Global Legionellosis Market

Market Size in USD Billion

USD

1.70 Billion

USD

3.26 Billion

2025

2033

USD

1.70 Billion

USD

3.26 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.70 Billion | |

| USD 3.26 Billion | |

| % | |

|

Legionellosis Market Size

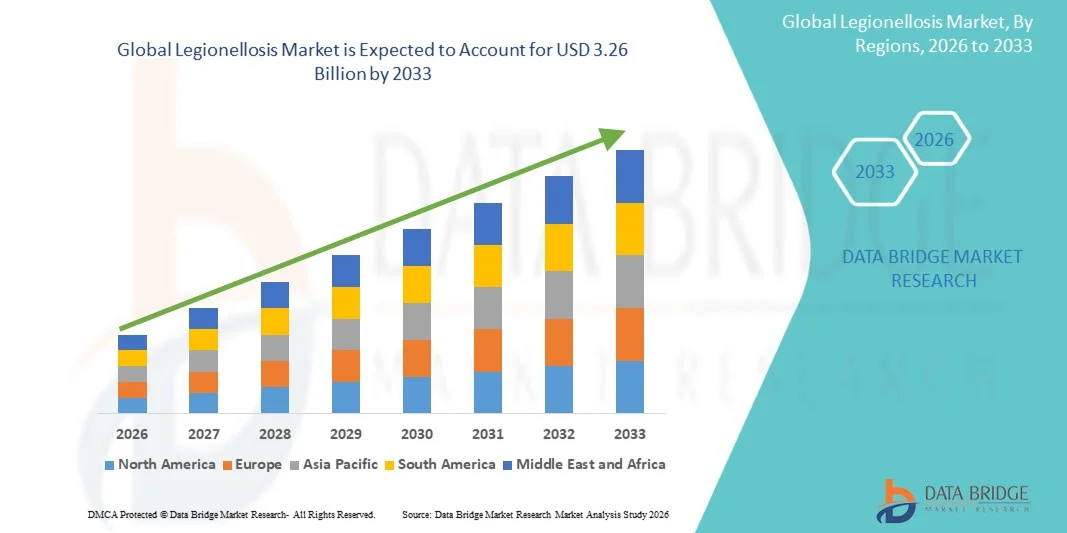

- The global Legionellosis market size was valued at USD 1.70 billion in 2025and is expected to reach USD 3.26 billion by 2033, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by increasing awareness of waterborne infectious diseases and advancements in diagnostic testing technologies, leading to earlier detection and improved clinical management of Legionellosis across hospitals, diagnostic laboratories, and public health systems. Rising investments in disease surveillance and water safety monitoring programs are further supporting market expansion

- Furthermore, growing demand for rapid diagnostic solutions, effective antibiotic therapies, and integrated water management systems for prevention and outbreak control is establishing Legionellosis solutions as critical components of modern infectious disease management. These converging factors are accelerating the uptake of Legionellosis diagnostics, treatment, and prevention solutions, thereby significantly boosting the industry's growth

Legionellosis Market Analysis

- Legionellosis, a serious bacterial infection caused by Legionella species and commonly associated with contaminated water systems, is increasingly recognized as an important segment within infectious disease management due to rising awareness of hospital-acquired infections, expanding environmental surveillance, and improved diagnostic testing capabilities

- The escalating demand for Legionellosis diagnostic and treatment solutions is primarily fueled by increasing incidence of waterborne disease outbreaks, aging populations vulnerable to respiratory infections, stricter water safety regulations, and growing adoption of rapid urinary antigen tests, PCR diagnostics, and targeted antibiotic therapies

- North America dominated the Legionellosis market with the largest revenue share of 38.40% in 2025, supported by advanced healthcare infrastructure, robust disease surveillance systems, high awareness of healthcare-associated infections, and widespread use of rapid diagnostic tools, with the U.S. witnessing substantial investments in prevention programs and outbreak monitoring

