Global Leucocytosis Market

Market Size in USD Billion

USD

33.94 Billion

USD

63.56 Billion

2024

2032

USD

33.94 Billion

USD

63.56 Billion

2024

2032

| 2025 - 2032 | |

| USD 33.94 Billion | |

| USD 63.56 Billion | |

| % | |

|

Leucocytosis Market Size

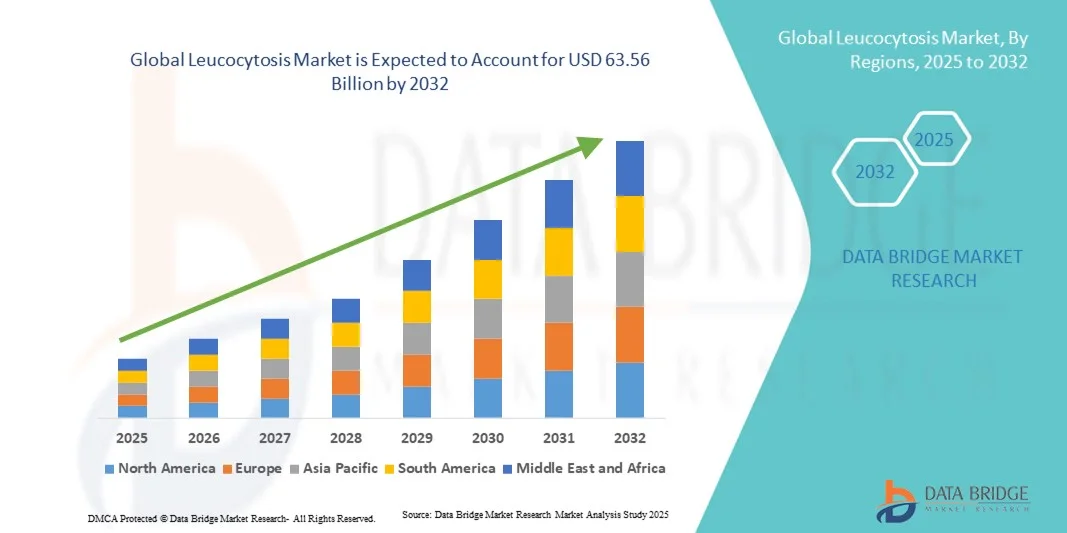

- The global leucocytosis market size was valued at USD 33.94 billion in 2024 and is expected to reach USD 63.56 billion by 2032, at a CAGR of 8.16% during the forecast period

- The market growth is largely fueled by the increasing prevalence of infections, inflammatory disorders, and other medical conditions that lead to elevated white blood cell counts, driving the demand for effective diagnosis and management of leucocytosis

- Furthermore, rising awareness among healthcare providers and patients regarding early detection, along with advancements in diagnostic technologies such as automated blood analyzers and laboratory testing solutions, is accelerating the adoption of leucocytosis management and treatment solutions, thereby significantly boosting the industry's growth

Leucocytosis Market Analysis

- Leucocytosis diagnostics and treatments, offering advanced laboratory testing and targeted therapeutic interventions, are increasingly vital components of modern healthcare systems in both hospitals and specialty clinics due to their enhanced accuracy, timely results, and integration with patient care workflows

- The escalating demand for leucocytosis management solutions is primarily fueled by the widespread adoption of advanced diagnostic technologies, growing prevalence of blood disorders, and a rising focus on early detection and effective treatment

- North America dominated the leucocytosis market with the largest revenue share of 41% in 2024, supported by advanced healthcare infrastructure, high healthcare spending, and the presence of leading diagnostic and pharmaceutical companies specializing in hematology. The U.S. remains the primary contributor, driven by widespread adoption of modern diagnostic tools, strong R&D activities, and public health initiatives targeting blood disorders

- Asia-Pacific is expected to be the fastest-growing region in the leucocytosis market during the forecast period, fueled by increasing population density, urbanization, rising healthcare awareness, and improved access to diagnostic and treatment facilities. Countries such as India, China, and Southeast Asian nations are witnessing rapid expansion of hospital networks and laboratory services, supporting market growth

- The therapeutic applications segment dominated the largest market revenue share of 57.1% in 2024, driven by its use in treating hematological malignancies, autoimmune disorders, and in stem cell transplantation procedures

Report Scope and Leucocytosis Market Segmentation

|

Attributes |

Leucocytosis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Leucocytosis Market Trends

Enhanced Diagnostic and Therapeutic Capabilities

- A significant and accelerating trend in the global leucocytosis market is the growing adoption of advanced diagnostic tools, including automated hematology analyzers, flow cytometry, and high-throughput blood testing platforms. These innovations are significantly improving the speed, accuracy, and reliability of leucocyte count assessment and related diagnostics

