Global Liquid Cooled Ev Charging Cable Market

Market Size in USD Billion

USD

381.43 Billion

USD

1,107.29 Billion

2025

2033

USD

381.43 Billion

USD

1,107.29 Billion

2025

2033

| 2026 - 2033 | |

| USD 381.43 Billion | |

| USD 1,107.29 Billion | |

| % | |

|

Liquid Cooled EV Charging Cable Market Size

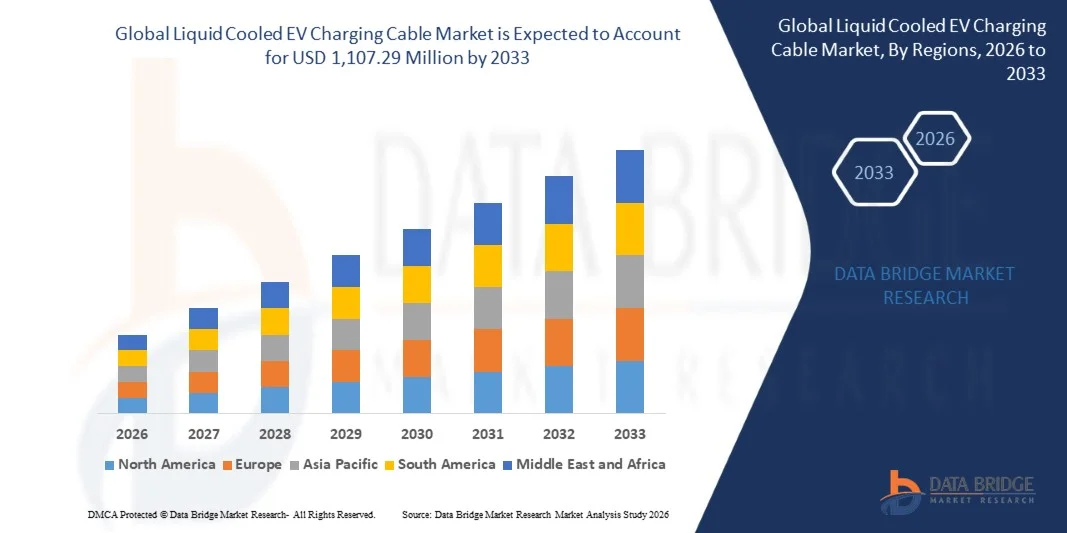

- The global liquid cooled EV charging cable market size was valued at USD 381.43 million in 2025and is expected to reach USD 1,107.29 million by 2033, at a CAGR of 14.25% during the forecast period

- The market growth is largely fuelled by the rising adoption of ultra-fast and high-power EV charging infrastructure, which requires efficient thermal management systems to prevent overheating and power loss in charging cables

- Increasing deployment of high-capacity electric vehicle charging stations across commercial highways, urban hubs, and fleet depots is further accelerating demand for liquid cooled charging cables

Liquid Cooled EV Charging Cable Market Analysis

- The market is witnessing strong technological advancements in cable cooling systems, including improved coolant circulation designs and lightweight flexible materials that enhance durability and efficiency

- Rising investments from governments and private players in EV charging infrastructure expansion are supporting large-scale installation of high-power fast chargers, thereby driving consistent demand for liquid cooled EV charging cables across key regions

- North America dominated the global liquid cooled EV charging cable market in 2025, driven by rapid expansion of ultra-fast EV charging infrastructure, increasing adoption of high-performance electric vehicles, and strong investments in megawatt charging networks

- Asia-Pacific region is expected to witness the highest growth rate in the global liquid cooled EV charging cable market, driven by rising electric vehicle penetration, expanding ultra-fast charging networks, strong manufacturing capabilities, and supportive government policies promoting sustainable mobility solutions

