Global Liquid Waterborne Printing Inks Market

Market Size in USD Billion

USD

4.62 Billion

USD

7.09 Billion

2024

2032

USD

4.62 Billion

USD

7.09 Billion

2024

2032

| 2025 - 2032 | |

| USD 4.62 Billion | |

| USD 7.09 Billion | |

| % | |

|

Liquid Waterborne Printing Inks Market Size

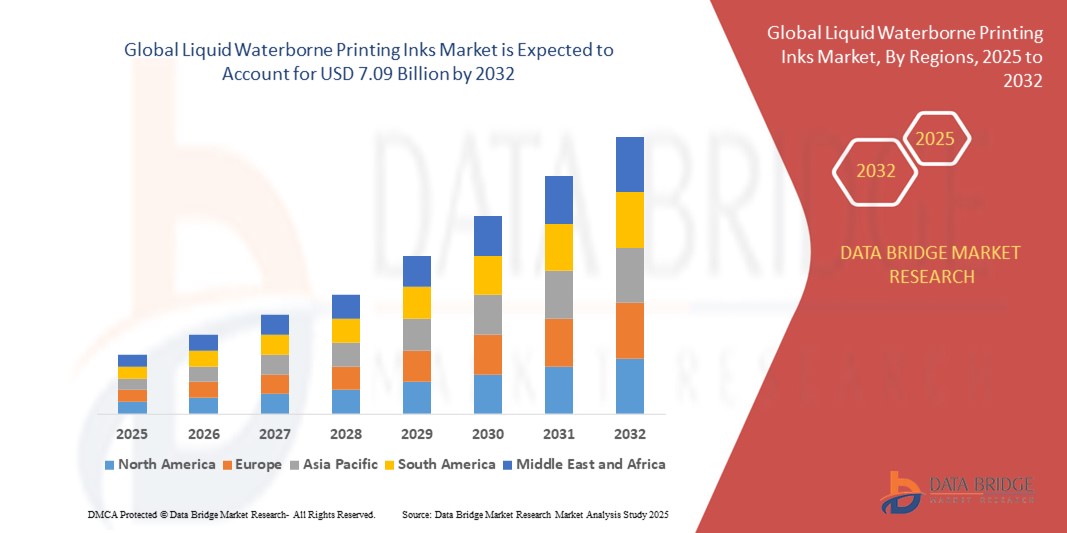

- The global liquid waterborne printing inks market size was valued at USD 4.62 billion in 2024 and is expected to reach USD 7.09 billion by 2032, at a CAGR of 5.50% during the forecast period

- The market growth is largely fuelled by the increasing demand for eco-friendly and low-VOC ink formulations across packaging, publishing, and commercial printing applications, alongside stricter environmental regulations driving the transition from solvent-based to waterborne technologies

- Growth in e-commerce and retail-ready packaging is further accelerating the demand for waterborne inks, as brands seek high-quality, sustainable print solutions for corrugated boxes and labels used in shipping and shelf display

Liquid Waterborne Printing Inks Market Analysis

- Rising consumer awareness about sustainable packaging and regulatory restrictions on solvent emissions are pushing converters and brand owners to adopt waterborne inks, especially in food and beverage and personal care sectors

- The shift toward flexible and corrugated packaging formats is boosting usage of liquid waterborne inks, particularly in flexographic and gravure printing processes due to their compatibility with paper, board, and flexible substrates

- North America dominated the liquid waterborne printing inks market with the largest revenue share of 34.6% in 2024, driven by increasing demand for sustainable and low-emission printing solutions, particularly in the packaging and commercial printing sectors

- Asia-Pacific region is expected to witness the highest growth rate in the global liquid waterborne printing inks market, driven by expanding manufacturing bases, growing middle-class population spurring consumption of packaged goods, and rising awareness about environmental impacts of solvent-based inks.

