Global Ion Implantation Equipment Market

Market Size in USD Billion

USD

7.42 Billion

USD

13.88 Billion

2025

2033

USD

7.42 Billion

USD

13.88 Billion

2025

2033

| 2026 - 2033 | |

| USD 7.42 Billion | |

| USD 13.88 Billion | |

| % | |

|

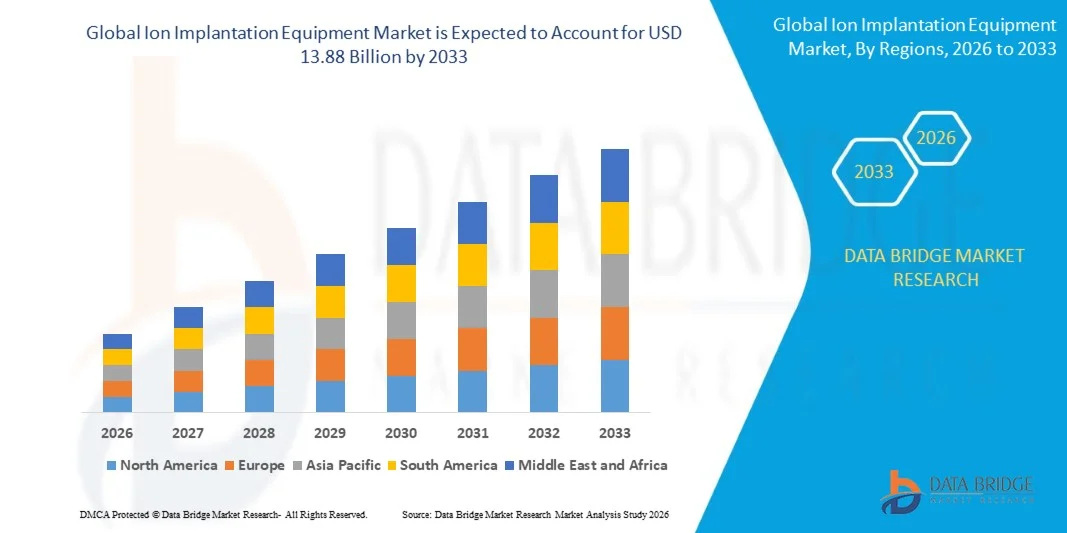

Ion Implantation Equipment Market Size

- The global Ion Implantation Equipment market size was valued at USD 7.42 billion in 2025 and is expected to reach USD 13.88 billion by 2033, at a CAGR of 8.2% during the forecast period

- The market growth is primarily driven by increasing semiconductor wafer fabrication activities, rising demand for advanced logic and memory chips, rapid adoption of AI processors, and growing investments in semiconductor manufacturing facilities globally

- In addition, increasing transition toward smaller process nodes, expansion of electric vehicle semiconductor demand, and rising need for precision doping technologies in advanced semiconductor manufacturing are positioning ion implantation equipment as a critical technology in wafer fabrication processes, thereby significantly accelerating overall market growth

Ion Implantation Equipment Market Analysis

- Ion implantation equipment, which is used to introduce dopants into semiconductor wafers with high precision and control, has become an essential component in semiconductor manufacturing due to increasing miniaturization and complexity of integrated circuits

- The escalating demand for ion implantation equipment is primarily driven by rapid growth of advanced semiconductor nodes, increasing production of AI chips, memory devices, and power semiconductors, along with rising deployment of electric vehicles, 5G infrastructure, and data centers globally

- Asia-Pacific dominated the Ion Implantation Equipment market with the largest revenue share of 48.6% in 2025, supported by strong semiconductor manufacturing ecosystems, expansion of wafer fabrication capacities, and large-scale investments in semiconductor fabrication facilities across China, Taiwan, South Korea, and Japan

- North America is expected to witness substantial CAGR of 9.1% during the forecast period due to increasing investments in domestic semiconductor manufacturing, rising government incentives for semiconductor localization, and expansion of advanced chip production facilities

- The high current implanters segment dominated the market with a market share of 39.8% in 2025, driven by their critical role in high-volume semiconductor manufacturing and advanced wafer processing applications

Report Scope and Ion Implantation Equipment Market Segmentation

|

Attributes |

Ion Implantation Equipment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Ion Implantation Equipment Market Trends

“Growing Adoption of Advanced Semiconductor Nodes and AI Chips ”

- A significant and accelerating trend in the global Ion Implantation Equipment market is the increasing adoption of advanced semiconductor nodes and AI-driven semiconductor architectures requiring ultra-precise doping and wafer processing technologies

- For instance, semiconductor manufacturers are increasingly deploying advanced ion implantation systems for FinFET, GAAFET, 3D NAND memory, and power semiconductor fabrication to improve transistor performance and device reliability

- Technological advancements in ion implantation systems, including AI-enabled process control, automated beam monitoring, and high-throughput wafer handling systems, are improving implantation precision, productivity, and operational efficiency

- The increasing transition toward 300 mm wafer processing and advanced packaging technologies is supporting demand for next-generation ion implantation equipment capable of handling complex semiconductor manufacturing requirements

- This trend toward advanced semiconductor manufacturing and precision wafer doping is reshaping industry expectations for process control, yield optimization, and device miniaturization across semiconductor fabrication facilities

- Demand for automated and energy-efficient ion implantation systems is growing rapidly across both developed and emerging semiconductor manufacturing regions due to increasing investments in advanced semiconductor fabrication expansion projects

- Increasing focus on semiconductor supply chain localization and domestic chip production initiatives is further accelerating adoption of ion implantation equipment globally .