- For instance, In 2022, Sysmex Corporation, a leading global provider of hematology analyzers, launched its XN-Series fully automated hematology platform, enhancing efficiency and diagnostic precision for blood disorders, including leucocytosis

- Integration of artificial intelligence and machine learning in diagnostic platforms is enabling predictive analytics and risk stratification, helping clinicians identify high-risk patients and optimize treatment plans

- The development of targeted therapies, including immunomodulators and gene-based treatments, is expanding treatment options for patients with underlying hematologic disorders causing leucocytosis

- Expansion of clinical trials and research studies focusing on rare causes of leucocytosis is increasing awareness of complex pathologies, leading to more effective diagnostic algorithms and treatment protocols

- The adoption of integrated electronic health records (EHRs) and clinical decision support systems (CDSS) allows for real-time patient monitoring and better management of chronic conditions associated with leucocytosis

- Growing collaborations between hospitals, diagnostic laboratories, and pharmaceutical companies are accelerating the development of novel therapies and comprehensive patient care solutions

Leucocytosis Market Dynamics

Driver

Increasing Prevalence of Blood Disorders and Rising Clinical Awareness

- The rising prevalence of infections, autoimmune disorders, and hematological malignancies that affect white blood cell counts is driving higher demand for accurate diagnostics and treatment options

- Increasing awareness among healthcare professionals about the clinical significance of abnormal leucocyte counts is leading to early diagnosis, timely intervention, and improved patient outcomes.

- For instance, In April 2023, Roche Diagnostics announced the expansion of its hematology testing portfolio to include more advanced assays for white blood cell abnormalities, supporting clinicians in the early detection and management of leucocytosis

- Pharmaceutical and biotechnology companies are developing novel drugs and targeted therapies aimed at treating underlying conditions that lead to leucocytosis, including cytokine modulators, immunotherapies, and small molecule inhibitors

- Public health initiatives and patient education campaigns focused on blood disorders and the importance of regular screenings are encouraging proactive health management, increasing demand for diagnostic services

- The growing adoption of personalized medicine approaches and precision therapy protocols is fostering tailored treatments based on patient-specific blood profiles, improving treatment efficacy

Restraint/Challenge

High Treatment Costs, Limited Access, and Variability in Diagnostic Standards

- The high cost of advanced diagnostics and targeted therapies limits adoption, particularly in low- and middle-income countries

- Limited availability of specialized testing facilities in rural and underserved areas restricts access to timely diagnosis and effective treatment

- For instance, In 2021, Médecins Sans Frontières (MSF) highlighted the difficulty of providing advanced hematology diagnostics in remote regions of Africa due to high costs and lack of infrastructure, exemplifying access barriers for patients with leucocytosis

- Variability in clinical guidelines and diagnostic standards across regions leads to inconsistent patient management practices and challenges in standardizing care

- Concerns about potential side effects of some therapies, such as immunosuppressants or aggressive pharmacological interventions, may reduce adoption among clinicians and patients

- Need for repeated testing and ongoing patient monitoring increases the burden on healthcare systems and patient adherence, which can hinder treatment continuity

- Lack of trained healthcare professionals and laboratory personnel in emerging markets can delay diagnosis and compromise care quality

Leucocytosis Market Scope

The market is segmented on the basis of type, application, and end user.

- By Type

On the basis of type, the Leukapheresis market is segmented into leukapheresis devices and leukapheresis disposables. The leukapheresis devices segment dominated the largest market revenue share of 52.4% in 2024, driven by its essential role in the collection of specific blood components for therapeutic and research purposes. These devices are critical in the treatment of hematological disorders, stem cell collection, and immunotherapy procedures. Advanced automation, precise separation technology, and safety features enhance clinical adoption. Hospitals, blood centers, and research institutes rely heavily on these devices for accurate and efficient component collection. The segment benefits from technological advancements such as closed-system processing, which reduces contamination risk. Maintenance support, training, and post-sales services by manufacturers strengthen adoption. Increasing prevalence of leukemia, autoimmune diseases, and hematologic malignancies drives demand. Growing stem cell therapy applications also contribute to device uptake. Device standardization ensures reproducibility and safety across multiple centers. Government initiatives promoting blood donation and component therapy support expansion. Rising collaborations with academic and research institutions further enhance usage. Regulatory approvals for high-efficiency devices boost market confidence.