- The flexography inks segment accounted for the largest market revenue share in 2024, attributed to its widespread use in packaging applications due to high-speed printing capabilities, quick drying nature, and adaptability to various substrates. Flexographic printing is particularly favored for food packaging and labeling, where low-VOC, water-based ink formulations are preferred for regulatory compliance and safety. This segment is also driven by the increasing demand for sustainable and cost-effective solutions across the printing industry

Report Scope and Liquid Waterborne Printing Inks Market Segmentation

|

Attributes |

Liquid Waterborne Printing Inks Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

• Expansion of Eco-Friendly Packaging Solutions Using Sustainable Inks • Rising Demand from Emerging Economies for Cost-Effective and Non-Toxic Printing Inks |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Liquid Waterborne Printing Inks Market Trends

Shift Toward Sustainable and Low-VOC Printing Solutions

- The global printing industry is witnessing a notable shift toward sustainable solutions, with liquid waterborne inks gaining traction due to their low levels of volatile organic compounds (VOCs). These inks reduce environmental impact and enhance worker safety, making them increasingly preferred across packaging and commercial printing sectors

- Stringent government regulations regarding emissions and increasing consumer preference for green products are influencing printers and manufacturers to adopt water-based alternatives. This transition is accelerating innovation in resin technology and pigment dispersion systems that ensure high-quality performance and print durability

- Brand owners are also contributing to this trend by demanding sustainable printing options for their labels and packaging. This is particularly evident in the food and beverage sector, where compliance with environmental and safety standards is essential

- For instance, in 2023, multiple European packaging converters shifted to waterborne inks for flexible packaging to comply with the European Union’s tightening emission norms, while maintaining visual appeal and functionality

- The trend is expected to grow further with the expansion of circular economy initiatives and extended producer responsibility programs. Industry players must continue investing in product development and scalability to address performance consistency, drying efficiency, and compatibility with diverse substrates

Liquid Waterborne Printing Inks Market Dynamics

Driver

Increasing Demand for Eco-Friendly and Regulatory-Compliant Printing Solutions

• The global emphasis on sustainability and regulatory compliance is a significant driver for the adoption of liquid waterborne inks. These inks, formulated with water as a primary solvent, release minimal VOCs and are considered safer for both humans and the environment. As regulatory bodies impose stricter emission and waste management standards, particularly in North America and Europe, waterborne inks are becoming the go-to solution for compliant printing practices

• Industries such as food packaging, pharmaceuticals, and personal care are prioritizing environmentally responsible labeling and branding strategies. Waterborne inks offer an ideal balance between print quality and sustainability, especially on substrates used for flexible packaging, corrugated boxes, and paperboard

• The driver is further amplified by the growing corporate focus on ESG (Environmental, Social, and Governance) performance. Print service providers and end-use brands are aligning their operations with sustainability goals, thus increasing the demand for non-toxic and recyclable materials, including liquid waterborne printing inks

• For instance, in 2024, a major North American retailer partnered with its private-label suppliers to transition all product labels to waterborne inks as part of its sustainability roadmap. This initiative not only reduced carbon footprint but also improved workplace safety in its supply chain

• Despite the benefits, manufacturers must ensure consistency in ink performance across printing platforms and substrates, while also improving drying times and print throughput to maintain competitiveness

Restraint/Challenge

Performance Limitations and Substrate Compatibility Issues

• Although liquid waterborne printing inks are environmentally favorable, they face certain technical limitations that hinder their full-scale adoption. One of the key challenges is slower drying time compared to solvent-based inks, especially in high-speed industrial printing applications. This can impact productivity and increase operational costs unless offset by specialized drying equipment

• These inks also struggle with substrate compatibility, particularly on non-porous materials such as certain plastics and foils. Achieving strong adhesion, color vibrancy, and resistance to abrasion or moisture remains difficult on these surfaces without additional primer coatings or surface treatments

• Small and medium printing firms often lack the infrastructure or budget to modify printing equipment or add drying systems to accommodate water-based inks. This slows market penetration, especially in price-sensitive regions where capital expenditure is tightly controlled

• For instance, in 2023, several flexible packaging converters in Southeast Asia reported ink smudging and lower print definition while using waterborne inks on polyethylene substrates, forcing them to revert temporarily to solvent-based alternatives

• To overcome these challenges, manufacturers must innovate around resin formulation and drying technology, offer technical support for press adjustments, and develop hybrid ink systems that combine the benefits of waterborne formulations with improved substrate versatility and drying efficiency

Liquid Waterborne Printing Inks Market Scope

The liquid waterborne printing inks market is segmented on the basis of type, substrate, and application.