Ion Implantation Equipment Market Dynamics

Driver

“Rising Demand for Advanced Semiconductor Manufacturing and Power Electronics ”

- The increasing demand for advanced semiconductor devices, AI processors, electric vehicle electronics, and high-performance computing chips is a major driver fueling the growth of the Ion Implantation Equipment market globally

- For instance, leading semiconductor foundries are heavily investing in advanced process nodes below 5nm, where ion implantation plays a critical role in transistor formation and wafer doping precision

- As semiconductor manufacturers focus more on improving chip density, power efficiency, and device performance, ion implantation equipment provides essential doping capabilities required for advanced integrated circuit fabrication

- Furthermore, growing adoption of electric vehicles, renewable energy systems, industrial automation, and IoT devices is increasing demand for power semiconductors globally, thereby accelerating investments in wafer fabrication technologies including ion implantation systems

- The compatibility of advanced ion implantation equipment with high-volume semiconductor manufacturing and automated fab environments is a key factor driving widespread industry adoption

- Expanding semiconductor fabrication capacity across Asia-Pacific, North America, and Europe is further supporting market expansion

- Government incentives and semiconductor manufacturing support programs are accelerating investments in advanced wafer processing technologies globally

Restraint/Challenge

“High Capital Investment and Complex Process Integration ”

- Challenges related to the high cost of ion implantation equipment and complex semiconductor process integration pose significant barriers to market expansion, particularly for smaller semiconductor manufacturers and emerging fabrication facilities

- For instance, advanced ion implantation systems require significant capital investment, cleanroom infrastructure, sophisticated beam control systems, and highly controlled manufacturing environments, increasing operational and deployment costs

- Addressing these challenges through automation, process optimization, and technological advancements is critical for improving manufacturing efficiency and reducing total cost of ownership

- While demand for advanced semiconductor manufacturing continues to rise, maintaining implantation accuracy, minimizing wafer defects, and controlling contamination remain major technical challenges in advanced semiconductor fabrication

- Overcoming these challenges through continuous innovation in beam control technologies, wafer handling systems, and process monitoring solutions will be essential for long-term market growth

- Supply chain disruptions in semiconductor equipment components and raw materials can impact production timelines and equipment availability globally

- Stringent semiconductor manufacturing standards and high precision process requirements can further increase operational complexity and compliance costs

Ion Implantation Equipment Market Scope

The market is segmented on the basis of type, wafer size, application, end user, and industry vertical. .

- By Type

On the basis of type, the global Ion Implantation Equipment market is segmented into high current implanters, medium current implanters, high energy implanters, and others. The high current implanters segment dominated the market with the largest revenue share of 39.8% in 2025, driven by their critical role in high-volume semiconductor manufacturing and advanced wafer processing applications. Increasing adoption of advanced semiconductor nodes and growing demand for memory and logic devices are supporting strong demand for high current ion implantation systems. Their ability to deliver high throughput and precise dopant control further strengthens segment dominance.

The high energy implanters segment is expected to witness the fastest growth during the forecast period, fueled by rising demand for advanced power semiconductors, automotive electronics, and high-voltage semiconductor applications.

- By Wafer Size

On the basis of wafer size, the market is segmented into 200 mm, 300 mm, and others. The 300 mm segment accounted for the largest market revenue share of 69.1% in 2025, driven by increasing adoption of 300 mm wafers in advanced semiconductor fabrication facilities due to higher production efficiency and reduced manufacturing costs per chip. Expansion of high-volume foundry operations and advanced memory chip production facilities is further supporting segment dominance.

The others segment is anticipated to register the fastest growth over the forecast period owing to increasing development of compound semiconductor technologies and specialized semiconductor applications requiring customized wafer processing solutions.

- By Application

On the basis of application, the Ion Implantation Equipment market is segmented into logic devices, memory devices, power semiconductors, MEMS, compound semiconductors, and others. The logic devices segment dominated the market with a share of 44.3% in 2025, driven by increasing global demand for AI processors, CPUs, GPUs, and advanced computing chips. Ion implantation equipment is extensively used in transistor formation and semiconductor doping processes for advanced logic chip manufacturing.

The power semiconductors segment is expected to witness the fastest growth during the forecast period, fueled by increasing adoption of electric vehicles, renewable energy systems, industrial automation, and energy-efficient power devices.

- By End User

On the basis of end user, the market is segmented into integrated device manufacturers (IDMs), foundries, OSAT companies, and research institutes. The foundries segment dominated the market in 2025 with a share of 46.2%, supported by increasing investments in large-scale semiconductor fabrication plants and rising outsourcing of chip manufacturing activities globally.

