Global Lichen Planus Market

Market Size in USD Billion

USD

160.25 Billion

USD

285.80 Billion

2025

2033

USD

160.25 Billion

USD

285.80 Billion

2025

2033

| 2026 - 2033 | |

| USD 160.25 Billion | |

| USD 285.80 Billion | |

| % | |

|

Lichen Planus Market Size

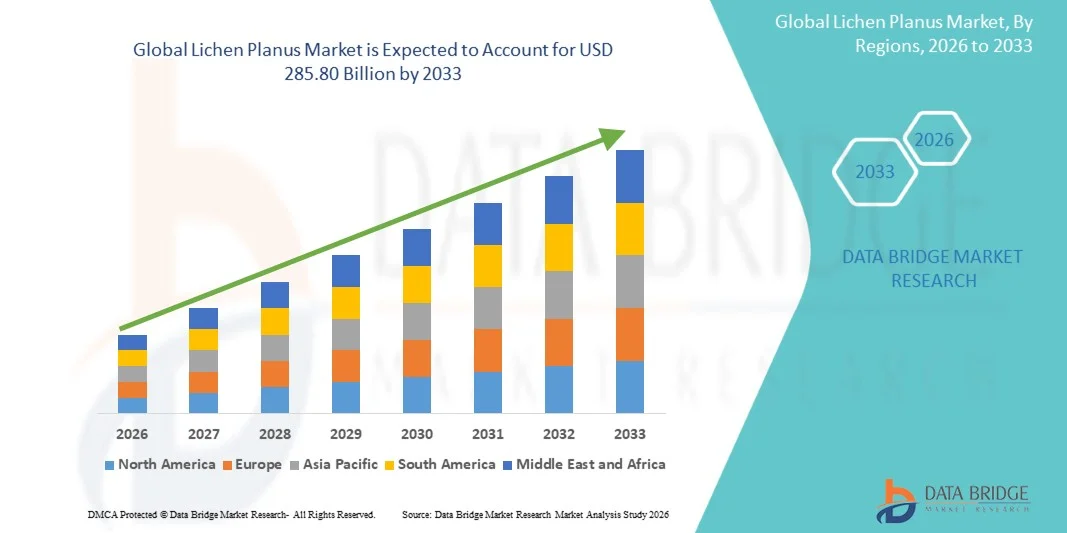

- The global lichen planus market size was valued at USD 160.25 billion in 2025and is expected to reach USD 285.80 billion by 2033, at a CAGR of 7.50% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic inflammatory and autoimmune skin disorders, along with increasing awareness regarding early dermatological diagnosis and treatment, leading to greater adoption of Lichen Planus therapies across hospitals, specialty clinics, and dermatology centers. Advancements in targeted dermatology treatments and improved access to healthcare services are further supporting market expansion

- Furthermore, growing demand for effective symptom management solutions, including corticosteroids, immunosuppressants, biologics, and phototherapy, is establishing Lichen Planus treatment options as essential components of modern dermatological care. These converging factors are accelerating the uptake of Lichen Planus solutions, thereby significantly boosting the industry's growth

Lichen Planus Market Analysis

- Lichen Planus, a chronic inflammatory condition affecting the skin, oral mucosa, scalp, nails, and genital regions, is increasingly recognized as an important segment within dermatology and autoimmune disease management due to rising awareness, improved diagnostic capabilities, and growing demand for long-term symptom control therapies

- The escalating demand for Lichen Planus diagnostic and treatment solutions is primarily fueled by increasing prevalence of autoimmune and inflammatory skin disorders, growing consultations in dermatology clinics, expanding use of corticosteroids and immunomodulators, and advancements in biologic therapies for severe or treatment-resistant cases

- North America dominated the lichen planus market with the largest revenue share of 37.60% in 2025, supported by advanced dermatology care infrastructure, strong presence of specialty treatment centers, favorable reimbursement systems, and increasing patient awareness, with the U.S. witnessing substantial utilization of prescription therapies and specialty dermatology services

- Asia-Pacific is expected to be the fastest growing region in the lichen planus market during the forecast period due to rising healthcare expenditure, improving access to dermatology specialists, increasing awareness of chronic skin diseases, and expanding treatment availability across countries such as China, India, Japan, and South Korea