- Asia-Pacific is expected to be the fastest growing region in the Legionellosis market during the forecast period due to expanding urban infrastructure, increasing healthcare expenditure, rising awareness of water hygiene standards, and growing diagnostic access across countries such as China, India, Japan, and Australia

- The Medication segment accounted for the largest market revenue share of 71.6% in 2025, driven by standard clinical use of antibiotics such as azithromycin, levofloxacin, and other anti-infective therapies

Report Scope and Legionellosis Market Segmentation

|

Attributes |

Legionellosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · Merck & Co., Inc. (U.S.) · F. Hoffmann-La Roche Ltd. (Switzerland) · Abbott Laboratories (U.S.) · Thermo Fisher Scientific Inc. (U.S.) · bioMérieux SA (France) · Siemens Healthineers AG (Germany) · Danaher Corporation (Cepheid) (U.S.) · Becton, Dickinson and Company (BD) (U.S.) · Quest Diagnostics Incorporated (U.S.) · Laboratory Corporation of America Holdings (Labcorp) (U.S.) · Hologic, Inc. (U.S.) · Bio-Rad Laboratories, Inc. (U.S.) · Sysmex Corporation (Japan) · Takeda Pharmaceutical Company Limited (Japan) · Teva Pharmaceutical Industries Ltd. (Israel) · Sun Pharmaceutical Industries Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Viatris Inc. (U.S.) · Sanofi S.A. (France) |

|

Market Opportunities |

· Expansion of rapid diagnostic and point-of-care testing solutions · Growing demand for water safety monitoring and prevention systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Legionellosis Market Trends

“Advancements in Rapid Diagnostics and Water Safety Monitoring Solutions”

- A significant and accelerating trend in the global Legionellosis market is the growing adoption of rapid diagnostic technologies, environmental surveillance systems, and preventive water management solutions aimed at improving detection and outbreak control. These innovations are strengthening public health responses and reducing the burden of Legionnaires’ disease worldwide

- For instance, hospitals, hotels, and large commercial facilities are increasingly implementing rapid urinary antigen tests and routine water testing programs to detect Legionellosis cases early and monitor the presence of Legionella bacteria in cooling towers and plumbing systems

- Advances in PCR-based molecular diagnostics are enabling faster and more accurate identification of Legionella species compared with traditional culture methods, supporting timely clinical treatment decisions

- Smart water management systems with automated temperature control, disinfection monitoring, and remote alerts are gaining traction to reduce bacterial growth risks in complex building water systems

- Increasing collaboration between healthcare institutions, environmental agencies, and facility managers is improving outbreak prevention protocols and regulatory compliance standards

- This trend toward proactive surveillance, rapid diagnosis, and preventive infrastructure management is reshaping expectations for Legionellosis control globally

Legionellosis Market Dynamics

Driver

“Rising Incidence of Waterborne Outbreaks and Increasing Public Health Awareness”

- The increasing incidence of waterborne disease outbreaks and growing awareness regarding respiratory infections linked to contaminated water systems are major drivers supporting the growth of the Legionellosis market

- For instance, healthcare facilities and municipalities are expanding routine Legionella screening programs in hospitals, hotels, spas, and cooling tower systems following reported outbreaks in urban centers

- Aging infrastructure, complex plumbing systems, and rising urbanization are increasing the need for water safety monitoring and bacterial risk management solutions

- Governments and regulatory agencies are strengthening compliance requirements for water hygiene, testing, and maintenance in high-risk public and commercial buildings

- In addition, growing awareness among clinicians regarding atypical pneumonia and Legionnaires’ disease symptoms is supporting earlier diagnosis and treatment rates

Restraint/Challenge

“Underdiagnosis, High Monitoring Costs, and Complex Infrastructure Management”

- Underdiagnosis remains a major challenge in the Legionellosis market, as symptoms often resemble other forms of pneumonia, leading to missed or delayed detection in many patients