- By Type

On the basis of type, the liquid waterborne printing inks market is segmented into flexography inks and gravure inks. The flexography inks segment accounted for the largest market revenue share in 2024, attributed to its widespread use in packaging applications due to high-speed printing capabilities, quick drying nature, and adaptability to various substrates. Flexographic printing is particularly favored for food packaging and labeling, where low-VOC, water-based ink formulations are preferred for regulatory compliance and safety. This segment is also driven by the increasing demand for sustainable and cost-effective solutions across the printing industry.

The gravure inks segment is expected to witness the fastest growth rate from 2025 to 2032, supported by their strong image reproduction, sharp detailing, and suitability for long-run, high-quality printing tasks. The growth is further propelled by rising use in decorative printing and flexible packaging, where brand owners seek vibrant and consistent results along with improved sustainability features provided by waterborne formulations.

- By Substrate

On the basis of substrate, the liquid waterborne printing inks market is segmented into films and paper and paperboard. The paper and paperboard segment dominated the market in 2024 due to the growing use of sustainable packaging materials and increasing applications in corrugated boxes, cartons, and labels. Waterborne inks offer strong adhesion and print clarity on porous surfaces, making them an ideal match for paper-based substrates. Rising environmental awareness and the shift away from plastic packaging are also contributing to this segment’s dominance.

The films segment is expected to witness the fastest growth rate from 2025 to 2032, driven by demand in flexible packaging formats. As converters adopt surface treatments and primer technologies to enhance ink adherence, the use of waterborne inks on film substrates such as polyethylene, polypropylene, and polyester is expanding, especially in food and personal care packaging.

- By Application

On the basis of application, the market is segmented into industrial, construction, and manufacturing. The industrial segment led the market in 2024, bolstered by extensive use in product labeling, signage, and large-scale printing operations that emphasize eco-compliance and safety. Waterborne inks are being widely adopted in this segment due to their low emissions, safer handling, and compatibility with automated printing lines.

The construction and manufacturing segments is expected to witness the fastest growth rate from 2025 to 2032, as companies seek environmentally friendly alternatives for marking, labeling, and instructional print on a wide range of building materials, tools, and equipment. Waterborne formulations are gaining preference for their durability, minimal odor, and reduced fire hazard, aligning with evolving workplace safety standards.

Liquid Waterborne Printing Inks Market Regional Analysis

• North America dominated the liquid waterborne printing inks market with the largest revenue share of 34.6% in 2024, driven by increasing demand for sustainable and low-emission printing solutions, particularly in the packaging and commercial printing sectors

• The region benefits from stringent environmental regulations encouraging the shift toward water-based formulations and the presence of established printing ink manufacturers. Growth is further supported by rising awareness of eco-friendly alternatives and the expansion of flexographic and gravure printing across retail and industrial applications

U.S. Liquid Waterborne Printing Inks Market Insight

The U.S. liquid waterborne printing inks market captured the largest share within North America in 2024, fueled by rising investment in sustainable packaging and advanced printing technologies. The country’s well-established food and beverage, pharmaceuticals, and e-commerce industries continue to drive demand for high-performance, water-based inks that comply with safety and sustainability standards. Moreover, increasing consumer preference for recyclable and biodegradable packaging materials is encouraging manufacturers to adopt waterborne formulations for labels, wrappers, and corrugated boxes

Europe Liquid Waterborne Printing Inks Market Insight

The Europe liquid waterborne printing inks market is expected to witness the fastest growth rate from 2025 to 2032, driven by regulatory policies promoting the reduction of volatile organic compounds (VOCs) and the adoption of green printing practices. The growth is reinforced by the widespread usage of flexographic and gravure printing across the food, cosmetics, and pharmaceuticals industries. Demand is further strengthened by initiatives supporting the circular economy, which prioritize water-based inks in packaging production and printing materials

Germany Liquid Waterborne Printing Inks Market Insight

The Germany liquid waterborne printing inks market is expected to witness the fastest growth rate from 2025 to 2032, propelled by a strong industrial base and robust packaging demand across various sectors. With Germany’s stringent environmental compliance framework and proactive sustainability goals, the shift to low-VOC, water-based inks is rapidly accelerating. The country's leadership in packaging innovation and printing technologies also enhances adoption in both consumer and industrial packaging segments

