Global Label Free Array Systems Market

Market Size in USD Billion

USD

1.52 Billion

USD

2.73 Billion

2024

2032

USD

1.52 Billion

USD

2.73 Billion

2024

2032

| 2025 - 2032 | |

| USD 1.52 Billion | |

| USD 2.73 Billion | |

| % | |

|

Label-Free Array Systems Market Size

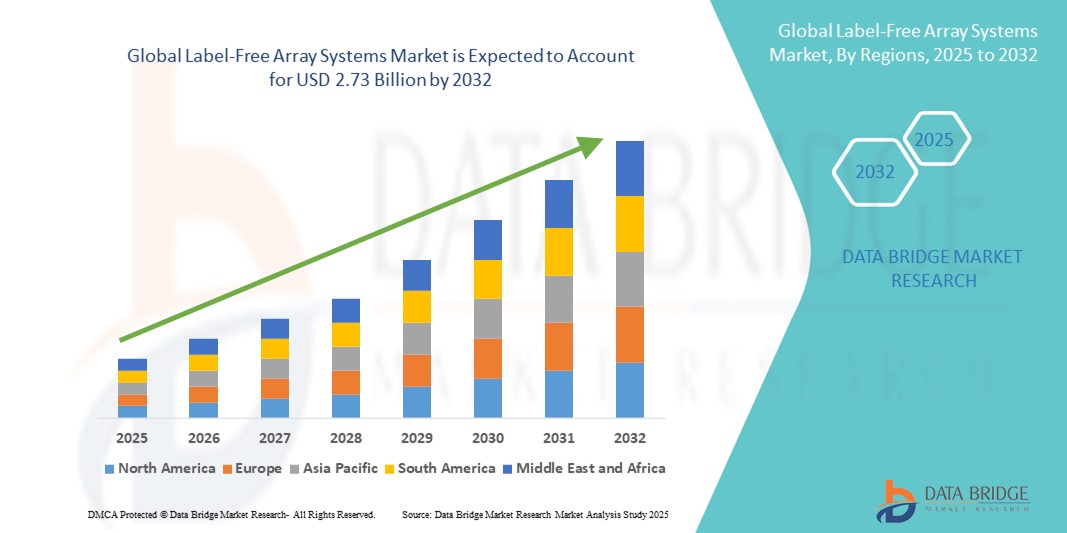

- The global label-free array systems market size was valued at USD 1.52 billion in 2024 and is expected to reach USD 2.73 billion by 2032, at a CAGR of 7.55% during the forecast period

- This growth is primarily driven by the increasing demand for personalized medicine, advancements in drug discovery and development, and the rising prevalence of chronic and infectious diseases. Label-free array systems offer significant advantages in biomolecular interaction analysis by eliminating the need for fluorescent, radioactive, or enzymatic labels, thereby providing more accurate and real-time data

- Furthermore, the market is witnessing a surge in research activities in biomedical sciences, the need for high-throughput screening, and the demand for cost-effective and efficient systems

Label-Free Array Systems Market Analysis

- Label-free array systems, enabling real-time biomolecular interaction analysis without the need for fluorescent or radioactive labels, are becoming essential tools in drug discovery, diagnostics, and biomedical research, providing more accurate, high-throughput, and cost-effective solutions for both academic and commercial laboratories

- The growing adoption of personalized medicine, advancements in biotechnology, and increasing prevalence of chronic and infectious diseases are driving the demand for label-free array systems, as researchers seek efficient and precise analytical platforms

- North America dominated the global label-free array systems market with the largest revenue share of 39.2% in the label-free array systems market in 2024, attributed to the presence of leading biotech companies, advanced research infrastructure, and high R&D expenditure, with the U.S. leading in adoption across pharmaceutical and academic research institutions

- Asia-Pacific is projected to be the fastest-growing region during the forecast period, driven by rising investment in life sciences research, expansion of biotechnology industries, and increasing government support for healthcare innovation

- Surface plasmon resonance (SPR) segment dominated the label-free array systems market with a market share of 42.6% in 2024, owing to its established reliability, sensitivity, and versatility for analyzing protein, nucleic acid, and small molecule interactions across various applications

Report Scope and Label-Free Array Systems Market Segmentation

|

Attributes |

Label-Free Array Systems Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Label-Free Array Systems Market Trends

Advancements in Real-Time, High-Throughput Analysis

- A key trend in the global label-free array systems market is the increasing adoption of high-throughput, real-time biomolecular interaction analysis platforms that eliminate the need for fluorescent, radioactive, or enzymatic labels, significantly improving efficiency and accuracy in drug discovery, diagnostics, and biomedical research