- The 500–900 kW segment held the largest market revenue share in 2025 driven by increasing deployment of high-power fast charging stations across commercial EV infrastructure and fleet charging networks. This range offers an optimal balance between charging speed and thermal efficiency, making it widely suitable for current ultra-fast charging requirements. Growing adoption of electric buses and heavy-duty vehicles is further strengthening demand for mid-to-high power capacity cables. In addition, continuous upgrades in charging station capabilities are supporting segment expansion

Report Scope and Liquid Cooled EV Charging Cable Market Segmentation

|

Attributes |

Liquid Cooled EV Charging Cable Key Market Insights |

|

Segments Covered |

· By Cable Power Capacity: 300–499 kW, 500–900 kW, Above 900 kW · By Application: Ultrafast Charging, Megawatt Charging · By Cable Length: Below 5 Meters, 5–8 Meters, Above 8 Meters · By Cable Diameter: Below 30 mm, 30–50 mm, Above 50 mm · By Jacket Material: Rubber, Thermoplastic Elastomer, Polyvinyl Chloride · By Cooling Fluid: Water Glycol, Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Liquid Cooled EV Charging Cable Market Trends

“Rising Demand For Ultra-Fast EV Charging Infrastructure”

- The growing shift toward high-power electric vehicle charging systems is significantly shaping the liquid cooled EV charging cable market, as consumers and fleet operators increasingly demand faster charging times with minimal energy loss. Liquid cooled cables are gaining traction due to their ability to manage high current loads efficiently while maintaining safety and performance standards. This trend is strengthening their adoption across public charging stations, highway corridors, and commercial EV fleets, encouraging manufacturers to develop advanced thermal management solutions tailored for ultra-fast charging applications

- Increasing penetration of heavy-duty electric vehicles such as trucks, buses, and long-range commercial EVs has accelerated the demand for high-capacity charging solutions supported by liquid cooling technology. These vehicles require megawatt-level charging infrastructure, which generates excessive heat that must be effectively controlled. This has led to rising collaboration between charging infrastructure providers and cable manufacturers to enhance performance reliability and durability under extreme load conditions

- The expansion of fast-charging networks across urban and intercity routes is influencing investment decisions, with operators prioritizing high-efficiency charging systems that reduce downtime and improve user experience. Liquid cooled EV charging cables are increasingly being integrated into next-generation charging stations to support higher power density and continuous operation. This is also driving technological upgrades in connector design, coolant circulation systems, and lightweight cable materials

- For instance, in 2025, leading charging infrastructure developers in China and Germany introduced high-power charging stations equipped with liquid cooled cable systems to support ultra-fast EV charging corridors. These deployments were designed to reduce charging time significantly while ensuring thermal stability during continuous high-load operations. The installations are also being expanded across commercial transport hubs and highway networks, improving EV adoption rates and charging accessibility for long-distance travel

- While demand for liquid cooled EV charging cables is growing, sustained market expansion depends on cost optimization, standardization of charging protocols, and advancements in durable cooling system design. Manufacturers are also focusing on improving efficiency, reducing maintenance requirements, and enhancing compatibility with next-generation EV platforms for broader global adoption

Liquid Cooled EV Charging Cable Market Dynamics

Driver

“Growing Adoption Of Ultra-Fast And Megawatt Charging Systems”

- Rising demand for high-speed electric vehicle charging infrastructure is a major driver for the liquid cooled EV charging cable market. As EV battery capacities increase, manufacturers and charging operators are adopting ultra-fast charging systems that require advanced thermal management to handle high power loads efficiently. This trend is also pushing innovation in liquid cooling technologies to ensure stable performance and prevent overheating during rapid energy transfer

- Expanding deployment of EV charging networks across highways, urban centers, and fleet depots is influencing market growth. Liquid cooled charging cables are essential for supporting continuous high-power operations, enabling faster turnaround times for electric vehicles. The increasing electrification of commercial transportation and logistics fleets further reinforces this demand across multiple end-use sectors

