Global Liquid Packaging Market

Market Size in USD Billion

USD

391.20 Billion

USD

572.72 Billion

2024

2032

USD

391.20 Billion

USD

572.72 Billion

2024

2032

| 2025 - 2032 | |

| USD 391.20 Billion | |

| USD 572.72 Billion | |

| % | |

|

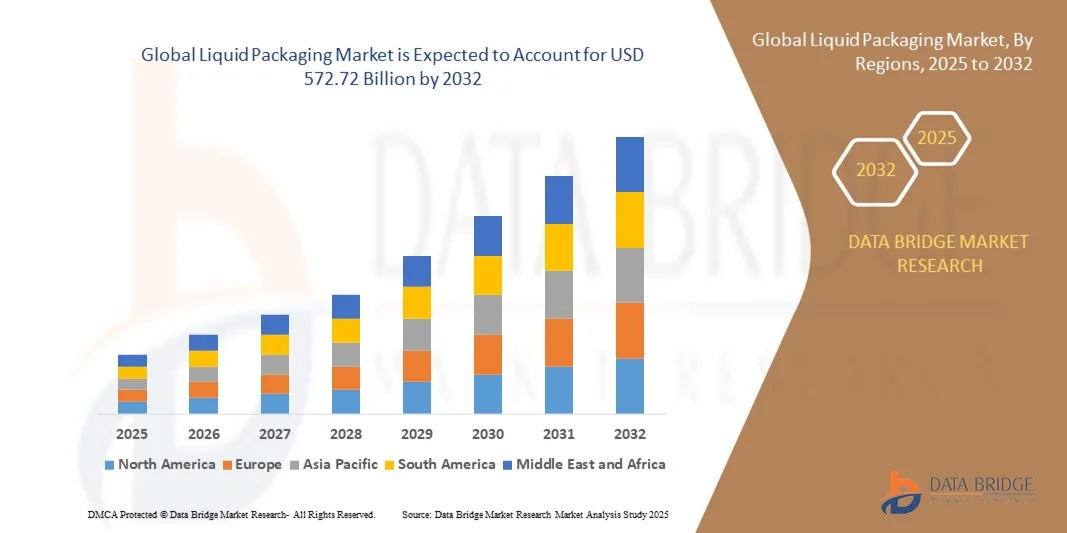

Global Liquid Packaging Market Size

- The global Liquid Packaging Market size was valued at USD 391.20 billion in 2024 and is projected to reach USD 572.72 billion by 2032, growing at a CAGR of 4.88% during the forecast period.

- The market expansion is primarily driven by increasing demand for sustainable and innovative packaging solutions across food, beverage, and pharmaceutical industries, coupled with advancements in eco-friendly materials and technologies.

- Additionally, rising consumer preference for convenience, safety, and extended shelf life is propelling the adoption of liquid packaging formats, further accelerating market growth and encouraging continuous product development in this sector.

Global Liquid Packaging Market Analysis

- Liquid packaging solutions, designed to safely contain and preserve liquids across various industries, are becoming essential due to their ability to enhance product shelf life, improve convenience, and support sustainability efforts in both commercial and residential sectors.

- The growing demand for liquid packaging is primarily driven by increasing consumer preference for eco-friendly materials, regulatory support for sustainable packaging, and technological advancements in lightweight and flexible packaging formats.

- Asia-Pacific dominated the Global Liquid Packaging Market with the largest revenue share of 32.5% in 2024, attributed to high consumer awareness, stringent regulations on packaging waste, and the presence of major packaging manufacturers investing in innovative and recyclable liquid packaging solutions.

- North America is expected to be the fastest-growing region in the Global Liquid Packaging Market during the forecast period, fueled by rapid urbanization, rising disposable incomes, and expanding food and beverage and pharmaceutical industries demanding efficient liquid packaging.

- The plastics segment dominated the market with the largest revenue share of 48.6% in 2024, due to its lightweight nature, cost-efficiency, and durability.

