Global Kidney And Pancreas Transplant Market

Market Size in USD Billion

USD

20.12 Billion

USD

47.82 Billion

2025

2033

USD

20.12 Billion

USD

47.82 Billion

2025

2033

| 2026 - 2033 | |

| USD 20.12 Billion | |

| USD 47.82 Billion | |

| % | |

|

Kidney and Pancreas Transplant Market Overview

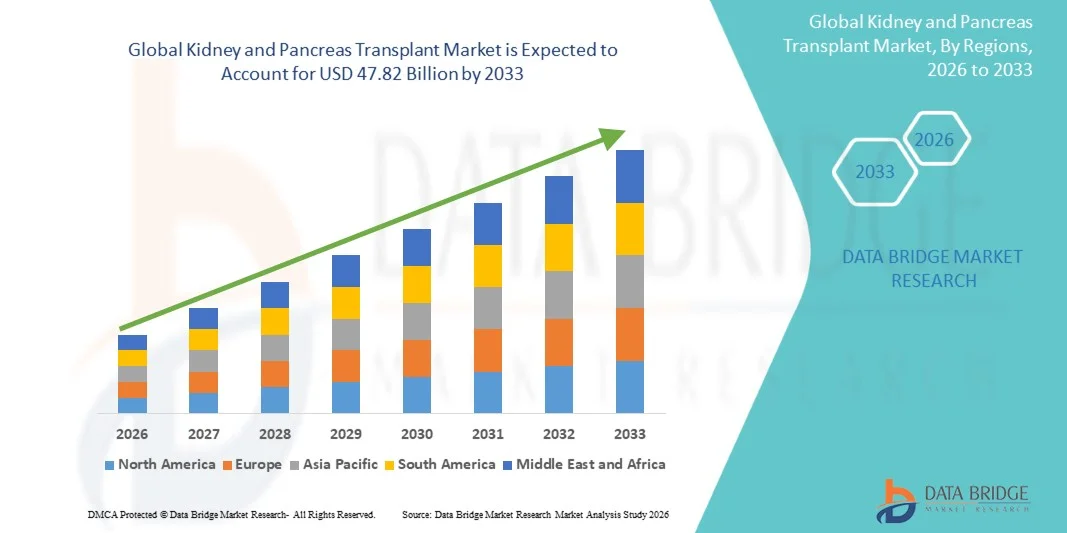

The Kidney and Pancreas Transplant Market was valued at USD 20.12 billion in 2025 and is projected to reach USD 47.82 billion by 2033, growing at a CAGR of 11.50% from 2026 to 2033. Market growth is supported by the rising prevalence of end-stage renal disease (ESRD), increasing incidence of type 1 and type 2 diabetes leading to organ failure, advances in immunosuppressive therapies, and improved surgical techniques for transplantation procedures.

The excellent success rates connected to kidney and pancreas transplant procedures, combined with accelerated recovery times and improved patient outcomes compared to long-term dialysis or insulin dependency, are driving increased adoption among both patients and medical professionals. Ongoing technological advancements in organ preservation technologies, including hypothermic and normothermic machine perfusion systems, enhanced immunosuppressant drug regimens, and integrated donor-recipient matching algorithms, are expanding the clinical applicability of kidney and pancreas transplantation across nephrology, endocrinology, and transplant surgery specialties. In addition, growing organ donation awareness programs, expanding healthcare infrastructure investments in emerging markets, and the proliferation of specialized transplant centers are creating new opportunities for stakeholders across the forecast period.

Key Market Trends & Insights

- North America dominated the Kidney and Pancreas Transplant Market with the largest revenue share of 45.0% in 2025, supported by high transplant volumes, advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of leading transplant centers and pharmaceutical companies.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 13.25% from 2026 to 2033, driven by expanding healthcare infrastructure, rising incidence of chronic kidney disease and diabetes, increasing healthcare expenditure, and growing organ donation initiatives.

- The Kidney segment led the market with a 78.5% market share in 2025, reflecting the significantly higher volume of kidney transplants performed globally compared to pancreas transplants and strong clinical evidence supporting improved patient survival and quality of life outcomes.

- The Pancreas segment is anticipated to be the fastest-growing organ type category at a CAGR of 13.80% from 2026 to 2033, driven by increasing prevalence of insulin-dependent diabetes, growing adoption of simultaneous kidney-pancreas transplantation, and technological advancements enabling improved graft survival.

- The Deceased Donors segment dominated the sources category with a 60.0% market share in 2025, supported by established organ procurement organizations, expanding deceased donor programs, and favorable regulatory frameworks promoting organ donation.

