Global Laser Defense Eyewear Market

Market Size in USD Billion

USD

1.09 Billion

USD

1.61 Billion

2025

2033

USD

1.09 Billion

USD

1.61 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.09 Billion | |

| USD 1.61 Billion | |

| % | |

|

Laser Defense Eyewear Market Size

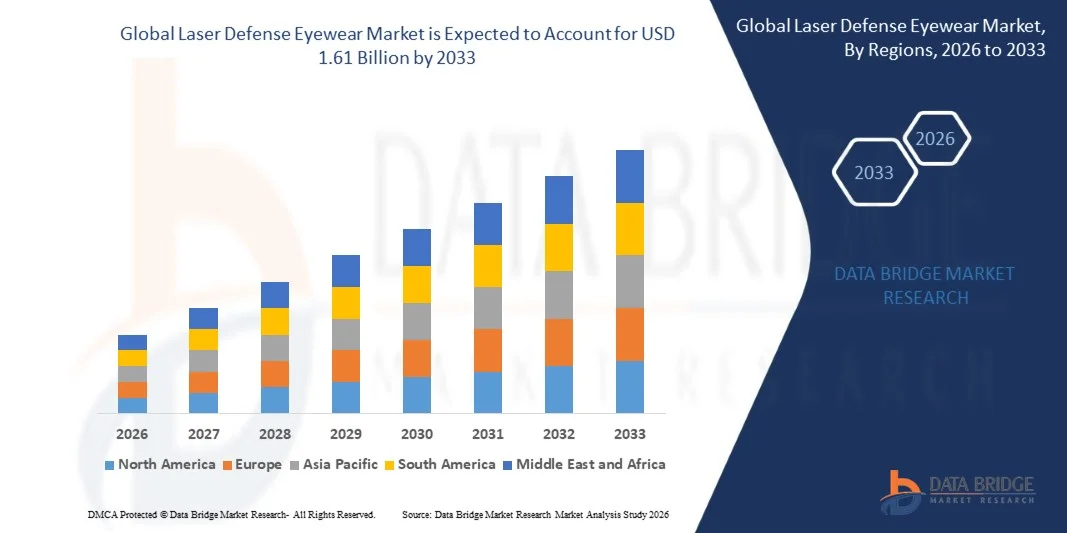

- The global laser defense eyewear market size was valued at USD 1.09 billion in 2025 and is expected to reach USD 1.61 billion by 2033, at a CAGR of 5.00% during the forecast period

- The market growth is largely fuelled by the rising adoption of advanced protective eyewear in military and defense operations to safeguard personnel from high-powered laser threats

- Increasing use of laser technology in defense applications, such as targeting systems, rangefinders, and directed energy weapons, is driving demand for specialized eyewear that ensures operational safety and visual clarity

Laser Defense Eyewear Market Analysis

- Laser defense eyewear is becoming an essential component of personal protective equipment for military, law enforcement, and security personnel, designed to prevent eye injuries from accidental or targeted laser exposure

- Technological advancements, including lightweight materials, anti-glare coatings, and adjustable lens systems, are enhancing the functionality, comfort, and usability of protective eyewear

- North America dominated the laser defense eyewear market with the largest revenue share in 2025, driven by rising adoption of advanced protective eyewear in military, law enforcement, and aviation applications, as well as increasing awareness about laser hazards.

- Asia-Pacific region is expected to witness the highest growth rate in the global laser defense eyewear market, driven by rapid urbanization, expansion of defense and aviation sectors, rising adoption of laser technologies, and increasing government initiatives promoting personnel safety and protective equipment standards

- The Wraparound Style segment held the largest market revenue share in 2025, driven by its wide coverage, lightweight design, and ability to protect eyes from multiple angles. These eyewear types provide effective shielding against direct and reflected laser beams while maintaining clear visibility for tactical operations. Wraparound eyewear is extensively used by armed forces and law enforcement during field missions, training exercises, and high-risk scenarios, ensuring both safety and operational efficiency. Its ergonomic design also enhances comfort for prolonged usage, making it a preferred choice among professionals

Report Scope and Laser Defense Eyewear Market Segmentation

|

Attributes |

Laser Defense Eyewear Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• GENTEX CORPORATION (U.S.) |

|

Market Opportunities |

• Rising Adoption Of Advanced Protective Eyewear In Defense Operations |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Laser Defense Eyewear Market Trends

