Global Lead Acid Ev Vehicle Market

Market Size in USD Billion

USD

6.63 Billion

USD

21.14 Billion

2025

2033

USD

6.63 Billion

USD

21.14 Billion

2025

2033

| 2026 - 2033 | |

| USD 6.63 Billion | |

| USD 21.14 Billion | |

| % | |

|

Lead Acid EV Vehicle Market Overview

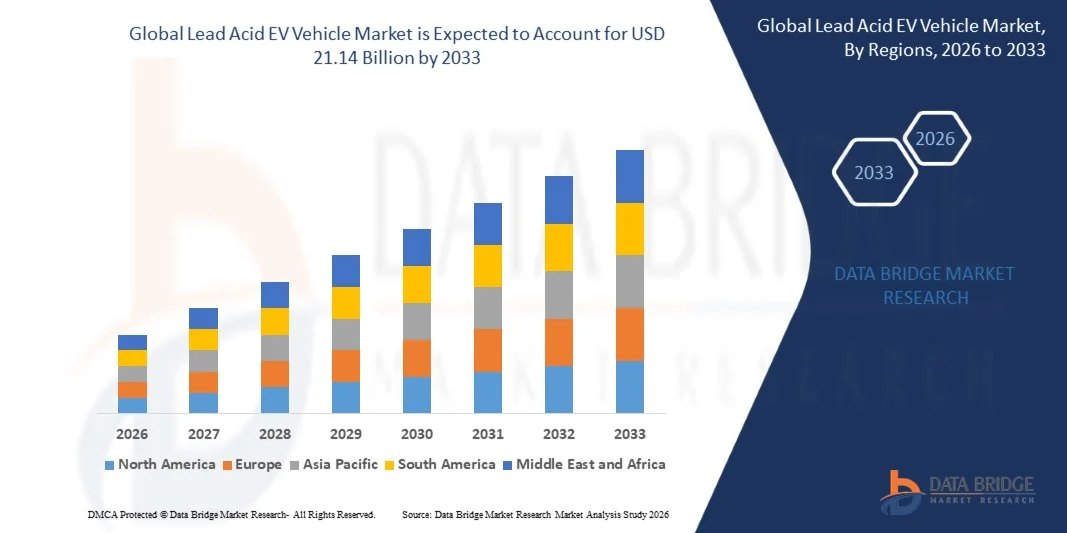

The Lead Acid EV Vehicle Market was valued at USD 6.63 billion in 2025 and is projected to reach USD 21.14 billion by 2033, growing at a CAGR of 15.60% from 2026 to 2033. The market is witnessing substantial growth driven by increasing adoption of low-speed electric vehicles, expanding demand for affordable energy storage solutions, and rising government initiatives promoting electric mobility across emerging economies. Lead acid batteries continue to play a significant role in electric two-wheelers, e-rickshaws, golf carts, neighbourhood electric vehicles, and industrial electric transportation due to their cost-effectiveness and established recycling infrastructure.

The growing emphasis on reducing transportation-related emissions, coupled with rising fuel prices and increasing urbanization, is encouraging consumers and fleet operators to transition toward electric mobility solutions powered by lead acid batteries. In many developing regions, lead acid battery-powered EVs remain a preferred option because of their lower upfront costs and widespread availability of replacement and maintenance services. In addition, advancements in enhanced flooded batteries and valve-regulated lead acid technologies are improving battery durability, charging performance, and operational reliability, supporting continued adoption across commercial and personal electric vehicle applications.

Key Market Trends & Insights

- North America dominated the lead acid EV vehicle market with the largest revenue share of approximately 35.8% in 2025, supported by strong adoption of industrial electric vehicles, golf carts, utility transportation systems, established battery recycling infrastructure, and growing investments in sustainable transportation solutions.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 17.2% from 2026 to 2033. Growth is driven by rapid urbanization, increasing demand for affordable electric transportation, rising adoption of electric three-wheelers and e-rickshaws, and strong government support for electric mobility across countries such as China, India, and Bangladesh.

