Global Ionomers Market

Market Size in USD Billion

USD

2.46 Billion

USD

3.96 Billion

2025

2033

USD

2.46 Billion

USD

3.96 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.46 Billion | |

| USD 3.96 Billion | |

| % | |

|

Ionomers Market Size

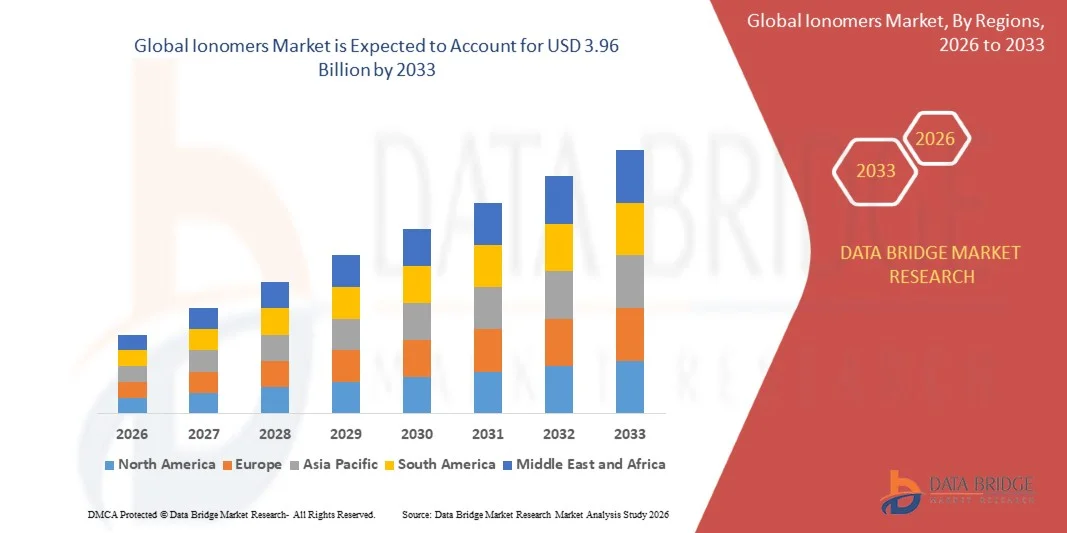

- The global ionomers market size was valued at USD 2.46 billion in 2025and is expected to reach USD 3.96 billion by 2033, at a CAGR of 6.14% during the forecast period

- The market growth is primarily driven by increasing demand for high-performance polymers across packaging, automotive, and industrial applications, supported by the rising shift toward lightweight, durable, and chemically resistant materials

- Furthermore, growing adoption of ionomers in sustainable packaging solutions, fuel cell membranes, and advanced adhesive systems is strengthening market expansion. These factors are collectively accelerating the use of ionomer-based materials across multiple end-use industries, thereby significantly supporting overall market growth

Ionomers Market Analysis

- Ionomers, a class of ionically modified polymers with enhanced toughness, transparency, and chemical resistance, are increasingly important in advanced material applications across packaging, automotive, adhesives, and energy systems due to their superior mechanical performance and versatility

- The rising demand for ionomers is primarily driven by their growing use in lightweight automotive components, high-performance packaging films, and sustainable adhesive solutions, along with increasing adoption in fuel cell and energy storage technologies

- North America dominated the ionomers market with the largest revenue share of 38.7% in 2025, supported by strong demand from packaging and automotive industries, advanced material R&D capabilities, and the presence of major chemical manufacturers, with the U.S. witnessing significant uptake in fuel cell and specialty polymer applications

- Asia-Pacific is expected to be the fastest growing region in the ionomers market during the forecast period due to rapid industrialization, expansion of packaging and electronics manufacturing, and increasing investments in automotive production and clean energy technologies

- Ethylene-Methacrylic Acid ionomers segment dominated the ionomers market with a market share of 41.5% in 2025, driven by its extensive use in food packaging, heat-sealable films, and impact-resistant applications across multiple end-use industries