- Government initiatives promoting EV adoption and infrastructure development are encouraging large-scale investments in fast-charging ecosystems. Incentives, subsidies, and regulatory support are accelerating the installation of high-capacity charging stations, which rely heavily on liquid cooled cable systems for safe and efficient energy delivery. This is further supported by collaborations between automotive manufacturers and charging solution providers

- For instance, in 2024, several automotive and energy companies in the U.S. and Europe announced joint initiatives to deploy megawatt charging systems integrated with liquid cooled cable technology for electric trucks and buses. These developments aim to reduce charging time significantly and improve fleet operational efficiency, thereby supporting large-scale commercial EV adoption. The initiatives also highlight growing industry alignment toward standardized high-power charging solutions

- Although strong demand supports growth, wider adoption depends on reducing system costs, improving coolant efficiency, and enhancing compatibility with diverse EV platforms. Continued investment in R&D, infrastructure scalability, and standardized charging architectures will be critical for maintaining long-term market expansion

Restraint/Challenge

“High Installation Costs And Technical Complexity”

- The relatively high cost of liquid cooled EV charging cable systems compared to conventional air-cooled alternatives remains a key challenge, limiting widespread adoption among cost-sensitive operators. Advanced cooling mechanisms, specialized materials, and complex engineering designs contribute to elevated production and installation expenses. This creates barriers for small and mid-scale charging infrastructure providers, particularly in developing regions

- Technical complexity in system integration and maintenance also restricts market growth. Liquid cooled cables require precise coolant circulation systems, leak-proof designs, and regular monitoring to ensure safe operation. Any system failure can impact charging efficiency and safety, increasing operational risks for service providers and end users

- Supply chain constraints and limited availability of standardized components further affect market scalability. Dependence on specialized manufacturing processes and certified materials increases lead times and operational costs. This also creates challenges in achieving consistent quality and performance across different charging infrastructure deployments

- For instance, in 2025, several charging network operators in Southeast Asia reported delays in large-scale deployment of liquid cooled charging stations due to high installation costs and limited availability of compatible cooling components. Maintenance complexity and skilled labor requirements further increased operational challenges, slowing down expansion plans in emerging EV markets

- Overcoming these challenges will require cost reduction through manufacturing optimization, improved standardization of charging systems, and development of more efficient cooling technologies. Collaboration between OEMs, infrastructure developers, and technology providers will be essential to enhance affordability, simplify deployment, and support long-term market scalability

Liquid Cooled EV Charging Cable Market Scope

The global liquid cooled EV charging cable market is segmented into six notable segments based on cable power capacity, application, cable length, cable diameter, jacket material, and cooling fluid.

- By Cable Power Capacity

On the basis of cable power capacity, the market is segmented into 300–499 kW, 500–900 kW, and above 900 kW. The 500–900 kW segment held the largest market revenue share in 2025 driven by increasing deployment of high-power fast charging stations across commercial EV infrastructure and fleet charging networks. This range offers an optimal balance between charging speed and thermal efficiency, making it widely suitable for current ultra-fast charging requirements. Growing adoption of electric buses and heavy-duty vehicles is further strengthening demand for mid-to-high power capacity cables. In addition, continuous upgrades in charging station capabilities are supporting segment expansion.

The above 900 kW segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising development of megawatt charging systems for next-generation electric trucks and high-performance EVs. These ultra-high power cables require advanced liquid cooling to manage extreme thermal loads during rapid energy transfer. Increasing investments in megawatt charging corridors and long-distance freight electrification are further accelerating demand. Manufacturers are focusing on enhancing durability and thermal stability for high-load applications. This segment is emerging as a key enabler of future EV infrastructure evolution.

- By Application

On the basis of application, the market is segmented into ultrafast charging and megawatt charging. The ultrafast charging segment held the largest market revenue share in 2025 driven by rapid expansion of high-speed public charging stations and growing consumer demand for reduced EV charging time. This segment is widely adopted in urban charging hubs, highways, and commercial EV stations due to its efficiency and convenience. Increasing penetration of premium electric vehicles requiring fast turnaround charging is further supporting growth. Technological advancements in charging systems are enhancing energy transfer efficiency.