- The Living Donors segment is expected to witness strong growth during the forecast period at a CAGR of 12.90% from 2026 to 2033, driven by improved donor safety protocols, expanding paired kidney exchange programs, and rising awareness of living donation benefits.

- The Hospitals segment dominated the end-user category with a 55.0% market share in 2025, supported by access to multidisciplinary transplant teams, comprehensive perioperative care infrastructure, and advanced surgical facilities.

- The Transplant Centers segment is expected to witness the fastest growth during the forecast period at a CAGR of 13.45% from 2026 to 2033, driven by specialized expertise, dedicated transplant programs, and expanding capacity to address growing waitlist demands.

Market Size & Forecast

- Global Market Value (2025): USD 20.12 Billion

- Expected Market Value (2033): USD 47.82 Billion

- Forecast CAGR (2026–2033): 11.50%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Kidney and Pancreas Transplant Market Segmentation

|

Attributes |

Kidney and Pancreas Transplant Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· AbbVie Inc. (U.S.) · Novartis AG (Switzerland) · Pfizer Inc. (U.S.) · Astellas Pharma Inc. (Japan) · Roche Holding AG (Switzerland) · Bristol-Myers Squibb Company (U.S.) · Sanofi S.A. (France) · Veloxis Pharmaceuticals A/S (Denmark) · Organ Recovery Systems (U.S.) · TransMedics, Inc. (U.S.) · XVIVO Perfusion AB (Sweden) · Paragonix Technologies, Inc. (U.S.) |

|

Market Opportunities |

· Expansion of organ preservation technologies including normothermic machine perfusion and portable perfusion devices to reduce organ discard rates and extend viable transport distances · Development of xenotransplantation and bioengineered organ solutions to address critical donor organ shortages and expand eligible patient populations |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Kidney and Pancreas Transplant Market Trends

Trend: Technological Advancements in Organ Preservation and Transportation

Clinical adoption of advanced organ preservation technologies continues to accelerate as innovations in hypothermic machine perfusion (HMP) and normothermic machine perfusion (NMP) systems improve organ viability, extend preservation times, and reduce discard rates. Advanced perfusion systems maintain donor kidneys and pancreases in optimal physiological conditions during transport, enabling better assessment of organ quality and improving transplant outcomes. Portable perfusion devices designed for ease of transport and integration with existing surgical workflows are expanding access to high-quality donor organs across greater geographic distances.

For instance,

The National Kidney Foundation invested in Northernmost to support development of the NoMo Kidney Pump, a next-generation hypothermic machine perfusion system designed to be small, portable, and airline-compatible. The device aims to improve cold storage outcomes and enable broader distribution of donor kidneys.

In addition, research demonstrates that machine perfusion technologies reduce delayed graft function rates and improve long-term graft survival compared to traditional static cold storage methods, supporting broader clinical adoption across kidney and pancreas transplantation programs. The integration of AI-powered organ quality assessment algorithms with perfusion systems is enabling more precise donor-recipient matching and optimization of organ utilization.

Kidney and Pancreas Transplant Market Dynamics

Key Market Driver: Rising Prevalence of End-Stage Renal Disease and Diabetes

The growing global burden of end-stage renal disease (ESRD) and diabetes mellitus is a primary driver of market growth. Kidney transplantation remains the gold standard treatment for ESRD patients, offering superior survival outcomes and quality of life compared to long-term dialysis. Similarly, pancreas transplantation provides insulin independence for patients with insulin-dependent diabetes, preventing or reversing secondary diabetic complications when performed early. The increasing prevalence of risk factors including hypertension, obesity, and metabolic syndrome is expanding the patient population requiring transplantation services.

For instance,

According to market research, nearly 30% of Type 1 diabetes patients and 10% to 40% of Type 2 diabetes patients eventually develop kidney failure, creating substantial demand for kidney and combined kidney-pancreas transplantation.

Rising disease prevalence combined with improved transplant outcomes is expected to strengthen adoption of kidney and pancreas transplantation procedures globally.

Key Restraint/Challenge: Critical Shortage of Donor Organs

The persistent shortage of donor organs relative to the growing number of patients on transplant waiting lists presents a significant barrier to market expansion. The gap between organ supply and demand continues to widen despite advances in organ procurement and allocation systems. Approximately one in five donated kidneys are discarded due to quality concerns or logistical challenges, representing lost transplantation opportunities. Extended waiting times for transplantation are associated with increased patient morbidity and mortality.

For instance,

According to Health Resources and Services Administration data, approximately 97,610 patients in the U.S. were waiting for kidney transplants, while only limited transplant procedures were performed due to donor organ scarcity.

The critical donor shortage constrains market growth potential despite strong underlying demand.