- The Positive Electrode segment held the largest market revenue share of approximately 34.6% in 2025 driven by its critical role in determining battery capacity, discharge performance, and overall energy storage efficiency. Continuous advancements in lead dioxide active materials and electrode manufacturing technologies are supporting segment dominance across electric three-wheelers and low-speed electric vehicles.

- The Separator segment is projected to register the fastest growth at a CAGR of 17.1% from 2026 to 2033, driven by increasing adoption of advanced AGM and gel battery technologies requiring high-performance separators to improve battery life, safety, and charging efficiency. Growing investments in battery performance enhancement are accelerating segment expansion.

- The Battery Electric Vehicle segment held the largest market revenue share of approximately 71.8% in 2025 driven by extensive deployment of lead acid batteries in electric rickshaws, neighborhood electric vehicles, golf carts, and industrial utility vehicles. The affordability and widespread availability of lead acid batteries continue to support adoption in cost-sensitive markets.

- The Plug-in Hybrid Electric Vehicle segment is projected to register the fastest growth at a CAGR of 16.4% from 2026 to 2033, driven by increasing demand for auxiliary energy storage systems and rising adoption of hybrid mobility solutions in developing economies. Growing emphasis on fuel efficiency and emission reduction is supporting segment growth.

- The Wire Bonding segment held the largest market revenue share of approximately 67.5% in 2025 driven by its cost-effectiveness, established manufacturing processes, and widespread use in lead acid battery assembly operations. The method remains highly preferred for large-scale production due to its operational reliability and lower implementation costs.

- The Laser Bonding segment is projected to register the fastest growth at a CAGR of 18.2% from 2026 to 2033, driven by increasing demand for precision manufacturing, improved electrical conductivity, and enhanced battery durability. Advancements in automated battery production technologies are encouraging adoption of laser bonding techniques.

- The <50 kWh segment held the largest market revenue share of approximately 58.9% in 2025 driven by its extensive utilization in electric two-wheelers, e-rickshaws, golf carts, and neighborhood electric vehicles. These applications prioritize affordability and shorter-range transportation requirements.

- The 50-110 kWh segment is projected to register the fastest growth at a CAGR of 16.9% from 2026 to 2033, supported by increasing adoption of commercial electric vehicles and utility transportation systems requiring greater energy storage capacity and longer operating durations.

- The Commercial Vehicle segment held the largest market revenue share of approximately 46.7% in 2025 driven by widespread deployment of lead acid battery-powered e-rickshaws, logistics vehicles, industrial transport units, and fleet mobility solutions across emerging economies. Strong demand for cost-effective commercial transportation continues to support segment leadership.

- The Two Wheeler segment is projected to register the fastest growth at a CAGR of 17.5% from 2026 to 2033, driven by increasing urban mobility demand, rising fuel costs, and growing adoption of affordable electric scooters and motorcycles in Asia-Pacific and Africa. Government incentives supporting electric two-wheeler adoption are further accelerating segment expansion.

Market Size & Forecast

- Global Market Value (2025): USD 6.63 Billion

- Expected Market Value (2033): USD 21.14 Billion

- Forecast CAGR (2026–2033): 15.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Lead Acid EV Vehicle Market Segmentation

|

Attributes |

Lead Acid EV Vehicle Key Market Insights |

|

Segments Covered |

· By Component: Positive Electrode, Negative Electrode, Electrolyte, and Separator · By Propulsion Type: Battery Electric Vehicle, Hybrid Electric Vehicle, and Plug-in Hybrid Electric Vehicle · By Method: Wire Bonding and Laser Bonding · By Battery Capacity: <50 kWh, 50-110 kWh, 111-200 kWh, 201-300 kWh, and >300 kWh · By Vehicle Type: Passenger Car, Commercial Vehicle, and Two Wheeler |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Johnson Controls (U.S.) |

|

Market Opportunities |

• Expansion Of Electric Three-Wheeler And Low-Speed Electric Vehicle Adoption • Advancements In Advanced Lead Acid Battery Technologies And Recycling Infrastructure Development |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Lead Acid EV Vehicle Market Trends

Trend: Rising Adoption Of Affordable Electric Mobility And Advanced Lead Acid Battery Technologies

Increasing demand for cost-effective electric transportation solutions across emerging economies is driving the adoption of lead acid battery-powered electric vehicles. While lithium-ion batteries continue to gain popularity in premium EV segments, lead acid batteries remain widely utilized in electric three-wheelers, low-speed electric vehicles, neighborhood electric vehicles, golf carts, and industrial mobility applications due to their affordability, established supply chains, and extensive recycling infrastructure.