The megawatt charging segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing electrification of heavy-duty transport and logistics fleets. Megawatt charging systems require advanced liquid cooled cables to handle extremely high power loads safely and efficiently. Rising investments in long-haul EV trucking infrastructure and industrial transport electrification are significantly boosting demand. Governments and private players are jointly developing large-scale high-capacity charging corridors. This segment is expected to play a critical role in future high-power EV ecosystems.

- By Cable Length

On the basis of cable length, the market is segmented into below 5 meters, 5–8 meters, and above 8 meters. The 5–8 meters segment held the largest market revenue share in 2025 driven by its optimal balance between flexibility and usability in most charging station configurations. This length is widely used in public charging infrastructure as it supports efficient vehicle connectivity without excessive cable loss or handling difficulty. Increasing deployment of standardized charging stations is further supporting segment dominance. Operators prefer this range for its operational convenience and safety compliance.

The above 8 meters segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for flexible charging setups in large commercial depots and multi-vehicle charging stations. Longer cables provide greater reach and adaptability in complex parking environments. Expansion of fleet charging infrastructure and bus depots is further supporting adoption. Manufacturers are improving lightweight design and thermal efficiency for longer cable systems. This segment is gaining traction in large-scale EV charging installations.

- By Cable Diameter

On the basis of cable diameter, the market is segmented into below 30 mm, 30–50 mm, and above 50 mm. The 30–50 mm segment held the largest market revenue share in 2025 driven by its widespread use in medium to high-power charging systems. This diameter range provides an effective balance between thermal management capacity and cable flexibility. It is widely adopted in fast charging stations due to its durability and efficient heat dissipation properties. Growing installation of high-power EV chargers is further driving demand.

The above 50 mm segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing deployment of ultra-high power charging systems requiring enhanced cooling capacity. Larger diameter cables support higher current flow and improved thermal performance. Rising adoption of megawatt charging systems for heavy-duty EVs is further boosting growth. Manufacturers are focusing on advanced insulation and material innovation to improve performance. This segment is becoming essential for next-generation charging infrastructure.

- By Jacket Material

On the basis of jacket material, the market is segmented into rubber, thermoplastic elastomer, and polyvinyl chloride. The thermoplastic elastomer segment held the largest market revenue share in 2025 driven by its excellent flexibility, durability, and heat resistance properties. It is widely used in high-performance charging cables due to its ability to withstand continuous mechanical stress and thermal load. Increasing demand for long-lasting and lightweight cable solutions is further supporting adoption. This material also offers improved safety and environmental resistance.

The rubber segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its superior insulation properties and high thermal stability in extreme operating conditions. Rubber jackets are increasingly used in heavy-duty and industrial charging applications. Rising demand for rugged and weather-resistant cable systems in outdoor charging stations is supporting growth. Manufacturers are enhancing rubber formulations to improve flexibility and lifespan. This segment is gaining importance in harsh environment applications.

- By Cooling Fluid

On the basis of cooling fluid, the market is segmented into water glycol and others. The water glycol segment held the largest market revenue share in 2025 driven by its high thermal conductivity and efficient heat dissipation performance in high-power charging applications. It is widely used in liquid cooled EV charging cables due to its stability and cost-effectiveness. Increasing deployment of fast charging infrastructure is further driving demand. Its proven reliability makes it the preferred choice for most systems.

The others segment is expected to witness the fastest growth rate from 2026 to 2033, driven by ongoing research into advanced cooling fluids with improved efficiency and environmental compatibility. New formulations are being developed to enhance thermal performance and reduce system maintenance requirements. Growing focus on sustainable and high-efficiency cooling technologies is further supporting adoption. Manufacturers are investing in innovation to improve system performance. This segment is expected to gain traction with next-generation charging systems.

