Global Labyrinthitis Market

Market Size in USD Million

USD

800.15 Million

USD

1,133.55 Million

2024

2032

USD

800.15 Million

USD

1,133.55 Million

2024

2032

| 2025 - 2032 | |

| USD 800.15 Million | |

| USD 1,133.55 Million | |

| % | |

|

Labyrinthitis Market Size

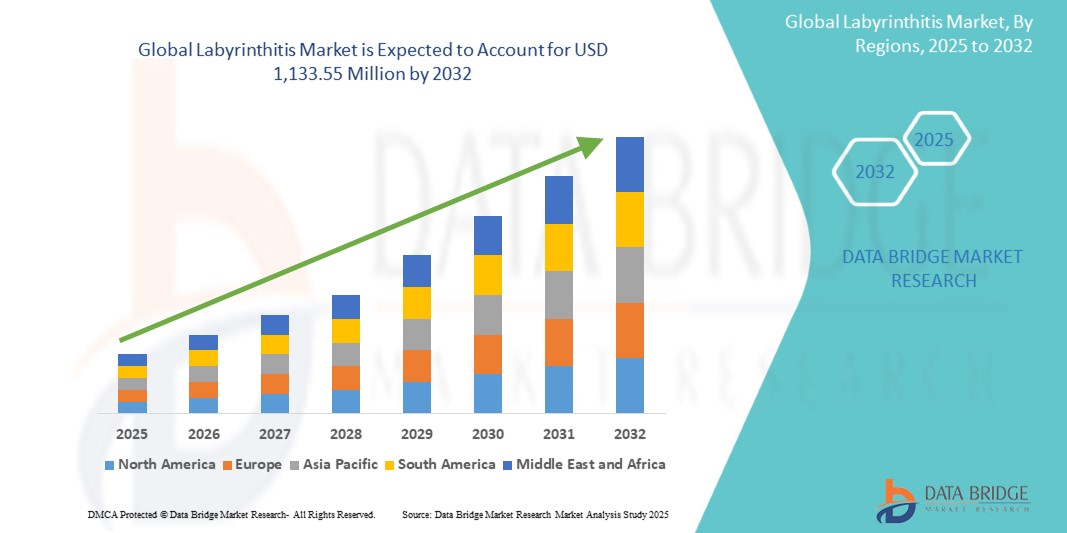

- The Global Labyrinthitis Market size was valued at USD 800.15 Million in 2024 and is expected to reach USD 1,133.55 Million by 2032, at a CAGR of 4.45% during the forecast period

- The market growth is primarily driven by the rising incidence of inner ear infections and autoimmune disorders, coupled with increasing awareness and early diagnosis of vestibular conditions that affect balance and hearing

- Furthermore, advancements in diagnostic imaging technologies such as MRI and CT, along with the expanded use of EEG and ENG for vestibular assessment, are enabling more accurate detection and treatment planning

- The growing demand for non-invasive pharmacological treatments such as corticosteroids, antiemetics, and antihistamines, along with improvements in healthcare access across emerging economies, are supporting the market’s expansion

Labyrinthitis Market Analysis

- Labyrinthitis, an inner ear disorder that causes inflammation of the labyrinth, is becoming an increasingly recognized condition in the field of neurology and otolaryngology due to its significant impact on balance, hearing, and quality of life. The rising prevalence of viral and bacterial infections, autoimmune disorders, and lifestyle-related stress is contributing to the increasing incidence of labyrinthitis worldwide.

- The growing demand for effective labyrinthitis treatment is primarily fueled by increasing awareness of vestibular disorders, the availability of advanced diagnostic tools like MRI, CT, EEG, and ENG, and an expanding patient pool seeking non-invasive treatment options for dizziness, vertigo, and hearing loss

- North America dominates the labyrinthitis market with the largest revenue share of 38.7% in 2025, attributed to high diagnostic accuracy, robust healthcare infrastructure, and the presence of specialized ENT and neurology clinics. The U.S. continues to lead regional growth, driven by early intervention practices, growing demand for advanced vestibular testing, and rising autoimmune-related labyrinthitis diagnoses

- Asia-Pacific is expected to be the fastest-growing region in the labyrinthitis market during the forecast period, supported by increased healthcare investments, a growing middle-class population, and rising public awareness about inner ear disorders. Emerging markets such as India and China are witnessing improved access to healthcare facilities and diagnostics, contributing to early detection and effective treatment.