- For instance, Biacore SPR systems offer real-time monitoring of protein, nucleic acid, and small molecule interactions without labeling, enabling researchers to accelerate lead identification and optimize experimental workflows. Similarly, Carterra LSA instruments provide automated, high-throughput analysis suitable for large-scale screening projects

- Integration with advanced software and AI-enabled analytics allows label-free systems to provide insights into binding kinetics, affinity, and molecular interactions, improving decision-making and reducing experimental errors. Some systems now include predictive modeling capabilities to optimize assay design and experimental outcomes

- Seamless integration of label-free array systems with laboratory information management systems (LIMS) and other analytical platforms facilitates centralized data management, allowing researchers to monitor multiple experiments, automate data capture, and generate comprehensive reports efficiently

- This trend toward more intelligent, automated, and high-throughput label-free analysis is reshaping expectations for laboratory workflows, leading companies such as ForteBio and Bio-Rad to develop next-generation systems with enhanced throughput, sensitivity, and user-friendly interfaces

- Demand for these advanced label-free array systems is growing across pharmaceutical, biotechnology, and academic research sectors, as organizations seek accurate, efficient, and scalable analytical platforms

Label-Free Array Systems Market Dynamics

Driver

Increasing Need for Efficient, High-Throughput Screening and Drug Discovery

- The rising demand for more efficient, precise, and label-free methods for biomolecular interaction analysis is a key driver of market growth. Researchers require platforms that provide real-time, high-throughput data to accelerate drug discovery, diagnostics, and biomarker identification

- For instance, in March 2024, Bio-Rad launched a next-generation SPR imaging system designed to improve throughput and sensitivity for pharmaceutical screening, enhancing workflow efficiency in academic and commercial laboratories. Such innovations by leading companies are expected to propel market growth in the forecast period

- Label-free array systems reduce the reliance on labels, minimize assay interference, and improve the accuracy of interaction studies, offering a compelling advantage over traditional labeled methods

- Pharmaceutical and biotechnology companies are increasingly integrating label-free platforms into their R&D workflows to accelerate lead identification, optimize binding studies, and streamline biomarker validation, driving adoption across the sector

Restraint/Challenge

High Costs and Technical Expertise Requirements

- Despite their advantages, label-free array systems often involve high initial investment costs and may require specialized technical expertise, posing challenges to adoption, particularly for small laboratories or institutions in developing regions

- For instance, advanced SPR or bio-layer interferometry (BLI) systems can be costly to purchase and maintain, and require trained personnel to operate and interpret complex datasets, limiting accessibility for some users

- Addressing these challenges through the development of more user-friendly interfaces, automated workflows, and cost-effective models will be critical for expanding market penetration

- Furthermore, the need for standardized protocols and robust data analysis tools remains a barrier for some laboratories seeking to integrate label-free systems into routine workflows, necessitating ongoing training and technical support

- Overcoming these hurdles through improved affordability, automation, and user training programs will be vital for sustained growth and wider adoption of label-free array systems globally

Label-Free Array Systems Market Scope

The market is segmented on the basis of technique, application, and end-user.

- By Technique

On the basis of technique, the label-free array systems market is segmented into Surface Plasmon Resonance (SPR), Microcantilever, Scanning Kelvin Nanoprobe, Enthalpy Array, Atomic Force Microscopy (AFM), Bio-Layer Interferometry (BLI), Cellular Dielectric Spectroscopy, Electrochemical Impedance Spectroscopy, Quartz Crystal Microbalance Interference-based Technique, Ellipsometry Technique, and Others. The Surface Plasmon Resonance (SPR) segment dominated the market with the largest market revenue share of 42.6% in 2024. This dominance is driven by SPR’s high sensitivity, reliability, and versatility in detecting molecular interactions such as protein-protein, protein-DNA, and antibody-antigen binding. Researchers prefer SPR systems due to their real-time label-free detection, robustness in high-throughput screening, and widespread adoption across pharmaceutical, biotech, and academic laboratories. In addition, the established presence of leading SPR system providers and extensive validation in multiple applications further reinforce its market dominance. The segment also benefits from continuous technological upgrades, including multi-channel SPR systems and AI-integrated analytics.

The Bio-Layer Interferometry (BLI) segment is anticipated to witness the fastest growth from 2025 to 2032, driven by its capacity for high-throughput analysis and automation. BLI allows simultaneous monitoring of multiple interactions, which reduces experimental time and enhances productivity in drug discovery and antibody development. Its ease of use, label-free detection, and compatibility with robotic platforms make it highly attractive for pharmaceutical companies and CROs. In addition, BLI’s lower sample consumption and scalable workflows support growing demands for efficiency and cost-effectiveness in large-scale research projects. The increasing integration of BLI with advanced data analysis software and AI for predictive modeling is further accelerating adoption.