Liquid Cooled EV Charging Cable Market Regional Analysis

- North America dominated the global liquid cooled EV charging cable market in 2025, driven by rapid expansion of ultra-fast EV charging infrastructure, increasing adoption of high-performance electric vehicles, and strong investments in megawatt charging networks

- The region benefits from advanced power grid systems and early deployment of high-capacity charging stations, which require efficient thermal management solutions such as liquid cooled cables. Growing demand for long-distance electric mobility and commercial fleet electrification is further accelerating market penetration

- In addition, strong participation from leading automotive and energy companies is supporting large-scale deployment of high-power charging systems, reinforcing North America’s leadership position in the market

U.S. Liquid Cooled EV Charging Cable Market Insight

The U.S. liquid cooled EV charging cable market captured the largest revenue share in 2025 within North America, driven by rapid electrification of transportation, strong growth in electric vehicle sales, and large-scale deployment of high-speed charging corridors. The country is witnessing significant investments in ultra-fast charging infrastructure to support both passenger EVs and commercial electric fleets. Increasing collaboration between automotive OEMs, energy providers, and charging network operators is further accelerating adoption. In addition, government incentives and funding programs for EV infrastructure expansion are boosting installation of megawatt charging systems, increasing demand for advanced liquid cooled cable solutions.

Europe Liquid Cooled EV Charging Cable Market Insight

The Europe liquid cooled EV charging cable market is expected to witness the fastest growth rate from 2026 to 2033, driven by strict carbon emission regulations, rapid adoption of electric mobility, and strong focus on sustainable transportation infrastructure. Increasing deployment of high-power charging stations along highways and urban centers is supporting demand for liquid cooled cable systems. The region’s emphasis on reducing charging time and improving EV efficiency is further accelerating adoption. In addition, rising investments in green mobility initiatives and cross-border EV charging networks are strengthening market expansion across residential, commercial, and public charging applications.

U.K. Liquid Cooled EV Charging Cable Market Insight

The U.K. liquid cooled EV charging cable market is expected to witness strong growth from 2026 to 2033, driven by increasing adoption of electric vehicles and government initiatives promoting zero-emission transportation. Expanding installation of ultra-fast charging stations across urban areas and highways is supporting demand for advanced liquid cooling technologies. Rising consumer preference for faster and more efficient charging solutions is further boosting market growth. In addition, strong retail and commercial charging infrastructure development is encouraging deployment of high-power EV charging systems integrated with liquid cooled cables.

Germany Liquid Cooled EV Charging Cable Market Insight

The Germany liquid cooled EV charging cable market is expected to witness rapid growth from 2026 to 2033, driven by strong automotive manufacturing leadership, increasing EV adoption, and emphasis on high-performance charging infrastructure. The country is investing heavily in ultra-fast and megawatt charging networks to support both passenger and commercial electric vehicles. Rising focus on energy efficiency and advanced engineering standards is accelerating adoption of liquid cooled cable systems. In addition, integration of renewable energy with EV charging infrastructure is further strengthening demand for efficient thermal management solutions.

Asia-Pacific Liquid Cooled EV Charging Cable Market Insight

The Asia-Pacific liquid cooled EV charging cable market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, expanding electric vehicle adoption, and strong government support for EV infrastructure development in countries such as China, Japan, and India. Increasing deployment of high-power charging stations across urban and highway networks is significantly boosting demand. The region’s strong manufacturing base for EV components is also supporting cost-effective production and wider adoption. In addition, growing investments in smart mobility and electrified transportation systems are further accelerating market expansion.

Japan Liquid Cooled EV Charging Cable Market Insight

The Japan liquid cooled EV charging cable market is expected to witness steady growth from 2026 to 2033 due to the country’s advanced automotive technology ecosystem, strong focus on innovation, and increasing adoption of electric vehicles. Rising demand for high-efficiency charging systems in urban infrastructure is supporting market expansion. Japan’s emphasis on precision engineering and energy-efficient technologies is driving adoption of liquid cooled charging solutions. In addition, integration of EV charging with smart grid systems and renewable energy sources is further enhancing market development.