“Rising Demand for Advanced Eye Protection in Military and Security Applications”

• Growing focus on safeguarding personnel from high-intensity laser threats is significantly shaping the laser defense eyewear market, as defense and security organizations increasingly prefer eyewear that offers reliable protection without compromising visual clarity. Laser defense eyewear is gaining traction due to its ability to filter harmful laser wavelengths while maintaining operational visibility, strengthening adoption across military, law enforcement, and security sectors

• Increasing awareness about eye safety, occupational hazards, and advanced defense technologies has accelerated demand for laser defense eyewear in combat operations, tactical training, and high-risk environments. Organizations are actively seeking eyewear that meets strict safety standards, prompting manufacturers to innovate with advanced coatings, lightweight materials, and adjustable lens systems

• Trends toward enhanced situational awareness and operational efficiency are influencing procurement decisions, with agencies emphasizing certifications, durability, and ergonomic design. These factors help organizations differentiate product offerings, build trust, and ensure compliance with safety regulations. Companies are increasingly using marketing campaigns and demonstrations to highlight protective benefits and reinforce brand positioning among security-conscious buyers

• For instance, in 2024, Gentex Corporation in the U.S. and Revision Military in Canada expanded their portfolios by incorporating advanced laser filtering technologies in protective eyewear for military personnel. The products were introduced in response to growing concerns over laser hazards in training and combat scenarios, with distribution across defense contractors, specialized retailers, and direct government supply channels

• While demand for laser defense eyewear is growing, sustained market expansion depends on continuous R&D, cost-effective production, and maintaining functional performance under varying operational conditions. Manufacturers are focusing on improving scalability, supply chain reliability, and developing innovative solutions that balance protection, comfort, and affordability for broader adoption

Laser Defense Eyewear Market Dynamics

Driver

“Rising Need for Eye Protection Against Laser Threats”

• Growing adoption of laser-based devices and directed energy weapons in military, aviation, and security operations is a major driver for the laser defense eyewear market. Organizations are increasingly seeking protective solutions to prevent eye injuries while maintaining operational effectiveness, encouraging innovation in eyewear technologies

• Expanding applications in defense, law enforcement, industrial safety, and research laboratories are influencing market growth. Laser defense eyewear helps personnel maintain visibility and situational awareness while providing protection against a variety of laser wavelengths, supporting operational efficiency

• Manufacturers are actively promoting laser defense eyewear through product innovation, compliance certifications, and demonstrations for tactical applications. These efforts are supported by rising awareness of occupational hazards and the increasing integration of laser technologies in security and defense systems

• For instance, in 2023, companies such as Oakley SI in the U.S. and Wiley X in Germany reported increased adoption of laser protective eyewear across military and law enforcement units. These initiatives followed heightened awareness of laser threats and compliance requirements, driving repeat procurement and product differentiation

• Although rising laser threats support market growth, wider adoption depends on cost optimization, standardization of protective performance, and regulatory compliance. Investment in advanced materials, lens coatings, and ergonomic design will be critical for meeting global demand and maintaining competitive advantage

Restraint/Challenge

“High Cost And Limited Awareness Compared To Conventional Protective Eyewear”

• The relatively higher cost of laser defense eyewear compared to standard protective glasses remains a key challenge, limiting adoption among budget-conscious organizations. Advanced materials, complex lens technologies, and testing requirements contribute to elevated pricing

• Awareness of functional benefits and laser-specific hazards remains uneven, particularly in emerging markets and smaller defense agencies. Limited understanding of laser protection requirements restricts adoption across certain operational environments

• Supply chain and distribution challenges also impact market growth, as laser defense eyewear requires sourcing from certified suppliers and adherence to stringent quality standards. Logistical complexities, including specialized storage and handling requirements, increase operational costs

• For instance, in 2024, distributors in Southeast Asia supplying military and security units reported slower uptake due to high pricing and limited knowledge about laser hazard mitigation. Compliance with international protective standards and certification requirements further constrained market penetration

• Overcoming these challenges will require cost-efficient production, expanded distribution networks, and focused educational initiatives for end-users and procurement officers. Collaboration with defense organizations, certification bodies, and manufacturers can help unlock long-term growth potential. Developing cost-competitive solutions with demonstrable protective performance will be essential for widespread adoption of laser defense eyewear globally

Laser Defense Eyewear Market Scope

The market is segmented on the basis of product type, type, application, and end user.