Report Scope and Ionomers Market Segmentation

|

Attributes |

Ionomers Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expanding adoption of PFSA ionomers in hydrogen fuel cells and electrolyzers · Growing shift toward recyclable, mono-material packaging solutions |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework |

Ionomers Market Trends

“Rising Adoption of High-Performance and Sustainable Polymer Solutions”

- A key and accelerating trend in the global ionomers market is the increasing integration of these materials in high-performance applications such as sustainable packaging, automotive lightweight components, and advanced adhesive systems due to their excellent toughness, transparency, and chemical resistance

- For instance, ionomer resins are widely used in multilayer food packaging films where they provide strong heat sealability and superior barrier protection for perishable goods

- Growing use of ionomers in fuel cell membranes and hydrogen energy systems is also emerging as a major trend, driven by global clean energy transition initiatives and demand for high-efficiency ion-conducting materials

- Furthermore, advancements in polymer modification technologies are enabling improved ionomer grades with enhanced flexibility, impact resistance, and processability, expanding their use in industrial and consumer applications

- Increasing adoption of ionomers in premium sports goods such as golf ball covers and protective gear is further expanding their footprint in high-value consumer applications requiring durability and elasticity

- This trend toward sustainable, high-performance, and multifunctional polymer materials is reshaping material selection strategies across end-use industries, increasing reliance on ionomer-based solutions

- The demand for ionomers with improved recyclability and environmental compatibility is growing rapidly across packaging and automotive sectors as industries move toward circular economy goals

Ionomers Market Dynamics

Driver

“Rising Demand from Packaging, Automotive, and Energy Applications”

- The increasing demand for lightweight, durable, and chemically resistant materials across packaging, automotive, and energy industries is a major driver for the global ionomers market growth

- For instance, ionomers are extensively used in automotive interior trims, protective films, and impact-resistant components due to their superior mechanical strength and flexibility

- Growing consumption of ionomers in food packaging applications, particularly for heat-sealable films and barrier layers, is further strengthening market demand globally

- Furthermore, rising investments in hydrogen fuel cell technology and energy storage systems are accelerating the adoption of PFSA-based ionomers for membrane applications

- The shift toward sustainable materials and high-performance polymers in manufacturing processes is further boosting the use of ionomers across multiple industrial sectors

- Increasing demand for advanced adhesive and coating solutions in electronics and construction industries is also contributing significantly to market expansion

- Expansion of electric vehicle production is In addition driving demand for ionomers in battery-related components and lightweight protective materials

- Rapid industrialization in emerging economies is further accelerating consumption of ionomer-based materials across packaging and manufacturing sectors

Restraint/Challenge

“High Cost and Limited Raw Material Availability Constraints”

- A major challenge restraining the global ionomers market is the relatively high production cost associated with specialized raw materials and complex polymer modification processes

- For instance, PFSA-based ionomers used in fuel cells require expensive fluorinated feedstocks, making them significantly costlier than conventional polymers

- Limited availability of raw materials and dependence on specific chemical supply chains also create supply volatility, impacting large-scale production scalability

- Furthermore, performance-sensitive applications often require precise processing conditions, which increases manufacturing complexity and operational costs for end users

- Competition from lower-cost alternative polymers such as polyethylene and EVA further limits adoption in price-sensitive markets and applications

- Stringent environmental regulations on fluoropolymer production in certain regions also add compliance burden and restrict manufacturing flexibility

- Addressing these challenges through cost optimization, raw material diversification, and scalable production technologies will be crucial for sustained market growth

Ionomers Market Scope

The market is segmented on the basis of type, ion type, application, and end use.

- By Type

On the basis of type, the ionomers market is segmented into Ethylene-Methacrylic Acid (E/MAA) ionomers, Ethylene-Acrylic Acid (E/AA) ionomers, Ethylene Methyl Acrylate (EMA) ionomers, Perfluorosulfonic Acid (PFSA) ionomers, Polyolefin-based ionomers, Specialty ionomers, and Others. The Ethylene-Methacrylic Acid (E/MAA) ionomers segment dominated the market with the largest revenue share of 41.5% in 2025, driven by its strong demand in packaging films, heat-sealable layers, and food-contact applications. E/MAA ionomers offer excellent clarity, toughness, and chemical resistance, making them highly suitable for multilayer packaging structures. Their widespread availability and cost-effectiveness further strengthen their dominance across global packaging and consumer goods industries. Increasing use in flexible packaging for processed food and pharmaceutical protection also supports sustained market leadership. In addition, their compatibility with extrusion and lamination processes enhances industrial adoption across large-scale manufacturing setups.