- The Topical segment held the largest market revenue share of 56.4% in 2025, driven by its widespread use as the preferred first treatment option for localized skin lesions and itching

Report Scope and Lichen Planus Market Segmentation

|

Attributes |

Lichen Planus Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Pfizer Inc. (U.S.) · Novartis AG (Switzerland) · AbbVie Inc. (U.S.) · Johnson & Johnson (U.S.) · Eli Lilly and Company (U.S.) · Sanofi S.A. (France) · F. Hoffmann-La Roche Ltd. (Switzerland) · Bristol Myers Squibb (U.S.) · Amgen Inc. (U.S.) · AstraZeneca plc (U.K.) · Sun Pharmaceutical Industries Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Teva Pharmaceutical Industries Ltd. (Israel) · Viatris Inc. (U.S.) · Glenmark Pharmaceuticals Ltd. (India) · Cipla Limited (India) · Lupin Limited (India) · Leo Pharma A/S (Denmark) · Bausch Health Companies Inc. (Canada) |

|

Market Opportunities |

· Development of targeted biologics and advanced immunotherapies · Rising Demand in Emerging Markets |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Lichen Planus Market Trends

“Advancements in Targeted Dermatology Treatments and Early Diagnosis Solutions”

- A significant and accelerating trend in the global Lichen Planus market is the increasing adoption of targeted dermatology therapies, advanced diagnostic tools, and personalized treatment approaches aimed at improving symptom control and long-term disease management. These innovations are enhancing outcomes for patients affected by cutaneous, oral, and genital forms of Lichen Planus

- For instance, dermatology clinics and specialty centers are increasingly prescribing topical calcineurin inhibitors, corticosteroids, and immunomodulatory therapies for persistent or severe Lichen Planus cases, helping reduce inflammation, itching, and lesion recurrence

- Growing use of dermoscopy, biopsy confirmation, and digital dermatology consultations is improving early and accurate diagnosis, particularly in atypical or chronic presentations

- Research into biologics and targeted immune pathway therapies is expanding treatment possibilities for refractory cases that do not respond adequately to conventional therapies

- Rising adoption of teledermatology platforms is also improving follow-up care, treatment monitoring, and access to specialists in underserved regions

- This trend toward precision treatment and improved diagnostic pathways is reshaping expectations for chronic inflammatory skin disorder management worldwide

Lichen Planus Market Dynamics

Driver

“Rising Prevalence of Autoimmune Skin Disorders and Growing Dermatology Awareness”

- Increasing prevalence of inflammatory and autoimmune skin disorders, combined with rising awareness of chronic dermatological conditions, is a major driver supporting the growth of the Lichen Planus market

- For instance, hospitals and dermatology practices are reporting higher patient visits for chronic itching, oral lesions, and recurrent skin eruptions, leading to increased diagnosis and treatment demand for Lichen Planus

- Improved healthcare access and greater patient willingness to seek specialist consultation for visible or painful skin conditions are further driving market expansion

- Growing awareness regarding the association of Lichen Planus with stress, immune dysregulation, and certain comorbidities is supporting earlier clinical evaluation

- In addition, increasing availability of prescription topical agents, phototherapy services, and oral immunosuppressive treatments is strengthening treatment adoption globally

Restraint/Challenge

“Chronic Recurrence, Limited Curative Options, and Diagnostic Complexity”

- One of the major challenges in the Lichen Planus market is the recurrent and chronic nature of the disease, which often requires long-term symptom management rather than permanent cure

- For instance, many patients with oral or erosive Lichen Planus experience repeated flare-ups despite corticosteroid treatment, leading to prolonged therapy cycles and reduced quality of life

- Diagnostic complexity due to symptom overlap with fungal infections, eczema, psoriasis, and other mucosal disorders can delay accurate treatment initiation

- Potential side effects associated with prolonged steroid or immunosuppressive therapy may also limit long-term treatment adherence in some patients

- Addressing these challenges through development of targeted therapies, better patient monitoring, and improved clinician awareness will be essential for sustained market growth