China Liquid Cooled EV Charging Cable Market Insight

The China liquid cooled EV charging cable market accounted for the largest market revenue share in Asia Pacific in 2025, driven by massive electric vehicle adoption, rapid expansion of charging infrastructure, and strong government support for green mobility initiatives. The country is aggressively deploying ultra-fast and megawatt charging stations across urban and intercity routes, significantly increasing demand for liquid cooled cable systems. Strong domestic manufacturing capabilities and cost-efficient production are further supporting large-scale deployment. In addition, China’s focus on smart transportation networks and electrified logistics is reinforcing its dominance in the regional market.

Liquid Cooled EV Charging Cable Market Share

The Liquid Cooled EV Charging Cable industry is primarily led by well-established companies, including:

- ABB (Switzerland)

• Siemens AG (Germany)

• Schneider Electric SE (France)

• Legrand SA (France)

• Nexans SA (France)

• Prysmian Group (Italy)

• TE Connectivity Ltd. (Switzerland)

• Phoenix Contact GmbH & Co. KG (Germany)

• Delta Electronics Inc. (Taiwan)

• Mitsubishi Electric Corporation (Japan)

• Toshiba Corporation (Japan)

• Sumitomo Electric Industries Ltd. (Japan)

• Hitachi Ltd. (Japan)

• Tesla Inc. (U.S.)

• ChargePoint Inc. (U.S.)

Latest Developments in Global Liquid Cooled EV Charging Cable Market

- In October, 2025, Phoenix Contact, product launch, introduced preassembled M12 push-pull network cables designed to support 10 Gbps Ethernet transmission using CAT6A X-coded architecture, integrated with 360° shielding technology. This development aims to enhance signal integrity and reduce electromagnetic interference in harsh industrial environments. The innovation strengthens high-speed industrial connectivity performance and supports reliable data transmission in automation systems. It is expected to improve operational efficiency in industrial communication networks and expand adoption in high-performance connectivity applications

- In September, 2025, Autel Energy, product integration, incorporated Phoenix Contact’s 1,000 A liquid cooled CCS2 cable and connector into its MaxiCharger DT1000 ultra-high-power EV charging system. This integration is designed to enhance high-power charging efficiency and ensure stable thermal management during ultra-fast charging operations. The development improves charging safety and reduces overheating risks in high-capacity EV infrastructure. It is expected to strengthen adoption of megawatt-level charging systems and accelerate deployment of next-generation EV fast charging networks

- In August, 2025, SINBON, capacity expansion, announced investment of approximately USD 8.5 million to expand its U.S. manufacturing operations with a new facility in Ohio. The expansion is aimed at increasing production capacity for cable assemblies and connectivity solutions used in automotive, industrial robotics, and renewable energy applications. This move strengthens localized supply chains and reduces dependency on overseas production. It is expected to enhance delivery efficiency and support growing demand for EV-related cable assembly solutions in North America

- In August, 2025, SINBON Electronics, facility expansion, inaugurated a new manufacturing plant in Mexico with an investment of around USD 27 million to expand production of cable assemblies and interconnection systems. The facility is focused on supporting automotive electrification and EV charging infrastructure development across regional markets. This expansion enhances production scalability and improves supply chain responsiveness for high-current cable systems. It is expected to strengthen regional manufacturing capabilities and support increasing demand for EV infrastructure components

- In May, 2025, Phoenix Contact, product development, launched its second-generation liquid cooled CHARX connect professional CCS charging cables capable of delivering up to 1,000 kW in boost mode and 800 kW in continuous operation. The solution is designed to support ultra-fast DC charging for electric vehicles and heavy-duty commercial EVs. This advancement significantly improves charging speed and thermal stability in high-power applications. It is expected to accelerate deployment of megawatt charging infrastructure and enhance performance efficiency in next-generation EV charging networks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.