The Perfluorosulfonic Acid (PFSA) ionomers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising adoption in fuel cells, hydrogen energy systems, and electrochemical applications. PFSA ionomers are critical components in proton exchange membranes, offering high ionic conductivity and thermal stability. Increasing global investments in hydrogen infrastructure and clean energy transition projects are significantly boosting demand for PFSA materials. For instance, fuel cell electric vehicles and green hydrogen production systems are expanding rapidly, directly supporting PFSA ionomer consumption. Technological advancements in membrane efficiency and durability are further enhancing their commercial viability. Growing emphasis on decarbonization across industrial sectors is expected to accelerate PFSA ionomer adoption globally.

- By Ion Type

On the basis of ion type, the ionomers market is segmented into sodium ionomers, zinc ionomers, lithium ionomers, magnesium ionomers, and others. The Sodium ionomers segment dominated the market with the largest revenue share in 2025, owing to their cost efficiency, wide availability, and strong performance in packaging and adhesive applications. Sodium ionomers provide balanced mechanical strength and flexibility, making them suitable for large-scale industrial use. Their extensive adoption in food packaging films and heat-sealing applications significantly contributes to their market dominance. In addition, ease of processing and compatibility with conventional polymer systems enhances their commercial preference. The segment also benefits from strong demand in consumer goods packaging where cost optimization is critical.

The Lithium ionomers segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand from energy storage systems and advanced electrochemical applications. Lithium ionomers are gaining traction due to their superior ionic conductivity and stability, making them suitable for next-generation battery and fuel cell technologies. Rapid expansion of electric vehicle production and battery innovation is significantly supporting segment growth. For instance, lithium-based materials are increasingly used in high-performance separators and membrane technologies. Rising investments in solid-state batteries and clean energy systems are further accelerating adoption. Continuous R&D in high-energy-density storage solutions is expected to strengthen lithium ionomer demand globally.

- By Application

On the basis of application, the ionomers market is segmented into packaging, automotive, adhesives & sealants, coatings, footwear, sports equipment, medical & healthcare, construction, and wire & cable insulation. The Packaging segment dominated the market with the largest revenue share in 2025, driven by increasing demand for high-barrier, heat-sealable, and durable packaging materials. Ionomers are widely used in food packaging films due to their excellent sealing strength and resistance to puncture and contamination. Growth in processed food consumption and pharmaceutical packaging requirements further supports segment dominance. Their ability to enhance shelf life and product safety makes them highly preferred in flexible packaging applications. In addition, rising demand for sustainable and recyclable packaging materials strengthens their usage across global supply chains.

The Automotive segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of lightweight and impact-resistant materials in vehicle manufacturing. Ionomers are used in interior trims, protective coatings, and structural components due to their durability and flexibility. Growing electric vehicle production is further boosting demand for advanced polymer materials with high performance-to-weight ratios. For instance, ionomers help improve fuel efficiency and reduce vehicle emissions through lightweight design integration. Increasing focus on vehicle safety and noise reduction is also supporting segment expansion. Continuous innovation in automotive material engineering is expected to accelerate ionomer adoption significantly.

- By End Use

On the basis of end use, the ionomers market is segmented into packaging industry, automotive industry, construction, electrical & electronics, healthcare & medical, consumer goods, sports & recreation, and industrial manufacturing. The Packaging Industry segment dominated the market with the largest revenue share in 2025, driven by strong demand for flexible, protective, and high-performance packaging solutions. Ionomers are widely used in food, beverage, and pharmaceutical packaging due to their sealing strength and barrier properties. The rapid expansion of e-commerce and global food distribution networks further strengthens segment dominance. Their role in improving product safety and extending shelf life makes them essential in modern packaging systems. In addition, growing emphasis on sustainable packaging solutions supports continued market leadership.