Key Market Opportunity: Emerging Technologies and Alternative Donor Sources

The development of xenotransplantation technologies, bioengineered organs, and improved preservation methods is creating opportunities to address critical donor organ shortages. Gene-edited pig kidney transplants represent a promising alternative donor source that could dramatically expand the available organ pool. Advances in 3D bioprinting of kidney scaffolds and decellularized extracellular matrix technologies are paving the way for potential future innovations in kidney and pancreas bioengineering.

For instance,

Research into xenotransplantation demonstrated significant advances in 2024, with gene-edited pig kidney transplants performed in human patients representing major milestones toward addressing the organ donor shortage.

These emerging technologies offer transformative opportunities to expand transplantation access and reduce waitlist mortality.

Kidney and Pancreas Transplant Market Scope

The kidney and pancreas transplant market is segmented on the basis of organ type, sources, and end-user.

By Organ Type

On the basis of organ type, the Kidney and Pancreas Transplant Market is segmented into kidney and pancreas. The kidney segment dominated the market with a 78.5% market share in 2025, reflecting the significantly higher volume of kidney transplantation procedures performed globally. Strong clinical evidence supporting improved patient survival, enhanced quality of life, and cost-effectiveness compared to long-term dialysis has driven widespread adoption across transplant programs worldwide. High procedure volumes in academic medical centers, university hospitals, and specialized nephrology practices contribute to segment leadership.

The pancreas segment is expected to witness the fastest growth at a CAGR of 13.80% from 2026 to 2033, driven by increasing prevalence of insulin-dependent type 1 diabetes, growing adoption of simultaneous pancreas-kidney (SPK) transplantation for diabetic patients with renal failure, and technological advancements improving pancreas graft survival rates. Enhanced surgical techniques and improved immunosuppressive regimens are expanding the eligible patient population for pancreas transplantation.

By Sources

On the basis of sources, the Kidney and Pancreas Transplant Market is segmented into living donors and deceased donors. The deceased donors segment dominated the market with a 60.0% market share in 2025, supported by well-established organ procurement organization infrastructure, favorable allocation systems, and expanding deceased donor programs across developed markets. Comprehensive regulatory frameworks governing organ recovery, preservation, and distribution contribute to high deceased donor transplant volumes. The concentration of deceased donor programs within major transplant centers and university hospitals drives segment leadership.

The living donors segment is expected to witness the fastest growth at a CAGR of 12.90% from 2026 to 2033, driven by improved living donor safety outcomes, expanding paired kidney exchange programs, and rising awareness of living donation benefits among potential donors and recipients. Enhanced laparoscopic and robotic-assisted nephrectomy techniques have reduced donor morbidity and recovery times, increasing willingness to donate.

By End-User

On the basis of end-user, the Kidney and Pancreas Transplant Market is segmented into hospitals, transplant centers, and others. The hospitals segment dominated the market with a 55.0% market share in 2025, driven by access to multidisciplinary transplant teams, comprehensive perioperative care infrastructure, and advanced surgical facilities required for complex transplantation procedures. Hospitals serve as primary centers for kidney and pancreas transplants requiring extended surgical times, intensive postoperative monitoring, and specialized immunosuppression management. The concentration of transplant surgery, nephrology, and endocrinology expertise within hospital systems contributes to high procedure volumes and equipment utilization.

The transplant centers segment is expected to witness the fastest growth at a CAGR of 13.45% from 2026 to 2033, driven by specialized transplant expertise, dedicated infrastructure, and expanding capacity to address growing waitlist demands. Standalone transplant centers and specialized units within healthcare networks are increasingly focused on streamlining the transplant process, reducing wait times, and improving patient throughput. Growing emphasis on center-specific outcomes reporting and quality metrics is driving investment in specialized transplant facilities.

Kidney and Pancreas Transplant Market Regional Analysis

North America dominated the kidney and pancreas transplant market with a revenue share of 45.0% in 2025, supported by high transplant volumes, advanced healthcare infrastructure, strong reimbursement frameworks, and the presence of leading transplant centers and pharmaceutical companies. Favorable regulatory pathways, robust clinical networks, and extensive surgeon experience with transplantation procedures contribute to regional market leadership.

U.S. Kidney and Pancreas Transplant Market Insight

The U.S. kidney and pancreas transplant market benefits from the highest volume of transplant procedures globally, extensive transplant center networks, and strong clinical protocols. Academic medical centers, large health systems, and specialized transplant programs continue to expand capacity and improve outcomes across kidney, pancreas, and combined kidney-pancreas transplantation. Favorable Medicare and commercial payer reimbursement supports procedural volumes, immunosuppressant utilization, and infrastructure investment. The U.S. accounted for 38.5% of the North American market share in 2025.