Lichen Planus Market Scope

The market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the Lichen Planus market is segmented into Retinoids, Corticosteroids, Antihistamines, and Others. The Corticosteroids segment dominated the largest market revenue share of 47.8% in 2025, driven by its position as the first-line therapy for reducing inflammation, itching, redness, and immune-mediated skin lesions associated with lichen planus. Topical and systemic corticosteroids are widely prescribed across dermatology settings due to their rapid symptomatic relief. Physicians prefer corticosteroids for oral, cutaneous, scalp, and genital lichen planus management. Strong clinical familiarity and broad product availability are supporting continued usage globally. Increasing patient diagnosis rates and improved dermatology consultations are boosting demand. Corticosteroids are also used in recurrent and severe flare-up cases. Availability in creams, ointments, gels, and tablets supports treatment flexibility. Low-cost generic formulations further enhance accessibility. Growing awareness regarding autoimmune skin disorders is adding to prescriptions. Hospital and retail pharmacy availability remains strong worldwide. These factors collectively ensure dominance of the Corticosteroids segment.

The Retinoids segment is expected to witness the fastest growth rate of 8.7% CAGR from 2026 to 2033, driven by increasing use in steroid-resistant, chronic, and severe lichen planus cases. Retinoids are gaining preference where long-term steroid exposure is undesirable. Rising demand for targeted dermatology therapies is supporting market expansion. Dermatologists increasingly recommend retinoids for mucosal and hypertrophic lesions. Growing awareness regarding advanced skin treatment options is boosting adoption. Development of safer retinoid formulations with improved tolerability is another key driver. Increasing research into immune-modulating skin therapies supports wider utilization. Expanding specialist dermatology clinics in emerging economies further aid growth. Better patient compliance through improved formulations is encouraging uptake. Rising cases of recurrent disease are creating additional demand. These factors position Retinoids as the fastest-growing treatment segment.

- By Route of Administration

On the basis of route of administration, the Lichen Planus market is segmented into Oral, Topical, and Others. The Topical segment held the largest market revenue share of 56.4% in 2025, driven by its widespread use as the preferred first treatment option for localized skin lesions and itching. Topical creams, gels, and ointments allow direct application with lower systemic side effects. Dermatologists frequently prescribe topical corticosteroids and calcineurin-based preparations for mild-to-moderate disease. Increasing preference for convenient outpatient treatment is supporting growth. Patients favor topical products for easy self-application and quick symptom management. Rising awareness regarding early skin treatment is further boosting demand. Availability of prescription and branded formulations through pharmacies supports accessibility. Lower treatment cost compared with systemic therapies enhances market penetration. Strong demand in homecare settings also supports segment leadership. Improved cosmetic formulations increase patient adherence. These factors maintain dominance of the Topical segment.

The Oral segment is expected to witness the fastest growth rate of 7.9% CAGR from 2026 to 2033, driven by increasing use in widespread, recurrent, and severe lichen planus conditions. Oral corticosteroids, retinoids, and antihistamines are commonly prescribed where topical therapy is insufficient. Rising incidence of oral lichen planus and mucosal involvement is boosting segment growth. Physicians increasingly recommend oral treatment for systemic symptom control. Growing patient demand for effective long-duration management further supports adoption. Better access to specialist consultations is increasing prescriptions. Expanding healthcare expenditure in emerging economies is aiding treatment uptake. Research into safer oral immunomodulators is another growth catalyst. Improved adherence programs and follow-up care support recurring demand. These factors make Oral the fastest-growing route of administration segment.

- By End-Users

On the basis of end-users, the Lichen Planus market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment accounted for the largest market revenue share of 42.6% in 2025, driven by high patient footfall for diagnosis, biopsy procedures, specialist consultations, and treatment of severe lichen planus cases. Hospitals offer multidisciplinary access to dermatologists, oral medicine experts, and pathology laboratories. Patients with complicated mucosal or erosive disease often seek hospital-based treatment. Availability of advanced diagnostic tools supports early confirmation of disease. Strong prescription volumes for systemic medicines contribute to segment growth. Hospitals also manage patients requiring injectable or monitored therapies. Increasing awareness and referrals from primary care centers further support demand. Rising healthcare spending in developing nations strengthens hospital access. Better reimbursement systems in developed markets add momentum. These factors ensure Hospitals remain the dominant end-user segment.