The leukapheresis disposables segment is projected to witness the fastest CAGR of 19.2% from 2025 to 2032, driven by recurring usage and the need for single-use, sterile kits for each procedure. Disposables include tubing sets, collection bags, and filters, which ensure contamination-free processing and patient safety. Hospitals and blood centers require consistent disposable supply to maintain uninterrupted procedures. Growing adoption of personalized medicine and cell therapy increases demand for high-quality disposables. Manufacturers are innovating with pre-assembled, easy-to-use kits to improve workflow efficiency. Disposable usage is critical in both research and therapeutic applications. Stringent regulatory guidelines for sterility and biocompatibility drive adoption of certified products. Academic research labs increasingly rely on standardized disposable kits for reproducibility. Logistics and supply chain efficiency ensure timely delivery to end users. Disposable kits reduce operational downtime and enhance patient safety. Multi-center clinical trials support increased consumable consumption. Partnerships with device manufacturers ensure bundled solutions, expanding adoption. Awareness of infection control and best practices boosts the shift toward disposables.

- By Application

On the basis of application, the Leukapheresis market is segmented into research applications and therapeutic applications. The therapeutic applications segment dominated the largest market revenue share of 57.1% in 2024, driven by its use in treating hematological malignancies, autoimmune disorders, and in stem cell transplantation procedures. Therapeutic leukapheresis removes pathogenic cells or collects stem cells for transplantation, offering a life-saving intervention for critically ill patients. Hospitals and transfusion centers increasingly adopt therapeutic leukapheresis due to improved patient outcomes and standardized procedures. The segment benefits from rising awareness of personalized medicine and immunotherapy. Insurance coverage and reimbursement policies support broader patient access. Continuous advancements in apheresis devices enhance safety, throughput, and efficiency. Training programs for healthcare professionals improve operational accuracy. Therapeutic leukapheresis is critical for CAR-T cell therapy and regenerative medicine. Hospital protocols prioritize therapeutic procedures for urgent clinical cases. Government and NGO initiatives promote accessibility for rare disorders. Clinical trials further validate therapeutic applications, encouraging adoption. Growing prevalence of leukemia and autoimmune diseases reinforces market dominance.

The research applications segment is expected to witness the fastest CAGR of 20.3% from 2025 to 2032, fueled by the increasing demand for stem cell research, immunotherapy development, and clinical studies. Research institutes and pharmaceutical companies rely on leukapheresis for isolating peripheral blood mononuclear cells (PBMCs), lymphocytes, and stem cells. Rising investment in genomics and personalized medicine drives usage. Collaboration with biotech companies accelerates adoption in preclinical and clinical research. Disposable kits and advanced collection devices enhance efficiency and reproducibility. Research applications include developing novel cell therapies and understanding disease mechanisms. Government and private funding for regenerative medicine increases market penetration. Academic institutions expand lab capacity and access to leukapheresis equipment. Multi-center research projects require standardized collection processes. High-throughput processing supports large-scale studies. Integration with cryopreservation and storage facilities improves workflow. Regulatory compliance for research-grade samples ensures safety and quality. Rapid growth in immunotherapy and vaccine research further accelerates segment expansion.

- By End User

On the basis of end user, the Leukapheresis market is segmented into blood component providers and blood centers, academic and research institutes, pharmaceutical and biotechnology companies, and hospitals and transfusion centers. The hospitals and transfusion centers segment accounted for the largest market revenue share of 45.7% in 2024, due to direct involvement in patient care, stem cell collection, and therapeutic apheresis procedures. These centers provide critical services for hematology, oncology, and immunotherapy treatments. Adoption is driven by availability of trained staff, advanced infrastructure, and integration with clinical workflows. Hospitals prioritize high-throughput, safe, and standardized procedures for patient outcomes. Regulatory compliance, insurance support, and reimbursement policies facilitate widespread use. Repeat treatments and long-term care reinforce steady demand. Partnerships with blood centers and research institutions improve efficiency. Hospitals implement strict quality control and monitoring for leukapheresis procedures. Rapid technological adoption, device upgrades, and continuous training enhance operational capacity. Clinical trials conducted in hospitals increase procedural demand. Patient preference for hospital-based therapeutic interventions ensures market dominance. Government initiatives promoting blood donations and stem cell therapies support expansion.

The academic and research institutes segment is projected to witness the fastest CAGR of 21.6% from 2025 to 2032, driven by the growing requirement for cellular research, immunotherapy studies, and stem cell isolation. These institutes require high-quality, reproducible leukapheresis samples for experimental and translational research. Investment in biotechnology and regenerative medicine accelerates equipment and consumable adoption. Collaboration with pharmaceutical companies facilitates multi-center research programs. Advanced devices and sterile disposable kits ensure safety and accuracy. Academic research also benefits from government funding and grant programs. Expansion of specialized laboratory facilities increases procedural capacity. Integration with bioinformatics and sample storage improves workflow efficiency. Clinical and preclinical studies rely on large-scale leukapheresis collection. Stem cell banking and immunotherapy research increase demand for high-quality leukapheresis. Academic centers adopt standardized protocols to ensure reproducibility. Research collaborations with hospitals enhance access to clinical samples. Growing awareness of personalized medicine and cell therapy applications drives adoption.

