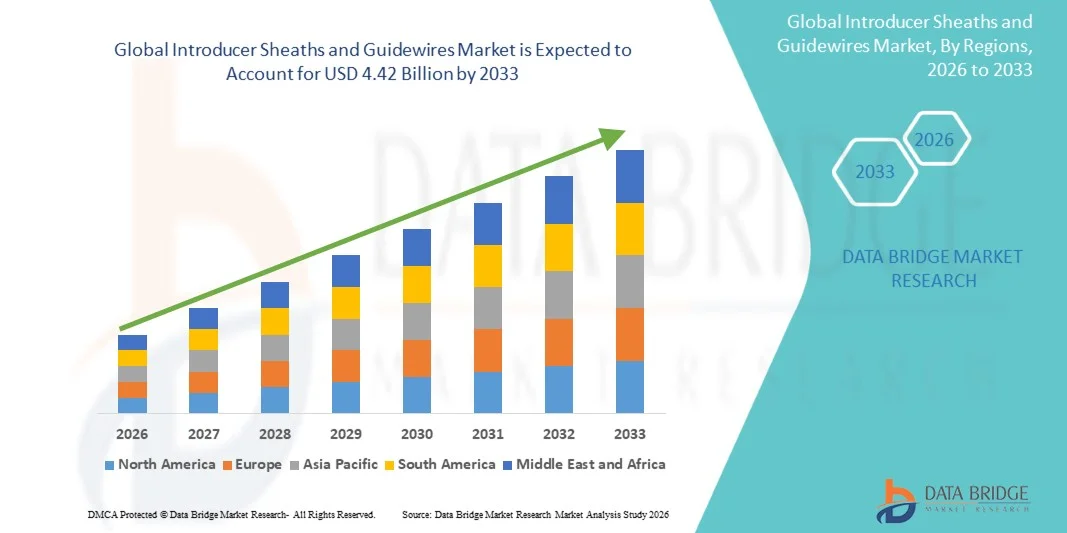

The Introducer Sheaths and Guidewires Market was valued at USD 2.88 billion in 2025 and is projected to reach USD 4.42 billion by 2033, growing at a CAGR of 5.53% from 2026 to 2033. The market is witnessing steady growth driven by the increasing prevalence of cardiovascular and neurovascular disorders, rising demand for minimally invasive procedures, and continuous technological advancements in interventional devices.

The growing global burden of chronic diseases such as coronary artery disease, peripheral artery disease, and stroke, combined with the rising aging population, is accelerating the adoption of introducer sheaths and guidewires across hospitals and catheterization laboratories. Healthcare providers are increasingly shifting toward minimally invasive surgical procedures due to reduced recovery times, lower complication risks, and improved procedural precision. In addition, advancements in hydrophilic coatings, steerable guidewire technologies, and imaging-compatible introducer systems are enhancing procedural efficiency and supporting broader applications across cardiology, radiology, urology, and neurovascular interventions.

Key Market Trends & Insights

- North America dominated the Introducer Sheaths and Guidewires Market with the largest revenue share of 38.42% in 2025, supported by advanced healthcare infrastructure, high procedural volumes, and strong adoption of minimally invasive cardiovascular interventions.

- The Guidewires segment led the market with a 57.36% share in 2025, driven by their extensive use across cardiovascular, neurovascular, peripheral vascular, and urology procedures.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.4% from 2026 to 2033, fueled by expanding healthcare access, rising cardiovascular disease prevalence, and increasing investments in interventional care across China, India, and Japan.

- Introducer Sheaths are the fastest-growing product type, projected to register a CAGR of 6.2%, reflecting the surge in demand for safer vascular access and improved procedural support during minimally invasive interventions.

- The Stainless Steel segment dominated the material category with a 34.82% revenue share in 2025, led by its superior strength, durability, and widespread use in conventional guidewire manufacturing.

- Administration of Medicine accounted for 63.58% of the market, preferred by the growing use of guidewire-assisted catheter systems in cardiovascular, oncology, and interventional radiology treatments.

- The Administration of Fluids segment is the fastest-growing application category, with a CAGR of 5.9%, driven by increasing demand for safe vascular access systems in emergency care, critical care, and surgical applications.