- By Application

On the basis of application, the label-free array systems market is segmented into drug discovery, biomolecular interactions, protein interface analysis, antibody characterization and development, protein complex and cascade analysis, detection of disease biomarkers, and others. The Drug Discovery segment dominated the market with the largest market revenue share of 39.8% in 2024. The dominance is attributed to the growing demand for label-free systems to accelerate lead identification, optimize binding studies, and reduce experimental errors in pharmaceutical R&D. Drug discovery labs rely on label-free analysis for screening compound libraries, characterizing molecular interactions, and identifying potential therapeutic candidates more efficiently than traditional labeled assays. Moreover, regulatory focus on precision and reproducibility in preclinical studies encourages adoption of label-free platforms.

The Detection of Disease Biomarkers segment is expected to witness the fastest growth from 2025 to 2032, driven by the rising prevalence of chronic and infectious diseases and increasing investments in diagnostic research. Label-free systems are highly suited for early biomarker detection due to their sensitivity, real-time monitoring capabilities, and minimal sample preparation requirements. As personalized medicine and point-of-care diagnostics expand, demand for biomarker detection using label-free arrays is expected to accelerate. The ability to integrate with high-throughput workflows and automated data analysis platforms further strengthens growth prospects for this application.

- By End-User

On the basis of end-user, the label-free array systems market is segmented into contract research organizations (cros), academic and research institutes, agricultural research institutes, and pharmaceutical and biotechnology industries. The Pharmaceutical and Biotechnology Industries segment dominated the market with the largest revenue share of 44.5% in 2024. This is driven by the high adoption of label-free systems in drug discovery, antibody development, and biomolecular research to enhance efficiency and accuracy. These industries prioritize platforms that reduce assay complexity, provide real-time data, and support high-throughput screening, making label-free systems essential in modern R&D workflows.

The Academic and Research Institutes segment is expected to witness the fastest growth from 2025 to 2032 due to increasing research activities, rising funding for life sciences, and adoption of advanced analytical techniques in universities and public research institutions. Label-free systems allow academic researchers to study fundamental molecular interactions, protein dynamics, and biomarker identification efficiently, supporting innovation and publication outputs. The growing availability of automated, user-friendly label-free platforms tailored for academic settings is also accelerating adoption in this segment.

Label-Free Array Systems Market Regional Analysis

- North America dominated the label-free array systems market with the largest revenue share of 39.2% in the label-free array systems market in 2024, attributed to the presence of leading biotech companies, advanced research infrastructure, and high R&D expenditure, with the U.S. leading in adoption across pharmaceutical and academic research institutions

- Researchers and institutions in the region highly value the accuracy, real-time monitoring, and high-throughput capabilities offered by label-free array systems for applications such as drug discovery, biomolecular interaction analysis, and antibody characterization

- This widespread adoption is further supported by strong government funding for life sciences research, a technologically skilled workforce, and the growing demand for precision medicine, establishing label-free array systems as essential tools in both academic and commercial laboratories

U.S. Label-Free Array Systems Market Insight

The U.S. label-free array systems market captured the largest revenue share of 41% in 2024 within North America, driven by the strong presence of leading biotechnology and pharmaceutical companies, advanced research infrastructure, and high R&D expenditure. Researchers increasingly prioritize label-free platforms for applications such as drug discovery, biomolecular interaction analysis, and antibody characterization. The adoption of automated, high-throughput systems and integration with laboratory information management systems (LIMS) further fuels market growth. Moreover, the U.S. emphasis on precision medicine and cutting-edge research accelerates the demand for advanced label-free technologies.

Europe Label-Free Array Systems Market Insight

The Europe label-free array systems market is projected to expand at a substantial CAGR during the forecast period, driven by rising investments in life sciences research, strict regulatory requirements for drug development, and increasing focus on diagnostic innovations. The growing adoption of connected laboratory solutions, coupled with the demand for high-throughput and accurate analytical platforms, is fostering market growth. European academic and commercial research centers are leveraging label-free systems for biomolecular studies, antibody development, and disease biomarker detection, contributing to the overall expansion of the market.

U.K. Label-Free Array Systems Market Insight

The U.K. label-free array systems market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the country’s robust biotechnology sector and increasing focus on translational research. The rising prevalence of chronic diseases and demand for precision medicine are driving investments in label-free systems for drug discovery and biomolecular interaction studies. In addition, strong research funding, advanced laboratory infrastructure, and the integration of automated analytical platforms are expected to stimulate market growth in both academic and commercial laboratories.

