Global Keratolytic Agents Market

Market Size in USD Billion

USD

1.16 Billion

USD

1.82 Billion

2025

2033

USD

1.16 Billion

USD

1.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.16 Billion | |

| USD 1.82 Billion | |

| % | |

|

Keratolytic Agents Market Size

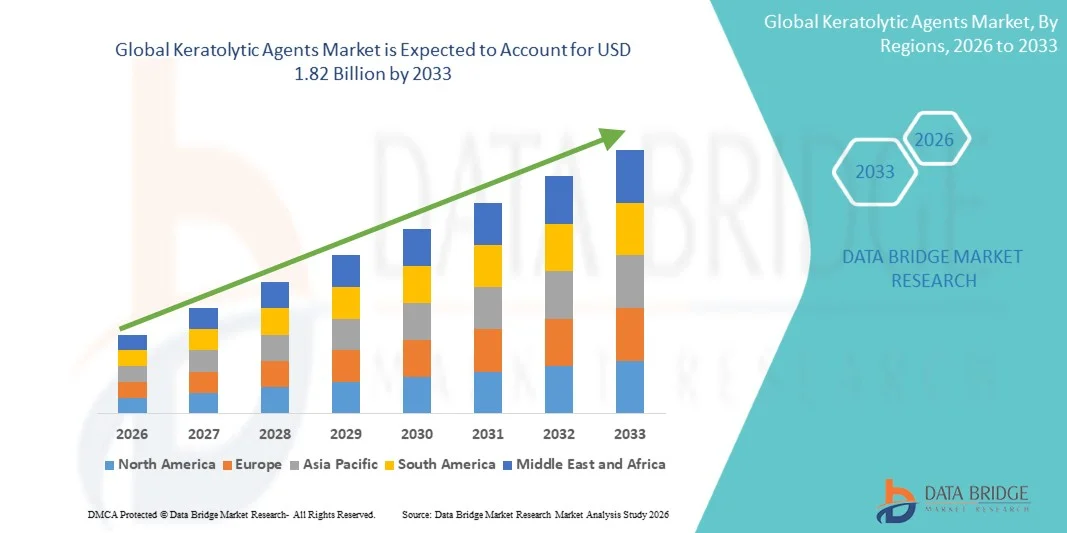

- The global keratolytic agents market size was valued at USD 1.16 billion in 2025 and is expected to reach USD 1.82 billion by 2033, at a CAGR of 5.80% during the forecast period

- The market growth of keratolytic agents is primarily driven by increasing awareness and demand for effective skin care treatments that address conditions such as acne, psoriasis, and hyperkeratosis. Technological advancements in formulation and delivery methods are further enhancing product efficacy, leading to wider adoption among consumers

- In addition, the rising preference for safe, easy-to-use, and clinically proven dermatological solutions is positioning keratolytic agents as a key component in modern skin care regimens. These factors are collectively accelerating market uptake, thereby significantly boosting growth prospects in the keratolytic agents industry

Keratolytic Agents Market Analysis

- Keratolytic agents, which help exfoliate the skin and treat conditions such as acne, hyperkeratosis, and psoriasis, are gaining prominence as essential components in modern dermatological care due to their proven efficacy, ease of use, and incorporation into a broad range of skincare formulations

- The rising demand for keratolytic agents is driven by increasing consumer awareness of skin health, heightened demand for effective OTC and prescription skin treatments, and an expanding portfolio of advanced formulations that improve skin tolerance and outcomes. These factors are significantly boosting product adoption across both consumer and clinical segments

- North America dominated the keratolytic agents market, accounting for approximately 38.7% of total revenue in 2025, supported by strong healthcare infrastructure, high consumer spending on skincare products, and extensive presence of leading dermatological brands. The U.S. represents a major share within the region, fuelled by strong demand for innovative topical solutions and growing dermatologist recommendations