In developing countries, manufacturers are increasingly integrating advanced valve-regulated lead acid (VRLA) and enhanced flooded batteries into electric vehicles to improve durability, reliability, and charging performance while maintaining low ownership costs. For instance, electric rickshaw fleets across India and Bangladesh continue to rely heavily on lead acid battery systems because of lower upfront costs and readily available maintenance networks. In industrial environments, lead acid-powered utility vehicles are widely deployed in warehouses, manufacturing facilities, and airports for material handling and internal transportation operations.

The rapid expansion of urban mobility solutions and last-mile transportation services is further increasing demand for affordable EV platforms powered by lead acid batteries. In addition, advancements in battery recycling technologies are supporting sustainable market growth, with global lead acid battery recycling rates exceeding 95% in several developed markets. Industry developments during 2025 involving next-generation lead carbon battery deployments in commercial electric vehicles demonstrated cycle life improvements of approximately 30–40% compared to conventional flooded lead acid battery systems.

Lead Acid EV Vehicle Market Dynamics

Key Market Driver: Growing Demand For Cost-Effective Electric Transportation Solutions

Governments and consumers worldwide are increasingly focusing on reducing transportation emissions while maintaining affordability, creating strong demand for low-cost electric mobility solutions. Lead acid battery-powered electric vehicles offer significantly lower acquisition costs compared to lithium-ion alternatives, making them attractive for commercial operators and price-sensitive consumers in developing economies.

Electric three-wheelers, e-rickshaws, and low-speed electric vehicles are increasingly being adopted across Asia-Pacific, Latin America, and Africa to provide economical urban transportation services. For instance, India continues to operate millions of electric rickshaws powered primarily by lead acid batteries, supporting affordable public transportation and employment generation. Vehicle manufacturers are also leveraging mature lead acid battery supply chains to reduce production costs and improve accessibility for first-time EV buyers.

Similarly, industrial and logistics sectors are deploying lead acid battery-powered utility vehicles for warehousing and material handling operations where low operating costs and ease of maintenance remain critical considerations. Commercial fleet deployments across Southeast Asia during 2024 reported operating cost reductions of approximately 20–25% compared to conventional fuel-powered alternatives in short-distance transportation applications.

Key Restraint/Challenge: Limited Energy Density And Shorter Operational Life Compared To Lithium-Ion Batteries

Despite widespread adoption, lead acid batteries face significant performance limitations that restrict their competitiveness in advanced electric vehicle applications. Their lower energy density results in shorter driving ranges and increased battery weight, making them less suitable for high-performance passenger electric vehicles and long-distance transportation requirements.

In addition, lead acid batteries typically require more frequent replacement than lithium-ion systems, increasing long-term ownership costs despite lower initial purchase prices. Charging times remain relatively longer, while repeated deep discharge cycles can accelerate battery degradation and reduce operational efficiency. These limitations are encouraging many automotive manufacturers to gradually transition toward lithium-ion technologies for mainstream EV platforms.

Industry benchmarking studies indicate that conventional lead acid batteries generally provide energy densities of around 30–50 Wh/kg, significantly lower than lithium-ion battery systems that commonly exceed 150–250 Wh/kg. The comparatively lower energy storage capability continues to restrict adoption in premium and high-range electric vehicle segments.