Leucocytosis Market Regional Analysis

- North America dominated the leucocytosis market with a 41% revenue share in 2024, supported by advanced healthcare infrastructure, high healthcare spending, and leading diagnostic and pharmaceutical companies

- The market drives the region, with widespread adoption of modern hematology analyzers, leukapheresis devices, and strong R&D activities. Public health initiatives for early detection of blood disorders, skilled medical personnel, and robust hospital networks further boost demand

- Technological advancements in diagnostics, high patient awareness, and regulatory support for quality and safety reinforce North America’s market leadership

U.S. Leucocytosis Market Insight

The U.S. leucocytosis market held North America’s revenue in 2024, driven by advanced diagnostic tools and laboratory expansion. Hospitals and specialty clinics invest in automated analyzers, flow cytometry, and leukapheresis for hematological disorders. Strong healthcare infrastructure, reimbursement policies, and public health programs enhance early detection and treatment. Collaboration with academic and pharmaceutical sectors, along with research initiatives, further supports growth.

Europe Leucocytosis Market Insight

The Europe leucocytosis market is projected to expand steadily, driven by well-developed healthcare systems, stringent clinical regulations, and rising awareness of hematological disorders. Germany, the U.K., and France see high utilization of leukapheresis, automated analyzers, and specialized lab services. Urbanization, preventive healthcare, and multi-center collaborations foster adoption of advanced diagnostics.

U.K. Leucocytosis Market Insight

The U.K. leucocytosis market is expected to grow at a notable CAGR, supported by hospital and clinic expansions in automated diagnostics and leukapheresis. Public health programs and rising patient awareness encourage early testing for blood disorders. Integration of laboratory systems and strong clinical infrastructure ensures timely, accurate diagnosis.

Germany Leucocytosis Market Insight

The Germany leucocytosis market is set for steady growth, driven by awareness of hematological health, adoption of advanced diagnostics, and precision treatment. Hospitals and labs are integrating automated analyzers, leukapheresis devices, and digital reporting. Government policies, reimbursement coverage, and high prevalence of leukemia and autoimmune conditions boost adoption.

Asia-Pacific Leucocytosis Market Insight

The Asia-Pacific leucocytosis market is poised for the fastest CAGR (2025–2032), fueled by population density, urbanization, rising healthcare awareness, and better diagnostic access. India, China, and Southeast Asia see rapid hospital and lab expansion. Government initiatives, affordable diagnostic solutions, and growing prevalence of blood disorders drive growth. High demand for leukapheresis and automated testing, along with expanding biotech research, supports adoption.

Japan Leucocytosis Market Insight

The Japan leucocytosis market grows due to aging population, healthcare awareness, and demand for accurate diagnostics. Hospitals adopt automated analyzers and leukapheresis devices. Government programs and preventive care campaigns encourage early detection. Integration with electronic reporting and research collaborations boost market growth.

China Leucocytosis Market Insight

China leucocytosis market held the largest revenue share in APAC in 2024, driven by urbanization, rising healthcare awareness, and hospital network expansion. Adoption of automated analyzers, leukapheresis devices, and advanced lab solutions increases. Government initiatives, prevalence of leukemia and autoimmune disorders, and affordable diagnostics support market expansion. Clinical research, hospital-academic collaborations, and digital health integration enhance adoption and patient outcomes.

Leucocytosis Market Share

The Leucocytosis industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Sysmex Corporation (Japan)

- Beckman Coulter (U.S.)

- Siemens Healthineers AG(Germany)

- BD (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- HORIBA, Ltd. (Japan)

- Ortho Clinical Diagnostics (U.S.)

- Bio-Rad Laboratories (U.S.)

- F. Hoffmann-La Roche AG (Switzerland)

- Mindray Medical International (China)

- Nihon Kohden Corporation (Japan)

- BioMérieux (France)

- Instrumentation Laboratory (U.S.)

- Danaher Corporation (U.S.)

Latest Developments in Global Leucocytosis Market

- In September 2025, researchers at Dana-Farber Cancer Institute and the Broad Institute introduced MARLIN, an AI-based diagnostic tool that utilizes DNA methylation patterns to classify acute leukemia subtypes within two hours. This advancement significantly reduces diagnosis time, enabling faster treatment decisions for patients with leukocytosis

- In August 2025, the development of Myelosoft, an AI-assisted web application, was reported. This platform allows clinicians to upload smartphone-captured peripheral blood smear images for rapid and automated analysis, enhancing the accuracy and efficiency of leukocyte abnormality detection in leukocytosis cases

- In June 2025, a study highlighted the effectiveness of AI and data science methods in biomedical diagnostics, including the automatic detection and counting of white blood cells. These advancements are crucial for diagnosing and treating blood diseases such as leukemia, which can lead to leukocytosis

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.