Report Scope and Global Liquid Packaging Market Segmentation

|

Attributes |

Liquid Packaging Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Liquid Packaging Market Trends

Sustainability and Innovation Driving Next-Gen Liquid Packaging

- A significant and accelerating trend in the Global Liquid Packaging Market is the rapid adoption of sustainable materials and innovative packaging technologies aimed at reducing environmental impact while maintaining product integrity and consumer convenience. Companies are increasingly investing in renewable, recyclable, and biodegradable materials to align with global environmental goals and consumer preferences.

- For instance, Tetra Pak has developed plant-based cartons using paperboard and sugarcane-derived polymers, offering fully renewable packaging solutions. Similarly, Elopak’s Natural Brown Board cartons reduce the use of bleaching chemicals and feature a visibly natural finish, appealing to environmentally conscious consumers.

- Technological innovation is also playing a critical role, with advancements such as aseptic packaging, intelligent tracking systems, and lightweight structures that reduce carbon footprint while extending shelf life. These innovations enhance logistical efficiency and product safety, particularly in the food and beverage and pharmaceutical sectors.

- The integration of smart packaging features—such as QR codes and sensors—enables greater transparency and traceability throughout the supply chain. This allows consumers and manufacturers to monitor product quality, authenticity, and usage data, aligning with the rising demand for connected, data-driven packaging solutions.

- Companies like SIG Combibloc and Amcor are leading the way by introducing high-performance liquid packaging that combines sustainability with digital functionality, including recyclable multi-layer structures and smart labeling for interactive customer engagement.

- The demand for liquid packaging that is both eco-conscious and technologically advanced is growing rapidly across global markets, driven by evolving regulatory frameworks, heightened consumer awareness, and brand commitments to circular economy practices.

Global Liquid Packaging Market Dynamics

Driver

Growing Demand Due to Sustainability Regulations and Expanding End-Use Applications

-

The increasing emphasis on environmental sustainability, combined with the expanding use of liquid packaging in food, beverage, pharmaceutical, and personal care industries, is a major driver of the Global Liquid Packaging Market’s growth. Governments worldwide are implementing stricter regulations on single-use plastics and encouraging the use of recyclable or biodegradable packaging materials, accelerating the shift toward sustainable liquid packaging.

- For instance, in 2024, Tetra Pak announced its commitment to develop a fully renewable and recyclable aseptic carton using plant-based polymers and responsibly sourced paperboard. Such initiatives are reinforcing the industry’s move toward low-impact packaging and attracting eco-conscious brands and consumers.

- Consumers are also increasingly prioritizing convenience, hygiene, and portability—especially in the post-pandemic era—which is driving demand for lightweight, resealable, and tamper-evident liquid packaging. These features are critical for on-the-go consumption, extended shelf life, and maintaining product integrity across the supply chain.

- Furthermore, the growing consumption of packaged beverages, dairy products, and liquid pharmaceuticals in emerging markets is creating new opportunities for liquid packaging manufacturers. Innovations such as aseptic packaging, spouted pouches, and smart labeling technologies are enabling brands to differentiate their products while enhancing user experience and supply chain efficiency.

- The rise of e-commerce and direct-to-consumer delivery models has further amplified the need for durable and protective liquid packaging solutions that can withstand transport conditions and minimize leakage or damage, making liquid packaging a vital component of modern distribution systems.

Restraint/Challenge

High Material Costs and Recycling Complexities

- Despite strong market growth, the Global Liquid Packaging Market faces challenges related to the high costs of advanced, sustainable packaging materials and the complexities involved in recycling multi-layered packaging. Many liquid packaging solutions, such as aseptic cartons or laminated pouches, contain layers of paper, plastic, and aluminum that are difficult to separate and recycle efficiently.

- For Instance, while carton packages are often marketed as recyclable, the lack of adequate recycling infrastructure in many regions—especially in developing countries—limits their end-of-life processing, contributing to landfill waste. This mismatch between recyclability claims and actual recycling capabilities can lead to consumer skepticism and regulatory scrutiny.

- Moreover, the adoption of bio-based or compostable materials often involves higher manufacturing costs, which can impact pricing competitiveness for producers, particularly in cost-sensitive markets. Small and medium-sized brands may find it challenging to adopt premium sustainable packaging solutions without significantly increasing product prices.