- Asia‑Pacific is projected to be the fastest‑growing region in the keratolytic Agents market over the forecast period, with an estimated CAGR from 2026 to 2033. Growth in this region is attributed to rising urbanization, increasing disposable incomes, expanding beauty and personal care markets, and growing access to professional dermatology services

- The topical segment dominated the largest market revenue share of 92% in 2025, due to localized efficacy, convenience, high patient compliance, and compatibility across hospitals, homecare, and specialty centres

Report Scope and Keratolytic Agents Market Segmentation

|

Attributes |

Keratolytic Agents Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Galderma (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Keratolytic Agents Market Trends

“Rising Adoption of Combination Formulations and Targeted Therapies”

- There is a growing trend toward developing combination keratolytic formulations that pair active agents like salicylic acid, urea, or alpha-hydroxy acids with other therapeutics to improve efficacy and minimize side effects

- For instance, in 2024, a leading dermatology brand launched a salicylic acid + urea cream targeting severe psoriasis, providing both exfoliation and hydration, which improved patient adherence and skin tolerance

- Advances in delivery systems such as gels, foams, and transdermal patches are enabling more targeted application and consistent dosing, enhancing treatment outcomes

- Natural and plant-based keratolytic agents, such as glycolic acid from sugarcane or lactic acid from milk, are increasingly incorporated into cosmetic and dermatological products due to rising consumer demand for “clean-label” skincare solutions

- Multi-functional topical treatments that address both therapeutic and cosmetic needs (e.g., exfoliation, moisturization, and anti-inflammatory effects) are shaping the market, creating differentiated products that appeal to both healthcare providers and consumers

Keratolytic Agents Market Dynamics

Driver

“Growing Prevalence of Skin Disorders and Rising Awareness of Treatment Options”

- The increasing global prevalence of skin conditions such as psoriasis, acne, keratosis pilaris, calluses, and hyperkeratosis is a primary driver of market growth. As more individuals seek effective treatments, keratolytic agents have become essential in both clinical and cosmetic applications

- For example, in 2025, Onyx Pharmaceuticals reported a significant increase in prescriptions for urea-based keratolytic creams among diabetic patients suffering from hyperkeratosis. This indicates that medical professionals are actively recommending these treatments, reflecting growing confidence in their therapeutic efficacy

- Rising awareness among consumers regarding effective skincare treatments, partly driven by dermatology-focused social media platforms, online consultations, and health education campaigns, is encouraging proactive management of skin disorders. Patients are now more informed and willing to invest in scientifically proven topical therapies

- The expansion of dermatology clinics, pharmacy networks, and retail access in emerging markets such as India, Brazil, and Southeast Asia is increasing product penetration. Wider availability ensures that more patients can access both over-the-counter and prescription-strength keratolytic products

- The cosmetic segment is also driving demand, as consumers increasingly seek exfoliating agents for smoother, brighter, and healthier-looking skin. This dual demand for therapeutic and cosmetic benefits expands the target consumer base and encourages manufacturers to offer versatile products

- The rise of self-care and home-based skincare regimens, accelerated by the COVID-19 pandemic and increasing telemedicine adoption, has further contributed to the demand for easy-to-use, safe, and effective keratolytic treatments

Restraint/Challenge

“Skin Irritation Concerns and Regulatory Hurdles”

- Despite their effectiveness, keratolytic agents may cause side effects such as redness, peeling, excessive dryness, or mild burning sensations, especially when used in higher concentrations or over long periods. These adverse effects can limit patient compliance and slow adoption.

- For instance, some high-concentration salicylic acid formulations released in 2023 were recalled or reformulated due to reports of skin irritation in sensitive individuals. This example highlights the need for careful dosing, precise formulation, and robust clinical testing to ensure safety.

- Regulatory compliance challenges are also significant. Each country has its own requirements for approval of keratolytic agents, particularly for combination therapies or higher-strength products. These regulatory variations can delay market entry, increase development costs, and limit global distribution.