Market Size & Forecast

- Global Market Value (2025): USD 2.88 Billion

- Expected Market Value (2033): USD 4.42 Billion

- Forecast CAGR (2026–2033): 5.53%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Introducer Sheaths and Guidewires Market Segmentation

|

Attributes |

Introducer Sheaths and Guidewires Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Boston Scientific Corporation (U.S.) · Medtronic (Ireland) · Abbott (U.S.) · Teleflex Incorporated (U.S.) · Terumo Corporation (Japan) · B. Braun SE (Germany) · Cook (U.S.) · Cardinal Health (U.S.) · Stryker Corporation (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Integer Holdings Corporation (U.S.) · Merit Medical Systems, Inc. (U.S.) · Penumbra, Inc. (U.S.) · Asahi Intecc Co., Ltd. (Japan) · Lepu Medical Technology (China) · Biotronik SE & Co. KG (Germany) · Oscor Inc. (U.S.) · Meril Life Sciences Pvt. Ltd. (India) · AngioDynamics, Inc. (U.S.) · Well Lead Medical Co., Ltd. (China) |

|

Market Opportunities |

· Expanding adoption of minimally invasive cardiovascular and neurovascular procedures · Rising healthcare investments in emerging economies · Increasing integration of hydrophilic coatings and imaging-compatible technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Introducer Sheaths and Guidewires Market Trends

Trend: Rising Adoption of Minimally Invasive Interventional Procedures

Hospitals and specialty care centers are increasingly adopting advanced introducer sheaths and guidewires to support minimally invasive cardiovascular, neurovascular, and peripheral vascular procedures that reduce surgical trauma, shorten recovery times, and improve procedural accuracy. The growing preference for catheter-based interventions is encouraging manufacturers to develop hydrophilic-coated guidewires, steerable navigation systems, and kink-resistant sheath technologies that enhance physician control and procedural efficiency. In addition, imaging-compatible materials and improved torque response capabilities are enabling safer navigation through complex anatomies during high-risk interventional procedures.

For instance, in February 2024, Terumo Corporation expanded its interventional systems portfolio with advanced guidewire technologies designed to improve navigation and procedural precision during complex cardiovascular interventions.

Introducer Sheaths and Guidewires Market Dynamics

Key Market Driver: Increasing Prevalence of Cardiovascular and Neurovascular Disorders

The rising global burden of cardiovascular diseases, stroke, and peripheral artery disorders has significantly increased the demand for introducer sheaths and guidewires used in minimally invasive diagnostic and therapeutic procedures. Healthcare providers are increasingly relying on advanced interventional devices to perform angioplasty, catheterization, thrombectomy, and structural heart procedures with improved precision and lower complication risks. Growing elderly populations, sedentary lifestyles, and increasing incidences of diabetes and hypertension are further accelerating procedure volumes and supporting continuous demand for high-performance vascular access technologies across hospitals and catheterization laboratories worldwide.

For instance, in January 2024, Boston Scientific Corporation introduced enhanced interventional guidewire solutions aimed at improving support and maneuverability during complex coronary and peripheral procedures.

Key Restraint/Challenge: High Cost and Regulatory Complexity of Advanced Interventional Devices

A major restraint in the Introducer Sheaths and Guidewires Market is the high development and procurement cost associated with technologically advanced interventional devices and specialty-coated systems. Manufacturers must comply with stringent regulatory standards related to material safety, biocompatibility, sterility, and clinical performance before obtaining product approvals across major healthcare markets. In addition, hospitals and ambulatory surgical centers often face budget limitations associated with adopting premium guidewire technologies and single-use vascular access systems, particularly in price-sensitive and developing healthcare environments where reimbursement support remains limited.

For instance, in March 2024, Medtronic plc highlighted increasing regulatory and compliance investments associated with the development of next-generation vascular access and interventional product platforms.

Key Market Opportunity: Expansion of Advanced Neurovascular and Peripheral Interventions

The growing adoption of advanced neurovascular and peripheral vascular procedures presents significant growth opportunities for manufacturers of introducer sheaths and guidewires with enhanced navigation and flexibility capabilities. Increasing investments in stroke treatment infrastructure, peripheral artery disease management, and image-guided interventions are driving demand for specialized guidewire systems capable of navigating highly complex vascular anatomies. Furthermore, ongoing innovations in hydrophilic coatings, steerability, and microcatheter compatibility are enabling the development of next-generation interventional solutions tailored for precision-based minimally invasive therapies across emerging and developed healthcare markets.

For instance, in May 2024, Stryker Corporation expanded its neurovascular product portfolio with advanced access technologies designed to support minimally invasive stroke and aneurysm treatment procedures.

Introducer Sheaths and Guidewires Market Scope

The introducer sheaths and guidewires market is segmented on the basis of product type, material, application, and end user.