- Companies such as SIG Combibloc and Amcor are working to address these challenges through the development of mono-material packaging and investment in closed-loop recycling initiatives. However, broader industry collaboration and government support will be essential to make sustainable liquid packaging scalable and affordable.

- Overcoming these obstacles through technological innovation, enhanced recycling systems, and cost-reduction strategies will be key to ensuring long-term growth and consumer acceptance in the liquid packaging sector.

Global Liquid Packaging Market Scope

The liquid packaging market is segmented on the basis of raw material, technique, resin, packaging type, and end-use.

- By Raw Material

On the basis of raw material, the Global Liquid Packaging Market is segmented into Plastics, Paper, Metal, and Glass. The plastics segment dominated the market with the largest revenue share of 48.6% in 2024, due to its lightweight nature, cost-efficiency, and durability. Plastic packaging provides excellent barrier properties against moisture and oxygen, making it ideal for beverages, dairy products, and liquid personal care items. It also offers versatility across both flexible and rigid formats.

The paper segment is expected to witness the fastest CAGR from 2025 to 2032, driven by growing environmental awareness, pressure to reduce plastic waste, and strong demand for recyclable or biodegradable alternatives. Innovations in coated paperboard and fiber-based liquid cartons are further accelerating adoption across juice, milk, and plant-based beverage packaging. Government bans on single-use plastics and circular economy initiatives are also playing a key role in expanding this segment.

- By Technique

On the basis of technique, the Global Liquid Packaging Market is segmented into Aseptic, Intelligent, Blow Molding, Vacuum, Form Fill Seal, and Modified Atmosphere. The aseptic segment held the largest revenue share of 41.3% in 2024, driven by its ability to preserve perishable liquids without refrigeration and extend shelf life. It is widely used in packaging dairy products, juices, and liquid pharmaceuticals, especially in markets with underdeveloped cold chain infrastructure.

The intelligent packaging segment is projected to witness the fastest growth from 2025 to 2032, fueled by advancements in connected technologies, smart labels, and traceability features. This technique enables real-time quality monitoring, anti-counterfeit protection, and consumer engagement via QR codes or NFC. Increasing demand for data-driven supply chains and product transparency in sectors such as pharmaceuticals and premium beverages is accelerating the adoption of intelligent packaging solutions.

- By Resin

On the basis of resin, the Global Liquid Packaging Market is segmented into Polyethylene (P.E.), Polypropylene (P.P.), Polyethylene Terephthalate (P.E.T.), and Others. The P.E. segment dominated the market in 2024 with a market share of 46.2%, driven by its cost-effectiveness, flexibility, and excellent heat-sealing and moisture barrier properties. PE is widely used in films, pouches, and bag-in-box formats for beverages, industrial fluids, and household liquids.

The P.E.T. segment is expected to grow at the fastest CAGR from 2025 to 2032, owing to its strength, transparency, and recyclability. PET is the preferred resin for rigid liquid packaging, especially in bottled water, soft drinks, and edible oil. Its compatibility with deposit return schemes and closed-loop recycling initiatives is further boosting demand. As consumer preference shifts toward sustainable and clear packaging, PET adoption is poised to accelerate across multiple industries.

- By Packaging Type

On the basis of packaging type, the Global Liquid Packaging Market is segmented into Flexible Liquid Packaging and Rigid Liquid Packaging. The rigid segment dominated the market in 2024 with a market share of 58.9%, attributed to its high durability, tamper resistance, and ability to protect contents during transportation and storage. Rigid packaging formats such as cartons, bottles, and jugs are commonly used in water, milk, and industrial liquids.

The flexible packaging segment is expected to witness the fastest CAGR from 2025 to 2032, driven by increasing demand for lightweight, space-saving, and eco-friendly packaging options. Formats such as stand-up pouches, spouted bags, and bag-in-box systems are gaining popularity for their convenience and lower environmental footprint. Flexible packaging also allows for efficient storage and is favored in e-commerce and portable, single-serve liquid applications.

- By End-Use Industry

On the basis of end-use industry, the Global Liquid Packaging Market is segmented into Food and Beverages, Non-Food, and Industrial. The food and beverages segment dominated the market in 2024 with the largest revenue share of 64.7%, driven by high consumption of packaged drinks, dairy, sauces, and soups. The sector’s reliance on both aseptic and refrigerated packaging formats sustains demand across rigid and flexible options. The growing popularity of ready-to-drink products and health-based beverages continues to drive innovation in this segment.