Key Market Opportunity: Expansion Of Electric Three-Wheelers And Advanced Lead Carbon Battery Technologies

The growing adoption of electric three-wheelers, neighborhood electric vehicles, and commercial fleet transportation is creating substantial opportunities for lead acid battery manufacturers. These vehicle categories prioritize affordability, ease of maintenance, and reliable performance over long-range capabilities, making lead acid technologies a practical solution for many operators.

Manufacturers are increasingly investing in advanced lead carbon battery technologies, For instance for electric rickshaws, utility vehicles, and light commercial EVs, to improve charge acceptance, extend cycle life, and enhance overall vehicle performance. In urban transportation markets, fleet operators are adopting improved lead acid battery systems to reduce replacement frequency and lower operating expenses while maintaining cost competitiveness.

In addition, ongoing advancements in battery recycling infrastructure and circular economy initiatives are strengthening the sustainability profile of lead acid batteries, creating opportunities across emerging EV markets in Asia-Pacific, Africa, and Latin America. Pilot deployments of lead carbon battery-powered commercial electric vehicles conducted during 2025 demonstrated cycle life improvements of approximately 40–60% and charging efficiency gains of nearly 15–20% compared to traditional lead acid battery configurations.

Lead Acid EV Vehicle Market Scope

The market is segmented on the basis of component, propulsion type, method, battery capacity, and vehicle type.

- By Component

On the basis of component, the lead acid EV vehicle market is segmented into Positive Electrode, Negative Electrode, Electrolyte, and Separator. The Positive Electrode segment held the largest market revenue share of approximately 34.6% in 2025 driven by its critical role in determining battery capacity, discharge performance, and overall energy storage efficiency. Continuous advancements in lead dioxide active materials and electrode manufacturing technologies are supporting segment dominance across electric three-wheelers and low-speed electric vehicles.

The Separator segment is projected to register the fastest growth at a CAGR of 17.1% from 2026 to 2033, driven by increasing adoption of advanced AGM and gel battery technologies requiring high-performance separators to improve battery life, safety, and charging efficiency. Growing investments in battery performance enhancement are accelerating segment expansion.

- By Propulsion Type

On the basis of propulsion type, the market is segmented into Battery Electric Vehicle, Hybrid Electric Vehicle, and Plug-in Hybrid Electric Vehicle. The Battery Electric Vehicle segment held the largest market revenue share of approximately 71.8% in 2025 driven by extensive deployment of lead acid batteries in electric rickshaws, neighborhood electric vehicles, golf carts, and industrial utility vehicles. The affordability and widespread availability of lead acid batteries continue to support adoption in cost-sensitive markets.

The Plug-in Hybrid Electric Vehicle segment is projected to register the fastest growth at a CAGR of 16.4% from 2026 to 2033, driven by increasing demand for auxiliary energy storage systems and rising adoption of hybrid mobility solutions in developing economies. Growing emphasis on fuel efficiency and emission reduction is supporting segment growth.

- By Method

On the basis of method, the market is segmented into Wire Bonding and Laser Bonding. The Wire Bonding segment held the largest market revenue share of approximately 67.5% in 2025 driven by its cost-effectiveness, established manufacturing processes, and widespread use in lead acid battery assembly operations. The method remains highly preferred for large-scale production due to its operational reliability and lower implementation costs.

The Laser Bonding segment is projected to register the fastest growth at a CAGR of 18.2% from 2026 to 2033, driven by increasing demand for precision manufacturing, improved electrical conductivity, and enhanced battery durability. Advancements in automated battery production technologies are encouraging adoption of laser bonding techniques.

- By Battery Capacity

On the basis of battery capacity, the market is segmented into <50 kWh, 50-110 kWh, 111-200 kWh, 201-300 kWh, and >300 kWh. The <50 kWh segment held the largest market revenue share of approximately 58.9% in 2025 driven by its extensive utilization in electric two-wheelers, e-rickshaws, golf carts, and neighborhood electric vehicles. These applications prioritize affordability and shorter-range transportation requirements.

The 50-110 kWh segment is projected to register the fastest growth at a CAGR of 16.9% from 2026 to 2033, supported by increasing adoption of commercial electric vehicles and utility transportation systems requiring greater energy storage capacity and longer operating durations.