- By Product Type

On the basis of product type, the Introducer Sheaths and Guidewires Market is segmented into introducer sheaths and guidewires. The Guidewires segment dominated the market with a 57.36% share in 2025, driven by their extensive use across cardiovascular, neurovascular, peripheral vascular, and urology procedures. Guidewires are essential components in minimally invasive interventions, enabling precise catheter navigation through complex anatomical pathways. Continuous advancements in hydrophilic coatings, torque control, and steerability are significantly improving procedural efficiency and physician control. Increasing prevalence of cardiovascular diseases and rising demand for angioplasty and catheterization procedures are further accelerating adoption. Hospitals and catheterization laboratories rely heavily on advanced guidewire systems for complex interventional procedures. The segment also benefits from growing technological innovation and increasing procedure volumes globally.

The Introducer Sheaths segment is projected to register the fastest growth at a CAGR of 6.2% from 2026 to 2033, driven by rising demand for safer vascular access and improved procedural support during minimally invasive interventions. These devices help facilitate smooth catheter insertion while minimizing vessel trauma and reducing procedural complications. Increasing adoption of image-guided surgeries and interventional radiology procedures is supporting strong segment growth. Technological advancements such as steerable sheaths, hemostatic valves, and kink-resistant materials are improving clinical outcomes and physician convenience. Growing investments in neurovascular and structural heart procedures are also increasing demand for advanced introducer systems. Expanding healthcare infrastructure and rising awareness regarding minimally invasive treatment approaches continue to support long-term growth opportunities.

- By Material

On the basis of material, the Introducer Sheaths and Guidewires Market is segmented into stainless steel, nitinol, polyurethane, PTFE, silicone-based materials, and hybrid materials. The Stainless Steel segment dominated the market with a 34.82% share in 2025 owing to its superior strength, durability, and widespread use in conventional guidewire manufacturing. Stainless steel materials provide excellent pushability and torque transmission, making them highly suitable for routine cardiovascular and peripheral interventions. Their cost-effectiveness and established clinical reliability continue to support extensive adoption across healthcare facilities worldwide. These materials are widely preferred in standard interventional procedures requiring high mechanical stability and consistent performance. Manufacturers also benefit from mature production technologies and lower raw material costs associated with stainless steel products. The segment maintains strong demand due to its broad application range and long-standing clinical acceptance.

The Nitinol segment is expected to witness the fastest growth at a CAGR of 6.1% from 2026 to 2033, driven by increasing demand for flexible, kink-resistant, and shape-memory interventional devices. Nitinol-based guidewires and introducer systems offer superior navigation capabilities in complex vascular anatomies compared to traditional materials. Growing adoption of minimally invasive neurovascular and peripheral vascular procedures is significantly accelerating demand for nitinol products. These materials provide enhanced durability, improved patient safety, and better procedural efficiency during challenging interventions. Continuous innovation in alloy engineering and coating technologies is further strengthening their clinical performance. Rising physician preference for highly maneuverable and atraumatic devices is also contributing to rapid segment expansion globally.

- By Application

On the basis of application, the Introducer Sheaths and Guidewires Market is segmented into administration of medicine and administration of fluids. The Administration of Medicine segment dominated the market with a 63.58% share in 2025 due to the growing use of guidewire-assisted catheter systems in cardiovascular, oncology, and interventional radiology treatments. These devices enable accurate delivery of therapeutic agents, embolization materials, and minimally invasive treatment solutions directly to targeted anatomical locations. Increasing prevalence of chronic diseases and rising procedural volumes are driving strong demand for precision-based vascular access technologies. Healthcare providers increasingly prefer minimally invasive drug administration techniques because they reduce complications, improve treatment outcomes, and shorten hospital stays. Technological advancements in catheter compatibility and vascular navigation systems are also improving procedural success rates. The segment continues to benefit from expanding interventional healthcare infrastructure worldwide.

The Administration of Fluids segment is projected to register the fastest growth at a CAGR of 5.9% from 2026 to 2033, supported by increasing demand for safe vascular access systems in emergency care, critical care, and surgical applications. Introducer sheaths and guidewires are increasingly used for efficient fluid management during complex medical procedures and intensive care treatments. Rising hospitalization rates and expanding surgical volumes are contributing to higher utilization of advanced vascular access technologies. Healthcare facilities are also emphasizing infection prevention and procedural safety, supporting demand for improved sheath designs and biocompatible materials. Growing adoption of minimally invasive procedures across emerging healthcare markets is further accelerating segment growth. Continuous product innovation focused on ease of insertion and reduced vessel trauma is strengthening future market expansion.