- Asia-Pacific is expected to be the fastest growing region in the Labyrinthitis Market during the forecast period due to increasing urbanization and rising disposable incomes

- The corticosteroids segment is expected to dominate the treatment category with a market share of 41.6% in 2025, driven by its widespread use in managing inflammation and reducing vestibular symptoms. Corticosteroids are often considered the first line of treatment for both infective and autoimmune labyrinthitis, particularly in acute episodes, due to their fast-acting anti-inflammatory benefits and high efficacy in restoring balance and hearing function

Report Scope and Labyrinthitis Market Segmentation

|

Attributes |

Labyrinthitis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Labyrinthitis Market Trends

“Improved Diagnosis and Digital Health Integration Transforming Vestibular Care”

- A significant and evolving trend in the global labyrinthitis market is the increased adoption of advanced diagnostic technologies and the integration of digital health platforms to enhance patient care and treatment outcomes for vestibular disorders. These advancements are enabling faster, more accurate diagnoses and supporting remote monitoring and follow-up care, particularly in regions with limited access to ENT specialists.

- For instance, the use of portable electronystagmography (ENG) and vestibular evoked myogenic potentials (VEMP) systems is expanding, offering physicians real-time data on inner ear function. Additionally, wearable balance trackers and mobile apps for dizziness and vertigo self-assessment are gaining traction in outpatient and home settings.

- Digital tools are also being increasingly used to deliver vestibular rehabilitation therapy (VRT) through guided virtual programs, allowing patients to manage symptoms from home. These programs offer exercises tailored to individual balance deficits, helping reduce dizziness, prevent falls, and restore quality of life.

- This convergence of vestibular diagnostics, pharmacologic treatments, and digital rehabilitation platforms is reshaping the standard of care for labyrinthitis. It enables clinicians to deliver personalized, multidisciplinary treatment strategies that are both cost-effective and scalable across diverse healthcare settings.

- As healthcare systems globally shift toward preventive care and outpatient management, digital health solutions for labyrinthitis are expected to play an increasingly central role, especially in aging populations and rural communities.

- The rising consumer demand for non-invasive, patient-centric care models and early intervention tools is fueling continued innovation in this space, positioning labyrinthitis management as a key segment within the broader neurology and ENT landscape.

Labyrinthitis Market Dynamics

Driver

“Rising Prevalence of Vestibular Disorders and Increasing Awareness”

- The growing global incidence of vestibular disorders due to infections, autoimmune conditions, aging, and stress-related factors is a major driver for the labyrinthitis market.

- As more individuals report symptoms such as vertigo, dizziness, tinnitus, and balance disturbances, demand for accurate diagnostic and treatment pathways is rising rapidly.

- The healthcare community is increasingly recognizing labyrinthitis as a critical cause of sudden hearing loss and chronic vertigo, prompting the inclusion of vestibular assessments in primary care and neurology evaluations.

- For instance, the growing adoption of balance disorder screening in geriatric assessments and the inclusion of vestibular checks in ENT evaluations are expanding early detection.

- Public awareness campaigns, online health platforms, and patient education by neurologists and audiologists are helping to destigmatize vestibular issues and encourage timely treatment, thereby expanding the market base.

- As diagnostic infrastructure strengthens in emerging economies and teleconsultation becomes more common, access to care for labyrinthitis patients is expected to significantly improve, driving global market growth.

Restraint/Challenge

“Underdiagnosis, Misinterpretation, and Limited Access to Specialized Care”

- One of the major challenges limiting the labyrinthitis market is the underdiagnosis and frequent misinterpretation of symptoms, often mistaken for general vertigo, migraines, or anxiety disorders.

- Many primary care settings lack access to advanced vestibular testing tools such as ENG, VNG, or MRI, leading to delayed or incorrect diagnoses. This is particularly problematic in rural and low-resource regions, where ENT specialists and audiologists are scarce.

- Additionally, the lack of standardized diagnostic and treatment guidelines across countries results in variability in clinical practice, which can impact patient outcomes and hinder consistent market expansion.

- Treatment costs for advanced imaging and custom vestibular therapies may not be covered by insurance, especially in developing economies, posing a barrier for lower-income patients.