- For instance, in smaller healthcare facilities without rapid testing access, Legionnaires’ disease cases may initially be treated as generic bacterial pneumonia without confirming Legionella infection

- Continuous environmental testing, disinfection programs, and water system upgrades can be costly for hospitals, hotels, and industrial facilities managing large infrastructures

- Older buildings with complex piping networks and inconsistent maintenance schedules further complicate effective Legionella control efforts

- Addressing these challenges through wider diagnostic access, stronger maintenance protocols, and cost-effective monitoring technologies will be essential for sustained market growth

Legionellosis Market Scope

The market is segmented on the basis of type, diagnosis, treatment, route of administration, dosage form, end-users, and distribution channel.

- By Type

On the basis of type, the Legionellosis market is segmented into Pneumonic, Non-Pneumonic, and Others. The Pneumonic segment dominated the largest market revenue share of 67.8% in 2025, primarily due to the high incidence of Legionnaires’ disease, which represents the most severe and clinically significant form of legionellosis. This category requires immediate hospitalization and intensive treatment, driving strong healthcare spending. Increasing elderly population and immunocompromised individuals are highly vulnerable to pneumonic infections. Rising urbanization and aging water infrastructure are increasing outbreak risks globally. Hospitals are prioritizing early diagnosis and treatment of pneumonia-associated legionella infections. Demand for advanced antibiotics and respiratory support systems further boosts market value. Public health monitoring programs are also increasing case identification rates. Strong reimbursement availability in developed countries supports treatment uptake. Improved physician awareness has reduced underdiagnosis in recent years. Growing prevalence of chronic respiratory disorders also contributes to disease severity. These combined factors continue to strengthen dominance of the Pneumonic segment.

The Non-Pneumonic segment is expected to witness the fastest growth rate of 9.7% CAGR from 2026 to 2033, driven by increasing recognition of Pontiac fever and mild legionella-related illnesses across outpatient settings. Historically underreported cases are now being captured due to better screening awareness. Growing use of multiplex respiratory testing panels is supporting diagnosis of mild infections. Increased travel activity and hotel or cruise-related exposure incidents are contributing to demand. Rising awareness among physicians about flu-like legionella symptoms is improving reporting rates. Many patients prefer outpatient treatment, creating new market opportunities. Expanding healthcare access in emerging markets also supports segment growth. Public health agencies are investing more in waterborne disease surveillance. Availability of oral treatment options is enhancing management convenience. Shorter recovery periods improve patient compliance and diagnosis follow-up. Increasing preventive healthcare behavior further supports testing demand. These factors collectively position Non-Pneumonic cases as the fastest-growing segment.

- By Diagnosis

On the basis of diagnosis, the Legionellosis market is segmented into Blood and Urine Tests, Chest X-ray, Sputum and Lung Tissue, and Others. The Blood and Urine Tests segment held the largest market revenue share of 42.5% in 2025, driven by widespread use of urinary antigen tests for rapid and accurate detection of Legionella pneumophila infections. These tests are preferred because they provide fast results and help clinicians begin treatment early. Hospitals rely heavily on laboratory-based screening for pneumonia patients. Rising awareness of respiratory infection outbreaks is boosting testing volumes globally. Blood biomarkers also assist in evaluating severity and treatment response. Diagnostic laboratories are increasingly adopting automated testing platforms. Demand from emergency departments and ICU settings further strengthens segment growth. Improved insurance coverage for infectious disease diagnostics supports adoption. Rising geriatric population increases need for fast diagnosis. High sensitivity and convenience make urine tests highly preferred. These factors ensure continued leadership of Blood and Urine Tests.