The Specialty Clinics segment is expected to witness the fastest growth rate of 9.1% CAGR from 2026 to 2033, driven by increasing preference for focused dermatology and oral care centers. Patients are seeking faster appointments, personalized care, and advanced skin treatment options. Specialty clinics provide targeted management for chronic and relapsing lichen planus cases. Growing urbanization and rising disposable incomes are supporting clinic visits. Availability of laser therapy, patch testing, and advanced topical procedures boosts demand. Increasing number of private dermatology chains also contributes to growth. Better patient counseling and follow-up care improve long-term adherence. Digital booking and teledermatology integration are supporting convenience. Expanding presence in emerging economies further aids adoption. These factors position Specialty Clinics as the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the Lichen Planus market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Retail Pharmacy segment dominated the largest market revenue share of 49.3% in 2025, driven by easy access to prescribed topical creams, oral antihistamines, corticosteroids, and supportive care products. Retail pharmacies remain the most convenient channel for repeat medication purchases. Patients often refill chronic prescriptions through neighborhood pharmacies. Strong penetration of organized pharmacy chains supports broad product availability. Pharmacist guidance on dosage and skin-care products further encourages consumer trust. Growing diagnosis rates are increasing prescription volumes globally. Generic availability also improves affordability through retail outlets. Expanding pharmacy infrastructure in emerging markets strengthens access. Immediate product availability supports treatment continuity. These factors secure leadership of the Retail Pharmacy segment.

The Online Pharmacy segment is expected to witness the fastest growth rate of 10.4% CAGR from 2026 to 2033, driven by rising digital healthcare adoption and growing demand for home-delivered dermatology medicines. Patients increasingly prefer online channels for privacy, convenience, and price comparison. Subscription refill models are supporting long-term treatment adherence. Smartphone penetration and secure payment systems are accelerating online purchases. Availability of discounts and promotional offers attracts cost-sensitive users. Telemedicine integration enables direct e-prescription fulfillment. Better logistics networks are expanding delivery reach to smaller cities. Chronic patients benefit from recurring auto-refill services. Rising consumer trust in regulated e-pharmacy platforms is further boosting growth. These factors collectively make Online Pharmacy the fastest-growing distribution channel segment.

Lichen Planus Market Regional Analysis

- North America dominated the Lichen Planus market with the largest revenue share of 37.60% in 2025, supported by advanced dermatology care infrastructure, strong presence of specialty treatment centers, favorable reimbursement systems, and increasing patient awareness. The region benefits from established healthcare networks, growing access to dermatologists, and rising demand for effective management of chronic inflammatory skin conditions

- Patients and healthcare providers in the region highly value the availability of prescription corticosteroids, immunomodulators, biologics, and specialized oral care solutions for managing cutaneous and oral lichen planus. Increasing emphasis on early diagnosis and symptom control is further strengthening treatment adoption

- This widespread adoption is further supported by high healthcare expenditure, strong insurance coverage, and continuous advancements in dermatology therapeutics, establishing North America as a leading region in the Lichen Planus market

U.S. Lichen Planus Market Insight

The U.S. Lichen Planus market captured the largest revenue share within North America in 2025, driven by substantial utilization of prescription therapies and specialty dermatology services. The country benefits from strong patient awareness, broad access to dermatologists, and availability of advanced treatment options for skin and mucosal disorders. Healthcare providers are increasingly focused on individualized treatment strategies, including topical therapies, systemic medications, and long-term follow-up care for recurrent cases. Rising demand for specialty skin clinics and oral healthcare services continues to support market growth in the U.S.

Europe Lichen Planus Market Insight

The Europe Lichen Planus market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of chronic inflammatory skin diseases, strong public healthcare systems, and growing demand for specialized dermatology care. The region is witnessing rising adoption of advanced prescription treatments, oral disease management solutions, and specialist consultations. Increasing research activities in autoimmune and inflammatory disorders are also contributing to market expansion across Europe.

U.K. Lichen Planus Market Insight

The U.K. Lichen Planus market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by growing awareness of chronic skin conditions and expanding access to dermatology specialists. Healthcare providers are increasingly emphasizing early intervention and long-term management of oral and skin manifestations. Rising demand for outpatient dermatology services and prescription treatment options is expected to stimulate market growth in the U.K.

Germany Lichen Planus Market Insight

The Germany Lichen Planus market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure, increasing patient awareness, and growing demand for evidence-based dermatological therapies. Germany’s advanced clinical care systems and emphasis on specialist treatment are promoting adoption of innovative therapies for inflammatory skin diseases. Rising aging population levels are also supporting steady market growth.