- By Vehicle Type

On the basis of vehicle type, the market is segmented into Passenger Car, Commercial Vehicle, and Two Wheeler. The Commercial Vehicle segment held the largest market revenue share of approximately 46.7% in 2025 driven by widespread deployment of lead acid battery-powered e-rickshaws, logistics vehicles, industrial transport units, and fleet mobility solutions across emerging economies. Strong demand for cost-effective commercial transportation continues to support segment leadership.

The Two Wheeler segment is projected to register the fastest growth at a CAGR of 17.5% from 2026 to 2033, driven by increasing urban mobility demand, rising fuel costs, and growing adoption of affordable electric scooters and motorcycles in Asia-Pacific and Africa. Government incentives supporting electric two-wheeler adoption are further accelerating segment expansion.

Lead Acid EV Vehicle Market Regional Analysis

North America Lead Acid EV Vehicle Market Insight

North America dominated the lead acid EV vehicle market with the largest revenue share of 35.8% in 2025, supported by increasing adoption of industrial electric vehicles, golf carts, neighborhood electric vehicles, and utility transportation systems. The region benefits from a well-established lead acid battery recycling infrastructure, strong aftermarket support networks, and growing investments in sustainable transportation solutions. Rising demand for cost-effective electric mobility options across commercial and industrial applications continues to support the widespread adoption of lead acid battery-powered vehicles throughout the region.

U.S. Lead Acid EV Vehicle Market Insight

The U.S. lead acid EV vehicle market captured the largest revenue share in 2025 within North America, driven by growing deployment of electric utility vehicles, warehouse transportation fleets, golf carts, and low-speed electric vehicles. Businesses are increasingly focusing on reducing operating costs through electrification while utilizing the mature lead acid battery ecosystem available across the country. The presence of established battery manufacturers, advanced recycling capabilities, and widespread charging infrastructure further supports market expansion. In addition, growing demand from logistics, manufacturing, and commercial sectors continues to stimulate adoption.

Europe Lead Acid EV Vehicle Market Insight

The Europe lead acid EV vehicle market is expected to witness significant growth from 2026 to 2033, primarily driven by increasing emphasis on sustainable transportation, circular economy initiatives, and advanced battery recycling programs. The region’s strong environmental regulations are encouraging adoption of recyclable battery technologies across low-speed electric vehicles and industrial transportation applications. Growing demand for affordable electric mobility solutions in urban environments, combined with increasing investments in battery manufacturing and recycling facilities, is supporting regional market expansion.

U.K. Lead Acid EV Vehicle Market Insight

The U.K. lead acid EV vehicle market is expected to witness strong growth from 2026 to 2033, driven by increasing adoption of electric utility vehicles, warehouse mobility solutions, and commercial fleet electrification initiatives. Businesses are increasingly seeking cost-effective electric transportation alternatives to meet sustainability goals and reduce operational expenses. The country's established logistics sector, expanding e-commerce industry, and growing investments in green transportation infrastructure are expected to continue supporting market development.

Germany Lead Acid EV Vehicle Market Insight

The Germany lead acid EV vehicle market is expected to witness strong growth from 2026 to 2033, fueled by rising industrial automation, growing adoption of electric material handling equipment, and strong focus on sustainable mobility solutions. Germany’s advanced manufacturing sector continues to deploy lead acid battery-powered industrial vehicles due to their reliability, affordability, and established maintenance ecosystem. Furthermore, the country's leadership in battery recycling and environmental sustainability initiatives is contributing to continued market expansion across commercial and industrial applications.

Asia-Pacific Lead Acid EV Vehicle Market Insight

The Asia-Pacific lead acid EV vehicle market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, increasing demand for affordable electric transportation, and rising government initiatives promoting clean mobility. Countries such as China, India, Bangladesh, and Indonesia are witnessing significant adoption of electric three-wheelers, e-rickshaws, and low-speed electric vehicles powered by lead acid batteries. The region also benefits from large-scale battery manufacturing capabilities and extensive distribution networks, improving product affordability and accessibility for a broader consumer base.