The Sputum and Lung Tissue segment is expected to witness the fastest growth rate of 10.3% CAGR from 2026 to 2033, driven by increasing need for confirmatory diagnosis in severe or atypical pneumonia cases. PCR and culture testing from respiratory samples provide strain-specific results useful for treatment planning. Hospitals are increasingly using advanced respiratory pathogen panels. Growing concern regarding antibiotic resistance is boosting demand for precise pathogen identification. Public health agencies rely on sputum cultures for outbreak tracing and surveillance. Technological advances have improved speed and accuracy of molecular testing. Physicians use lung tissue tests in complicated or recurrent infections. Increasing severe pneumonia admissions globally support this segment. Research institutions are expanding respiratory infectious disease studies. Better laboratory infrastructure in emerging countries is also contributing growth. Rising clinical emphasis on evidence-based treatment supports demand. These factors make Sputum and Lung Tissue the fastest-growing diagnostic segment.

- By Treatment

On the basis of treatment, the Legionellosis market is segmented into Medication, Sooner Therapy, and Others. The Medication segment accounted for the largest market revenue share of 71.6% in 2025, driven by standard clinical use of antibiotics such as azithromycin, levofloxacin, and other anti-infective therapies. Prompt antibiotic treatment remains the cornerstone of legionellosis management. Severe cases require hospitalization and immediate drug intervention, increasing market demand. Rising pneumonia burden worldwide is significantly supporting prescription growth. Hospitals maintain large stocks of anti-infective medicines for respiratory emergencies. Generic availability has improved access across developing countries. Increasing awareness among clinicians regarding early antibiotic initiation is strengthening outcomes. Elderly and immunocompromised patients often need prolonged therapy. Pharmaceutical innovation in broad-spectrum antibiotics also supports market expansion. Strong physician confidence in medication-based management reinforces dominance. Improved diagnostic speed further increases timely prescriptions. These factors ensure Medication remains the leading treatment segment.

The Sooner Therapy segment is expected to witness the fastest growth rate of 8.9% CAGR from 2026 to 2033, driven by increasing focus on rapid supportive intervention immediately after diagnosis. This includes oxygen support, fluid management, fever control, and respiratory stabilization. Hospitals are emphasizing early supportive care to reduce ICU admissions and mortality. Growing adoption of standardized pneumonia management protocols supports demand. Emergency departments are increasingly using rapid stabilization pathways. Aging populations with comorbidities often require supportive treatment alongside antibiotics. Expansion of respiratory care infrastructure globally contributes to growth. Rising awareness regarding sepsis prevention also drives early intervention demand. Home monitoring tools are improving early symptom response. Healthcare providers increasingly integrate supportive and pharmacological treatment plans. Faster clinical recovery rates are supporting segment adoption. These factors collectively make Sooner Therapy the fastest-growing treatment segment.

- By Route of Administration

On the basis of route of administration, the Legionellosis market is segmented into Oral, Parenteral, and Others. The Parenteral segment dominated the largest market revenue share of 58.4% in 2025, driven by high use of intravenous antibiotics in moderate-to-severe hospitalized patients. Parenteral delivery ensures rapid drug absorption and immediate therapeutic action. ICU patients and those with severe pneumonia are primary users of injectable treatment. Hospitals prefer this route for accurate dosing and close monitoring. Rising hospitalization rates from respiratory infections support segment growth. Availability of multiple injectable antibiotics strengthens demand. Increasing critical care infrastructure globally contributes to adoption. Physicians often initiate IV therapy before shifting patients to oral medicines. Improved infusion technologies also support efficiency. Emergency care dependence on parenteral medicines reinforces leadership. These factors maintain dominance of the Parenteral segment.

The Oral segment is expected to witness the fastest growth rate of 9.5% CAGR from 2026 to 2033, driven by increasing treatment of mild and moderate cases in outpatient settings. Oral medicines provide convenience, affordability, and easy long-term adherence. Post-discharge continuation therapy also supports segment demand. Rising telemedicine consultations are encouraging home-based treatment pathways. Growing retail pharmacy access increases availability of oral antibiotics. Patients prefer tablets and capsules due to comfort and lower costs. Expanding healthcare access in emerging markets further boosts growth. Physicians increasingly transition stabilized patients from IV to oral therapy. Strong generic competition improves affordability. Rising awareness of early treatment supports prescription growth. These factors position Oral administration as the fastest-growing route segment.