Asia-Pacific Lichen Planus Market Insight

The Asia-Pacific Lichen Planus market is poised to grow at the fastest CAGR during the forecast period due to rising healthcare expenditure, improving access to dermatology specialists, increasing awareness of chronic skin diseases, and expanding treatment availability across countries such as China, India, Japan, and South Korea. Rapid urbanization, lifestyle changes, and growing environmental triggers are increasing dermatology consultations across the region. Expanding healthcare coverage and improving pharmaceutical access are further accelerating market growth in Asia-Pacific.

Japan Lichen Planus Market Insight

The Japan Lichen Planus market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong demand for high-quality dermatological care. Japanese healthcare providers increasingly focus on early diagnosis, symptom management, and long-term monitoring of inflammatory skin diseases. Availability of advanced therapeutics and strong patient compliance are further supporting market expansion.

China Lichen Planus Market Insight

The China Lichen Planus market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large patient base, improving healthcare accessibility, and increasing awareness of dermatological disorders. China is witnessing growing adoption of prescription therapies, hospital-based dermatology services, and expanding specialty clinics. Government healthcare reforms, rising disposable incomes, and improving access to modern treatments are key factors propelling the Lichen Planus market in the country.

Lichen Planus Market Share

The Lichen Planus industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- AbbVie Inc. (U.S.)

- Johnson & Johnson (U.S.)

- Eli Lilly and Company (U.S.)

- Sanofi S.A. (France)

- Hoffmann-La Roche Ltd. (Switzerland)

- Bristol Myers Squibb (U.S.)

- Amgen Inc. (U.S.)

- AstraZeneca plc (U.K.)

- Sun Pharmaceutical Industries Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Viatris Inc. (U.S.)

- Glenmark Pharmaceuticals Ltd. (India)

- Cipla Limited (India)

- Lupin Limited (India)

- Leo Pharma A/S (Denmark)

- Bausch Health Companies Inc. (Canada)

Latest Developments in Global Lichen Planus Market

- In February 2021, researchers published updated clinical guidance emphasizing corticosteroids as the first-line therapy for cutaneous and oral lichen planus, while also highlighting growing use of calcineurin inhibitors and immunomodulators for patients with recurrent or resistant disease. This reinforced continued demand for prescription therapies in the global lichen planus treatment market

- In November 2021, dermatology centers in North America and Europe expanded use of biologic and systemic immunosuppressive therapies for severe lichen planus cases, particularly erosive and widespread variants, reflecting a shift toward targeted treatment options beyond conventional steroids

- In October 2023, Lipella Pharmaceuticals announced that the U.S. FDA cleared its Investigational New Drug (IND) application for LP-310, a liposomal tacrolimus oral rinse developed for symptomatic Oral Lichen Planus (OLP). The approval enabled a multicenter Phase 2a clinical trial and marked a significant pipeline advancement in a disease area with no approved therapies

- In November 2024, Lipella Pharmaceuticals announced completion of the first cohort dosing in its multicenter Phase 2a trial of LP-310 for Oral Lichen Planus. Initial findings showed no product-related serious adverse events and minimal systemic tacrolimus exposure, supporting the potential for localized treatment with improved safety

- In February 2025, Lipella Pharmaceuticals reported positive topline Phase 2a results for LP-310 in Oral Lichen Planus, demonstrating clinically meaningful reductions in pain, ulceration, and inflammation. The results represented one of the most notable late-stage clinical developments in the lichen planus market.

- In April 2025, Lipella Pharmaceuticals announced completion of full enrollment in its Phase 2a multicenter dose-ranging study of LP-310 for Oral Lichen Planus across seven U.S. sites. The company stated that final topline data remained on schedule, highlighting continued momentum toward regulatory advancement.

- In May 2025, Lipella Pharmaceuticals presented Phase 2a clinical data for LP-310 at the joint American Academy of Oral Medicine and European Association of Oral Medicine meeting, showcasing statistically significant safety and efficacy outcomes. This presentation increased medical community visibility for a potential first approved therapy in Oral Lichen Planus

- In September 2025, Lipella Pharmaceuticals announced positive final Phase 2a results for LP-10/LP-310 in Oral Lichen Planus, with all enrolled patients completing treatment and statistically significant improvements reported across efficacy endpoints. The company also confirmed plans to initiate a pivotal Phase 2b study, signaling further commercialization progress in the market

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.