Germany Label-Free Array Systems Market Insight

The Germany label-free array systems market is expected to expand at a considerable CAGR during the forecast period, supported by high R&D investment, advanced biotechnology infrastructure, and a growing emphasis on innovation in diagnostics and therapeutics. Researchers in Germany are increasingly adopting label-free technologies for antibody characterization, protein complex analysis, and high-throughput screening applications. Furthermore, the integration of label-free systems with AI-based analytics and laboratory automation enhances data accuracy, efficiency, and scalability, promoting market adoption in both academic and industrial research settings.

Asia-Pacific Label-Free Array Systems Market Insight

The Asia-Pacific label-free array systems market is poised to grow at the fastest CAGR of 23% during the forecast period of 2025 to 2032, driven by increasing investments in biotechnology and pharmaceutical research, rising prevalence of chronic and infectious diseases, and rapid technological adoption in countries such as China, Japan, and India. Government initiatives promoting life sciences innovation, coupled with expanding laboratory infrastructure, are accelerating the deployment of label-free systems. In addition, the region is emerging as a manufacturing hub for analytical instruments, improving affordability and accessibility across research institutions.

Japan Label-Free Array Systems Market Insight

The Japan label-free array systems market is gaining momentum due to the country’s advanced research ecosystem, strong focus on drug discovery, and high adoption of precision medicine. Japanese research institutions and pharmaceutical companies increasingly utilize label-free systems for biomolecular interaction studies, protein analysis, and antibody development. The integration of these systems with automated workflows and AI-based analytics enhances efficiency and accuracy, driving adoption in both academic and industrial laboratories.

India Label-Free Array Systems Market Insight

The India label-free array systems market accounted for the largest market revenue share in Asia-Pacific in 2024, driven by rapid growth in biotechnology research, expanding pharmaceutical R&D, and increasing government support for life sciences innovation. India’s growing research infrastructure, combined with rising adoption of advanced analytical instruments in academic and commercial labs, supports the demand for label-free systems. The availability of cost-effective solutions and domestic manufacturing of laboratory instruments further accelerates market growth across drug discovery, biomarker detection, and protein interaction studies.

Label-Free Array Systems Market Share

The Label-Free Array Systems industry is primarily led by well-established companies, including:

- Agilent Technologies, Inc. (U.S.)

- Danaher Corporation (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Bio-Rad Laboratories, Inc. (U.S.)

- PerkinElmer (U.S.)

- Corning Incorporated (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Attana AB (Sweden)

- Molecular Devices, LLC (U.S.)

- Eppendorf AG (Germany)

- Illumina, Inc. (U.S.)

- Merck KGaA (Germany)

- BD (U.S.)

- Sartorius AG (Germany)

- Waters Corporation (U.S.)

- Horiba, Ltd. (Japan)

- Lucid Scientific (U.S.)

- Zellkraftwerk GmbH (Germany)

- Molecular Devices, LLC (U.S.)

What are the Recent Developments in Global Label-Free Array Systems Market?

- In September 2024, Carterra, Inc. launched the Carterra Ultra, a new high-throughput surface plasmon resonance (HT-SPR) platform. The Carterra Ultra is designed to offer enhanced sensitivity, allowing for the characterization of molecules as small as 100 Daltons. This new platform aims to accelerate drug discovery by providing high-resolution data for both small and large molecules and supporting workflows for artificial intelligence and machine learning (AI/ML) based approaches

- In August 2023, Danaher Corporation announced a definitive agreement to acquire Abcam plc. Abcam is a leading global supplier of protein consumables, including antibodies, reagents, and assays. This acquisition, which was completed in December 2023, was a strategic move to strengthen Danaher's position in the life sciences market and expand its portfolio of tools for biological research and drug discovery

- In April 2022, Sartorius launched the Octet SF3, its first Surface Plasmon Resonance (SPR) system. Up until this point, the company's Octet brand was primarily associated with Bio-Layer Interferometry (BLI). With the launch of the Octet SF3, Sartorius became the first company to offer both leading label-free technologies, BLI and SPR, under a single brand. The new system was designed to provide robust and high-throughput characterization of biomolecular interactions

- In November 2021, Agilent Technologies completed the acquisition of ACEA Biosciences. ACEA was a developer of real-time, label-free cell analysis technologies. The acquisition integrated ACEA's xCELLigence technology into Agilent's portfolio, enhancing its offerings for cell analysis, drug discovery, and cancer research

- In March 2021, Sartorius introduced the new Octet® R series of systems, a new high-performance line of Bio-Layer Interferometry (BLI) products. This series, which included the Octet® R2, R4, and R8, was designed to provide a balance of cost and throughput for different lab needs, from academic startups to high-volume research. The systems offered a future-proof, field-upgradeable option for labs to increase their throughput as their needs grew

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.