- By Dosage Form

On the basis of dosage form, the Legionellosis market is segmented into Tablets, Capsules, Injections, and Others. The Injections segment held the largest market revenue share of 49.1% in 2025, driven by strong hospital demand for immediate treatment of severe legionella infections. Injectable formulations are widely used in emergency and inpatient settings. They provide faster clinical response compared with oral forms. ICU treatment protocols heavily depend on injectable antibiotics. Rising severe pneumonia admissions are boosting segment revenue. Hospitals maintain stable procurement volumes for injectables. Availability of branded and generic injectables supports supply. Improved infusion safety systems also aid growth. Physicians prefer injections during early critical phases of treatment. Strong inpatient treatment trends reinforce segment leadership. These factors ensure Injections remain dominant.

The Tablets segment is expected to witness the fastest growth rate of 9.8% CAGR from 2026 to 2033, driven by increasing outpatient management and recovery-phase prescriptions. Tablets are convenient, portable, and widely accepted by patients. Lower pricing compared with injectable therapies supports broader use. Retail and online pharmacy growth improves access globally. Post-hospital discharge patients commonly continue treatment through tablets. Generic manufacturing expansion strengthens affordability. Better adherence programs are supporting completion of therapy. Growing preference for homecare treatment also drives demand. Physicians often prescribe tablets for mild infections. Increasing awareness of early consultation boosts prescriptions. These factors make Tablets the fastest-growing dosage form segment.

- By End-Users

On the basis of end-users, the Legionellosis market is segmented into Hospitals, Specialty Clinics, Homecare, and Others. The Hospitals segment accounted for the largest market revenue share of 63.7% in 2025, driven by the majority of severe legionellosis cases requiring inpatient treatment. Hospitals offer ICU care, respiratory support, diagnostics, and intravenous therapy under one setting. Rising pneumonia-related admissions significantly support demand. Availability of infectious disease specialists strengthens treatment quality. Advanced laboratory infrastructure aids rapid diagnosis. Growing elderly patient admissions further contribute to growth. Strong reimbursement systems support hospital-based care. Emergency outbreak management often begins in hospitals. Expansion of tertiary healthcare centers worldwide boosts capacity. High medicine consumption within hospitals supports revenue leadership. These factors ensure hospitals remain dominant.

The Homecare segment is expected to witness the fastest growth rate of 10.1% CAGR from 2026 to 2033, driven by increasing preference for recovery management outside hospital settings. Patients with mild illness or post-discharge needs are increasingly treated at home. Oral medication availability supports this transition. Telehealth monitoring is improving physician oversight. Lower treatment costs encourage homecare adoption. Elderly patients prefer familiar home environments for recovery. Nursing support services are expanding globally. Governments are promoting decentralized care models. Remote monitoring devices improve safety and compliance. Faster discharge protocols from hospitals also support growth. These factors make Homecare the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the Legionellosis market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Others. The Hospital Pharmacy segment dominated the largest market revenue share of 56.8% in 2025, driven by strong inpatient dispensing of antibiotics, injectables, and supportive respiratory medicines. Most severe cases are diagnosed and treated in hospitals. Immediate medicine availability supports emergency treatment protocols. Bulk procurement systems reduce costs for healthcare providers. High patient turnover sustains medicine demand. ICU and respiratory wards are major consumers. Reliable supply chains strengthen hospital pharmacy dominance. Physician-controlled dispensing also improves compliance. Increasing hospital admissions globally support revenue growth. Expanded hospital infrastructure boosts pharmacy sales. These factors keep Hospital Pharmacy dominant.