• By Product Type

On the basis of product type, the laser defense eyewear market is segmented into Wraparound Style, Goggle Style, and Over Spectacles Style. The Wraparound Style segment held the largest market revenue share in 2025, driven by its wide coverage, lightweight design, and ability to protect eyes from multiple angles. These eyewear types provide effective shielding against direct and reflected laser beams while maintaining clear visibility for tactical operations. Wraparound eyewear is extensively used by armed forces and law enforcement during field missions, training exercises, and high-risk scenarios, ensuring both safety and operational efficiency. Its ergonomic design also enhances comfort for prolonged usage, making it a preferred choice among professionals.

The Goggle Style segment is expected to witness the fastest growth rate from 2026 to 2033, driven by superior sealing, fog resistance, and adaptability for extreme conditions. Goggle-style eyewear offers enhanced protection in high-intensity operations such as combat exercises, aviation missions, and industrial security environments. Its robust design and customizable lenses provide reliable defense against multiple laser wavelengths, while maintaining optical clarity. The increasing adoption of goggle-style eyewear in specialized applications is anticipated to drive growth, particularly in regions with heightened security and defense initiatives.

• By Type

On the basis of type, the laser defense eyewear market is segmented into Reusable and Disposable. The Reusable segment held the largest market revenue share in 2025, attributed to its long-term cost-effectiveness, durability, and ability to withstand repeated use. Reusable eyewear is preferred by military personnel, pilots, and law enforcement for extended missions, training, and combat operations. The segment’s growth is supported by the availability of high-quality materials, anti-glare coatings, and adjustable lenses that maintain protection over long periods. Increasing investments in advanced eyewear technologies further reinforce its market dominance.

The Disposable segment is expected to witness the fastest growth rate from 2026 to 2033, driven by demand for cost-efficient solutions in temporary operations, training exercises, and emergency deployments. Disposable laser eyewear provides adequate protection without long-term maintenance, ensuring safety during short-term assignments or high-turnover scenarios. Its convenience, ease of use, and adherence to safety standards make it an attractive option for organizations with budget constraints or dynamic operational needs. Growth in this segment is further supported by rising awareness of laser hazards in emerging markets.

• By Application

On the basis of application, the laser defense eyewear market is segmented into Pilots, Law Enforcement, and Transportation Workers. The Pilots segment held the largest market revenue share in 2025, driven by increasing threats from laser targeting systems and laser pointers in aviation. Laser eyewear for pilots ensures eye safety while maintaining clear visibility and operational performance during flight. Technological advancements, such as lightweight frames and anti-reflective coatings, enhance user comfort and situational awareness. Adoption is further supported by regulatory mandates and safety protocols across commercial and defense aviation sectors.

The Law Enforcement segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the growing need for tactical operations, riot control, and counter-laser measures. Police and security personnel increasingly rely on laser defense eyewear to protect against potential hazards during field operations. The eyewear enhances mission safety without restricting mobility or communication, making it critical for modern security forces. Rising investments in public safety infrastructure and awareness about laser threats are accelerating market adoption.

• By End User

On the basis of end user, the laser defense eyewear market is segmented into Paramilitary Forces and Armed Troops. The Armed Troops segment held the largest market revenue share in 2025, driven by high adoption in combat and field operations requiring protection against laser-based weapons. Laser eyewear ensures operational readiness, visual clarity, and safety during intense military engagements. It is also incorporated into standard-issue personal protective equipment for modern armies worldwide.

The Paramilitary Forces segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by increased deployment for border security, counter-terrorism operations, and internal security tasks. These forces increasingly rely on laser defense eyewear to mitigate risks posed by laser threats while maintaining tactical efficiency. Rising investments in paramilitary modernization and safety training programs are expected to drive adoption further in emerging and developed markets alike.

Laser Defense Eyewear Market Regional Analysis

• North America dominated the laser defense eyewear market with the largest revenue share in 2025, driven by rising adoption of advanced protective eyewear in military, law enforcement, and aviation applications, as well as increasing awareness about laser hazards.

• Organizations in the region value high-quality protection, ergonomic designs, and multi-wavelength laser filtering capabilities, ensuring personnel safety during training, tactical operations, and combat scenarios.

• This widespread adoption is further supported by robust defense budgets, technologically advanced infrastructure, and government initiatives emphasizing eye safety, establishing laser defense eyewear as a standard protective solution across military and security operations.