The non-food segment is projected to experience the fastest CAGR from 2025 to 2032, fueled by increased demand for hygienic and durable packaging in cosmetics, personal care, and pharmaceutical liquids. Rising consumer focus on wellness, coupled with stricter hygiene and shelf-life requirements, is prompting the adoption of specialized liquid packaging with features like tamper-evidence, UV protection, and enhanced product dosing or dispensing.

Global Liquid Packaging Market Regional Analysis

- Asia-Pacific dominated the Global Liquid Packaging Market with the largest revenue share of 32.5% in 2024, driven by strong demand from the food and beverage sector, widespread adoption of sustainable packaging practices, and the presence of leading industry players.

- Consumers and manufacturers in the region increasingly favor eco-friendly and recyclable packaging materials, such as paper-based cartons and PET bottles, in response to growing environmental awareness and regulatory pressure to reduce plastic waste.

- This growth is further supported by high levels of packaged product consumption, well-established recycling infrastructure, and ongoing investments in advanced packaging technologies. These factors collectively position North America as a key hub for innovation and implementation of liquid packaging solutions across industries including dairy, juice, pharmaceutical, and household liquids.

U.S. Liquid Packaging Market Insight

The U.S. liquid packaging market captured the largest revenue share 78% in North America in 2024, driven by rising demand for convenience-based products and sustainable packaging solutions across the food & beverage, pharmaceutical, and personal care sectors. The shift toward eco-friendly materials and increasing regulations around single-use plastics are pushing manufacturers to innovate with recyclable and biodegradable options. Additionally, the popularity of ready-to-drink beverages, coupled with advancements in aseptic and flexible packaging technologies, is bolstering market growth. E-commerce expansion and consumer preference for portable, spill-proof packaging are further accelerating demand.

Europe Liquid Packaging Market Insight

The Europe liquid packaging market is projected to expand at a substantial CAGR throughout the forecast period, primarily supported by strong sustainability mandates and a highly regulated packaging landscape. European consumers are increasingly inclined toward environmentally responsible products, leading to a surge in demand for recyclable, lightweight, and biodegradable liquid packaging formats. The beverage and dairy sectors are key contributors, while pharmaceutical applications continue to gain momentum. Liquid packaging is being integrated into both existing product lines and new product innovations, supported by active investments in material science and packaging automation.

U.K. Liquid Packaging Market Insight

The U.K. liquid packaging market is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the rising adoption of sustainable packaging practices and growing consumer awareness of environmental issues. The beverage sector, particularly bottled water, juices, and plant-based drinks, is a primary driver of demand. Innovations in smart and tamper-evident packaging, as well as the shift toward paper-based and compostable materials, are shaping the future of the market. The U.K.'s strong e-commerce infrastructure and focus on minimizing carbon footprint are expected to further stimulate market development.

Germany Liquid Packaging Market Insight

The Germany liquid packaging market is expected to expand at a considerable CAGR during the forecast period, driven by the country’s advanced manufacturing capabilities, stringent environmental regulations, and high consumer demand for sustainable solutions. Germany’s strong focus on waste reduction and recycling is promoting the adoption of reusable and eco-friendly packaging formats across industries. The food and pharmaceutical sectors remain prominent end-users, with increasing integration of innovative packaging technologies such as smart sensors, multilayer barriers, and refill systems. Germany’s leadership in sustainability is setting benchmarks for packaging innovation across Europe.

Asia-Pacific Liquid Packaging Market Insight

The Asia-Pacific liquid packaging market is poised to grow at the fastest CAGR of 24% during the forecast period of 2025 to 2032, supported by rapid urbanization, a booming middle-class population, and significant growth in the food and beverage industry. Countries such as China, India, and Indonesia are witnessing a rising preference for packaged and processed beverages, dairy products, and liquid detergents, driving substantial demand for flexible and rigid packaging formats. Government initiatives promoting clean and sustainable packaging, along with increased local production capabilities, are improving both accessibility and affordability of advanced liquid packaging solutions across the region.