- Another limiting factor is the lack of awareness among healthcare providers regarding the autoimmune and post-viral origins of labyrinthitis, leading to underuse of corticosteroids or incorrect prescription of antibiotics in non-bacterial cases.

- Addressing these challenges requires capacity building, training of primary care physicians in vestibular assessments, and the wider distribution of portable, cost-effective diagnostic tools.

- Collaborations between tech developers and healthcare systems to deploy AI-enabled screening tools, mobile diagnostic apps, and standardized clinical protocols could help bridge the accessibility gap and ensure more timely and accurate care

Labyrinthitis Market Scope

The market is segmented on the basis of type, diagnosis, treatment, and end use.

• By Type

On the basis of type, the labyrinthitis market is segmented into infective labyrinthitis, autoimmune labyrinthitis, and others. The infective labyrinthitis segment dominates the market with the largest revenue share of 58.3% in 2025, driven by the high prevalence of viral and bacterial infections affecting the inner ear. Viral causes such as upper respiratory tract infections and influenza are particularly common triggers, leading to sudden episodes of vertigo and hearing loss.

The autoimmune labyrinthitis segment is projected to witness the fastest CAGR of 5.8% from 2025 to 2032, as awareness grows around autoimmune inner ear disease (AIED) and its role in chronic balance disorders. Advancements in autoimmune diagnostics and steroid-based therapies are facilitating early and targeted intervention, particularly in developed healthcare markets.

• By Diagnosis

On the basis of diagnosis, the market is segmented into physical examination, blood test, magnetic resonance imaging (MRI) and computed tomography (CT), electroencephalogram (EEG) and electronystagmography (ENG), and others. The MRI and CT segment holds the largest revenue share in 2025, driven by their role in ruling out structural abnormalities and accurately assessing inner ear inflammation. These imaging tools are critical in differentiating labyrinthitis from other neurological conditions such as stroke or vestibular neuritis.

The ENG/EEG segment is projected to witness the fastest growth during the forecast period, fueled by the rising availability of portable vestibular testing equipment and growing demand for objective balance assessments in ENT and neurology clinics.

• By Treatment

On the basis of treatment, the labyrinthitis market is segmented into corticosteroids, antibiotics, antiemetics, antihistaminics, and others. The corticosteroids segment is expected to dominate the market with a market share in 2025, owing to their effectiveness in reducing inner ear inflammation, improving balance, and restoring partial hearing loss in both autoimmune and post-viral cases. Corticosteroids remain the first-line treatment for acute labyrinthitis in clinical practice.

The antiemetics segment is anticipated to grow at the fastest CAGR from 2025 to 2032, supported by the increasing use of symptom-relief medications to control nausea and vertigo in both acute and chronic vestibular episodes.

• By End Use

On the basis of end use, the market is segmented into hospitals and clinics, academic and research institutions, and others. The hospitals and clinics segment accounted for the largest market revenue share in 2025, owing to the concentration of ENT specialists, access to advanced diagnostic imaging, and the availability of multi-disciplinary care under one roof. Emergency departments also play a crucial role in the initial assessment and management of sudden-onset vertigo.

The academic and research institutions segment is expected to witness the fastest CAGR from 2025 to 2032, as universities and neuroscience research centers increasingly focus on the pathophysiology of inner ear disorders, driving innovation in diagnostic techniques and therapeutic interventions.

Labyrinthitis Market Regional Analysis

- North America dominates the labyrinthitis market with the largest revenue share of 38.7% in 2024, driven by a rising prevalence of vestibular disorders, strong diagnostic infrastructure, and increased awareness about inner ear-related balance and hearing issues.

- Consumers in the region benefit from early access to ENT specialists, advanced imaging technologies such as MRI and CT, and comprehensive treatment options ranging from corticosteroids to vestibular rehabilitation therapy.

- This widespread adoption of labyrinthitis diagnosis and management is further supported by high healthcare expenditure, a well-developed hospital network, and growing emphasis on neurological and audiological health, establishing North America as a key hub for both clinical care and research in vestibular disorders.

U.S. Labyrinthitis Market Insight

The U.S. labyrinthitis market captured the largest revenue share of 80.3% within North America in 2025, driven by high awareness of vestibular disorders, robust ENT infrastructure, and widespread access to advanced diagnostic tools such as MRI, CT, and ENG. The country’s growing elderly population and rising incidence of autoimmune and post-viral inner ear disorders are increasing patient volumes. Additionally, the integration of telehealth, mobile vestibular rehabilitation programs, and multidisciplinary care models is further fueling the demand for personalized labyrinthitis management. Insurance coverage for ENT consultations and corticosteroid treatments also supports market expansion.