The Online Pharmacy segment is expected to witness the fastest growth rate of 11.4% CAGR from 2026 to 2033, driven by rapid digital health adoption and demand for convenient medicine delivery. Patients increasingly order follow-up oral prescriptions online after discharge. Smartphone penetration and e-commerce trust are accelerating usage. Competitive pricing attracts cost-conscious consumers. Wider geographic reach improves medicine access in remote areas. Subscription refill models improve adherence. Integration with telemedicine platforms supports seamless prescribing. Fast logistics networks enhance patient convenience. Growing regulatory support for e-pharmacy channels aids expansion. Younger consumers strongly prefer digital purchase options. These factors collectively make Online Pharmacy the fastest-growing distribution channel segment.

Legionellosis Market Regional Analysis

- North America dominated the Legionellosis market with the largest revenue share of 38.40% in 2025, supported by advanced healthcare infrastructure, robust disease surveillance systems, high awareness of healthcare-associated infections, and widespread use of rapid diagnostic tools. The region benefits from established public health monitoring frameworks, strong hospital infection prevention protocols, and increasing investments in environmental water safety management

- Healthcare providers and regulatory agencies in the region highly prioritize early detection, outbreak control, and prevention of Legionella contamination in hospitals, hotels, commercial buildings, and community water systems. Growing adoption of rapid urinary antigen tests, molecular diagnostics, and water monitoring technologies is further strengthening market growth

- This widespread adoption is further supported by strong healthcare spending, strict compliance requirements, and increasing focus on public health preparedness, establishing North America as a leading region for Legionellosis diagnosis, surveillance, and prevention

U.S. Legionellosis Market Insight

The U.S. Legionellosis market captured the largest revenue share within North America in 2025, driven by substantial investments in prevention programs and outbreak monitoring. The country is witnessing increased adoption of rapid diagnostic tests, laboratory surveillance systems, and water safety compliance programs across healthcare and commercial facilities. Hospitals, long-term care centers, hotels, and municipal authorities are increasingly implementing Legionella risk management strategies that include regular water testing, disinfection systems, and environmental monitoring. Rising awareness of healthcare-associated pneumonia and waterborne outbreaks is further propelling market growth in the U.S.

Europe Legionellosis Market Insight

The Europe Legionellosis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent public health regulations, increasing awareness of waterborne infections, and expanding disease surveillance systems. The region is witnessing rising demand for rapid diagnostics, environmental monitoring services, and water treatment solutions across hospitals, hotels, and residential complexes. Strong regulatory oversight and focus on preventing outbreaks are contributing significantly to market expansion across Europe.

U.K. Legionellosis Market Insight

The U.K. Legionellosis market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by strict building water safety regulations and increasing awareness of Legionella control measures. Healthcare facilities, commercial properties, and public institutions are increasingly adopting routine water testing and preventive maintenance protocols. Growing demand for fast diagnostic services and outbreak management programs is expected to stimulate market growth in the U.K.

Germany Legionellosis Market Insight

The Germany Legionellosis market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, strong environmental compliance standards, and increasing focus on water hygiene management. Germany’s hospitals, hotels, and industrial facilities are increasingly utilizing water quality monitoring systems and rapid diagnostics to reduce infection risks. The country’s emphasis on preventive healthcare and public safety is supporting market growth.

Asia-Pacific Legionellosis Market Insight

The Asia-Pacific Legionellosis market is poised to grow at the fastest CAGR during the forecast period, driven by expanding urban infrastructure, increasing healthcare expenditure, rising awareness of water hygiene standards, and growing diagnostic access across countries such as China, India, Japan, and Australia. The region is witnessing rapid growth in commercial buildings, healthcare facilities, and municipal water systems requiring improved Legionella monitoring and prevention strategies. Government investments in sanitation, healthcare modernization, and disease surveillance are further accelerating market expansion.