Japan Liquid Packaging Market Insight

The Japan liquid packaging market is gaining traction due to its strong culture of convenience, high technological adoption, and focus on sustainable living. Japan's aging population and urban lifestyle are spurring demand for lightweight, easy-to-open, and resealable packaging formats, particularly in personal care and food products. The market is also influenced by strong regulatory standards around waste management and recycling. Advanced features such as anti-counterfeit labels, smart packaging, and barrier coatings are becoming increasingly common, as manufacturers prioritize both functionality and eco-conscious design.

China Liquid Packaging Market Insight

The China liquid packaging market accounted for the largest market revenue share in Asia Pacific in 2024, fueled by robust growth in the food & beverage and pharmaceutical industries. The country’s rapid urbanization, growing e-commerce penetration, and expanding middle class are significantly contributing to demand for innovative, affordable, and sustainable packaging solutions. Domestic manufacturers are investing heavily in automation and material development to meet both domestic and export demands. Additionally, China’s push toward sustainable packaging, in line with its national plastic reduction policies, is catalyzing innovation in biodegradable and recyclable liquid packaging formats.

Global Liquid Packaging Market Share

The Liquid Packaging industry is primarily led by well-established companies, including:

- Tetra Pak International S.A. (Switzerland)

- Stora Enso Oyj (Finland)

- Nippon Paper Industries Co., Ltd. (Japan)

- Smurfit Kappa Group plc (Ireland)

- WestRock Company (U.S.)

- Greatview Aseptic Packaging Co., Ltd. (China)

- Mondi Group (U.K.)

- Elopak AS (Norway)

- SIG Combibloc Group AG (Switzerland)

- Billerud AB (Sweden)

- International Paper Company (U.S.)

- Asia Pulp & Paper Group (Indonesia)

- Liquid Packaging Solutions Inc. (U.S.)

- UFlex Ltd. (India)

- Amcor plc (Australia)

What are the Recent Developments in Global Liquid Packaging Market?

- In May 2023, Tetra Pak launched a next-generation plant-based aseptic packaging solution made from over 80% renewable materials. This innovation is part of the company’s sustainability strategy to reduce carbon emissions and improve recyclability. Designed for dairy and juice applications, the packaging incorporates responsibly sourced paperboard and plant-based polymers, helping brands meet growing consumer demand for eco-conscious products. This move strengthens Tetra Pak’s leadership in sustainable packaging within the Global Liquid Packaging Market.

- In April 2023, SIG Combibloc announced the expansion of its fully recyclable aseptic carton product line with a new tethered cap design, in line with upcoming EU regulations. This innovation ensures that caps remain attached to the packaging after opening, reducing plastic litter and enhancing recycling rates. The solution was co-developed with leading beverage manufacturers in Europe and positions SIG at the forefront of regulatory-compliant, environmentally friendly packaging solutions.

- In March 2023, Elopak partnered with Blue Ocean Closures (Sweden) to develop a paper-based closure system for liquid cartons. This breakthrough aims to replace plastic caps with bio-based, recyclable alternatives, further improving the sustainability profile of paperboard liquid packaging. The initiative reflects Elopak’s commitment to eliminating unnecessary plastic and responding to customer demands for plastic-free, fully recyclable packaging formats.

- In February 2023, Amcor plc unveiled a new range of high-barrier flexible liquid packaging designed for premium beverages, condiments, and personal care liquids. The pouches offer extended shelf life, reduced material weight, and improved functionality with features such as spouts and resealable zippers. This innovation supports Amcor’s pledge to make all its packaging recyclable or reusable by 2025, aligning with the circular economy goals driving the global market.

- In January 2023, Mondi Group introduced its FlexiBag Recyclable, a mono-material stand-up pouch for liquid applications, developed in collaboration with a leading European dairy brand. The pouch is made from polyethylene and is fully recyclable in existing waste streams. Designed for milk and drinkable yogurt, it offers excellent shelf stability, reduced packaging weight, and a lower carbon footprint compared to traditional rigid alternatives, reinforcing Mondi’s position in sustainable flexible liquid packaging.

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Liquid Packaging Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Liquid Packaging Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Liquid Packaging Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.