- By End User

On the basis of end user, the Introducer Sheaths and Guidewires Market is segmented into hospitals, clinics, and ambulatory centres. The Hospitals segment dominated the market with a 61.24% share in 2025, driven by high patient inflow, advanced interventional infrastructure, and increasing volumes of minimally invasive procedures. Hospitals perform a large number of cardiovascular, neurovascular, and peripheral vascular interventions that require sophisticated guidewire and introducer sheath technologies. Availability of skilled specialists, catheterization laboratories, and advanced imaging systems further supports strong segment dominance. Increasing investments in surgical modernization and interventional cardiology departments are accelerating adoption of technologically advanced vascular access devices. Hospitals also benefit from favorable reimbursement structures and higher purchasing capacities for premium interventional products. The segment continues to lead due to rising procedural complexity and growing demand for precision-guided treatments globally.

The Ambulatory Centres segment is expected to witness the fastest growth at a CAGR of 6.4% from 2026 to 2033, driven by increasing preference for outpatient minimally invasive procedures and cost-effective treatment environments. These centers offer shorter patient stays, reduced healthcare costs, and faster procedural turnaround compared to traditional hospital settings. Growing advancements in portable imaging systems and compact interventional technologies are enabling more procedures to be performed in ambulatory environments. Rising demand for same-day surgeries and outpatient vascular interventions is significantly supporting segment expansion. Healthcare systems are also increasingly focusing on reducing hospital burden and improving procedural efficiency through decentralized care models. Expanding healthcare accessibility and growing patient preference for convenient treatment options continue to create strong growth opportunities for ambulatory centres worldwide.

Introducer Sheaths and Guidewires Market Regional Analysis

North America dominated the Introducer Sheaths and Guidewires Market with the largest revenue share of 38.42% in 2025, supported by advanced healthcare infrastructure, high procedural volumes, and strong adoption of minimally invasive cardiovascular interventions. The region also benefits from rising prevalence of cardiovascular and neurovascular disorders, favorable reimbursement policies, and rapid adoption of technologically advanced vascular access devices across hospitals and catheterization laboratories. Increasing investments in interventional cardiology, growing demand for precision-guided procedures, and continuous innovation in hydrophilic coatings and steerable guidewire technologies continue to strengthen North America’s leadership position in the global market.

U.S. Introducer Sheaths and Guidewires Market Insight

The U.S. introducer sheaths and guidewires market is witnessing strong growth due to rising volumes of minimally invasive cardiovascular and neurovascular procedures, increasing prevalence of chronic diseases, and rapid adoption of advanced interventional technologies. The country’s highly developed healthcare infrastructure, along with strong presence of leading medical device manufacturers and catheterization laboratories, is driving demand across hospitals and specialty care centers. In addition, growing emphasis on precision-guided interventions, favorable reimbursement frameworks, and continuous innovation in hydrophilic coatings and steerable guidewire systems is accelerating market expansion across the United States.

Europe Introducer Sheaths and Guidewires Market Insight

The Europe introducer sheaths and guidewires market remains a major contributor to global revenue, driven by strong healthcare infrastructure, technological innovation, and increasing demand for minimally invasive interventional procedures. The widespread adoption of advanced vascular access devices across cardiology, radiology, and neurovascular applications is supporting market expansion throughout the region. Increasing investments in interventional healthcare technologies, coupled with growing elderly population and rising prevalence of cardiovascular disorders, continue to enhance the adoption of introducer sheaths and guidewires across Europe.

U.K. Introducer Sheaths and Guidewires Market Insight

The U.K. introducer sheaths and guidewires market is experiencing steady growth, supported by increasing adoption of minimally invasive surgical procedures, rising cardiovascular disease burden, and growing investments in advanced healthcare technologies. Increasing demand for precision-based vascular access devices and image-guided interventions is contributing significantly to market expansion. Furthermore, advancements in guidewire coating technologies, steerable catheter systems, and interventional radiology procedures are improving procedural efficiency and patient outcomes, positioning the U.K. as an important market for interventional medical devices.

Germany Introducer Sheaths and Guidewires Market Insight

The Germany introducer sheaths and guidewires market is expanding steadily due to the country’s advanced healthcare system, strong medical technology sector, and increasing adoption of next-generation interventional devices. Hospitals and specialty clinics are increasingly utilizing advanced guidewires and introducer systems for cardiovascular, peripheral vascular, and neurovascular procedures. Continuous advancements in minimally invasive surgical technologies, hydrophilic coatings, and imaging-compatible devices, along with strong focus on healthcare innovation and patient safety, are further driving market growth in Germany.