U.S. Laser Defense Eyewear Market Insight

The U.S. laser defense eyewear market captured the largest revenue share in North America in 2025, fueled by the high adoption of advanced defense technologies and rising concerns about laser threats in military and aviation sectors. Organizations increasingly prioritize eye protection during field operations, pilot missions, and security deployments. The growing demand for reusable, multi-functional eyewear, along with integration into tactical gear and safety protocols, is driving market growth. Furthermore, awareness campaigns and procurement regulations emphasizing laser safety are significantly contributing to market expansion.

Europe Laser Defense Eyewear Market Insight

The Europe laser defense eyewear market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent occupational safety regulations and increasing deployment of laser technologies in defense and aviation. Rising urbanization, coupled with growing investments in public safety and security, is fostering the adoption of laser protective eyewear. European organizations are also prioritizing ergonomic and lightweight designs for prolonged use. The market is experiencing significant growth across military, law enforcement, and transportation applications, with eyewear integrated into both new procurement contracts and modernization programs.

U.K. Laser Defense Eyewear Market Insight

The U.K. laser defense eyewear market is expected to witness rapid growth from 2026 to 2033, driven by heightened security concerns, adoption of laser-based training systems, and a growing focus on occupational safety. Government and defense agencies are increasingly procuring advanced eyewear to protect personnel during operations and exercises. The U.K.’s well-developed defense infrastructure, along with strong awareness of laser hazards and integration with tactical gear, is expected to continue supporting market expansion.

Germany Laser Defense Eyewear Market Insight

The Germany laser defense eyewear market is projected to grow at a robust pace from 2026 to 2033, fueled by increasing awareness of digital and laser-related hazards and rising demand for advanced, sustainable protective solutions. Germany’s emphasis on technological innovation, infrastructure modernization, and safety compliance promotes adoption in military and law enforcement sectors. Laser eyewear integration with tactical and operational equipment is becoming more prevalent, meeting local requirements for high protection standards and operational efficiency.

Asia-Pacific Laser Defense Eyewear Market Insight

The Asia-Pacific laser defense eyewear market is expected to witness the fastest growth rate from 2026 to 2033, driven by rising defense modernization, urbanization, and adoption of advanced laser technologies in countries such as China, Japan, and India. Growing awareness of eye safety in aviation, law enforcement, and paramilitary operations is supporting market expansion. In addition, government initiatives promoting protective equipment standards and the presence of emerging eyewear manufacturers are enhancing accessibility and affordability for a wider user base.

Japan Laser Defense Eyewear Market Insight

The Japan laser defense eyewear market is expected to grow rapidly from 2026 to 2033 due to the country’s technologically advanced defense and aviation sectors, high safety standards, and increasing use of laser-based equipment. The adoption is supported by the growing number of training facilities, connected operational systems, and aging workforce requirements for user-friendly protective eyewear. Integration with other tactical and operational gear enhances safety while maintaining visibility and performance in field and aerial applications.

China Laser Defense Eyewear Market Insight

The China laser defense eyewear market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, growing defense budgets, and increased adoption of laser technologies across military and transportation sectors. The country’s strong domestic manufacturing base, combined with government support for protective equipment standards, is facilitating widespread adoption. Rising awareness of laser hazards, expansion of paramilitary and aviation operations, and availability of cost-effective eyewear solutions are key factors propelling the market in China.

Laser Defense Eyewear Market Share

The Laser Defense Eyewear industry is primarily led by well-established companies, including:

• GENTEX CORPORATION (U.S.)

• Honeywell International Inc. (U.S.)

• Metamaterial Inc. (Canada)

• NoIR LaserShields (U.S.)

• Revision Military (Canada)

• Kentek Corporation (U.S.)

• RX Safety (U.S.)

• Univet S.r.l. (Italy)

• Global Laser Ltd (U.K.)

• uvex group (Germany)

• Thorlabs, Inc. (U.S.)

• 3M (U.S.)

• MCR Safety (U.S.)

• Bolle Safety (France)

• Stanley Black & Decker, Inc. (U.S.)

• Gateway Safety, Inc. (U.S.)

• PERRIQUEST DEFENSE RESEARCH ENTERPRISES, LLC (U.S.)

• ESS (U.S.)

• Laser Safety Industries (U.S.)

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.