- Price sensitivity poses another barrier. Prescription-strength keratolytic creams and advanced formulations often come at a premium, which can deter cost-conscious consumers, especially in developing markets or among individuals who may prefer over-the-counter alternatives.

- Consumer skepticism regarding the long-term safety of chemical keratolytic agents may further restrict adoption, especially when combined with limited knowledge of proper application and dosage. Education campaigns and dermatologist guidance are critical to addressing these concerns.

- To overcome these challenges, companies must invest in comprehensive clinical research, effective patient education, and innovative formulations that balance efficacy, safety, and affordability, ensuring both regulatory compliance and sustained market growth.

Keratolytic Agents Market Scope

The market is segmented on the basis of indication, dosage form, agents, route of administration, end-users, and distribution channel.

• By Indication

On the basis of indication, the Keratolytic Agents market is segmented into psoriasis, dry skin, acne vulgaris, warts, dandruff, and others. The psoriasis segment dominated the largest market revenue share of 38.5% in 2025, driven by the chronic nature of the disease, increasing prevalence, frequent prescriptions in hospitals and specialty centres, and strong patient compliance. Awareness programs, government initiatives, and physician trust reinforce dominance. Topical treatment ease, combination therapies, and multiple dosage forms support adoption. Hospitals, homecare, and specialty centres widely stock psoriasis formulations. Brand recognition and proven efficacy further strengthen the market. Continuous R&D ensures product relevance. Emerging markets are witnessing growth due to increased access and awareness. Patient adherence is high. Dermatologists favor psoriasis agents. Availability across OTC and prescription channels enhances penetration.

The acne vulgaris segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, fueled by rising skincare awareness, OTC adoption, and growing self-treatment trends among adolescents and adults. E-commerce penetration and online pharmacy availability accelerate adoption. Formulation innovations and digital marketing campaigns support faster uptake. Hospitals and specialty centres are integrating newer therapies. Patient preference for non-greasy and effective products drives growth. Emerging markets show strong uptake. Combination therapies enhance treatment efficacy. Physician recommendation reinforces adoption. Consumer trust and accessibility sustain growth. Awareness campaigns boost patient compliance. Lifestyle and cosmetic trends further accelerate demand.

• By Dosage Form

On the basis of dosage form, the Keratolytic Agents market is segmented into creams, lotions, gels, shampoos, face wash, solutions, and others. The creams segment dominated the largest market revenue share of 34.2% in 2025, due to versatility, ease of application, and high compliance across hospitals, homecare, and specialty centres. Multiple dosage forms and combination therapy compatibility support widespread use. Physician trust, brand recognition, and patient familiarity reinforce dominance. OTC availability enhances adoption. Hospitals and homecare providers widely stock creams. Topical application ensures localized efficacy with minimal systemic effects. Marketing initiatives increase visibility. Consumer trust improves adoption. Regulatory approvals strengthen market confidence. Emerging markets show rising demand. Continuous R&D supports sustained relevance.

The gels segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by non-greasy texture, targeted application, younger consumer preference, and rising e-commerce penetration. Hospitals and specialty centres are increasingly adopting gels. Formulation innovations improve absorption and efficacy. Digital marketing campaigns boost awareness. Consumer convenience and lifestyle trends accelerate uptake. OTC availability enhances accessibility. Combination therapies support product adoption. Emerging markets are witnessing strong growth. Physician recommendations further drive usage. Product diversification sustains interest. Social media influence reinforces adoption.

• By Agents

On the basis of agents, the market is segmented into urea, salicylic acid, lactic acid, alpha hydroxy acids, propylene glycol, and others. The salicylic acid segment dominated the largest market revenue share of 28.6% in 2025, driven by effectiveness in psoriasis, acne, and dandruff treatment, widespread availability, and high patient adherence. Hospitals, homecare, and specialty centres widely use salicylic acid formulations. Brand recognition, physician trust, and proven efficacy reinforce dominance. Topical ease of application and combination therapy compatibility further support adoption. Regulatory approvals enhance confidence. Marketing and awareness campaigns improve visibility. Patient adherence remains high. Emerging markets show growing uptake. Product innovation sustains market relevance. Continuous R&D supports long-term leadership.