Europe Labyrinthitis Market Insight

The European labyrinthitis market is projected to expand at a substantial CAGR throughout the forecast period, driven by a growing elderly population, expanding neurological screening programs, and strong ENT specialization across the region. The rising focus on early detection and intervention for balance disorders is enhancing demand for diagnostic imaging and vestibular testing technologies. Government-supported healthcare systems and ongoing medical research into inner ear inflammation and autoimmune labyrinthitis are fostering innovation. The region is witnessing increased adoption of vestibular rehabilitation therapies and digital balance training platforms across both clinical and home settings.

U.K. Labyrinthitis Market Insight

The U.K. labyrinthitis market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by NHS-driven initiatives for neurological health, rising awareness of hearing and balance issues, and the growing availability of vestibular rehabilitation services. Patients increasingly seek non-invasive treatments such as antiemetics, corticosteroids, and guided therapy exercises to manage vertigo and dizziness. The U.K.’s adoption of digital health tools, alongside strong ENT specialist networks, is expected to bolster the market, particularly in urban and aging populations where balance issues are more prevalent.

Germany Labyrinthitis Market Insight

The German labyrinthitis market is expected to expand at a considerable CAGR, driven by high public awareness, government support for neurotology care, and widespread access to cutting-edge diagnostic imaging. Germany’s emphasis on preventive healthcare, clinical accuracy, and sustainable pharmaceutical practices supports the use of corticosteroids and vestibular aids for managing labyrinthitis. In addition, ongoing academic research and innovation in autoimmune diagnostics and inner ear pathology contribute to Germany’s leading role in shaping the European vestibular disorder landscape.

Asia-Pacific Labyrinthitis Market Insight

The Asia-Pacific labyrinthitis market is poised to grow at the fastest CAGR of over 6.5% in 2025, fueled by rapid urbanization, increasing healthcare investments, and a growing burden of viral and bacterial infections leading to inner ear inflammation. Countries such as China, Japan, and India are witnessing improved access to ENT services and imaging tools, alongside growing awareness of balance and hearing health. Public health campaigns and government funding to improve rural healthcare are enabling earlier diagnosis and broader treatment outreach, contributing to rapid market acceleration.

Japan Labyrinthitis Market Insight

The Japan labyrinthitis market is gaining momentum due to the country’s aging population, high-tech healthcare infrastructure, and emphasis on precision diagnostics. Japan leads in the adoption of portable vestibular assessment tools and AI-integrated balance monitoring systems, supporting early-stage diagnosis and remote care for vestibular conditions. Cultural emphasis on elderly wellness and fall prevention is boosting the adoption of customized rehabilitation therapies, positioning Japan as a key market for innovative vestibular treatment solutions.

China Labyrinthitis Market Insight

The China labyrinthitis market accounted for the largest revenue share in Asia-Pacific in 2025, driven by an increasing number of upper respiratory infections, rapid expansion of ENT healthcare facilities, and strong domestic production of pharmaceutical and diagnostic tools. China’s growing middle class and urban healthcare reforms are supporting better access to corticosteroids, antibiotics, and vestibular therapies. The government's push toward digital health and rural outreach programs is also encouraging early diagnosis and treatment in previously underserved regions, further propelling the market.

Labyrinthitis Market Share

The Labyrinthitis industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Sanofi S.A. (France)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Mylan N.V. (U.S.) (Note: now merged with Upjohn to form Viatris)

- Eli Lilly and Company (U.S.)

- Sun Pharmaceutical Industries Ltd. (India)

- Shandong Taihua Bio & Tech Co. (China)

- Cipla Inc. (India)

- F. Hoffmann-La Roche (Switzerland)

- GlaxoSmithKline plc (UK)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AstraZeneca (UK)

- Intas Pharmaceutical Ltd. (India)

- Dr. Reddy’s Laboratories (India

- Abbott (U.S.)

- Sound Pharmaceutical (U.S.)

- Amneal Pharmaceuticals (U.S.)

- Nicholas Piramal (India) (now part of Piramal Enterprises)

- Solvay (Belgium)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.