Japan Legionellosis Market Insight

The Japan Legionellosis market is gaining momentum due to the country’s advanced healthcare system, dense urban infrastructure, and strong emphasis on hygiene and public health safety. Japanese healthcare providers and facility managers increasingly rely on routine water quality monitoring, rapid testing, and preventive maintenance systems. Demand is also rising in hospitality and elderly care sectors, supporting steady market growth.

China Legionellosis Market Insight

The China Legionellosis market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid urbanization, expanding healthcare infrastructure, and increasing awareness of waterborne disease prevention. China is witnessing strong growth in diagnostic services, hospital infection control programs, and water system monitoring across commercial and residential developments. Government focus on public health safety and modern infrastructure management is significantly propelling the market in the country.

Legionellosis Market Share

The Legionellosis industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Hoffmann-La Roche Ltd. (Switzerland)

- Abbott Laboratories (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- bioMérieux SA (France)

- Siemens Healthineers AG (Germany)

- Danaher Corporation (Cepheid) (U.S.)

- Becton, Dickinson and Company (BD) (U.S.)

- Quest Diagnostics Incorporated (U.S.)

- Laboratory Corporation of America Holdings (Labcorp) (U.S.)

- Hologic, Inc. (U.S.)

- Bio-Rad Laboratories, Inc. (U.S.)

- Sysmex Corporation (Japan)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Viatris Inc. (U.S.)

- Sanofi S.A. (France)

Latest Developments in Global Legionellosis Market

- In March 2021, the U.S. Centers for Disease Control and Prevention (CDC) reported that Legionnaires’ disease cases, which had declined during the first year of the COVID-19 pandemic, rebounded in 2021, highlighting renewed public health concern over legionellosis and the continued need for water system monitoring and outbreak prevention programs.

- In May 2022, researchers published a major review titled Legionnaires’ Disease: Update on Diagnosis and Treatment, outlining advances in PCR-based testing, urine antigen diagnostics, and first-line antibiotic therapies such as azithromycin and levofloxacin. The publication reinforced growing clinical focus on faster diagnosis and earlier treatment of legionellosis worldwide.

- In August 2022, hospitals and infectious disease centers across Europe and North America increased use of molecular diagnostic testing for severe community-acquired pneumonia cases, helping improve detection of Legionella infections beyond traditional urine antigen methods and supporting more targeted treatment decisions.

- In July 2023, the World Health Organization issued a Disease Outbreak News report on a legionellosis outbreak in Poland, drawing international attention to the importance of rapid surveillance, environmental investigation, and coordinated response systems for Legionella contamination events.

- In September 2023, public health authorities in multiple countries strengthened building water management guidance for hospitals, hotels, and large facilities following recurring Legionella outbreaks, supporting demand for prevention services, environmental testing, and water treatment solutions in the legionellosis market.

- In April 2024, researchers published a comprehensive review titled Severe Legionnaires’ Disease in Annals of Intensive Care, highlighting improvements in rapid urine antigen testing, molecular diagnostics, and intensive care management strategies for critically ill patients. The study underscored growing innovation in severe legionellosis treatment pathways

- In June 2024, healthcare systems increasingly adopted broader Legionella PCR testing panels for pneumonia patients, reflecting market demand for high-sensitivity diagnostics capable of detecting multiple Legionella species and serogroups beyond conventional tests

- In July 2025, researchers published results from the multicentre SwissLEGIO study showing that microbiological testing significantly influenced antibiotic prescribing practices for Legionnaires’ disease in Switzerland. The findings highlighted the commercial and clinical importance of advanced diagnostics in guiding optimized therapy selection

- In August 2025, New York City health officials investigated a major community cluster of Legionnaires’ disease in Harlem, with over 100 reported cases and multiple deaths, reinforcing continued global demand for outbreak control services, water safety monitoring, and rapid clinical diagnosis solutions

- In September 2025, Institut Pasteur updated its legionellosis disease information, noting that no vaccine currently exists for Legionnaires’ disease and emphasizing the continued market need for antibiotics, preventive water management systems, and improved diagnostic technologies

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.