The urea segment is expected to witness the fastest CAGR of 9.5% from 2026 to 2033, fueled by increasing adoption for dry skin care, homecare penetration, OTC availability, and growing awareness. Hospitals and specialty centres are expanding use. E-commerce and online pharmacy availability support faster uptake. Formulation innovations improve usability. Physician recommendations reinforce adoption. Combination therapies enhance efficacy. Emerging markets show strong growth. Patient preference for effective moisturizing agents accelerates adoption. Digital marketing campaigns boost awareness. Lifestyle trends support rapid uptake.

• By Route of Administration

On the basis of route of administration, the market is segmented into topical and others. The topical segment dominated the largest market revenue share of 92% in 2025, due to localized efficacy, convenience, high patient compliance, and compatibility across hospitals, homecare, and specialty centres. Topical ease of application, multiple dosage form options, and combination therapy use reinforce adoption. Physician trust and brand recognition strengthen market dominance. Emerging markets contribute to growth. OTC availability ensures widespread access. Marketing campaigns improve visibility. Patient familiarity supports sustained adoption. Continuous R&D ensures relevance. Hospital and homecare stocking improve distribution. Regulatory approvals increase confidence. Awareness programs further reinforce usage.

The others segment is expected to witness the fastest CAGR of 6.5% from 2026 to 2033, driven by alternative delivery methods, combination therapy innovations, and expanding clinical adoption. Hospitals and specialty centres are adopting novel routes. Digital availability and e-commerce support faster uptake. Patient education enhances acceptance. Emerging markets show rapid adoption. Physician recommendations reinforce usage. Convenience and accessibility sustain growth. Topical continues stable growth while novel routes grow faster. Clinical studies improve adoption. Combination therapies enhance outcomes.

• By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty centres, and others. Hospitals accounted for the largest market revenue share of 41% in 2025, driven by prescription-based usage, institutional demand, and consistent patient flow. Hospitals provide treatment continuity, specialty centres offer targeted care, and homecare enables self-treatment. Physician trust, brand recognition, and awareness programs reinforce dominance. OTC availability and online penetration support institutional and patient adoption. Marketing campaigns improve visibility. Emerging markets contribute to hospital-driven growth. Patient adherence remains high. Combination therapies strengthen outcomes. Continuous R&D ensures treatment effectiveness. Insurance coverage supports accessibility.

The homecare segment is expected to witness the fastest CAGR of 11.0% from 2026 to 2033, fueled by self-treatment trends, e-commerce availability, OTC adoption, and convenience. Specialty centres and hospitals show stable growth. Digital marketing and patient awareness accelerate uptake. Physician recommendations reinforce adoption. Emerging markets show rapid growth. Combination therapies enhance product usage. Product diversification sustains interest. Consumer trust strengthens adoption. Accessibility and convenience drive faster uptake.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. Retail pharmacies held the largest market revenue share of 45% in 2025, due to accessibility, convenience, and widespread OTC availability. Hospitals and specialty centres cater to prescription demand. Marketing campaigns, physician trust, and brand recognition reinforce retail dominance. Product visibility ensures adoption. Consumer familiarity and loyalty support sustained usage. Emerging markets contribute to growth. Awareness initiatives boost adoption. Digital marketing improves reach. Regulatory approvals support confidence.

The online pharmacy segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, driven by e-commerce penetration, doorstep delivery, digital marketing, and convenience. Retail and hospital pharmacies show steady growth. Consumer awareness, smartphone adoption, and online consultations accelerate adoption. Emerging markets show strong uptake. Convenience and accessibility sustain faster growth. Marketing campaigns strengthen visibility. Increasing trust in online purchases further drives adoption. Expansion of digital healthcare platforms supports long-term growth.