Asia-Pacific Introducer Sheaths and Guidewires Market Insight

The Asia-Pacific introducer sheaths and guidewires market is expected to witness rapid growth, driven by expanding healthcare infrastructure, rising cardiovascular disease prevalence, and increasing investments in minimally invasive treatment capabilities across countries such as China, India, and Japan. Growing awareness regarding early disease diagnosis, rising adoption of advanced interventional technologies, and increasing demand for cost-effective vascular access solutions are supporting regional market expansion. In addition, the growing presence of medical device manufacturing facilities and improving healthcare accessibility are accelerating adoption across hospitals and specialty care centers.

Japan Introducer Sheaths and Guidewires Market Insight

The Japan introducer sheaths and guidewires market is witnessing consistent growth due to rising investments in advanced interventional healthcare technologies, increasing aging population, and growing demand for minimally invasive cardiovascular procedures. Hospitals and research institutions are increasingly adopting high-performance guidewires and introducer systems for precision-based diagnostic and therapeutic applications. Moreover, continuous advancements in vascular navigation technologies and the country’s strong focus on high-quality healthcare and patient safety standards are further contributing to market growth.

China Introducer Sheaths and Guidewires Market Insight

The China introducer sheaths and guidewires market is growing rapidly, driven by expanding healthcare infrastructure, increasing prevalence of cardiovascular disorders, and rising government focus on improving access to advanced medical treatments. Growing adoption of minimally invasive procedures across hospitals and specialty centers is significantly boosting demand for advanced vascular access devices. In addition, rising investments in medical device manufacturing, increasing awareness regarding early interventional treatment, and rapid technological advancements are positioning China as one of the fastest-growing markets for introducer sheaths and guidewires globally.

Introducer Sheaths and Guidewires Market Share

The introducer sheaths and guidewires industry is primarily led by well-established companies, including:

- Boston Scientific Corporation (U.S.)

- Medtronic (Ireland)

- Abbott (U.S.)

- Teleflex Incorporated (U.S.)

- Terumo Corporation (Japan)

- Braun SE (Germany)

- Cook (U.S.)

- Cardinal Health (U.S.)

- Stryker Corporation (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Integer Holdings Corporation (U.S.)

- Merit Medical Systems, Inc. (U.S.)

- Penumbra, Inc. (U.S.)

- Asahi Intecc Co., Ltd. (Japan)

- Lepu Medical Technology (China)

- Biotronik SE & Co. KG (Germany)

- Oscor Inc. (U.S.)

- Meril Life Sciences Pvt. Ltd. (India)

- AngioDynamics, Inc. (U.S.)

- Well Lead Medical Co., Ltd. (China)

Latest Developments in Introducer Sheaths and Guidewires Market

- In December 2025, Atraverse Medical received U.S. FDA 510(k) clearance for its HOTWIRE™ Fully Integrated Transseptal Access System, combining the HOTWIRE™ RF Guidewire and RF Generator for left-heart access procedures. The system is designed to improve procedural workflow efficiency, enhance control during transseptal access, and support compatibility with multiple sheath systems. This milestone highlights continued advancements in guidewire-enabled electrophysiology and structural heart interventions

- In October 2025, Medtronic plc announced the launch of the Stedi™ Extra Support Guidewire, developed to enhance stability and predictability during transcatheter aortic valve replacement (TAVR) procedures. The guidewire is compatible with commercially available TAVR systems and is designed to improve valve deployment performance for patients with severe aortic stenosis. This launch reflects increasing innovation in guidewire technologies for structural heart interventions

- In September 2025, BrosMed Medical announced CE MDR approval for its Pregarde™ Guiding Sheath, designed for peripheral diagnostic and interventional procedures. The sheath features a hydrophilic coating, reinforced triple-layer structure, and radiopaque marker technology to improve navigation, support, and procedural safety. The approval reinforces the company’s expansion in the European interventional vascular device market

- In August 2025, Merit Medical Systems announced the U.S. commercial launch of its Prelude Wave™ Hydrophilic Sheath Introducer with SnapFix™ Technology, designed to improve radial access procedures by reducing arterial spasm and occlusion risks. The new sheath introducer features enhanced lubricity, kink resistance, and securement performance to improve procedural efficiency and patient comfort during cardiovascular interventions. This development highlights the growing focus on advanced vascular access technologies in minimally invasive procedures

- In July 2025, Stryker Corporation announced the launch of the next-generation InThrill® Thrombectomy System through its Inari Medical division. The system includes an advanced InThrill sheath and over-the-wire thrombectomy catheter designed for small vessel and arteriovenous access thrombectomy procedures. The development strengthens Stryker’s vascular intervention portfolio and demonstrates increasing innovation in sheath-supported thrombectomy technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.