U.K. Liquid Waterborne Printing Inks Market Insight

The U.K. liquid waterborne printing inks market is expected to witness the fastest growth rate from 2025 to 2032, driven by growing environmental awareness and regulatory pressure to adopt low-emission printing alternatives. The market benefits from the increasing use of digital and flexographic printing for retail packaging, labeling, and promotional materials. Local manufacturers are also embracing water-based formulations to meet eco-labeling and recyclability requirements

Asia-Pacific Liquid Waterborne Printing Inks Market Insight

The Asia-Pacific liquid waterborne printing inks market is expected to witness the fastest growth rate from 2025 to 2032, supported by rising industrialization, growing packaging needs, and government-led environmental initiatives in countries such as China, India, and Japan. As manufacturers increasingly move toward sustainable operations, waterborne inks are gaining favor in flexible packaging, food-grade labels, and paper-based substrates. The region also benefits from cost-effective production capabilities and the expanding retail and e-commerce ecosystem

China Liquid Waterborne Printing Inks Market Insight

The China liquid waterborne printing inks market accounted for the largest revenue share in Asia-Pacific in 2024, driven by the country’s expansive manufacturing and packaging industries. The shift towards eco-friendly inks is gaining momentum due to national pollution control policies and increasing global pressure for sustainable exports. Domestic ink manufacturers are scaling production of high-quality waterborne solutions to serve the growing demand from food packaging, printing, and industrial sectors

Japan Liquid Waterborne Printing Inks Market Insight

The Japan liquid waterborne printing inks market is expected to witness the fastest growth rate from 2025 to 2032, supported by the country’s focus on environmental compliance and sustainable innovation. Japanese companies are investing in advanced ink formulations to align with international standards and minimize VOC emissions. The market is also benefiting from a mature printing industry and demand for premium packaging solutions across electronics, personal care, and food products. The integration of smart and eco-conscious packaging design is further contributing to the rising use of waterborne inks across multiple applications

Liquid Waterborne Printing Inks Market Share

The Liquid Waterborne Printing Inks industry is primarily led by well-established companies, including:

- DIC CORPORATION (Japan)

- Flint Group (Luxembourg)

- TOYO INK SC HOLDINGS CO., LTD. (Japan)

- Sakata Inx (India) Private Limited (India)

- Siegwerk Druckfarben AG & Co. KGaA (Germany)

- Hubergroup India Private Limited (India)

- T&K TOKA Corporation (Japan)

- Altana (Germany)

- TOKYO PRINTING INK MFG CO., LTD. (Japan)

- Wikoff Color Corporation (U.S.)

- Royal Dutch Printing Ink Factories Van Son (Netherlands)

- Dainichiseika Color & Chemicals Mfg. Co., Ltd. (Japan)

- Zeller+Gmelin (Germany)

- Sun Chemical (U.S.)

- Alden & Ott Printing Inks Co (U.S.)

- Gardiner Colours Limited (U.K.)

- MALLARD INK CO AND OFFSET BLANKET CO., INC. (U.S.)

- INX International Ink Co. (U.S.)

- INKNOVATORS (India)

- Avreon Chemicals India Private Limited (India)

Latest Developments in Global Liquid Waterborne Printing Inks Market

- In May 2024, Marabu is raising the bar in decorative inkjet printing on glass with its new high-performance digital printing ink, UltraJet DUV-CP. This innovative technology delivers superior print quality at twice the speed of previous models while reducing overall ink consumption. The UltraJet DUV-CP allows for the creation of unique effects on glass, plastic, and metal containers with ink film thicknesses of up to 3 mm

- In June 2021, Siegwerk, a leading global provider of printing inks and coatings for packaging and labels, introduced UniNATURE, a new generation of sustainable water-based inks for paper and board applications. This innovative product line is made from renewable and natural components, offering an eco-friendly alternative to traditional inks. UniNATURE enhances the recyclability of paper and board packaging while contributing to a reduction in microplastics found in inks

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Liquid Waterborne Printing Inks Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Liquid Waterborne Printing Inks Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Liquid Waterborne Printing Inks Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.