Keratolytic Agents Market Regional Analysis

- North America dominated the keratolytic agents market with the largest revenue share of 38.7% in 2025, supported by strong healthcare infrastructure, high consumer spending on skincare products, and the extensive presence of leading dermatological brands

- The U.S. represents a major share within the region, fueled by strong demand for innovative topical solutions and growing dermatologist recommendations for conditions such as psoriasis, acne, and hyperkeratosis. Consumers are increasingly prioritizing clinically effective keratolytic treatments for both therapeutic and cosmetic applications

- The widespread adoption is further supported by high disposable incomes, a technologically aware population, and increasing awareness of preventive dermatology practices. Robust R&D investments and established pharmaceutical distribution networks continue to drive product availability, innovation, and market growth in the region

U.S. Keratolytic Agents Market Insight

The U.S. keratolytic agents market captured the largest revenue share in 2025 within North America, driven by strong demand for advanced topical solutions and increasing dermatologist recommendations. Prescription and over-the-counter urea- and salicylic acid-based formulations have seen significant adoption in dermatology clinics and retail channels, reflecting rising consumer confidence in their effectiveness for both therapeutic and cosmetic purposes. Consumers are increasingly seeking high-quality keratolytic products that provide dual benefits for clinical care and skin appearance improvement, further propelling market growth.

Europe Keratolytic Agents Market Insight

The Europe keratolytic agents market is projected to expand at a substantial CAGR during the forecast period, driven by the rising prevalence of skin disorders and growing awareness of clinically effective treatments. Dermatology clinics in countries such as Germany and France have been actively recommending combination keratolytic therapies for psoriasis and keratosis pilaris, leading to higher adoption rates. Urbanization, rising disposable incomes, and a growing focus on preventive dermatology are encouraging the use of quality keratolytic formulations. Growth is observed across residential, professional dermatology, and cosmetic sectors, reflecting strong multi-segment demand. In addition, the increasing preference for plant-derived keratolytic agents is shaping product development and market expansion.

U.K. Keratolytic Agents Market Insight

The U.K. keratolytic agents market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by increasing consumer awareness of skin health and preventive dermatology practices. Pharmacy chains and retail outlets in cities such as London and Manchester have reported rising sales of salicylic acid- and urea-based creams for both therapeutic and cosmetic purposes. Concerns regarding chronic skin conditions like acne, psoriasis, and keratosis pilaris are motivating consumers to adopt clinically validated keratolytic agents. The U.K.’s robust retail and e-commerce infrastructure ensures widespread availability of both OTC and prescription-grade products, further stimulating market growth.

Germany Keratolytic Agents Market Insight

The Germany keratolytic agents market is expected to expand at a considerable CAGR during the forecast period, fueled by growing awareness of dermatological health and preventive skincare. Dermatology centers in major cities recommend urea- and salicylic acid-based creams for chronic hyperkeratotic conditions, reflecting confidence in their therapeutic effectiveness. Germany’s strong healthcare system and regulatory standards ensure access to safe, clinically tested keratolytic products, while the increasing interest in eco-conscious and plant-based formulations is shaping product development. Adoption is strong across both residential and professional skincare applications, including dermatology clinics and spas.

Asia-Pacific Keratolytic Agents Market Insight

The Asia-Pacific keratolytic agents market is projected to grow at the fastest CAGR from 2026 to 2033, driven by rising urbanization, increasing disposable incomes, and growth of the beauty and personal care sector. In China, Japan, and India, the expanding middle-class population is increasingly investing in professional dermatology services and clinically validated keratolytic treatments for therapeutic and cosmetic use. Expanding access to skincare products, increasing awareness of preventive dermatology, and technological advancements in formulations are enabling broader adoption across urban and semi-urban regions. The region is experiencing growth across residential and professional dermatology segments, with keratolytic agents widely used in routine skincare, clinical therapies, and cosmetic treatments.