Europe Kidney and Pancreas Transplant Market Insight

The Europe kidney and pancreas transplant market remains a major contributor, with strong transplant programs across Germany, the U.K., France, Spain, and the Netherlands. Growing adoption of machine perfusion technologies and standardized organ allocation systems are improving transplant access and outcomes across public and private healthcare systems. Cross-border organ sharing agreements through Eurotransplant and other networks are optimizing organ utilization and reducing discard rates.

U.K. Kidney and Pancreas Transplant Market Insight

The U.K. kidney and pancreas transplant market is characterized by expanding transplant programs within NHS hospitals and specialized transplant centers. Investment in deceased donation infrastructure, machine perfusion systems, and paired kidney exchange programs is improving access to transplantation and reducing waiting times. The U.K. accounted for 18.2% of the European market share in 2025.

Germany Kidney and Pancreas Transplant Market Insight

Germany's robust hospital infrastructure and advanced surgical capabilities support comprehensive transplant programs across kidney and pancreas transplantation. Strong clinical training networks, favorable reimbursement frameworks, and participation in Eurotransplant allocation contribute to high procedure volumes and technology adoption. Germany is expected to grow at a CAGR of 9.85% from 2026 to 2033.

Asia-Pacific Kidney and Pancreas Transplant Market Insight

The Asia-Pacific kidney and pancreas transplant market is poised for rapid growth at a CAGR of 13.25% during the forecast period, driven by expanding healthcare infrastructure, rising prevalence of chronic kidney disease and diabetes, increasing healthcare expenditure, and growing organ donation awareness initiatives. Private healthcare systems and government-supported transplant programs in China, Japan, India, South Korea, and Australia are investing in transplant capabilities to meet growing patient demand.

Japan Kidney and Pancreas Transplant Market Insight

The Japan kidney and pancreas transplant market benefits from advanced healthcare infrastructure, strong surgical expertise, and favorable reimbursement for transplant procedures. Living donor kidney transplants represent a significant proportion of total transplants due to cultural factors and established living donation programs. Japan held a 22.4% market share in the Asia-Pacific region in 2025.

China Kidney and Pancreas Transplant Market Insight

The China kidney and pancreas transplant market is experiencing rapid growth driven by healthcare modernization initiatives, expanding hospital transplant programs, and increasing government support for organ donation systems. Domestic pharmaceutical development of immunosuppressants and organ preservation technologies is complementing imported solutions, improving market accessibility. China is expected to grow at a CAGR of 14.60% from 2026 to 2033.

Kidney and Pancreas Transplant Market Share

The kidney and pancreas transplant industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Astellas Pharma Inc. (Japan)

- Roche Holding AG (Switzerland)

- Bristol-Myers Squibb Company (U.S.)

- Sanofi S.A. (France)

- Veloxis Pharmaceuticals A/S (Denmark)

- Organ Recovery Systems (U.S.)

- TransMedics, Inc. (U.S.)

- XVIVO Perfusion AB (Sweden)

- Paragonix Technologies, Inc. (U.S.)

Latest Developments in Kidney and Pancreas Transplant Market

- In February 2026, the National Kidney Foundation announced its investment in Northernmost to support development of the NoMo Kidney Pump, a next-generation hypothermic machine perfusion system designed to be portable and airline-compatible for improved kidney transport and preservation.

- In December 2025, Medtronic received U.S. FDA clearance for expanded indications of its Hugo Robotic-Assisted Surgery System for urologic surgical procedures, including robotic-assisted nephrectomy, supporting minimally invasive approaches to living donor kidney procurement.

- In October 2024, the National Kidney Foundation's Innovation Fund invested in ZeitLife to advance development of normothermic machine perfusion fluids designed to keep donor kidneys functioning in near-physiological conditions, with expected market launch within 2 to 5 years.

- In September 2024, researchers at Massachusetts General Hospital reported successful gene-edited pig kidney xenotransplantation in human patients, representing a major milestone in addressing the critical organ donor shortage for kidney transplantation.

- In August 2024, a study published in JAMA demonstrated that mortality among living kidney donors significantly declined over the past decade, supporting expansion of living donor programs with fewer than one death per 10,000 donors reported between 2013 and 2022.

- In June 2024, Northwestern Medicine performed the first known awake kidney transplant surgery with next-day discharge, demonstrating the potential for spinal anesthesia to reduce recovery times and expand transplantation access for patients with risks or phobias to general anesthesia.

- In April 2024, Veloxis Pharmaceuticals announced expanded distribution agreements for Envarsus XR (extended-release tacrolimus) in European markets, supporting improved immunosuppression adherence for kidney transplant recipients.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.