The Electrical & Electronics segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing use of ionomers in wire insulation, electronic coatings, and advanced device components. Ionomers offer excellent dielectric strength and thermal stability, making them suitable for high-performance electronic applications. Rising demand for consumer electronics and miniaturized devices is further accelerating material adoption. For instance, ionomer-based materials are increasingly used in protective layers for sensitive electronic components. Expansion of 5G infrastructure and smart devices is also contributing to segment growth. Continuous advancements in electronic material engineering are expected to significantly boost ionomer usage in this sector.

Ionomers Market Regional Analysis

- North America dominated the ionomers market with the largest revenue share of 38.7% in 2025, supported by strong demand from packaging and automotive industries, advanced material R&D capabilities, and the presence of major chemical manufacturers

- The region benefits from high adoption of high-performance polymers in food packaging, automotive lightweight components, and fuel cell technologies, supporting consistent demand for ionomer materials

- Consumers and industries in North America increasingly prioritize advanced material properties such as durability, chemical resistance, and sustainability, which further strengthens ionomer adoption across end-use sectors

U.S. Ionomers Market Insight

The U.S. ionomers market captured the largest revenue share within North America in 2025, fueled by strong demand from packaging, automotive, and advanced materials industries. The country benefits from a highly developed chemical manufacturing base and rapid adoption of high-performance polymers across industrial applications. Consumers and manufacturers increasingly prioritize lightweight, durable, and chemically resistant materials, driving ionomer usage in multiple sectors. Moreover, rising applications in food packaging films, automotive lightweight components, and fuel cell technologies are significantly contributing to market expansion. The presence of leading polymer producers and strong R&D capabilities is further accelerating innovation and commercialization of advanced ionomer grades.

Europe Ionomers Market Insight

The Europe ionomers market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent environmental regulations and increasing demand for sustainable polymer solutions. The region is witnessing growing adoption of ionomers in packaging applications as industries shift toward recyclable and high-performance materials. Europe also benefits from strong integration of ionomers in automotive lightweighting, adhesives, and coating applications across industrial sectors. In addition, rising emphasis on circular economy practices and reduced carbon emissions is supporting steady market growth. Expanding use in food packaging and industrial applications further strengthens regional demand.

U.K. Ionomers Market Insight

The U.K. ionomers market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for advanced packaging materials and high-performance adhesive solutions. Rising environmental concerns and regulatory pressure to reduce plastic waste are encouraging adoption of recyclable ionomer-based materials. The growing use of ionomers in automotive, construction, and consumer goods sectors is further supporting market expansion. In addition, advancements in sustainable packaging technologies are strengthening demand across food and retail industries. The country’s focus on innovation and material efficiency continues to drive steady market growth.

Germany Ionomers Market Insight

The Germany ionomers market is expected to expand at a considerable CAGR during the forecast period, fueled by strong automotive manufacturing and industrial polymer demand. The country’s leadership in engineering and material innovation is driving adoption of ionomers in lightweight automotive components and high-durability applications. Increasing focus on sustainability and energy efficiency is further boosting their use in packaging and industrial sectors. Germany also shows strong integration of ionomers in advanced adhesive and coating technologies. The emphasis on eco-friendly and high-performance materials continues to support sustained market expansion.

Asia-Pacific Ionomers Market Insight

The Asia-Pacific ionomers market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid industrialization, urbanization, and expanding manufacturing activities. Rising demand for packaged food, consumer goods, and automotive products across emerging economies is significantly boosting ionomer consumption. Furthermore, strong investments in electric vehicles, renewable energy, and industrial infrastructure are accelerating regional growth. The region also benefits from expanding production capabilities and cost-efficient manufacturing ecosystems. Increasing adoption of advanced packaging and polymer solutions is further strengthening market momentum.