Japan Keratolytic Agents Market Insight

The Japan keratolytic agents market is gaining momentum due to high urbanization, a tech-savvy population, and strong emphasis on preventive dermatology. Dermatology clinics and retail outlets in major cities report increasing demand for urea- and salicylic acid-based keratolytic products for chronic skin conditions and cosmetic use. Japan’s aging population is driving demand for effective, easy-to-apply, and safe topical treatments suitable for residential and clinical applications.

China Keratolytic Agents Market Insight

The China keratolytic agents market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to rapid urbanization, rising middle-class income, and increasing access to professional dermatology services. Dermatology clinics in Shanghai and Beijing report strong demand for urea- and salicylic acid-based keratolytic formulations for therapeutic and cosmetic applications. Expanding access to skincare education, professional dermatology services, and high-quality locally manufactured products is driving broader adoption and sustained market growth.

Keratolytic Agents Market Share

The Keratolytic Agents industry is primarily led by well-established companies, including:

• Galderma (Switzerland)

• Pfizer (U.S.)

• Bayer (Germany)

• Novartis (Switzerland)

• Johnson & Johnson (U.S.)

• Sanofi (France)

• Fresenius Kabi (Germany)

• HRA Pharma (France)

• Glenmark Pharmaceuticals (India)

• Abbott Laboratories (U.S.)

• Boehringer Ingelheim (Germany)

• L’Oréal (France)

• Cipla (India)

• Mylan (U.S.)

• Beiersdorf (Germany)

• Sun Pharma (India)

• Shiseido (Japan)

• Dr. Reddy’s Laboratories (India)

• Hoffmann-La Roche (Switzerland)

• Amorepacific Corporation (South Korea

Latest Developments in Global Keratolytic Agents Market

- In January 2022, the global topical and keratolytic market began to gain renewed commercial and R&D focus, as market research identified increased demand for keratolytic products in acne, psoriasis, dry skin, and callus treatment, laying the groundwork for expansion in both therapeutic and cosmetic applications. This trend was highlighted in industry trend reports for the year

- In September 2022, market intelligence reports signaled rising investment in skin‑exfoliating and keratolytic combination therapies, particularly in formulations targeting dermatological conditions like hyperkeratosis and seborrheic dermatitis — a strategic shift toward multi‑use keratolytic products

- In March 2023, Beiersdorf expanded its UreaRepair PLUS product portfolio with a higher‑concentration urea‑based keratolytic cream aimed at improved foot‑care outcomes, especially in diabetic skin care settings — illustrating a shift from cosmetic exfoliants toward medical‑need keratolytic products

- In June 2023, global skincare companies reported that salicylic acid and urea‑based keratolytic products continued to dominate due to their effectiveness and consumer acceptance for acne, psoriasis, and callus removal — influencing both OTC product launches and prescription product pipelines

- In October 2023, La Roche‑Posay (L’Oréal) expanded its keratolytic‑oriented exfoliation system under its dermo‑cosmetics division, using digital skin diagnostics to personalize AHA/PHA‑based keratolytic solutions — a convergence of digital analysis and active formulation

- In January 2024, Perrigo Company launched a new private‑label keratolytic product line for major retail pharmacy chains (such as CVS and Walgreens) featuring simplified ingredients and consumer‑friendly claims for wart and psoriasis care — indicating rising mainstream retail penetration

- In March 2024, Glenmark Pharmaceuticals entered the foot‑care keratolytic space with a topical urea‑salicylic acid combo cream targeting callused diabetic skin, marking a notable example of pharma companies innovating beyond traditional systemic treatments toward topical keratolytic solutions

- In April 2025, refinements in keratolytic R&D were reported, including collaborations between major dermatology product developers (e.g., research alliances focusing on combining salicylic acid with other active agents for enhanced acne and plaque reduction efficacy) with intentions to launch improved dual‑mechanism products by the end of 2025

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.