Japan Lead Acid EV Vehicle Market Insight

The Japan lead acid EV vehicle market is expected to witness notable growth from 2026 to 2033 due to increasing demand for compact electric mobility solutions, industrial electric vehicles, and environmentally sustainable transportation systems. The Japanese market places strong emphasis on reliability, safety, and operational efficiency, supporting continued adoption of advanced lead acid battery technologies in utility vehicles and commercial transportation fleets. In addition, growing investments in battery recycling and energy storage innovation are further contributing to market growth.

China Lead Acid EV Vehicle Market Insight

The China lead acid EV vehicle market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s large electric three-wheeler fleet, expanding urban transportation networks, and extensive domestic battery manufacturing industry. China remains one of the largest markets for affordable electric mobility solutions, with lead acid battery-powered vehicles widely utilized in commercial transportation, logistics, and short-distance urban mobility applications. Strong government support for electric mobility, combined with the presence of major battery manufacturers and efficient recycling infrastructure, continues to drive market growth across the country.

Lead Acid EV Vehicle Market Share

The Lead Acid EV Vehicle industry is primarily led by well-established companies, including:

• Johnson Controls (U.S.)

• Exide Technologies (U.S.)

• GS Yuasa International Ltd. (Japan)

• Middle East Battery Company (Saudi Arabia)

• Reem Batteries & Power Appliances Co. SAOC (Oman)

• EnerSys (U.S.)

• Saft (France)

• NorthStar (Sweden)

• C&D Technologies (U.S.)

• Robert Bosch GmbH (Germany)

• East Penn Manufacturing Company (U.S.)

• Panasonic Corporation (Japan)

• Trojan Battery Company (U.S.)

• Samsung SDI Co., Ltd. (South Korea)

• Leoch Battery Corporation (China)

• Exide Industries Ltd. (India)

• Century Batteries Indonesia (Indonesia)

• Tai Mao Battery Co., Ltd. (Taiwan)

• Infocom Network Limited (Bangladesh)

• Hitachi Chemical Energy Technology Co. Ltd. (Japan)

Latest Developments in Lead Acid EV Vehicle Market

- In February 2026, Exide Industries Ltd., Capacity Expansion, announced plans to enhance its lead-acid battery manufacturing capabilities for electric three-wheelers and commercial EV applications. The initiative is intended to strengthen domestic supply, improve production efficiency, and support growing demand for affordable electric mobility solutions, reinforcing market growth across emerging economies.

- In May 2025, Exide Industries Ltd., Strategic Investment, announced a major investment to expand lead-acid battery production capacity dedicated to electric vehicle applications. The expansion aims to improve battery availability for low-speed EVs and commercial fleets, reduce supply constraints, and strengthen the company’s position in the rapidly expanding electric mobility market.

- In October 2024, GS Yuasa International Ltd., Supply Agreement, entered into a long-term partnership with an electric vehicle manufacturer to supply lead-acid batteries for micro-electric vehicles in developing markets. The agreement is expected to enhance product accessibility, support cost-effective EV deployment, and sustain demand for lead-acid battery technology in entry-level electric transportation.

- In March 2024, EnerSys, Product Development, introduced an advanced lead-carbon battery solution designed for electric utility vehicles and fleet applications. The technology offers improved cycle life, faster charging capabilities, and enhanced operational reliability, supporting wider adoption of lead-acid battery systems in commercial mobility applications.

- In July 2023, East Penn Manufacturing Company, Manufacturing Expansion, expanded its battery production facilities to increase output of advanced lead-acid batteries for transportation and industrial electric vehicle markets. The development is expected to improve supply chain resilience, meet rising customer demand, and strengthen the company’s competitive position globally.

- In September 2022, GS Yuasa International Ltd., Technology Development, launched a next-generation valve-regulated lead-acid battery platform focused on electric mobility applications. The innovation was developed to improve battery durability, energy efficiency, and maintenance performance, helping expand the use of lead-acid batteries in cost-sensitive electric vehicle segments worldwide.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.