Japan Ionomers Market Insight

The Japan ionomers market is gaining momentum due to strong demand from automotive, electronics, and high-performance packaging industries. The country’s advanced manufacturing ecosystem supports adoption of ionomers in precision applications and specialty materials. Increasing focus on lightweight, durable, and technologically advanced materials is driving usage in automotive and industrial sectors. Integration of ionomers in electronics and coating applications is further enhancing market growth. In addition, Japan’s emphasis on innovation and strict quality standards continues to support steady market expansion.

India Ionomers Market Insight

The India ionomers market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, expanding middle-class population, and strong growth in packaging demand. Increasing adoption of flexible packaging, automotive components, and construction materials is significantly driving market growth. The country’s growing manufacturing base and rising consumer goods consumption are further supporting ionomer demand. In addition, government initiatives promoting industrial development and smart manufacturing are accelerating market expansion. Availability of cost-effective materials and strong domestic production capabilities continue to strengthen India’s position in the region.

Ionomers Market Share

The Ionomers industry is primarily led by well-established companies, including:

- DuPont de Nemours, Inc. (U.S.)

- The Chemours Company LLC (U.S.)

- Dow Inc. (U.S.)

- Syensqo SA/NV (Belgium)

- AGC Inc. (Japan)

- 3M (U.S.)

- Solvay SA (Belgium)

- Arkema S.A. (France)

- Asahi Kasei Corporation (Japan)

- LG Chem Ltd. (South Korea)

- Exxon Mobil Corporation (U.S.)

- BASF SE (Germany)

- Celanese Corporation (U.S.)

- SABIC (Saudi Arabia)

- Mitsui Chemicals, Inc. (Japan)

- Toray Industries, Inc. (Japan)

- Sumitomo Chemical Co., Ltd. (Japan)

- Evonik Industries AG (Germany)

- LyondellBasell Industries N.V. (Netherlands)

- Daikin Industries, Ltd. (Japan)

What are the Recent Developments in Global Ionomers Market?

- In February 2026, Chemours partnered with 2CRSi to advance two-phase liquid cooling technologies, leveraging high-performance fluoropolymer materials derived from its advanced chemistry portfolio. The collaboration focuses on improving thermal management in high-density computing systems, indirectly expanding ionomer-related fluoropolymer applications

- In March 2025, W. L. Gore & Associates expanded collaboration with automotive manufacturers to optimize GORE-SELECT® PFSA ionomer membranes for heavy-duty fuel cell stacks. The focus is on improving durability, efficiency, and cost competitiveness of hydrogen-powered vehicles. These reinforced ionomer systems are increasingly used in next-generation fuel cell electric vehicles (FCEVs)

- In February 2025, DuPont highlighted its latest Nafion™ PFSA ionomer membranes and dispersions at the International Hydrogen & Fuel Cell Expo in Tokyo. The company emphasized improved durability and conductivity of its ionomer technology for use in PEM electrolyzers and fuel cells, supporting the global hydrogen economy expansion. This development reinforces Nafion’s position as a key material in energy transition applications

- In December 2024, researchers at Imperial College London developed a new ion-exchange membrane for redox flow batteries, improving energy efficiency and reducing crossover losses. The development highlights growing innovation in ionomer-like polymer membranes for large-scale energy storage applications beyond fuel cells

- In November 2024, Syensqo announced the launch of Aquivion® N+ 125D, a next-generation fluoro-ionomer based on its non-fluorosurfactant (NFS) technology. The product is designed for hydrogen-related applications, particularly in fuel cells and green hydrogen systems. This innovation is part of Syensqo’s sustainability roadmap aimed at reducing PFAS-related environmental impact while improving ionomer performance for electrochemical applications

- In October 2023, Dow announced expansion of its Surlyn™ ionomer resin applications in luxury and cosmetic packaging, introducing circular and bio-based grades made from recycled plastic waste and bio-feedstocks. These new ionomer materials are being used in premium perfume and cosmetics packaging in collaboration with global luxury brands, supporting sustainability and circular economy goals while maintaining high clarity, toughness, and sealing performance

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Ionomers Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Ionomers Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Ionomers Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.