The OSAT companies segment is expected to witness the fastest growth during the forecast period due to increasing demand for advanced semiconductor packaging and testing services.

- By Industry Vertical

On the basis of industry vertical, the market is segmented into consumer electronics, automotive electronics, telecommunications, industrial electronics, healthcare electronics, and others. The consumer electronics segment dominated the market with the largest revenue share in 2025 due to increasing production of smartphones, laptops, gaming devices, and wearable electronics globally.

The automotive electronics segment is expected to witness the fastest growth during the forecast period driven by increasing semiconductor content in electric vehicles, ADAS systems, infotainment systems, and autonomous driving technologies.

Ion Implantation Equipment Market Regional Analysis

- Asia-Pacific dominated the Ion Implantation Equipment market with the largest revenue share of 48.6% in 2025, supported by strong semiconductor manufacturing ecosystems, increasing investments in foundry expansion projects, and rising adoption of advanced semiconductor fabrication technologies across China, Taiwan, South Korea, and Japan

- Manufacturers and semiconductor fabrication facilities in the region place significant emphasis on high-volume chip production, process precision, and advanced node manufacturing, leading to widespread adoption of ion implantation equipment across wafer fabrication plants

- This strong market position is further supported by increasing government initiatives promoting semiconductor self-sufficiency, expansion of AI chip manufacturing capacity, and presence of leading semiconductor manufacturers across the region

U.S. Ion Implantation Equipment Market Insight

The U.S. Ion Implantation Equipment market captured the largest revenue share within North America in 2025, driven by increasing investments in domestic semiconductor manufacturing and rising demand for AI processors, automotive chips, and advanced packaging technologies. Government support programs encouraging semiconductor production localization and expansion of advanced wafer fabrication facilities continue to support sustained market growth.

Europe Ion Implantation Equipment Market Insight

The Europe Ion Implantation Equipment market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by increasing semiconductor manufacturing investments and growing focus on reducing dependence on imported semiconductor supply chains. Rising adoption of automotive semiconductors and industrial electronics is further supporting market expansion.

Germany Ion Implantation Equipment Market Insight

The Germany Ion Implantation Equipment market is expected to expand at a considerable CAGR during the forecast period, driven by strong industrial automation capabilities, automotive semiconductor demand, and increasing investments in semiconductor R&D and advanced manufacturing technologies.

Asia-Pacific Ion Implantation Equipment Market Insight

The Asia-Pacific Ion Implantation Equipment market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid expansion of semiconductor fabrication plants, increasing production of AI and memory chips, and strong government support for semiconductor manufacturing initiatives.

Japan Ion Implantation Equipment Market Insight

The Japan Ion Implantation Equipment market is gaining momentum due to increasing investments in advanced semiconductor equipment technologies and strong presence of major semiconductor equipment manufacturers. The country’s focus on precision engineering and advanced wafer processing technologies continues to fuel market growth.

India Ion Implantation Equipment Market Insight

The India Ion Implantation Equipment market accounted for a significant revenue share in Asia-Pacific in 2025, attributed to increasing semiconductor manufacturing initiatives, expansion of electronics manufacturing activities, and government support for domestic semiconductor ecosystem development. Rising investments in chip fabrication and packaging facilities are further supporting long-term market growth in the country.

Ion Implantation Equipment Market Share

The Ion Implantation Equipment industry is primarily led by well-established companies, including:

- Applied Materials, Inc. (U.S.)

- Axcelis Technologies, Inc. (U.S.)

- Nissin Ion Equipment Co., Ltd. (Japan)

- ULVAC, Inc. (Japan)

- Sumitomo Heavy Industries Ion Technology Co., Ltd. (Japan)

- Tokyo Electron Limited (Japan)

- Canon Anelva Corporation (Japan)

- Lam Research Corporation (U.S.)

- Hitachi High-Tech Corporation (Japan)

- Plasma-Therm LLC (U.S.)

- Veeco Instruments Inc. (U.S.)

- Ion Beam Services (France)

- SCREEN Holdings Co., Ltd. (Japan)

What are the Recent Developments in Global Ion Implantation Equipment Market?

- In December 2025, Axcelis Technologies, Inc. introduced advanced ion implantation systems optimized for AI processor and advanced logic semiconductor manufacturing applications, focusing on improved implantation precision and productivity

- In October 2025, Applied Materials, Inc. expanded its semiconductor process equipment portfolio with enhanced ion implantation solutions designed for advanced memory and power semiconductor applications

- In August 2025, Nissin Ion Equipment Co., Ltd. announced advanced high-energy ion implantation technologies aimed at improving process control and wafer uniformity in advanced semiconductor fabrication

- In June 2025, ULVAC, Inc. strengthened its semiconductor equipment portfolio through development of automated ion implantation systems optimized for next-generation semiconductor manufacturing environments

- In March 2024, Sumitomo Heavy Industries Ion Technology Co., Ltd. introduced advanced implantation process technologies focused on improving defect reduction, beam stability, and operational efficiency in semiconductor fabrication facilities

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ion Implantation Equipment Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ion Implantation Equipment Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ion Implantation Equipment Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.